Opened Mar29 Apr20 169P 177C double calendar on 3/13/18www.tradingview.com

IV rank a little high on this

max risk is the debit until the front month expiration

debit 2.36

Theta 3.54

Underlying price when opened 173.20

Upper and Lower expected move 167.70 176.90

break evens 167 and 180 gives a little more room above

With the break even points being clearly outside of the expected move (per implied volatilty which is often overstated anyway) this trade has a high probability of profit. I will close it before expiration no matter what. www.tradingview.com

Calendarspread

Neutral double calendar Earnings 49P 56C mar23 mar29www.tradingview.com

Trying out this strategy for earnings tomorrow, when sets up with good IV spread the crush should profit what is typically considered a bought spread.

Direction is not an issue, only that the break-even points are outside of recent earnings moves. This setup goes as wide as possible without letting the belly of the profit/loss go below the trade expenses (commission and fees). This one usually moves so should settle in profit and the cost or max loss is minimal when closed before the short, front week expiration. The intention is to close as soon as the vol crush occurs unless movement is taking it more profitable at the moment.

The main analysis involved is checking the last several earnings moves so that all or most of them are within the break evens of the setup. So it is a sort of trend analysis looking at the trends/history of earnings moves.

This stocks options become reasonably liquid at earnings time so the fills in closing should not kill the trade. I have looked at several of these over the past few weeks and seems clear when good or bad trade. Now to place live trades and get the real learning (in the muscles) by doing. If these work out will post more with clearer entrance guidelines. Hard to find a better probability of profit or reward to risk ratio.

Sunday night parameters:

Stock price 52.27

debit of double calendar spread ~0.12 ($12 per contract) depending on fill

Theta $3.60

break-even points (conservative, actually small profit) ~ 47.50 and 58.50

max loss $12 plus expenses

projected (IV adjusted for post crush) belly of p/l return (zero price movement from earnings) ~ $4

max profit at the strikes of the legs: $43 at 49 strike and $53 at 56 strike

Opening Nov17 Short 259.5C and 256P Long Nov24 260.5C & 255P Double Calendar spread actually a tiny bet on little movement of SPY before Friday

Debit $20/contract.

Theta 14

Will take the short legs off with any sign of price jumping or within 2 days. A big price jump without the short legs could improve the profit so will be watching this closely and out by Friday.

This time leverage can be powerful, that 14 Theta is because the longs will lose around 11 while the shorts are losing 25 in a day netting $14/day (here's the hitch, true if all else stays the same). An up move without the shorts will profit quickly but a down move even more so as the volatility should pop up increasing the value of the longs that I will be selling to close. We will see. Thanks for looking and keep smilng!

Opening CAT Oct 6 Nov 17 125 Put Calendarwww.tradingview.com

This is what I call a Ecalendar for pre earnings announcemnet calendar spread to take advantage of the volatility expansion that occurs somewhere from 30-45 days before an earnings binary event. CAT is one of many that pops up (the IV) like a gear tooth in a clear pattern; my goal is to place the trade before the pop and profit from the rise in premium.

For the week or three that this should approach target the ideal is no price movement - so I chose category support and resistance but in honesty the price history has little importance to me on this type of trade. The important characteristics I want are high option volume, high open interest and low premium bid/ask spread in those expiries that I may roll through before final exit (in short liquid open contracts).

Trade Price: $3.00 ($300 per contract)

My target profit for this trade: .37 ($37/contract) This is a preset closing order and is reset for that amount after rolling either leg as well.

The trade is defined risk and that is the only loss management involved (no stop loss orders).

Theta 0.62

Delta -4.21

CAT price at open of position: $124.38

MSFT Options - Opening Sep22 Oct20 Put Calendar 72.5www.tradingview.com

It is right around the time that the volatility may expand pre-earnings (E announce in about a month). This trade will benefit if volatility does indeed expand.

Typical historical IV expansion is about 50%, this kind of boost can override a lot of price movement - msft price when it moves tends to run up prior to earnings which could allow one or more rolls of the short leg, all of the weekly possibilities have decent liquidity for that. Let's see what happens!

