The Bank of Japan can’t let goThis week financial markets were dominated by central banks policy decisions. While the Federal Reserve (Fed) and Bank of England (BOE) kept rates on hold, the policy board of the Bank of Japan (BOJ) decided to further increase the flexibility in its yield curve control policy.

The BOJ previously set a strict cap of 1.0% for the 10-year Japanese Government Bond (JGB) yield. But it has now decided that 1% should be a “reference” (not a strict cap), which effectively allows the yield to rise above 1% when the BOJ thinks it is appropriate. The upper bound of 1% appears to be a level they can’t let go of. By doing so, the BOJ is choosing an exit path that gives them the maximum flexibility but minimum volatility around the Yen. We view this as a dovish move as consensus expectations were for the BOJ to move the cap to 1.25% rather than 1%.

Japan’s remains on a narrow path

One of the reasons holding back the BOJ from normalisation of policy rates, is they still believe Japan’s recovery since the re-opening in October 2022 remains on a narrow path as it relies heavily on tourism, while the broader services sectors have yet to pick up significantly and manufacturing activity has been hampered by soft exports. Japan’s flash PMI readings for October showed us a bifurcated economy where the services sector is stronger than the manufacturing sector. Manufacturing PMI clocked in at 47.6, which is in contraction territory. Services PMI was 51.1, which is down from last month’s reading of 53.8 but is still in expansion territory, no doubt helped by fiscal stimulus and the accommodative monetary policy environment.

BOJ on the lookout for an intensified virtuous cycle between wages and prices

BOJ governor Ueda indicated that the BoJ will be monitoring the upcoming spring union-employer wage negotiations. A strong outcome could catalyse the earlier attainment of sustained inflation in Japan, but overall, Japan’s recovery isn’t strong enough yet for employers, especially small enterprises, to meaningful support wage hikes in the broad economy. While headline inflation bolted north of 4% in January 2023, it appears to have peaked and has begun receding. While core inflation remains around the 4% mark. The Producer Price Index (PPI) slowed to 2% annually in September suggesting a stabilization or even drop in CPI ahead.

The BOJ revised its outlook for core inflation (all items less fresh food and energy) to 3.8% in FY23, 1.9% for FY24 and 1.9% for FY25. The BoJ stated that the inflation uptick “needs to be accompanied by an intensified virtuous cycle between wages and prices”.

The Yen is unlikely to appreciate under BOJ’s policy change owing to the large gap in interest rates between the US and Japan. The direction of the Yen matters for Japanese equities owing to Japan high export tilt. The exporters stand to benefit amidst a weaker Yen.

Fire power abounds for Japanese equities

Japanese equities had a strong first half in 2023, attaining 33-year highs. Yet valuations at 15.7x price to earnings ratio (P/E), still trade at a 30% discount to its 15-year average providing room to catch up. More importantly, earnings revision estimates in Japan are currently the highest among the major economies. Earnings yield at 4.07% for the Nikkei 225 Index has been trending above bond yields 0.947% for 10 Year JGBs , keeping the well-known TINA (There is no Alternative) trade alive in favour of Japanese equities.

Tailwind from corporate governance reforms

Tokyo Stock Exchange’s (TSE) call for listed companies to focus on achieving sustainable growth and enhancing corporate value is beginning to bear fruit. The call was aimed at companies with a price to book (P/B) ratio below one. Those companies were asked to develop a plan for improvement, disclose and then implement and track its progress. The progress has been encouraging with 31% of companies on the prime market making a disclosure of their plan .

Large companies with a price to book ratio below one have been more proactive with disclosure. Historically cash-heavy Japanese companies face increasing pressure to improve their numbers, possibly by funnelling historically high excess cash reserves into increased buybacks or dividends.

