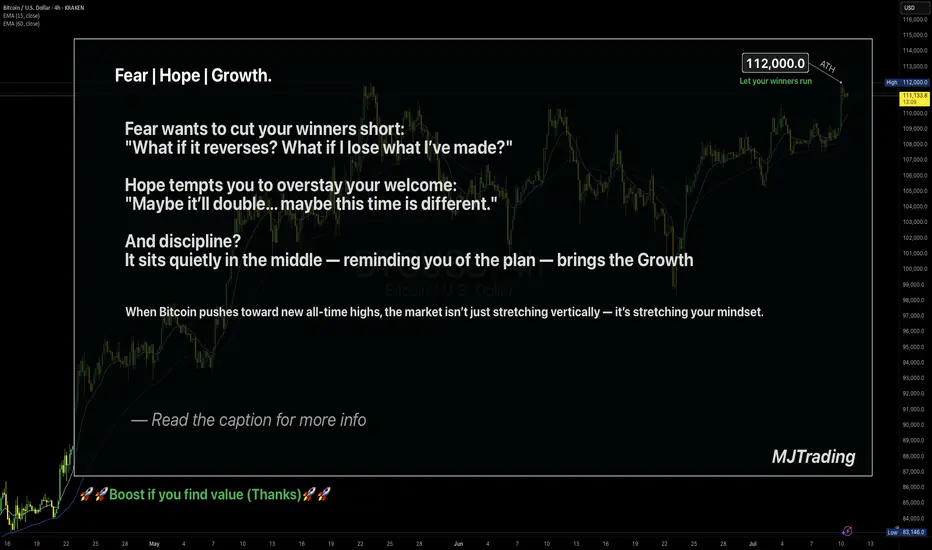

Let your winners run🧠 Fear | Hope | Growth – When Trading Meets Emotion

The message on the chart isn't just poetic — it's real psychology.

🔹 Fear wants to cut your winners short.

It sneaks in after a small move in your favor.

"What if it reverses? I better lock this in."

And just like that, a great trade turns into a missed opportunity.

🔹 Hope drags you into holding too long.

It dreams: "Maybe it doubles... maybe this time it'll be massive."

But it's not guided by data — it's driven by fantasy.

🔹 Discipline is what sits in the middle.

Quiet. Neutral.

It doesn’t scream or seduce — it just follows the plan.

And that’s where Growth lives — not just on the PnL, but in your psychology.

When Bitcoin pushes toward new ATHs, these emotions get amplified.

The real question becomes: Can you manage yourself, not just your trade?

📌 A Real Example from My Desk

In my earlier BTCUSD idea — “Another Edge – Decision Time” (shared above) —

I sent that setup to one of my managed clients.

He entered long exactly at the edge of the channel — a clean, strategic buy.

Price moved beautifully in our favor…

But he manually closed the trade at 106,600 — long before the move matured.

Why?

Because fear of giving back profit overwhelmed the original plan.

The chart was right. The timing was right.

But the exit was emotional, not tactical.

✅ The trade made money.

❌ But the lesson is clear: a profitable trade doesn’t always mean a disciplined one.

🎯 Final Takeaway:

“Fear kills your winners. Hope kills your timing. Discipline grows your equity and your character.”

🗣 What would you have done in that position?

Held longer? Closed at resistance? Let it run toward ATH?

Let’s talk psychology — drop your thoughts 👇

#MJTrading

#TradingPsychology #BTCUSD #FearHopeDiscipline #LetYourWinnersRun #PriceAction #BTCATH #ForexMindset #CryptoStrategy

Alltimehigh

Options Blueprint Series: All-Time High Christmas Tree SpreadIntroduction

As Nasdaq futures continue to show bullish momentum, traders are eyeing the potential for a new all-time high. With market conditions favoring upward movements, leveraging options strategies that maximize upside potential becomes crucial. One such strategy is the Christmas Tree Spread, traditionally used to limit risk while maintaining profit potential. However, in this article, we will explore a modified version where all strikes are Out-Of-The-Money (OTM), creating a setup that profit to the upside no matter how high Nasdaq goes. This approach aligns perfectly with the optimistic outlook for Nasdaq futures and sets the stage for potential gains.

Strategy Overview

The Christmas Tree Spread is a versatile options strategy that can be tailored to suit various market conditions. Traditionally, when using calls, it involves buying one call at a lower strike price and selling three calls at higher strike prices and buying two more calls at even higher strike prices, creating a balanced risk-reward profile. In this modified version, we adjust the strikes to all be Out-Of-The-Money (OTM), enhancing the bullish nature of the strategy.

