Chinese Real Estate Large Cap IndexThis is an updated version of my previous "Evergrande + others" chart of Chinese real estate. Instead of including some smaller companies with longer price history, this focuses on large market cap companies. I weighted the prices against each other equally by their 42 day average, and then weighted that by the market cap:

1. Sun Hung Kai Properties (0016) HKD 268.5 billion -2.06% Sun Hung Kai Properties Limited develops and invests in properties for sale and rent in Hong Kong, Mainland China, and internationally. It...See Company Profile HKD

2. China Overseas Land & Investment (0688) HKD 252.28 billion 24.86% China Overseas Land & Investment Limited, an investment holding company, engages in the property development and investment, and treasury...See Company Profile HKD

3. China Resources Land (1109) HKD 245.3 billion 4.88% China Resources Land Limited, an investment holding company, invests, develops, manages, and sells properties in the Peoples Republic of China....See Company Profile HKD

4. China Vanke Co. (2202) HKD 235.54 billion -11.14% China Vanke Co., Ltd., a real-estate company, develops and sells properties in the Peoples Republic of China. The company operates through...See Company Profile HKD

5. CK Asset (1113) HKD 202.95 billion 13.53% CK Asset Holdings Limited operates as a property developer in Hong Kong, the Mainland, Singapore, the United Kingdom, continental Europe,...See Company Profile HKD

6. Longfor (0960) HKD 177.07 billion -20.57% Longfor Group Holdings Limited, an investment holding company, engages in property development, investment, and management businesses in China....See Company Profile HKD

7. Sino Land Co. (0083) HKD 91.07 billion 21.52% Sino Land Company Limited, an investment holding company, invests in, develops, manages, and trades in properties. It operates through six...See Company Profile HKD

8. Country Garden Co. (2007) HKD 80.22 billion -49.28% Country Garden Holdings Company Limited, an investment holding company, invests, develops, and constructs real estae properties primarily in...See Company Profile HKD

9. Greentown China (3900) HKD 40.51 billion 28.98% Greentown China Holdings Limited, an investment holding company, engages in the property development and related business in China. It operates...See Company Profile HKD

10. Yuexiu Property Co. (0123) HKD 29.82 billion 40 .17% Yuexiu Property Company Limited, together with its subsidiaries, develops, sells, and manages properties primarily in Mainland China and Hong...See Company Profile HKD

source: fknol.com

(Unfortunately they no longer sort by market cap by default. To view it you'll have to sign up for fknol's terrible website.)

Here was the logic I used:

'a' = 42 day price average.

'b' = adjust b based on the market cap. if the market cap is larger, c gets smaller, market cap smaller, c larger.

Market....a=42D_AVG.....b=a/Market_Cap_Billions

---------------------------------------------------------------------------------------------

0016.......94.14................0.3506

0688.......21.49................0.08518

1109.......35.14................0.1433

2202.......18.51................0.07858

1113.......51.73................0.2549

0960.......37.36................0.211

0083.......0.3542..............0.003889

2007.......5.662................0.07058

3900.......13.34................0.3293

0123.......0.09548............0.003202

(I had to fill in the table with dots so it would show correctly.)

Now, for each row, take each market and divide by 'b':

'market1'/b1 + 'market2'/b2 + ... :

'0016'/0.3506+'0688'/0.08518+'1109'/0.1433+'2202'/0.07858+'1113'/0.2549+'0960'/0.211+'0083'/0.003889+'2007'/0.07058+'3900'/0.3293+'0123'/0.003202

You can also exclude the second column, skip computing 'b', and instead divide the price by 'a' and you would have a 42 day average price weighted index. Dividing a price by an average would normalize it near 1, weighting each price equally.

Does it make sense? Thanks for taking a look!

Misc. Analysis:

Total valuation, going by the info, is roughly 1623.26 billion HKD , which is ~200 billion USD. This is not an unusually large amount, but the importance of these companies is far beyond their numerical market cap. Chinese citizens and companies purchase properties around the world, so I think this price action goes hand in hand with global real estate, possibly with this index as a leading indicator. A large global surplus of buyers in the last few decades has pushed real estate prices everywhere to unreasonable levels and now there is a deficit of buyers. Any serious bailout will distort prices and at some point it's possible that the price action becomes useless. The CCP owns a piece of every company already so I think this would be the more probable route.

Good luck and don't forget to hedge your bets!