Conclusion

Inflation has been missing in Japan for more than a decade. So now that it has arrived aided by the post pandemic pick up of the Japanese economy, policy makers are not in a rush to obliterate it. With wage growth lagging behind inflation, the Bank of Japan does not appear ready to wean itself from Yield Curve Control until a more intensified virtuous cycle is observed between wages and prices. The BOJ’s policy decision this week is unlikely to allow the appreciation of the Yen, which should continue to provide a competitive advantage to Japanese exporters.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Boj

Boy that was a week!What a week that was! The dance around 150 certainly didn't disappoint. After the break and failure the week prior which continued on Monday, I thought that was it, that price gave it a good shot but ultimately failed, and would perhaps settle below.

To nobodies surprise then when the BoJ held rates at -0.10% that we made almost a straight line move back above the once solid wall. So severe was the buying, I wouldn't have blamed anybody buying dips on Wednesday.

The top was just over 151.700, and despite a small bounce on Thursday lunch, we spent the rest of the week grinding back towards 150. I don't think the Fed decision can really be to blame, it seemed almost certain we'd get a pause, in fact the market mostly agreed in the minutes after the release with a very muted reaction.

Today's jobs numbers was a different story, seeing an 80 pip decline. The past 3 days have almost all but wiped out the BoJ fuelled push giving us a messy looking Daily chart which is no longer respecting the uptrend nor 150 in any meaningful capacity.

Heading into next week i'll be watching to see where price settles. Give everybody the weekend to digest what happened and follow the price action Mon/Tue and let that inform an entry.

Hope you all had a great trading week, and I'll see you in a couple days.

EURJPY H4 | Bullish momentum to extend?EUR/JPY is falling towards a pullback support and could potentially bounce off this level to climb higher.

Buy entry is at 159.764 which is a pullback support that aligns close to the 38.2% Fibonacci retracement level.

Stop loss is at 159.281 which is a level that aligns with the 50.0% Fibonacci retracement level.

Take profit is at 160.847 which is a swing-high resistance.

High Risk Investment Warning

Trading Forex/CFDs on margin carries a high level of risk and may not be suitable for all investors. Leverage can work against you.

Stratos Markets Limited (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 67% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Europe Ltd, previously FXCM EU Ltd (www.fxcm.com):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 72% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Trading Pty. Limited (www.fxcm.com):

Trading FX/CFDs carries significant risks. FXCM AU (AFSL 309763), please read the Financial Services Guide, Product Disclosure Statement, Target Market Determination and Terms of Business at www.fxcm.com

Stratos Global LLC (www.fxcm.com):

Losses can exceed deposits.

Please be advised that the information presented on TradingView is provided to FXCM (‘Company’, ‘we’) by a third-party provider (‘TFA Global Pte Ltd’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by TFA Global Pte Ltd.

The speaker(s) is neither an employee, agent nor representative of FXCM and is therefore acting independently. The opinions given are their own, constitute general market commentary, and do not constitute the opinion or advice of FXCM or any form of personal or investment advice. FXCM neither endorses nor guarantees offerings of third party speakers, nor is FXCM responsible for the content, veracity or opinions of third-party speakers, presenters or participants.

USD/JPY: Anticipating Downward Movement at Strong ResistanceUSD/JPY is one of the most traded currency pairs in the world. The value of the USD/JPY pair is quoted in Japanese yen per one U.S. dollar. For traders, it is important to note that the pair is currently at a strong resistance level and is expected to move downwards.

Outlook

According to, the USD/JPY pair is expected to face resistance at the 151.70 area, which is its highest level since October 2022. The YTD peak could also offer some resistance to the USD/JPY pair ahead of the multi-decade top. The Bank of Japan's policy of patience sent the yen to an all-time low, and the Japanese authorities are always in close communication with U.S. counterparts on currencies and share a mutual understanding that excessive moves in the currency should be avoided. Therefore, traders should keep an eye on the pace of the decline in the Japanese yen.

Fundamental Analysis

The unwavering stance on negative rates by the Bank of Japan puts a spotlight on USD/JPY movements, amid whispers of potential interventions. The interest rate differential between the policy rates of the Federal Reserve and the Bank of Japan (BoJ) is an important influence on the USD/JPY exchange rate. Higher interest rates make a currency relatively more attractive because they allow for higher returns on investment.