Calendar

short Sep 22 72.50 Put

long Oct 20 72.50 Put

debit .63 ($63/contract)

Theta .71 Delta -10.2

Opening IWM Sep 15 Oct 20 136 Put Calendar Spreadwww.tradingview.com

Often do but have not had a position in IWM lately so here goes. A little movement could favor this trade but it is mostly neutral.

I have drawn a daily trend line and am using 3 indicators - trying out updates to Williams percentR and a new Pivot HighLow and will update/publish

after trading with them a while. While having fun with indicators I mostly believe that flipping a coin 2 out of 3 would be nearly as accurate in that

nothing an indicator tells us has any effect on what the price will do tomorrow.

8-16-17 Open Sep 15 Oct 20 136 Put Calendar debit 1.46 ($146) 1 contract. Will trade the short and long each to reduce the debit/break-even and record

the updates here. Spot at open 137.70, Theta .7 and delta -7. Thanks to user NaughtyPines for great examples of this kind of trade.

CL continuation from last ideathis is the trade i will be looking at, instead of one shown is last published idea, due to the extra time it provides me. The last one used up to much of the front month

RUT Put Calendar (Volatility Play)With the moved down in volatility the last couple of days and RVX (Russell Volatility Index) almost at the year lows a Put calendar seems like a pretty safe bet. I will be buying the Nov 1230 Put and selling the Oct 1230 Put. Looking to close it early as soon as we get a volatility spike.

Double Calendar on Gold looking for a volatility spike.After 80 plus days in a sideways move consolidating, we are right at a point where Gold can start to move. With volatility at the lows, a good strategy would be to buy a double calendar to take advantage of any strong move that will make volatility expand. I will be buying the Dec 1365 Call and 1295 Put, and Selling the Nov 1365 Call and 1295 Put.

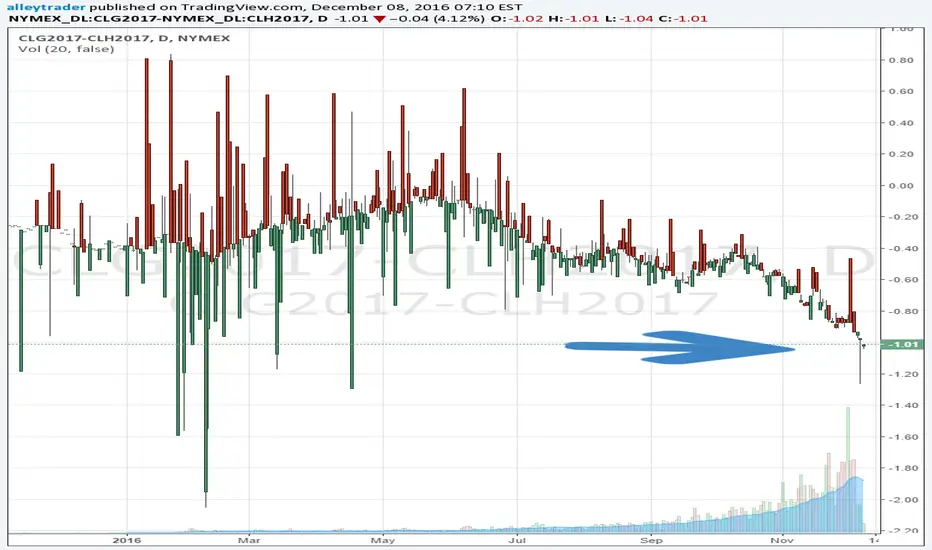

oil calendar longneutral direction trade counting on the spread to narrow,

Keep in mind the buying power required for most of the pairs trades and take profits early, due to long Buying power required the ROI will be strong

Apples are ripe and sweeter on top Possible rally?? Shorting until support develops. Long entry may be at the support retest/bounce.

Long term soy bean contract spread narrowingThis trade is to try and take advantage of my thinking that the price between the two contracts will become less. This trade could see a large loss, before we see gains, but has a nice margin relief.