Time to invest in JPY and TN/bond? Hello FX/futures traders!

Market is at a pivotal point. Not in a bad way, but in a good way!

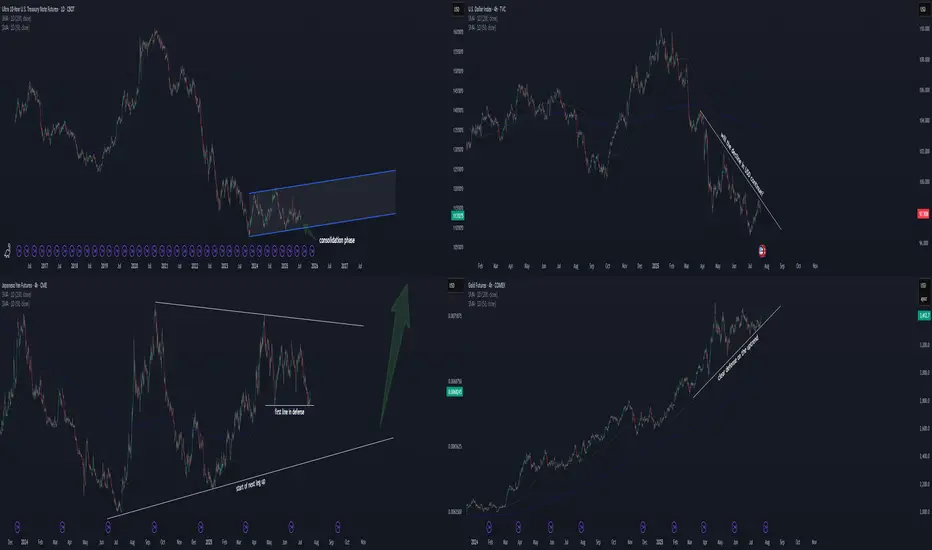

Chart 2: TVC:DXY

Let's start with the US Dollar . A declining USD was just well defended the last few days. If this is true, then the stock up, dollar down scenario is likely to continue. This is good for equities.

Chart 4: COMEX:GC1!

Gold defends its trendline as well. It seems like gold wants to go up more. A raising gold in the current scenario suggests declining USD TVC:DXY . This isn't always true, but we have to look at the current correlation and makes the best educated guess on this.

Logical Deduction 1:

Chart 1: CBOT:TN1!

A consolidation phase has been going on for almost 2 years now. This is definitely

a good sign to long bond, as at least we know the likely bottom for stoploss. With dollar leaning down and gold up, I think TN will defend its current level around 110-113.

Logical Deduction 2:

Chart 3: CME:6J1!

JPY is defending its first key level since May 2025. A wedge is forming, and the breakout is about to take place later this year. Likely the consolidation phase will take more time (with likelihood to breakout to either side). But with a declining USD side by side, I consider now a good entry point to long JPY with controllable risk.

Let me know what you think!

10yryields

10Y Note Auction & Why Markets did %10 Movement with Last Data?Hello Traders tomorrow we have 10-Year Note Auction data and I wanted to prepare a nice little information for you about this topic because the data released last month showed an immediate 10% increase and from what I saw, many people had no idea what was happening.

📌 What is the 10-Year Note Auction?

The U.S. government regularly issues 10-year Treasury notes to finance its budget. The auction result reflects investor demand and long-term interest rate expectations. The yield (interest rate) that results from the auction is a key benchmark for financial markets globally.

🔄 Connection to U.S. Stocks and EUR/USD

🟢 If Demand Is Strong (Yields Stay Low):

Investors are eager to buy U.S. debt, pushing prices up and yields down.

This indicates confidence in the U.S. economy and little concern about inflation or rate hikes.

Stock markets generally react positively.

🔴 If Demand Is Weak (Yields Rise):

Investors require higher returns, possibly due to inflation fears or policy tightening expectations.

This pushes yields up, increasing borrowing costs and reducing the attractiveness of risk assets.

Stocks typically decline, and the dollar strengthens.

💱 Effect on EUR/USD

🟢 If Yields Rise:

U.S. dollar becomes more attractive due to higher returns.

Investors buy USD to invest in Treasuries.

EUR/USD typically falls.