Technical Analysis

The USD/JPY pair is currently at a key resistance level of 151.93. A firm break above this level will target 100% projection of 129.62 to 145.06 from 137.22 at 152.66. However, for the shift to lead to a bullish trend, the price must start making higher highs and lows. That means a break above the 150.75 resistance level. Otherwise, the price might start a period of consolidation near the 150.00 key level.

Conclusion

In conclusion, the USD/JPY pair is currently at a strong resistance level and is expected to move downwards. Traders should keep an eye on the pace of the decline in the Japanese yen. The interest rate differential between the policy rates of the Federal Reserve and the Bank of Japan (BoJ) is an important influence on the USD/JPY exchange rate.

USDJPY H4 | Falling to Fibo confluence supportUSDJPY is falling towards a pullback support and could potentially bounce off this level to rise towards our take-profit target.

Entry: 150.433

Why we like it:

There is a pullback support that aligns with a confluence of Fibonacci levels i.e. the 38.2% retracement and the 61.8% projection levels

Stop Loss: 149.740

Why we like it:

There is a level that aligns with the 100.0% Fibonacci projection level (keeping a relatively tight Stop Loss due to potential intervention measures by the BoJ)

Take Profit: 151.703

Why we like it:

There is a swing-high resistance level

Please be advised that the information presented on TradingView is provided to Vantage (‘Vantage Global Limited’, ‘we’) by a third-party provider (‘Everest Fortune Group’). Please be reminded that you are solely responsible for the trading decisions on your account. There is a very high degree of risk involved in trading. Any information and/or content is intended entirely for research, educational and informational purposes only and does not constitute investment or consultation advice or investment strategy. The information is not tailored to the investment needs of any specific person and therefore does not involve a consideration of any of the investment objectives, financial situation or needs of any viewer that may receive it. Kindly also note that past performance is not a reliable indicator of future results. Actual results may differ materially from those anticipated in forward-looking or past performance statements. We assume no liability as to the accuracy or completeness of any of the information and/or content provided herein and the Company cannot be held responsible for any omission, mistake nor for any loss or damage including without limitation to any loss of profit which may arise from reliance on any information supplied by Everest Fortune Group.

Yen Weakens against Dollar as BOJ Adjusts Monetary PolicyThe Japanese yen weakened beyond 151 against the mighty dollar, thanks to the Bank of Japan's (BOJ) recent adjustments to its monetary policy.

The winds of change are blowing in our favor, and it's time to seize this moment and take action! By going long on USDJPY, we can potentially capitalize on this favorable market trend and secure significant gains. The BOJ's limited adjustments to their monetary policy have created a fertile ground for us to explore and maximize our profits.

Why should you consider going long on USDJPY, you ask? Well, let me break it down for you:

1. BOJ's Monetary Policy Adjustments: The BOJ's recent tweaks to their monetary policy indicate a shift towards a more accommodative stance, which typically leads to a weaker yen. With the yen already breaching the 151 mark against the dollar, this provides an excellent opportunity to ride the wave of yen depreciation.

2. Favorable Dollar Strength: The US dollar has been flexing its muscles lately, exhibiting strength against various major currencies. By pairing it with the weakened yen, we have a powerful combination that can potentially amplify our gains.

3. Potential for Increased Volatility: As the yen weakens and the market reacts to the BOJ's policy adjustments, we can expect increased volatility in the USDJPY pair. For experienced traders like us, volatility often translates into profitable opportunities.

Now, it's time for action! Take advantage of this exciting market development and consider going long on USDJPY. Remember, the key to success lies in seizing opportunities when they arise, and this is undoubtedly one of those moments.

As always, remember to conduct thorough research, employ proper risk management strategies, and consult with your trusted financial advisor or broker before making any trading decisions.

Wishing you fruitful trades and a prosperous journey in the forex market!

