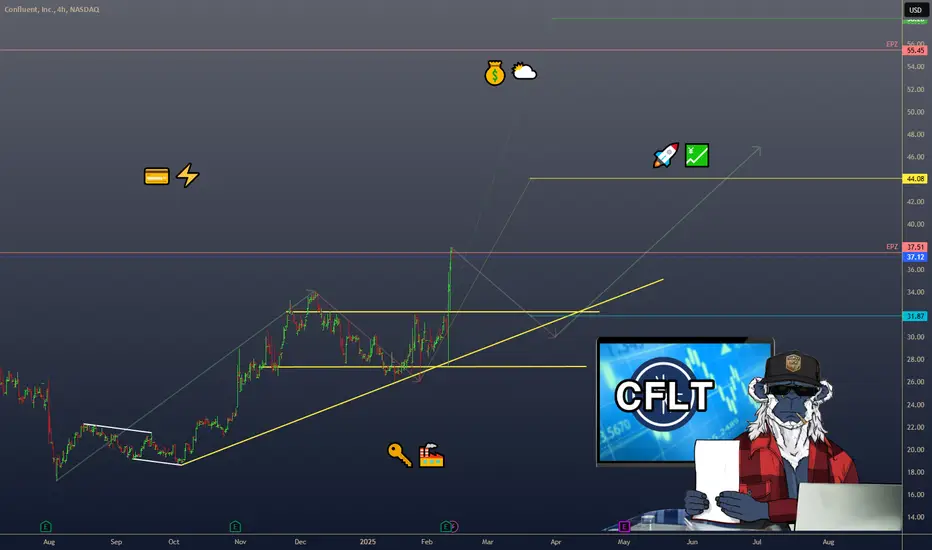

Moonshot Ideas $CFLT > $40- We are entering era of Agentic AI which requires real time data and agent decides to take an action on that event in near real time.

- Confluent valuation is so cheap in a massive TAM and an exploding tailwind of AI Agents. I am seeing all the tech companies and startups are building AI Agents and apetite for real time data streaming capability, processing is required.

- NASDAQ:CFLT need to ride this wave and one way they could do is by making Apache Flink to natively support Python instead of just relying on Java. If they build sdk, python library which could do the heavy lifting when it comes to stream processing, transformation then NASDAQ:CFLT would be number one choice and popular among growing Python community and ML community.

- I wouldn't be surprised to see NASDAQ:CFLT well above 60 dollars in next 2-3 years.

CFLT

$CFLT will break $35 range if Q1 | FY 2025 is good- NASDAQ:CFLT has been range bound for two years now where the lower end is $14-18 and upper range is $35-38.

- If FY 2025, Q1 exceeds expectation of the analyst then this stock will be able to get through the long term resistance and turn it into support.

- NYSE:IOT is a peer company which operates in IOT and streaming data application layer which has shown promising results and returns. I believe NASDAQ:CFLT is a solid company and can reach $45+ comfortably.

CONFLUENT ($CFLT) – DATA STREAMING’S RISING STARCONFLUENT ( NASDAQ:CFLT ) – DATA STREAMING’S RISING STAR

1/7

Ready for a snapshot of Confluent? Here’s what’s sparking chatter on X: 23% YoY revenue growth, $0.09 EPS (beats by $0.03), and free cash flow at $ 29M—above estimates! Let’s dive in. 🚀💹

2/7 – REVENUE & EARNINGS BLAST

• Overall revenue: +23% YoY

• Subscription revenue: +24% YoY 💳

• Q4 EPS: $0.09 (est. $0.06) ⚡️

• FCF: $ 29M vs. est. GETTEX:27M 💰

3/7 – CONFLUENT CLOUD SHINES

• Cloud revenue: +38% YoY 🌥️

• Big piece of their puzzle—shows they’re nailing the cloud-based approach

• Key to future scaling & recurring income streams 🔑

4/7 – SECTOR SNAPSHOT

• Confluent competes in data streaming & management

• Growth suggests they’re keeping pace—maybe even undervalued if adoption keeps climbing 🤔

• Keep an eye on how they stack up vs. other cloud/data players like Snowflake or Datadog 🏭

5/7 – RISK ASSESSMENT

• Market Saturation: More competitors in cloud/data → potential pricing pressure 💼

• Tech Shifts: Rapid changes could leave older solutions behind 🔄

• Economic Downturn: Slowed IT budgets might delay or shrink deals 🌐

• Customer Concentration: If a few big clients leave, it stings big time 🏹

6/7 – SWOT HIGHLIGHTS

Strengths:

Strong Confluent Cloud growth (+38% YoY!)

Broader customer base (+17%) 🙌

Weaknesses:

Heavily niche in ‘data in motion’ 🤏

High acquisition costs in a crowded market 🏷️

Opportunities:

Expand into new verticals & geographies

AI/ML integration for next-level analytics 🤖

Threats:

Fierce giants with deep pockets 🦖

Regulatory changes in data privacy ⚖️

7/7 – Where do you see Confluent heading next?