🔴 If Yields Fall:

Lower yields reduce the appeal of the dollar.

Investors may move capital elsewhere.

EUR/USD tends to rise.

🗓️ Latest 10-Year Treasury Auction – April 9, 2025

Auction Size: $39 billion

High Yield: 4.435%

Expected (WI) Yield: 4.465%

Outcome: Strong demand – yield came in lower than expected.

📊 Post-Auction Market Reactions

🔹 10Y Treasury Yield:

Before auction: ~4.466%

After auction: Dropped to ~4.38%

➝ Reflects strong investor demand and confidence in long-term stability.

🔹 S&P 500 Index:

Lower yields reduce borrowing costs and support equity valuations.

Investors often shift toward riskier assets like stocks when yields fall.

The S&P 500 responded positively after the auction.

🔹 EUR/USD:

Falling yields reduce the dollar's relative appeal.

This may push EUR/USD higher, depending on other macroeconomic influences (like ECB policy or geopolitical risks).

✅ Conclusion

The April 9, 2025, 10-year Treasury auction showed strong demand with a yield lower than market expectations. This led to a drop in yields, a positive reaction in U.S. stock markets, and potential downward pressure on the dollar, which may support EUR/USD.

Buy idea on Crude Oil (CL1!)Based on :

- US10Y Leading long spike

- Commercials and Non Commercials at Extremes

- Open Interest at Extremes

- Cycles and quantitative data

- Undervalued conditions

-Demand zone

Interest Rates don't seem to want to slow downWe believed that interest rates were going higher in Early April/Late March.

The Bullish Engulfing formation was a sign that higher interest rates were coming TVC:TNX

The 10 Yr Yield Downtrend was broken, it retraced some, we posted that it was likely consolidating, & seems to want to go a little higher.

Central Banks worldwide are lowering rates while the US is raising them.

---

Please see our profile for more info... We do post a lot.

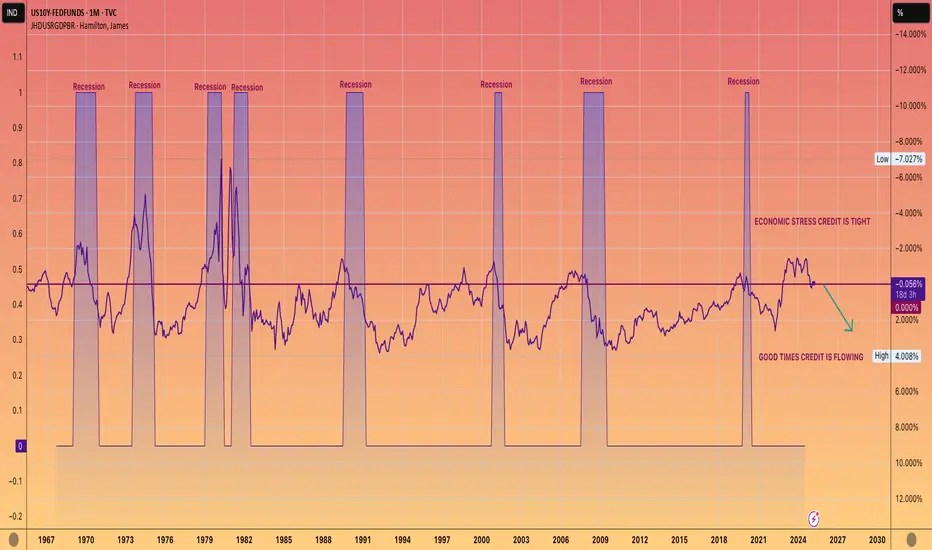

WE ARE COMING OUT OF A RECESSION. NOT GOING INTO ONE.This chart shows 10-year yield, which is closely tied to mortgage rates, minus the Federal funds rate.

When this figure is negative, it typically indicates that we are experiencing a recession or economic downturn.

Conversely, a positive number usually aligns with economic growth, often referred to as the good times.

While it's up to you to determine the reasons behind a official recession not being declared during the Biden administration, the undeniable data reflects a prolonged period of economic strain.

However, the current trend seems to be shifting towards a positive reading, which should lead to more accessible lending and economic growth.