Ready to ride the wave of yen depreciation? Don't miss out on this incredible opportunity! Take action now and go long on USDJPY to potentially maximize your profits. Remember, the forex market waits for no one, so seize the moment and make your move today!

Heavy Dollar news day tomorrowWhat an insane session for USDJPY! We know the ExMo is low due to the compression we've seen, but even compared to more normalised figure, what we've seen today has broken all expectations.

There are two questions going forward. The most immediate is the Dollar news we have scheduled for Nov 1st. Those being ADP at 12:15pm London (due to daylight savings) followed by the Fed rate decision at 6pm. The second is whether or not the BoJ have any other tools to alleviate the Yen weakness other than simply intervening like we've seen before.

Let's tackle the new first. I wouldn't expect ADP to cause much of a stir given the Fed decision always overshadows anything else, and if the Fed holds at 5.50%, then I wouldn't expect anything other than a small bump. Given the move we've seen today I think some form of relax to happen, possibly with a slight downward trajectory for profit taking....possibly we just slide a little lower into the end of the week?

As for the BoJ, I'm nervous above 150.

I'll take it a day at a time above here and be mindful of any macro factors that change the longer term outlook for either the Dollar or Yen. But it seems like the only mechanism Japan has to stop the devaluation is to inject a whole bunch of money into buying the Yen.

Be careful out there and I'll see you tomorrow.

ZARJPY: My Bearish Speculation Against The JPY Carry TradeWe have some Bearish Divergence on the ZARJPY, but the main reason I entered this trade was to speculate against the JPY Carry Trade and front-run the potential flight we may get back to the Yen if Japanese Yields were suddenly to go up or even become uncapped during the BoJ meeting tonight.

I could have shorted EURJPY, GBPJPY, AUDJPY, or USDJPY instead, but I feel ZARJPY may give a more violent reaction as it is a currency that has generated some of the highest yields vs the JPY thus far, and if that yield were threatened, I think it would move down quite fast compared to the other pairs.

I guess as a side note: This might end up being a Bearish 5-0 in the long run.

USD/JPY holds below 150 ahead of BoJ meetingThe Japanese yen is drifting on Monday after pushing the US dollar back below 150 on Friday. In the European session, USD/JPY is trading at 149.71, up 0.05%.

The Bank of Japan holds its two-day meeting beginning on Monday and there's plenty of anticipation around the meeting. BoJ meetings were once dreary affairs that barely made the news, but that has changed in the era of high inflation.

The central bank has been an outlier with its ultra-loose monetary policy, insisting that inflation has been transient. The BoJ recently tweaked its yield curve control (YCC) program, widening the trading band for 10-year Japanese government bond yields to 1%, which sent the yen sharply higher.

There is pressure on the BoJ to again raise the trading band as yields have risen close to 0.90%. The surge in US Treasury yields has widened the US/Japan rate differential, which has weakened the yen. If the BoJ does not take any action at this meeting, the yen could weaken further, raising the risk of Tokyo intervening in the currency markets.

One move the BoJ is expected to take is to revise upwards its quarterly inflation forecasts. The latest Tokyo Core CPI reading rose from 2.5% to 2.7% y/y, an indication that underlying inflation remains sticky. If the BoJ does raise the inflation forecasts, it would signal a move toward monetary policy normalization, which could shore up the struggling yen.

The Federal Reserve has sounded hawkish about inflation and received support for its stance from Friday's core PCE price index, which rose 0.3% in September, up from 0.1% in August and the highest level in four months. There are some inflation risks heading into next year, but the markets have priced in pauses in the November and December meetings.

149.05 and 148.45 are providing support

There is resistance at 149.91 and 150.51

AUDJPY: Big week for JPY Yen this weekThere's talk of the BoJ lifting the limit on yields to 1.5% from 1% this week, which would be a very strong catalyst for the Yen to start showing some strength.

We can see that this pair does not have any direction at the moment, trading in a flag pattern, but I don't see this as either bullish or bearish at the moment.