1️⃣ Bullish—Cloud growth = unstoppable! 🌟

2️⃣ Neutral—Need more consistent profitability 🤔

3️⃣ Bearish—Competition is too intense 🐻

Vote below! 🗳️👇

Bullish on data streaming but CFLT to $15 for better risk/reward- While I believe NASDAQ:CFLT chart looks good and it might go to $40 after earnings in Q1 2025. But data platform infra is getting very competitive.

- First layer of competition comes from Hyperscalers like AWS, GCP and Azure which have their own variant of stream processing. Confluent had some leverage in terms of managed offering.

- I believed that company is unique, in a strong niche but stock based compensation and dilution has always been a problem.

- With volume of data, consumption based model makes sense. I liked that billing strategy over flat subscription type model as the prior one is easier to pass cost to consumers + have some margin (fixed).

Why I'm bearish on this name lately?

- I believe redpanda acquisition by Snowflake NYSE:SNOW would impede growth for NASDAQ:CFLT massively.

- Snowflake has a moat in data warehousing, they are trying to become all things data infrastructure.

- Streaming ingestion into snowflake is a capability which could have great synergy. While I wanted to see NASDAQ:CFLT acquisition by NYSE:SNOW but it is not possible as of now in my opinion as confluent market cap is 10 billion+ which could hamper NYSE:SNOW cash flows.

- Therefore, redpanda would be a better acquisition for NYSE:SNOW but it will severly impact NASDAQ:CFLT technical addressable market.

I would buy NASDAQ:CFLT under $20 because their future business is going to be impacted materialistically.

Confluent (NASDAQ: CFLT) Surges 35% on Stellar Quarterly ReportShares of Confluent (NASDAQ: NASDAQ:CFLT ) skyrocketed on Thursday, igniting a fervor among investors as the company's quarterly financial report surpassed even the loftiest expectations. With a remarkable surge of 35.4%, the stock exemplified the resilience and potential of Confluent in the data streaming and cloud market.

Unveiling a Financial Triumph:

Confluent's (NASDAQ: NASDAQ:CFLT ) fourth-quarter performance shattered forecasts, with revenue surging to $213 million, marking a remarkable 26% year-over-year increase. Fueling this impressive growth was a 31% climb in subscription revenue, propelling adjusted earnings per share (EPS) to an impressive $0.09. Analysts, taken aback by the company's stellar performance, had anticipated revenue of $205.3 million and an adjusted EPS of $0.05, making Confluent's triumph all the more exhilarating.

Confluent Cloud Soars to New Heights:

Amidst its financial triumph, Confluent (NASDAQ: NASDAQ:CFLT ) achieved a significant milestone with its first-ever quarter of $100 million in Confluent Cloud revenue, signaling a remarkable 46% year-over-year increase. Moreover, the company boasted a dollar-based net retention rate of 125%, a testament to its ability to retain and expand its existing customer base. This strategic focus on cloud services aligns with Confluent's vision of becoming a consumption-oriented business, poised to capitalize on the burgeoning $60 billion data streaming platform market.

Navigating the Path Forward:

While the third quarter had left investors apprehensive about Confluent's (NASDAQ: NASDAQ:CFLT ) transition strategy, the fourth-quarter results served as a resounding affirmation of its trajectory. CEO Jay Kreps emphasized the company's commitment to driving innovation in the data-in-motion market, highlighting Confluent's pivotal role in removing barriers and propelling technological advancements forward. With a clear roadmap ahead, Confluent is poised to capitalize on the immense opportunities within the rapidly evolving data landscape.

A Bullish Outlook:

Looking ahead, Confluent's (NASDAQ: NASDAQ:CFLT ) guidance for the first quarter and full year further solidifies its position as a frontrunner in the industry. With management forecasting revenue of $211.5 million for the first quarter and a full-year projection of $950 million, Confluent is poised to surpass Wall Street's expectations and cement its status as a market leader. As CEO Jay Kreps aptly stated, the data-in-motion market remains ripe for disruption, and Confluent stands at the forefront of this transformative journey.

Conclusion:

In conclusion, Confluent's (NASDAQ: NASDAQ:CFLT ) remarkable surge following its quarterly report underscores the company's unwavering commitment to innovation and excellence. With stellar financial results, groundbreaking achievements in Confluent Cloud, and a bullish outlook for the future, Confluent is primed for continued success in the dynamic world of data streaming and cloud technology. As investors celebrate this momentous occasion, the stage is set for Confluent to carve out a formidable presence in the data landscape, driving value for customers and shareholders alike.

CFLT Confluent Options Ahead of EarningsAnalyzing the options chain and the chart patterns of CFLT Confluent prior to the earnings report this week,

I would consider purchasing the 45usd strike price Calls with

an expiration date of 2024-4-19,

for a premium of approximately $4.35.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Looking forward to read your opinion about it.

