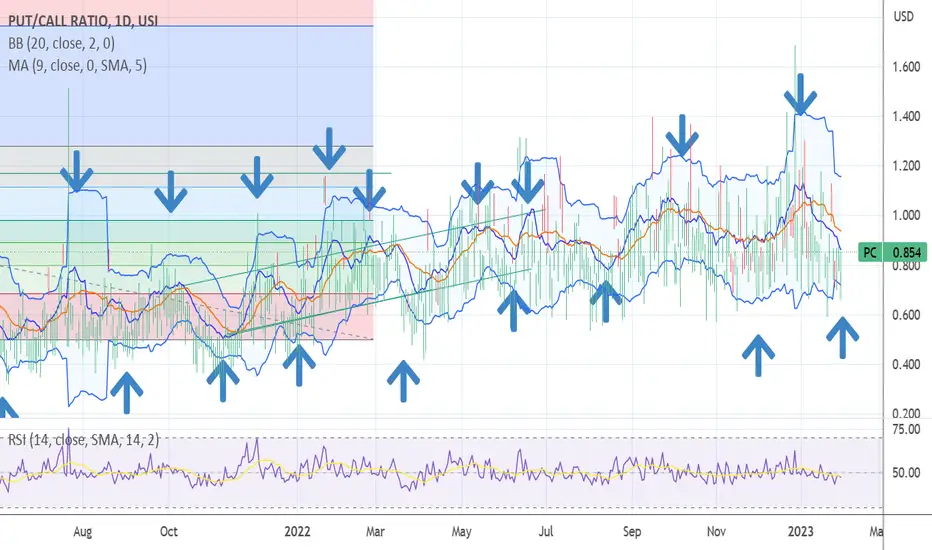

PUT CALL SIGNALS 20DAY/10DAY Chart posted is that of the 20 day and 10 day put call signal we are reaching a level to be net long PUTS and SHORTING

CALL

REGN Regeneron Pharmaceuticals Options Ahead of EarningsLooking at the REGN Regeneron Pharmaceuticals options chain ahead of earnings , I would buy the $730 strike price Puts with

2023-2-17 expiration date for about

$16.53 premium.

If the options turn out to be profitable Before the earnings release, I would sell at least 50%.

Looking forward to read your opinion about it.

RITM Rithm Capital Ready for a Breakout!RITM Rithm Capital to release Q4 and full year 2022 financial results for the period ended December 31, 2022 on Wednesday, February 8, 2023 prior to the opening of the New York Stock Exchange!

2.02 EPS

4.363B MARKET CAP

10.86% DIV YIELD!!!

4.73 P/E Ratio!!!

Extremely undervalued in my opinion!

But now comes the best part! You can buy the following options:

2023-2-17 expiration date

$10 strike price

for only $0.05 premium now!

So the expiration date is after the earnings, if the stock goes to $11, and i wouldn`t be surprised if the results are great, then this is a 20X call that you are reading about.

This is a premium call in my opinion, do you research before investing, as you know!

LMT - MyMI Option PlayLockheed Martin not only landed on a fundamental price level today (The price that it was at before Covid March 2020 Market Crash), but it also acquire roughly a $1B in Volume total, 2nd to JNJ. We like it for the continue concerned across seas that seem to be gaining more and more tension. Whether it's Ukraine/Russia or the worries in Asia, we will be looking to place some CALLs (ITM) to hold at least back to $458 to confirm that a Support to Resistance Conversion is not being completed.

If so, Lockheed could potentially lose support at the $440 Levels and move back down below the 410-420 Price Levels

Regardless, we will be playing options to create a new positioning moving forward.

DAL Delta Air Lines Options Ahead of EarningsIf you haven`t bought DAL at my last call:

then you should know that looking at the DAL Delta Air Lines options chain ahead of earnings, I would buy the $35 strike price in the money Calls with

2023-1-20 expiration date for about

$1.79 premium.

If the options turn out to be profitable Before the earnings release, i would sell at least 50%.

Looking forward to read your opinion about it.

CALM Cal-Maine Foods Options Ahead Of EarningsAfter the last price target was reached:

Now looking at the CALM Cal-Maine Foods options chain ahead of earnings , i would buy the $60 strike price Calls with

2023-1-20 expiration date for about

$5.70 premium.

If the options turn out to be profitable Before the earnings release, i would sell at least 50%.

Looking forward to read your opinion about it.

levels for banknifty[

b]important levels for bank nifty

>trade wisely and carefully and don't forget to place stop-loss its just an idea

>follow for more content like this bcoz this motivate me for posting more and more content like this

thankyou

NSE:BANKNIFTY1! :BANKNIFTY"]NSE:BANKNIFTY

DOCU DocuSign to test its last supportIf you haven`t shorted DOCU DocuSign, Inc. here:

Then looking at the DOCU DocuSign options chain, i would buy the $45 strike price Puts with

2022-11-18 expiration date for about

$3.90 premium.

Yes, i think it can test its last support this year.

Looking forward to read your opinion about it.

Another bounce? Based off the previous resistance the candlestick from last week broke above closing above. This could be a good sign however it may be time to retrace a bit to bounce off that new support. Patiently waiting is all I can say. We are in the long run for this one but definitely see potential in $$$ falling from the sky. I’ll keep you guys updated.