I'm not sure how or when or if to trade this but monitoring, my idea is based on BoJ protecting its currency generally, I am seeing the Aussie getting stronger so think we'll go up before coming back down, let's see...

NZDJPY: Back at strong supportLooking at this pair I'm expecting another bounce from support, I'm cautious as not overly confident in New Zealand Dollar out-performance in the coming weeks, but I'm still seeing the Yen struggling against many crosses.

I think we'll be into a sideways movement for the next few sessions and so for this week I'm looking for a signal on the LTF to go long.

USD/JPY edges lower, Tokyo Core CPI risesThe Japanese yen has steadied after three straight days of losses. In the European session, USD/JPY is trading at 150.11, down 0.19%.

Tokyo Core CPI climbed 2.7% y/y in October, above 2.5% in September which was also the consensus estimate. The index, which excludes fresh food is a key indicator of inflation trends in Japan and is closely monitored by the Bank of Japan. Tokyo's headline CPI also rose in October, from 2.8% to 3.3%.

The Bank of Japan will find it hard to ignore these hotter-than-expected inflation readings. The timing of these releases is awkward for the BoJ, which holds its policy meeting on Oct. 30-31. Underlying inflation is proving to be stickier than expected and BoJ policy makers may have to revise upwards their inflation outlooks for 2023 and 2024. High inflation is a risk to Japan's recovery, putting pressure on the BoJ to make some kind of move at the meeting.

The central bank will have a busy agenda at next week's meeting. Aside from stubbornly high inflation, the BoJ will have to decide whether to tweak its yield curve control (YCC) program and what to do about the falling yen. The Japanese currency breached the symbolic 150 line this week for the first time since October 3rd, raising speculation that the BoJ could shift its policy or even intervene in the currency markets.

Tokyo has responded to the yen breaching 150 with the usual verbal intervention, warning investors not to sell the yen. The BoJ won't be providing any advance warning about a currency intervention, so traders should remain on alert.

For those doubting US exceptionalism, the superb US GDP of 4.9% in the third quarter was proof in the pudding of a robust US economy. This was the fastest growth rate since Q4 of 2021, boosted by strong consumer spending in the third quarter. The sharp rise in growth hasn't changed market expectations with regard to rates, which have priced in pauses at the November and December meetings.

USD/JPY is testing support at 1.5017. Below, there is support at 149.67

There is resistance at 1.5049 and 1.5099

NZD slides against the Japanese YenThe New Zealand Dollar (NZD) is trading bearish against the Japanese Yen (JPY) at 87.386 on Friday, October 27, 2023, following comments from Japan's Chief Cabinet Secretary Taro Matsuno that the Bank of Japan (BoJ) is expected to conduct appropriate monetary policy.

Matsuno's comments come amid rising expectations that the BoJ will eventually tighten monetary policy in response to rising inflation in Japan. The BoJ has been maintaining an ultra-loose monetary policy stance for many years, but this has led to a significant weakening of the JPY in recent months.

The NZDJPY currency pair has been under pressure in recent weeks as investors have priced in the possibility of a more hawkish BoJ. The pair has fallen by over 5% since the start of October.

The bearish outlook for NZDJPY is further supported by the technical outlook. The pair has broken below a key support level at 88.00, and is now on track to test the next support level at 86.50.

Factors Weighing on NZDJPY

There are a number of factors weighing on NZDJPY at present, including:

Expectations of BoJ tightening: The BoJ is expected to be one of the last major central banks to tighten monetary policy, which is putting downward pressure on the JPY.

Rising inflation in Japan: Japan's inflation rate has been rising in recent months, which is putting pressure on the BoJ to tighten monetary policy.

Global risk aversion: Global investors are currently risk averse, which is leading to a sell-off in riskier assets such as the NZD.

Weak New Zealand economic data: The New Zealand economy has been slowing in recent months, which is weighing on the NZD.

Technical Outlook for NZDJPY

The technical outlook for NZDJPY is bearish. The pair has broken below a key support level at 88.00, and is now on track to test the next support level at 86.50. If NZDJPY breaks below 86.50, it could fall to 85.00 or even lower.