AKA The good times are coming.

relief pumpSeems like election bull was already priced in, new money got washed.

Bonds are making a comeback, cash is a position.

Expecting more downturn after a relief pump, coinciding with yields retracement.

Yields trending with equity price are usually signs of either economical expansion or economical fears, such as slowdown or recession, during up and downs. The markets just jumped from one narrative to the other:

expansion(trump gets in office) ---> slowdown(tariffs imposed)

I think the expansion narrative will take a while to settle back(end of Q2 at least) after all the executive orders signed.

Although, I'm still long for the month of March, nice opportunity for a relief pump, before resuming of slowdown narrative.

don't get caught chasing yields higher Intraday Update: The divergent RSI in the 10yr ZN's is allowing for a pullback/moderation of overbought intraday conditions, and yields have recovered near term. However, we expect dips to be bought in any dip towards the 110'00 level.

BTCUSD Daily Inflection Point UpdatePreviously I mentioned the weekly was consolidating, but there is potential for this momentum consolidation to have a breakout leg as momentum shifts and the final emotional price movements are played out. I was too conservative in my price projections; a lot more than I used to be- but there wasn't a whole lot of TA involved- I figured the dollar issues would crop up earlier.

Now that the Fed had pivoted. the yields are creeping back up pushing bitcoin back down. The fed doesn't let on just how dire the situation is- and with global tensions rising, the dollar is at significant risk.

I expect a broad correction in all the markets- and cash to become very tight.

There is daily momentum consolidation- and if any other events occur that send yields upward- bitcoin is likely to suffer as a consequence. If instead we sail into the new year unscathed- then this consolidation may provide another leg up; but a break below 88k and a push towards 60k may solidify bitcoins correction.

DAILY

WEEKLY

10y+ bonds are becoming even more attractive for investorsThe US economy in December added the most jobs since March and the unemployment rate unexpectedly fell, capping a surprisingly strong year and supporting the case for a pause in Federal Reserve interest-rate cuts.

Nonfarm payrolls increased 256,000, exceeding all but one forecast of economists. The unemployment rate fell to 4.1%, while average hourly earnings rose 0.3% from November.

YIELDS are rising, and traders are fully pricing in the first rate cut in October. The 10-year yield may aim for the 5% level, similar to the March 2023 movement. However, let's not forget that at that time the interest rate was 5.5%, and there were no expectations for combating 9% inflation.

Currently, inflation is even below 3%, and concerns that the US will impose new sanctions or that tax cuts will create a new wave of inflation are purely speculative fears, not facts, which have created an emotional backdrop in the markets.

On the contrary, 10, 20, and 30-year bonds are becoming even more attractive for investors.

And don't forget, pre-election promises often do not turn into reality.

Darling Ingredients - Watch this chanel to rebouns The company transforms organic waste into sustainable products such as biodiesel and animal feed. The stock's current value is significantly below estimates, offering steady growth thanks to environmental trends and regulatory incentives

You Are Here -> 10YR YIELDSThe next financial crisis is potentially right around the corner

11:11

The question is, has the fed lost control?

Is it by design?

In less than 50 Days the fed gets back together, 11/7

Election is 11/5

Veterans Day is 11/11

10 Year in Trouble...Ruh-Roh Raggy...the 10YR is now playing peekaboo over the downward trendline we have developed over the last few months.

What about DXY?I haven't updated my DXY analysis for a while. So let's dust it off.

The last update was in September when the atmosphere was changing in a way that we couldn't predict the US Election clearly and for a short period, the market thought the results wouldn't be as it is today. That was why I was a bit bearish on DXY. By getting closer to Election Day the clouds were going away and it got easier for the market to see the outcome. So, it strengthened the dollar while weakening the Gold as we expected the geopolitical tensions to cool off.

What's next?

For now, I see the 10-year bond yield can show a bit more weakness to come just below 3.99%. Then after that, we should update our analysis and see what comes next. But I think ~4% is low for now and after that, I like to see a jump back up. In this short-term correction DXY would follow the 10-year bond yield and most probably come into the range of 104 to 105. That's also can be a small driver for Gold to go higher a bit.

Look up!True story there's not enough YFI for everyone and it hit 90k before BTC just saying.. 🤷♂️

"You know yfi and btc have different supply/market cap scenarios right???"