For this setup, while Nasdaq Futures are trading at 19,982.75, we select the following strike prices for Nasdaq futures options with an expiration date of September 2024:

Buy one 20000 call

Sell three 21500 calls

Buy two 21750 calls

By choosing these strikes, we position ourselves to benefit from any substantial upward movement in Nasdaq futures. All strikes being OTM ensures that the breakeven point is set above the current price, effectively betting on a new all-time high for Nasdaq. This configuration guarantees profit to the upside, regardless of how high Nasdaq futures rise.

Strategy Rationale

The rationale behind selecting an all OTM strike setup for the Christmas Tree Spread lies in the current bullish outlook for Nasdaq futures. As markets exhibit strong upward trends, the potential for Nasdaq to achieve new all-time highs becomes increasingly plausible. This strategy aims to capitalize on such a possible bullish scenario.

Why OTM Strikes?

Lower Cost: OTM options are generally cheaper, reducing the initial cost of setting up the spread.

Increased Profit Potential: Since all strikes are set above the current market price, the profit potential is maximized for any substantial upward movement.

Risk Mitigation: The structure of the spread inherently limits risk, as losses are capped while allowing for upside gains.

Breakeven Point: The breakeven point for this modified Christmas Tree Spread is calculated based on the premiums paid and received for the options. Given the strikes selected (20000, 21500, and 21750), the breakeven point is above the current E-mini Nasdaq-100 futures price (20,465.62), aligning with the expectation of a new all-time high.

Detailed Setup and Example Trade

Setup Details:

Buy one 20000: This is the lower strike option, purchased to gain exposure to significant upside potential.

Sell three 21500 calls: These are the middle strike options, sold to offset the cost of the purchased call and to create a spread.

Buy two 21750 calls: These are the higher strike options, purchased to cap the potential loss from the sold calls and complete the spread.

Premiums Involved: Assuming the following hypothetical premiums:

20000 call: 683.38 points

21500 calls: 145.42 each (436.26 total for three)

21750 calls: 109.25 each (218.5 total for two)

Net Cost:

Total cost of buying calls: 683.38 (20000 call) + 218.5 (21750 calls) = 901.88

Total premium received from selling calls: 436.26 (21500 calls)

Net cost: 901.88 – 436.26 = 465.62

Risk Profile and Reward-to-Risk Ratio:

Maximum Risk: The maximum risk is limited to the net cost of the trade, which is 465.62 points.

Maximum Reward: The maximum reward would take place at 21500 on expiration and is 1034.39 points. The structure ensures 534.39 points of profit as the index potentially climbs higher.

Breakeven Point: The breakeven point is the initial cost added to the lower strike price, which is 20000 + 465.62= 20,465.62.

Trade Scenario: To illustrate, let's consider the potential outcomes at expiration in September 2024:

If Nasdaq is below 20000: All options expire worthless, and the net loss is the initial cost: 465.61 points.

If Nasdaq is at 21500: The 20000 call gains 1500, the 21500 calls expire worthless, and the 21750 calls expire worthless. Net gain = 1500 - initial cost = 1034.39 points.

If Nasdaq is at or above 21750: The 20000 call gains 1500, two of the 21500 calls each lose 250, and the 21750 calls expire worthless. Net gain = $1500 - 750 (total loss from sold calls) – 465.61 (initial cost) = 534.39 points.

Risk Management

Risk management is a crucial aspect of any trading strategy, especially when dealing with options. For the modified Christmas Tree Spread strategy on E-mini Nasdaq-100 futures options, several risk management techniques can be employed to ensure that potential losses are minimized and profits are protected.

Use of Stop-Loss Orders:

Stop-Loss: Implementing stop-loss orders can help limit losses if the market does not move as expected. Setting a stop-loss at a certain percentage below the purchase price can automatically exit the position, reducing the risk of holding losing trades.

Hedging Techniques:

Protective Puts: Purchasing protective puts can provide additional downside protection if the market moves significantly against the position. This can be considered if there are signs of a strong bearish reversal.

Spreading Risk: Diversifying the strike prices or expiration dates can spread the risk and reduce the impact of a single adverse market movement. However, this needs to be balanced with the strategy's intent and market conditions.

Avoiding Undefined Risk Exposure:

Capped Risk: The strategy inherently caps risk by buying the 21750 calls, which limits the maximum loss from the sold 21500 calls. Ensuring that all components of the strategy are correctly implemented and monitored helps avoid unexpected risks.

Regular Monitoring: Regularly reviewing the position and market conditions ensures that the strategy remains aligned with the trader’s expectations and risk tolerance. Adjustments can be made as necessary to manage exposure.

By incorporating these risk management techniques, traders can enhance the robustness of the modified Christmas Tree Spread strategy, ensuring that potential losses are minimized while maximizing the chances of achieving the desired profit.