Trading Strategy

Traders who are bearish on NZDJPY could consider shorting the pair at current levels. A stop loss could be placed above the recent high at 88.00. A profit target could be placed at 86.50 or 85.00.

It is important to note that the foreign exchange market is volatile and prices can move quickly. Traders should always use risk management techniques when trading currencies.

USDJPY: Thoughts and Analysis Today's focus: USDJPY

Pattern – Ascending Triangle Break (BoJ Intervention?)

Support – 149.28 - 148.43

Resistance – 149.90 - 150.16

Hi, and thanks for checking out today's update. Today, we are looking at the USDJPY on the daily chart.

Speculation continues as to whether we will see intervention from the BoJ as the USDJPY continues to trade above 150. Currently, the breakout of an ascending triangle pattern yesterday continues to confirm today as buyers continue the run above 149.90 resistance and 150.

Pricewise, things look firm on the buyer side, but will we see any surprises today with BoJ intervention? Last time price was above 150, we saw a 1.75% decline. Could another round be on the cards if prices contnue to push higher?

Good trading.

USDJPY: The Short - when??I think that retail traders in the main are expecting this pair to crash from 150, I have been, and it may well do (as per my related idea below)...

Commentators and past experience suggests that the BoJ will intervene around 150 to 151.5 because they have to, due to the debt relationship with the USA, they're stuck between a rock and a hard place.

We all know what happens when retailers think they know best...I'm starting to think that we'll push higher to 154 before the dump.

I think the current global conflict will help the USD get there, but that level will be unsustainable for Japan so will come back down with a bang.

In the meantime I'm still day trading up and down and catching some moves on this pair, but I'm starting to think the big one is a little way off yet, let's see...

USDJPY nearing 150 again! Overview

USDJPY is nearing the 150 handle again. The Bank of Japan (BOJ) may intervene, creating lucrative JPY buying opportunities.

The Details

The Yen is weakening. The JPY Currency Index ( TVC:JXY ) has the Yen at all-time lows. The last time the Yen was this weak was in September and October 2022; the BOJ intervened in the FX markets to strengthen the Yen—sharp moves of 500 pips formed in hours!

USDJPY is back at the 2022 intervention levels. On the 3rd of October 2023, it is suspected that the Bank of Japan (BOJ) intervened to strengthen the Yen, which formed the 'BOOM' move identified on my chart. The intervention caused a bearish move of 300 pips.

In the coming days, USDJPY may reach the 150 handle again. The BOJ has two options:

Further Intervention - The BOJ may continue with FX intervention. This could bring a bullish shock to the Yen, especially USDJPY, like in October 2022. Expect a move of 400 to 600 pips to the downside on USDJPY. Maybe more. Maybe less. This could be followed by further JPY buying.

Interest rates - The BOJ may move away from negative interest rates. A rate change is BIG news for the Yen. Possibly, the Nikkei also. This is significant because monetary policy shifts from negative to zero or even negative to positive rates. This change could end the JPY selling and mark highs on the USDJPY chart.

Either option, the JPY weakness, especially short-term, is ending.

Things to consider:

Beware of slippage. The initial move will likely be quick and sharp, causing significant slippage on JPY orders.

If you catch the wrong side of the move, you could blow your trading account if you are over-leveraged and over-exposed.

The swap rate on holding the Yen is terrible, especially USDJPY. So, USDJPY Put Options or trading the JPY currency index may be better than spot FX.

Excessive and volatile moves against the Yen could be the catalyst that brings intervention rather than USDJPY reaching critical levels.

USDJPY may reach the 155 handle before the BOJ take action. My area of focus is 150 to 155.