"Ya, but... but.. but.." BOOM

Yahh ummm Number still go up bra! it don't matter to the memeholics so then why should I care ya know?

Soooo little time with sooo little coin. You tell me if that matters! Every Bitcoin Maxii from here to to the moon blabs about it none stop! "Olny 21Mil Only 21Mil! BTC Digital Gold!

Oh ya?? So tell me Circulating supply 33.60K YFI whats that make YFI then?

"One coin to rule them all until there is wait two or three... Oh wait there's another one!!!"

YOLO Moonboyz 🌛 If you feel so inclined to do so.

🚽👄Toilet Mouth: "Why do all your post say Short!?" or a bunch of "BUT, BUT, BUT"

⭐Not my job to tell you to buy or sell entries matter to most I only care about my exits.

⭐Let each person determine their cost to acquire and choice to play or not.

No Advice to give just thoughts that I can't shake after the last 8 years in the world of "CRYPTO"

Things 🤷♂️ #Fixed IDK!

🙏 FOR JUST A HEALTHLY PULLBACK!

""KEEP CALM AND MANAGE THY RISK & BALANCE your Senses!""

I am The CoinSLayer 👨💻😈

You have been warned by The Coin SLayer!

P.S. Now witha bag!

P.S.S. well two or Ten

US DOLLAR - Let Me Explain My Bearish Thesis...In this video, I’ll share why I believe the markets are on the verge of a major downturn.

By analyzing the US dollar chart alongside Gold, the S&P 500, and Bond Yields, I’ll explain why we may be approaching the final stages of this market cycle for stocks and asset prices.

This shift could devastate the economy, setting the stage for the next bull market. While the extent of the drop will depend on market forces, I’ll explore how such a scenario could unfold. We’ve already seen Oil prices plunge to zero—if you think that can’t happen to other markets, time may prove otherwise.

This is simply a turning point, a necessary reset to pave the way for future growth.

This is not financial advice.

20% Interest Rates Could Crash The Market 98%It’s been a while since I last posted, but I’ve got a good reason to start again.

If you take a close look at the charts in this video, you'll notice the potential for a significant market decline across the board.

By analyzing the Dow Jones and interest rates together, it becomes evident that we are nearing this point.

I'm not influenced by news or personal biases—I just prefer not to invest when the market is in this state.

Whether it’s stocks, precious metals, or crypto, I believe it’s wise to be cautious when these signals appear.

The long-term interest rate chart gives me strong reasons to believe we could see a historic drop in asset prices.

Basic concepts like mean reversion and resistance turning into support are some of the key factors that back my AriasWave analysis.

Stay tuned for more updates now that I’m back to sharing new ideas.

Bitcoin - Another sign that Fed credibility is waning.A Sick Feeling in the Belly of the Yield Curve

Another sign that Fed credibility is waning.

The socioeconomic point of view is that, as the Supercycle bear market develops, central banks will lose their mantle as being omnipotent directors of markets. Whereas in the bull market, central bankers like Alan “the Maestro” Greenspan were lauded because positive social mood was driving the stock market higher, in the bear market central bankers will be vilified as negative social mood causes a downtrend in stock prices.

Yesterday, Fed Chairman Jerome Powell sought to reassure Americans that the series of interest rate hikes that the central bank is embarking on would not tip the U.S. economy into recession. The bond market promptly ignored those soothing words and the yield curve flattened. A flattening yield curve, whereby the positive gap between short-dated bonds and long-dated bonds is narrowing, is a sign that the market is anticipating slower economic growth. When the yield curve inverts, with long-dated yields below short-dated, it has historically been a signal that an economic recession is on the horizon.

That historical relationship is most generally related to the yield spread between 2-year yields and 10-year yields, and that yield curve has been flattening over the past year from 1.50% to around 0.20% where it is currently hovering. So, not quite inverted yet, but trending in that direction.

However, in the so-called belly of the yield curve, the area between 5 and 10-year maturity, the message is already here. The chart below shows that the yield spread between 5 and 10-year U.S. Treasury yields has declined precipitously over the last year and, yesterday, turned negative. This yield curve inversion is a clue that a 2-yr /10-yr (2s 10s in industry vernacular) inversion is probably on its way.