Application with Micro E-mini Nasdaq Options

The modified Christmas Tree Spread strategy can also be effectively applied to Micro E-mini Nasdaq futures options. Micro E-mini options offer the same strategic benefits but with smaller contract sizes (10 times less), making them more accessible for traders with smaller accounts or those looking to manage risk more precisely.

Advantages of Using Micro E-mini Options:

Lower Capital Requirement: The smaller contract size of Micro E-mini options means a lower initial cost, making it easier for more traders to participate.

Fine-Tuned Risk Management: Smaller positions allow for more precise control over risk, as traders can scale in and out of positions more easily.

Similar Profit Potential: While the absolute profit may be smaller compared to standard E-mini options, the percentage returns can be similar, providing an effective way to capture upside movements in E-mini Nasdaq-100 futures.

Comparison of Standard E-mini vs. Micro E-mini Options: Standard E-mini options have larger contract sizes and are typically used by traders with more significant capital to invest. In contrast, Micro E-mini options offer smaller contract sizes, making them ideal for traders with smaller accounts or those who prefer to manage risk more precisely. Both options provide the same strategic advantages but cater to different levels of investment and risk management needs.

Using Micro E-mini Nasdaq futures options provides traders with the same strategic advantage of capturing significant upside potential while managing risk effectively, aligning well with the bullish market outlook for E-mini Nasdaq-100 futures.

Conclusion

The modified Christmas Tree Spread strategy offers a robust and flexible approach to capitalizing on the bullish momentum of E-mini Nasdaq-100 futures. By strategically placing all strikes Out-Of-The-Money and targeting a new all-time high, this setup ensures profit potential to the upside, no matter how high Nasdaq climbs. With proper risk management and precise execution, traders can maximize their gains while minimizing risks. Whether using standard E-mini options or Micro E-mini options, this strategy provides a powerful tool for navigating the current market conditions and positioning for future growth.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Options Blueprint Series: Backspreads as a Portfolio Hedge1. Introduction

Backspreads are a versatile options strategy as they allow traders to benefit from significant moves in the underlying asset, particularly when there is an expectation of increased volatility.

2. Understanding Backspreads

A backspread is an advanced options strategy involving the sale of a small number of options and the purchase of a larger number of out-of-the-money options. This setup creates a position that benefits from large price movements in the underlying asset.

3. Generic Uses of Backspreads

Backspreads offer traders a flexible tool to capitalize on significant price movements and shifts in market volatility. Here are some common uses:

Market Sentiment Alignment:

Bullish Sentiment (Call Backspreads): Traders use call backspreads when they expect a significant upward move. This strategy involves selling a smaller number of lower-strike call options and buying a larger number of higher-strike call options.

Bearish Sentiment (Put Backspreads): Conversely, put backspreads are used when traders anticipate a significant downward move. This involves selling a smaller number of higher-strike put options and buying a larger number of lower-strike put options.

Volatility Trading:

Backspreads are particularly useful in trading volatility. They create positions with positive Vega, meaning they benefit from increases in implied volatility. This makes backspreads an excellent choice during times of market uncertainty or expected volatility spikes.

4. Hedging an Equity Portfolio using with S&P 500 Futures Put Backspreads

Put backspreads offer an effective way to hedge a long equity portfolio against sharp downward moves. By setting up a put backspread, traders can create a position that not only provides downside protection but also benefits from increased market volatility.

Setting Up a Put Backspread for Hedging:

Sell 1 OTM Put: The initial step involves selling one out-of-the-money (OTM) put option. This option will generate a premium, which can be used to offset the cost of the puts that will be purchased.

Buy 2 Lower OTM Puts: Next, purchase two lower OTM put options. These options will provide the necessary downside protection. Depending on the strike selected, the cost of these puts will be fully or partially covered by the premium received from selling the higher-strike put.

Constructing a Positive Vega Position:

The structure of the put backspread results in a position with positive Vega. This characteristic is particularly valuable as volatility typically rises during periods of sharp declines.

Risk Profile:

Below is the risk profile of a put backspread used for hedging purposes as described in section #6 below.

5. Market Scenarios

Understanding how a put backspread behaves under different market scenarios is crucial for effective trade management and risk mitigation. Here, we explore the potential outcomes:

Market Moving Up or Staying the Same: Flat P&L

If the market moves up or remains around the current level, the put backspread will likely expire worthless.

Market Moving Down Sharply: Increased Profitability

If the market experiences a sharp decline, the put backspread would potentially become profitable.

Impact of Increased Volatility: Enhanced Gains

A rise in implied volatility benefits the put backspread as higher volatility increases the value of the bought puts more than the sold put, adding to the overall profitability of the strategy.

Maximum Risk and Trade Management:

Maximum Risk: Limited to the difference between the strike prices minus the net credit received (or plus the net debit paid).