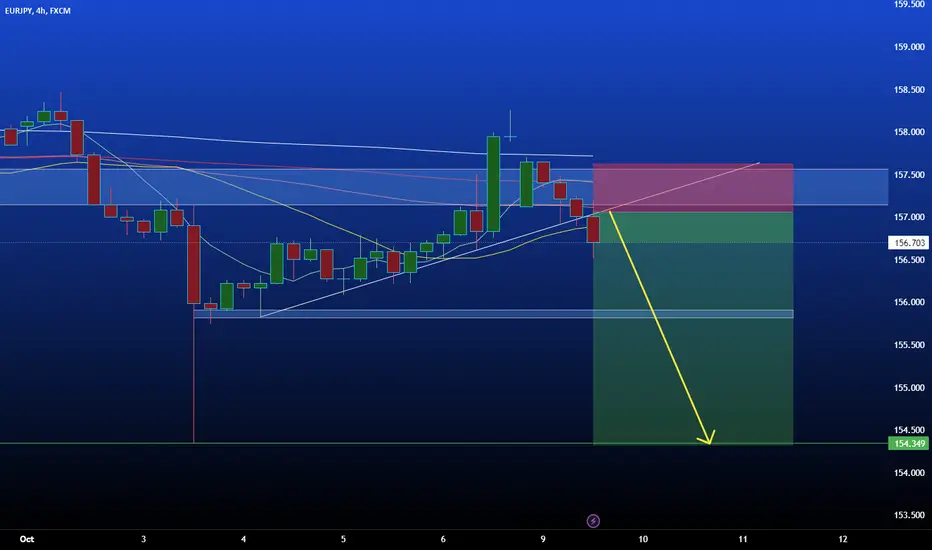

EURJPY: Price gone higher than expected for a better entry.Price moved a lot higher to fill the overnight gap down.

My idea yesterday became invalid but this gives me a better entry:

Gap down suggests general direction and now the gap has been filled, supported by a pinbar on the 1hr I'm getting in short with a first TP at 156 (ultimately I think 154), but I think this could be the start of the reversal.

AUDJPY: Is this the start of the reversal?We saw some JPY strength last week and I think we could be starting to see reversal, however my confirmation of this will be below 93 support.

Even though BoJ hasn't intervened yet, there was a lot of buying in the week which we saw against the USD, I still expect BoJ intervention soon.

Nice pinbar rejection on the 4HR from my resistance block.

Looking for a short here on LTF's, but with tight SL and will keep it following any move down.

EURJPY: Finally ready to reverse?EURJPY has been hanging around 157 - 157.5 range for some time, we saw a break below last week which quickly recovered, but we've broken back below now so I expect a stronger push back down to the low of last week (caused by JPY buying).

With price action there was also a failure to make a new high, we saw a short pinbar on the 4HR before we broke back below my resistance block.

I see this happening again as the BoJ look to defend their currency, I'm expecting JPY to start to perform well across the board - they may not provide any interest but their inflation is low and their economic performance is looking ok to me to, and also money flows and so a reversal should be coming soon.

I also think the EURO is in trouble, with stagflation, this will lead to recession imo and will hit the EURO so this is one of the JPY crosses I'm expecting big declining moves from.

Yen Drops Below 150 Per Dollar - Exercise Caution in TradingThe Japanese yen has recently dropped below the critical threshold of 150 per dollar, primarily due to mounting concerns regarding intervention measures. In light of this situation, I strongly urge you to exercise caution and consider pausing yen trading until further clarification is obtained.

The sudden decline in the yen's value has raised concerns among market participants, as it suggests the possibility of intervention by the Japanese government or central bank. Intervention refers to deliberate actions taken by authorities to influence their currency's exchange rate, typically through buying or selling large amounts of their own currency in the foreign exchange market. Such interventions can have a profound impact on the currency's value and create significant volatility in the market.

Given the uncertainty surrounding the current situation, it is prudent to reassess our trading strategies and ensure that we are not unnecessarily exposed to potential risks. Therefore, I strongly recommend that you temporarily halt yen trading until we receive further guidance or clarification from reliable sources regarding any potential intervention measures.

In the meantime, I encourage you to closely monitor the latest news and market developments related to the yen. Stay informed about any official statements or actions from the Japanese government or central bank, as these can provide valuable insights into the future direction of the currency. Additionally, consider diversifying your portfolio to reduce reliance on yen-based assets until the situation stabilizes.