Despite what the Fed says, a beast of a recession may be approaching.

U.S. Treasury 10-Year Yield Minus 5-Year Yield

10yr possible false breakoutPossible false breakout US 10yr yields and this is a risk for risk sensitive currencies like USDJPY and USDCHF

Chart Analysis of 10-Year U.S. Treasury Bond Yields

Based on current chart patterns and Elliott Wave Theory, it appears we are in Wave 4 of a higher-degree cycle for the 10-year U.S. Treasury bond yields. Wave 4 is typically a corrective phase following a strong trending Wave 3, suggesting that this phase may involve consolidation or retracement.

Key Levels to Watch:

38% Retracement (Lower Orange Line) : If yields bottom near this retracement level, it may indicate a potential support zone where Wave 4 could complete its correction.

61% Retracement (Upper Orange Line) : Should the yields find support at the 38% level, they might subsequently target the 61% retracement level of Wave 3, suggesting a potential upward move.

Market Implications : If the bond yields continue to rise and reach these retracement levels, we could witness a significant bearish trend in the broader market. However, it's crucial to recognize that market conditions are dynamic and can affect these projections.

Disclaimer : This analysis is based on the current technical chart patterns and Elliott Wave Theory. Market conditions are subject to change, and unforeseen factors can impact outcomes. Therefore, it's essential to stay informed and consult with a financial advisor before making investment decisions.

Regards

FOMC Showdown Poised to Ignite a Surge in Yield SpreadsWith inflation finally cooling and the Fed signaling rate cuts, it seems relief is on the horizon—until you look at the job market. As recession risks grow and Treasury yields falter, a steepening yield curve presents a compelling opportunity.

Positioning in the yield curve ahead of the FOMC meeting offers a more measured way to navigate the uncertainty.

COOLING CPI SIGNALS GREEN LIGHT FOR RATE CUTS

This week’s inflation report showed headline CPI cooling to 2.5%, the lowest since February 2021. With this release, inflation has finally fallen decisively below the stubborn 3% mark and is now just 0.5% above the Fed’s target range. PCE inflation reflects similar levels, likely giving the Fed the signal to start cutting rates.

JOB MARKET REPRESENTS MATERIAL RECESSION RISKS

Recent job market data suggests it may be too soon to declare a soft landing. The labor market is significantly weakening, and with household savings dwindling and credit delinquencies increasing, conditions may worsen before improving.

U.S. economic data from the past week indicates that the labor market is in a precarious situation. The August JOLTS report showed job openings dropping to their lowest since early 2021, reflecting decreased labor demand, while unemployment edged up slightly.

Additionally, the August jobs report revealed a modest gain of 142,000 non-farm jobs, falling short of expectations, with downward revision for July bringing those figures down to just 89,000.

As covered by Mint Finance previously a recession is likely to lead to a sharp steepening of the yield curve.

We covered average levels of the yield spread at the start of recessions in detail previously, but in summary with the current 10Y-2Y spreads at 15 basis points, there may be up to 85 basis points of further upside in the spread.

TREASURY YIELD PERFORMANCE

Despite a short recovery following the ominous jobs report on 2/August, Treasury yields have continued to decline. Unsurprisingly, short-dated treasuries have underperformed as 2Y yields are 27 basis points lower, while 30Y yields have only declined by 12 basis points and 10Y by 15 basis points.

Overlaying yield performance with economic releases, the largest impact on yields over the last few months has been from FOMC releases and non-farm payrolls while performance around CPI releases has been mixed. Potentially suggesting traders are more concerned about recession risk than moderating inflation.

OUTLOOK FOR SEPTEMBER FOMC MEETING

Source: CME FedWatch

FedWatch currently suggests that a 25 basis point rate cut is more likely in the upcoming FOMC meeting scheduled on September 17/18. However, probabilities of a 50 basis point rate cut are also relatively high at 43%.

Source: CME FedWatch

While the odds of a 25 basis point cut have remained in majority, the 50 basis point cut has been uncertain with probability shifting over the past week.

FOMC meetings have driven a rally in yield spreads over the past year.