ORCL Oracle Corporation Options Ahead Of EarningsIf you haven`t bought the last breakout before the earnings:

Then you should know that looking at the ORCL Oracle Corporation options chain ahead of earnings, i would buy the $78 strike price Puts with

2022-12-30 expiration date for about

$2.49 premium.

If the options turn out to be profitable Before the earnings release, i would sell at least 50%.

Looking forward to read your opinion about it.

PATH UiPath Inc. Options Ahead Of EarningsLooking at the PATH UiPath Inc. options chain ahead of earnings , i would buy the $15 strike price Calls with

2023-2-17 expiration date for about

$0.90 premium.

If the options turn out to be profitable Before the earnings release, i would sell at least 50%.

Looking forward to read your opinion about it.

S SentinelOne Options Ahead Of EarningsLooking at the S SentinelOne options chain ahead of earnings , i would buy the $19 strike price Calls with

2023-3-17 expiration date for about

$1.40 premium.

If the options turn out to be profitable Before the earnings release, i would sell at least 50%.

Looking forward to read your opinion about it.

AMC Bull Flag BREAKOUTAMC has finally broken out of a multi-day bull flag and is headed to $10 or higher. 12/2 $10 calls is what I would buy and I’d sell at one of the Fibonacci take-profits targets or a solid reversal on the 15m chart with Heikin Ashi Candles next Week or Friday. Enjoy‼️

BBY Best Buy Options Ahead Of EarningsLooking at the BBY Best Buy options chain ahead of earnings , i would buy the $73 strike price Calls with

2022-11-25 expiration date for about

$2.79 premium.

If the options turn out to be profitable Before the earnings release, i would sell at least 50%.

Looking forward to read your opinion about it.

JD Options Ahead of EarningsLooking at the JD options chain ahead of earnings, i would buy the $47 strike price in the money Calls with

2022-11-18 expiration date for about

$8.50 premium.

If the options turn out to be profitable Before the earnings release, i would sell at least 50%.

Looking forward to read your opinion about it.

AAL American Airlines Options Ahead Of EarningsLooking at the AAL American Airlines options chain, i would buy the $15 strike price Calls with

2022-11-18 expiration date for about

$0.46 premium.

Looking forward to read your opinion about it.

FTCH Farfetch Limited Options Ahead of EarningsLooking at the FTCH Farfetch Limited options chain ahead of earnings , i would buy the $11strike price Calls with

2022-12-16 expiration date for about

$1.17 premium.

If the options turn out to be profitable Before the earnings release, i would sell at least 50%.

Looking forward to read your opinion about it.

PM Philip Morris Options Ahead Of EarningsLooking at the PM Philip Morris options chain, i would buy the $90 strike price Calls with

2022-11-18 expiration date for about

$1.69 premium.

Looking forward to read your opinion about it.

CVXUSDT LONG IDEACVX Swing Long Idea:

Entry Zones:

- EP 1 = 4.7496

- EP 2 = 4.7026

- EP 3 = 4.6669

TP Zones:

- TP 1 = 7.2039

- TP 2 = 7.4992

- TP 3 = 7.7380

- TP 4 = 7.9767

STOP LOSS = 4.450

* If the price goes down below 4.6265, please invalidate this analysis.

BAKEUSDT SHORT IDEABAKE Swing Short Idea

Entry - 0.2293

TP - 0.2080

SL - 0.2360

* This trade will give you approx. +9% ROI times your leverage upon TP completion. Set your entry as limit order and entry with confirmation

XRPUSDT LONG IDEAXRP Swing Long Idea

Entry - 0.4763, 0.4678, 0.4579, 0.4507

TP - 0.5798, 0.5713, 0.5628, 0.5522

TP (Impulsive) - 0.6469, 0.6301, 0.6133, 0.5926

SL - 0.4401, 0.4168

Bearish Divergence Trigger - 0.56

go Long JEPI for alt Strat & monthly incomeThis is exactly the strategy to employ at market tops. You want broad market exposure along with some different alternative strategy funds in your portfolio to complement your trades.

This ETF has a very interesting strategy and it has just launched. I would not worry about the track record for the construction is solid, low expense ratio 0.35%, a dividend yield of 8.34%. It's composed of a wide variety of high-quality, low volatility stocks while also selling calls.

I took a look at the holdings and they include some NDX and some SPX names. It gives you a wide variety of exposure from Chubb and Deere to Elly Lilly and Google, and it appears currently they are selling calls against the SPX. So this, combined with the monthly payout of a dividend and the hedge it provides gives you income and stability. The dividends can either be reinvested, spent, or use for new opportunities.

UPS United Parcel Service Options Ahead of EarningsMy recent experience with those global package delivery companies was extremely painful. The have raised their prices a lot, on some occasions you pay the same price to send something to another country than taking the trip yourself and deliver that package in person.

So i have tried to avoid UPS, like many of you, and go for smaller unknown companies. I think this attitude will reflect in the upcoming earnings.

Looking at the UPS United Parcel Services options chain, i would buy the $160 strike price Puts with

2022-11-4 expiration date for about

$4.85 premium.

Looking forward to read your opinion about it.