Please remember that our primary objective is to protect our investments and mitigate risk. By exercising caution and temporarily pausing yen trading, we can better position ourselves to navigate the current market uncertainties and make informed decisions when clarity emerges.

If you have any questions or require further guidance, please do not hesitate to reach out to me or our dedicated support team. We are here to assist you and ensure that you have the necessary information to make well-informed trading decisions.

So this happened on the USDJPY overnightThe USDJPY crept over the 150 price level before crashing down almost 300 pips to retest the 22nd September swing low and 61.8% Fibonacci retracement level at the 147.40 price level.

Eventually, the price settled along the 149 price level and back within the bullish channel.

The 150 price level is significant as it was likely the BoJ's price level for an intervention. This move could be viewed as the first stealth intervention as the Ministry of Finance did not confirm the intervention.

Is this going to be a repeat of the series of BoJ interventions we saw in October 2022?

USDJPY: My next 2 moves as I expect BoJ to defend their currencyI'm expecting USDJPY to carry on meandering towards the 150 mark, and it's at this level that we've previously seen BoJ step in to defend their currency,

We saw the same in June / July 2022, and I think we'll see it again.

BoJ has started hinting at a change to monetary policy for the first time in a long time, we saw a very small reaction in the past week to this, but right now the dollar is too strong for this to have made a difference.

I'm expecting DXY to retrace from current levels and this cross could be a big beneficiary if BoJ do what I think, it's always good to trade strength against weakness.

There could well be some little long scalp opportunities for me (with very very tight SL's moving to BE asap) on the way up to 150 (within the rising wedge) as that's still some good pips away, but for me the bigger moves now will be to the downside.

I'm not planning on getting caught with any longs up here...

This is a big news week for this pair with FOMC on Wednesday and BoJ interest rate decision and conference Friday, will be interesting to see how this all pans out ahead of these fundamentals, but beyond them I'm expecting things to play out as per this idea.

I've plotted two moves, first from the 150 ish mark down to support, and then another sell down to the rising long term trendline.

USD/JPY rebounds, US GDP, Tokyo Core CPI nextThe Japanese yen has stemmed a 3-day slide, in which it declined around 1.5% against the US dollar. In the European session, USD/JPY is trading at 149.31, down 0.23%. In the US, third estimate GDP for the second quarter is expected to be revised lower to 2.1%.

Japan will release Tokyo Core CPI on Friday. The core rate, a key inflation gauge, is expected to ease to 2.6% y/y in August, down from 2.8% y/y in September. Core inflation has remained above the Bank of Japan's 2% inflation target for 15 consecutive months, which seems to indicate broad inflationary pressure. Still, Governor Ueda has said he will not phase out massive monetary stimulus, arguing that wages need to rise in order ensure that inflation remains sustainable around 2%. Japan's weak economy is making it easier for the BoJ to maintain its ultra-easy policy, and Friday's inflation release won't change the BoJ's stance.

The Japanese yen has paid the price for the BoJ's insistence on maintaining an ultra-loose policy and has had only one winning week against the dollar since July. The US/Japan rate differential continues to rise as Japanese yields stay put while US Treasury yields continue to move higher. USD/JPY is close to the 150 line and could breach it shortly. This will put pressure on Tokyo to intervene in the currency markets to prop up the ailing Japanese currency.

The US dollar is having an off day against the major currencies on Thursday, but the greenback has looked sharp against the majors lately. The markets are concerned that interest rates could remain higher for longer, as the US economy has been showing signs of resilience. Oil prices have hit $93 and are contributing to higher inflation - In August, US CPI rose from 3.3% to .3.7%. The futures markets have priced in a rate hike before the end of the year at 36.5%, which means the markets are uncertain if interest rates have peaked.

There is resistance at 149.19 and 149.93

USD/JPY tested support at 148.79 earlier. Below, there is support at 148.05