With FOMC meeting slated for next week, it is interesting to note that performance in yield spread prior to meetings has been more compelling than performance post-FOMC meeting. Over the last 5 meetings, pre-FOMC meetings, the 10Y-2Y spread has increased by 4 basis points.

Performance is even more compelling in the 30Y-2Y spread which has increased by an average of 13 basis points.

AUCTION DEMAND FAVORS 10Y

Recent auction for 10Y treasuries indicated strong demand with a bid/cover ratio of 2.64, which is higher than the average over the last 10 auctions of 2.45. Contrastingly, the 30Y auction was less positive with a bid/cover ratio of 2.38, below the average of 2.42. 2Y auction was sharply weaker with a bid/cover of 2.65 compared to average of 2.94.

Auction uptake suggests higher demand for 10Y treasuries than 30Y treasuries and fading demand for near-term 2Y treasuries.

HYPOTHETICAL TRADE SETUP

Recent economic data has made an upcoming rate cut nearly certain. However, the size of the cut remains unclear. CME FedWatch currently indicates a 42% probability of a larger 50-basis-point cut, driven by the recent CPI report and weak jobs data.

With rising recession risks, the Fed might opt for a larger rate cut. However, if they choose a moderate 25-basis-point cut, market sentiment could stabilize. Historically, yield spreads around FOMC meetings suggest that positioning before the meetings tends to be more advantageous than after. This is especially relevant now, as moderating sentiment from a 25-basis-point cut could trigger a temporary reversal in yield spreads.

Considering the underperformance of the 10Y-2Y spread in September and increased auction demand for 10-year Treasuries, a long position in the 10Y-2Y spread may be the most favorable strategy for gaining exposure to the steepening yield curve.

Investors can express views on the yield curve using CME Yield Futures through a long position in 10Y yield futures and a short position in 2Y yield futures.

CME Yield Futures are quoted directly in yield with a 1 basis point change representing USD 10 in one lot of Yield Future contract. This makes spread calculations trivial with a 1 basis point change in spread representing PnL of USD 10.

The individual margin requirements for 2Y and 10Y Yield futures are USD 330 and USD 320, respectively. However, with CME’s 50% margin offset for the spread, the required margin drops to USD 325 as of September 13, making this trade even more compelling.

A hypothetical trade setup offering a reward to risk ratio of 1.46x is provided below:

Entry: 14.2 basis points

Target: 35 basis points

Stop Loss: 0 basis point

Profit at Target: USD 208 (20.8 basis points x 10)

Loss at Stop: USD 142 (14.2 basis points x 10)

Reward to Risk: 1.46x

MARKET DATA

CME Real-time Market Data helps identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs tradingview.com/cme .

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed. Please read the FULL DISCLAIMER the link to which is provided in our profile description.

10 year Treasury- Massive Head and Shoulders on the Weekly ChartAppears to have broken the neckline, targeting 3.5% or 2.76% in the next few months

Gold vs the 10yr yieldThis is a ratio chart.

Gold is on top

10 year Yield is on bottom

in the middle you can see the ratio between gold prices and the 10yr yield rising and falling.

As you can tell, when the ratio reaches a low, gold prices tend to rise and yields tend to fall.

Vice/versa when the ratio is at a high, Gold prices tend to fall, and yields tend to rise.

Of course the ratio chart is not "CAUSING" the prices to rise or fall.

In my humble opinion, we are relatively close to the long term low point on the ratio chart.

Meaning that either gold prices should rise and or yields should fall, and or both maybe...

Barrons has recently published a piece saying that rising supply of gold could contribute to prices ending the year around 2100. usd

This would be a drop in price, and doesn't fit in with my narrative.

It might be interesting to see how this ratio plays out, and perhaps it will help you form a bias for your next Gold trade!

US10Y - US Ten Year Yields WeeklySome weekly consolidation; Possible yields haven't topped yet. These inflection points lead to weekly and monthly trend changes which I will be looking for a potential spike as momentum shifts back down and rates test the keltner channel mid or upper line. There is also a possibility that rates breakout of the resistance (trend change) of this bullish leg from 2020. The Red line on the keltner channel oscillator at the bottom.

I expect more black swan events to occur as chaos ramps up in the next year.