CFLT Uptrend Rectangle pattern with BreakoutNASDAQ:CFLT Confluent, Inc. operates a data streaming platform in the United States and internationally.

Uptrend rectangle pattern, above AVWAP from Highest point and ipo day. Breakout (pivot point) ~34 with Massive 6 weeks accumaltion.

Breakout (pivot point): ~34

Target ~ 63

The Week Ahead: ARKK, KRE, GDXJ; CFLT, COIN, DASH EarningsWith broad market implied volatility having crushed out mightily over the past couple of weeks, I'm left scrounging around in the exchange-traded fund and/or (ugh) single name space for premium. There aren't a lot of underlyings with ideal IVR/IV metrics to play, but there are a few things that still have decent IV in them, even if it isn't toward the top of its 52-week range.

There isn't anything in the exchange-traded fund space as of Friday close with an IVR >50%, but there are a few with 30-day IV >35% (which is the combination of metrics I like to see). Here there are, ranked by 30-day with stuff <$20/share weekend weeded out:

ARKK 41

KRE 41

KWEB 39

GDXJ 37

USO 36

XOP 35

Pictured here is a fairly plain Jane delta neutral short strangle in ARKK in the June expiry with the short legs camped out around the 16 delta, paying 1.00 at the mid price with break evens at 30 and 43.

The KRE June 16th 37/48 short strangle (16 delta) is paying around 1.25.

The KWEB June 16th 28 short straddle is paying around 1.95. (Going 16 delta short strangle didn't end up paying much; the 26/30.5 was paying .55).

The GDXJ June 16th 35/46 short strangle (17 delta) is paying 1.04 at the mid.

The USO June 16th 60.76 short strangle (17 delta) is paying 1.65 at the mid.

The XOP June 16th 112/143 short strangle (17 delta) is paying 3.04 at the mid.

Broad Market

Ugh. Why even go here ... . Broad market exchange-traded funds, ranked by 30-day IV:

IWM 21.3%

QQQ 20.6%

EFA 16.2%

SPY 16.1%

DIA 14.3%

Bond Funds

My only observation here is to note that TLT premium is better than SPY's (as is EMB's).

EMB 20.9%

TLT 17.0%

HYG 9.5%

AGG 7.4%

And, of course, there are earnings ... . I've screened and ranked these by >50% 30-day IV, as well as for options liquidity and thrown out underlyings that are trading at <$20/share:

COIN 111.2 (Thursday after market close)

W 107

RUN 92.9

CFLT 80.9 (Wednesday after market close)

PPL 73.4 (Thursday before market open)

FOUR 72.0

DASH 70.2 (Thursday after market close)

The drawbacks to W, RUN, and FOUR involve strike to strike granularity, which is why I haven't bothered to look up their announcement days and times. W and RUN have 1 1/2 wides; FOUR, has 5-wides. Not having 1-wides can not only make setting up delta neutral a pain; it can making rolling out a pain if you have to do that to manage the trade, so I generally avoid underlyings with weak strike granularity for earnings plays that are generally just made to take advantage of the ensuing volatility contraction. I would consequently lean toward plays in COIN, CFLT, PPL, and DASH for volatility contraction plays, looking to get into

CFLT, Wednesday before market close (since it announces Wednesday after market close).

PPL, Wednesday before market close (since it announces Thursday before market open).

COIN, Thursday, before market close.

DASH, Thursday, before market close.

Preliminary Setups:

CFLT May 19th 22.5 Short Straddle, 3.60 credit, 18.90/26.10 break evens

PPL: May 19th 29 Short Straddle, 1.03 credit. (Well, that's ... weak sauce. It's possible that the platform is misreporting 30-day, so this will have to be checked during the NY session).

COIN: May 19th 45/67 Short Strangle, 3.29 credit. (A smidge pesky, since I'd want to set up my put side tent somewhere between the 45 and the 40 strike, where there aren't any strikes at the moment.)

DASH: May 19th 52/73 Short Strangle, 1.95 credit.

8/3/22 CFLTConfluent, Inc. ( NASDAQ:CFLT )

Sector: Technology Services (Packaged Software)

Market Capitalization: $8.079B

Current Price: $29.02

Breakout Price: $31.00

Buy Zone (Top/Bottom Range): $27.65-$19.45

Price Target: $33.50-$36.30 (1st), $45.10-$49.20 (2nd)

Estimated Duration to Target: 26-29d, 73-76d

Contract of Interest: $CFLT 8/19/22 30c, $CFLT 10/21/22 35c

Trade price as of publish date: $2.55/contract, $2.60/contract

US Stock In Play: $CFLT$CFLT bounced off a significant price support, an area of value with significant buying interest.

this would be the 3rd time $58 held through the 3 period of market weakness (Oct'21, Dec'21 and now)