Trade Management: It is essential to actively manage the position.

6. Trade Example

To illustrate the application of a put backspread as a hedge, let's consider a detailed trade example using S&P 500 Futures Options.

Trade Rationale:

Current Market Condition: The S&P 500 Futures have just created a new all-time high, indicating that the market is at a crucial juncture. From this point, the market could either continue its upward trajectory or experience a severe change of direction.

Implied Volatility (VIX): The VIX, which measures the implied volatility of options, is currently very low at 11.99. This low volatility environment makes it an ideal time to enter a backspread, as any future increase in volatility will significantly benefit the position.

Trade Setup:

Underlying Asset: S&P 500 Futures

Current Price: 5447

Strategy: Put Backspread

Expiration Date: December 2024

Specifics:

Sell 1 OTM Put: Sell 1 4600 put option

Buy 2 Lower OTM Puts: Buy 2 4100 put options

Entry Price:

Sell 1 4600 Put: Receive $2,160 premium per contract (43.2 points)

Buy 2 4100 Puts: Pay $1,068.5 premium each; total $2,137 for two contracts (21.37 points x 2)

Net Cost:

The net cost of the backspread is the premium paid for the bought puts minus the premium received from the sold put.

Net Cost: $2,137 (paid) - $2,160 (received) = $23 net credit

As seen below, we are using the CME Group Options Calculator in order to generate fair value prices and Greeks for any options on futures contracts.

Maximum Risk:

500 – 0.46 = 499.54 points (distance between strike prices minus the net credit received).

7. Importance of Risk Management

Risk management is a fundamental aspect of successful trading and investing. It involves identifying, analyzing, and mitigating potential risks to protect capital and maximize returns. When implementing a put backspread as a portfolio hedge, understanding and applying robust risk management practices is crucial.

Using Stop Loss Orders and Hedging Techniques:

Stop Loss Orders: Placing stop loss orders helps limit potential losses by automatically closing a position when the market reaches a certain price level. This ensures that losses do not exceed a predetermined amount, providing a safety net against adverse market movements.

Hedging Techniques: Utilizing hedging strategies, such as combining put backspreads with other options or futures contracts, can provide additional layers of protection. This approach can help manage risk more effectively by diversifying exposure and reducing the impact of unfavorable market conditions.

Importance of Avoiding Undefined Risk Exposure:

Defined Risk Strategies: Employing strategies with clearly defined risk parameters, such as put backspreads, ensures that potential losses are limited and known in advance. This contrasts with strategies that expose traders to unlimited risk, which can lead to catastrophic losses.

Position Sizing: Properly sizing positions based on risk tolerance and account size is essential. This involves calculating the maximum potential loss and ensuring it aligns with the trader's risk management plan.

Precise Entries and Exits:

Entry Points: Entering trades at optimal levels, based on technical analysis, support and resistance and UFO levels, and market conditions, enhances the probability of success. In the case of put backspreads, entering when volatility is low and market conditions are favorable increases the potential for profitability.

Exit Points: Setting clear exit points, including profit targets and stop loss levels, helps manage risk and lock in gains. Regularly reviewing and adjusting these levels based on market developments ensures that positions remain aligned with the trader's overall strategy.

Continuous Monitoring and Adjustment:

Regular Review: Continuously monitoring market conditions, position performance, and risk parameters is essential for effective risk management. This involves staying informed about economic events, market trends, and changes in volatility.

Adjustments: Making timely adjustments to positions, such as rolling options, adjusting stop loss levels, or hedging with additional instruments, helps manage risk dynamically and adapt to changing market conditions.

By incorporating these risk management practices, traders can effectively use put backspreads to hedge their portfolios and protect against significant market downturns.

8. Conclusion

In summary, put backspreads offer a powerful tool for hedging long equity portfolios, especially in low volatility environments and/or when markets are at all-time highs. By understanding the mechanics of put backspreads, their application in various market scenarios, and the importance of active risk management, traders can enhance their ability to protect their investments and capitalize on market opportunities.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Naukri (Info Edge) - ATH - above 2805NSE:NAUKRI is likely to hit all time highs if it stays above 2805.

If Bitcoin Really is The New GoldLet's say the equities market crashes along with commodities, then we would expect gold's price to increase, but maybe Bitcoin will become the new gold due to the nature of the pandemic that we are currently amidst. The key point is this: gold is neither easily transportable, transferrable, nor is it readily portable. It would be impractical to expect be able to readily access gold throughout the entire time it takes for our planet to either acquire herd immunity to SARS-CoV-19 or to produce a vaccine which would be used to prevent said virus. Bitcoin is advantageous in this aspect. A $120,000 per coin call sounds hopeful at one point or another, but such lofty thoughts like that don't seem too far out of reach, especially during times like these.