China

Chinese Real Estate Large Cap Custom Index v2Just a quick update of the last chart I posted, which had a bug. These stocks:

'0123'

'0083'

refer to Malaysian stocks, but these stocks:

'123'

'83'

are the symbols we want.

Here is the updated index for your usage:

'16'/0.3506+'688'/0.08518+'1109'/0.1433+'2202'/0.07858+'1113'/0.2549+'960'/0.211+'83'/0.1272+'2007'/0.07058+'3900'/0.3293+'123'/0.3196

See here for more discussion:

Thanks for taking a look!

What Would Happen to Henry Hub NG if China Attacks Taiwan?Since last week the media has published videos and Chinese politicians' statements about the Chinese military drills near Taiwan. Taiwan has also conducted military exercises and preparatory work with the civilian population in the event of an attack. On August 3, the NYT, quoting Chinese state media, published an article about the following Chinese military drills scheduled on August 4 and a place of exercises. Chinese media offered five swaths of the sea surrounding Taiwan. If true, it can be a hostile act, possibly igniting conflict between China and unrecognized Taiwan. Both countries are essential for the world economy, meaning the conflict would affect markets. I hope it will not happen . However, this risk urged me to start a series of posts ' What would happen to asset_name if China attacks Taiwan? '

A brief: China is the second economy in the world by nominal GDP. China is the main trading party for the US, Europe, and many other countries and regions. The country is also a giant gas consumer and LNG importer. According to the EIA, the US was the fourth LNG supplier in China in 2021.

Henry Hub natural gas is a local benchmark. However, its price partly depends on the US LNG trade achievements and obstacles.

In case of a conflict, it would halt LNG export to Taiwan. I estimate Henry Hub participants would also wait for sanctions on Chinese banks or even prohibition of gas trade with China. These would drive expectations of short-term oversupply in the US local market resulting in a sharp price drop of natural gas in America.

In the end, some LNG exporters would change their export from China and Taiwan to other Asian countries, e.g., South Korea, Japan, and India. Other LNG sellers would divert shipments to Europe, suffering from high continent natural gas prices , bringing relief to Europe in terms of volumes and price.

The main shock could happen later. Possible export and import prohibitions between China and the US with Allies would bring manufacturing decline, pushing gas demand lower and cutting its price. It would get a more sustained bearish effect on Henry Hub prices than temporary shipment redirection.

With the technical analysis help, I estimate a first bearish move could put prices down to a support level of $6.4/MMBtu . Then, in case of sanctions, it would go down to the next support of $5.5/MMBtu . It is hard to forecast how long Taiwan can fight and what sanctions will be imposed. I doubt that sensitive restrictions would be imposed during the first days. I also doubt that the US will impose harsh O&G sanctions if China takes over Taiwan quickly. I expect it could happen a month after the start of the conflict. Breaking $5.5/MMBtu through, it would drop to the last winter's $4/MMBtu .

Put options are the best instruments for shorting HH on the potential conflict. For the first target of $6.4/MMBtu , the option with the corresponding strike and expiration in September could suit well. For the following targets of $5.5/MMBtu and $4/MMBtu , I suppose corresponding strikes with October and November expiration.

For futures traders, I guess a stop-loss is $8.5/MMBtu . The stop-loss is ugly and huge in today's Henry Hub Volatility environment. Timing for the trade matters much. I believe that options with an end-of-month expiration date could be good. The position holding period is 7 days to next Thursday. If the bad doesn't happen, it is better to close the long put or futures short position. However, we do not know the date. Solely China knows the exact date if the plan exists. The risk could realize during the next 7 days or be postponed to next month or even later. If the risk realizes later, I expect the same effect on the market, and only target adjustments could be needed.

I wish you peace!

Thank you for your reading, and have profitable trading! Comment your thoughts!

What would happen to S&P 500 if China attacks Taiwan?Since last week the media has published videos and Chinese politicians' statements about the Chinese military drills near Taiwan. Taiwan has also conducted military exercises and preparatory work with the civilian population in the event of an attack. On August 3, the NYT, quoting Chinese state media, published an article about the following Chinese military drills scheduled on August 4 and a place of exercises. Chinese media offered five swaths of the sea surrounding Taiwan. If true, it can be a hostile act, possibly igniting conflict between China and unrecognized Taiwan. Both countries are essential for the world economy, meaning the conflict would affect markets. I hope it will not happen . However, this risk urged me to start a series of posts ' What would happen to asset_name if China attacks Taiwan? '

A brief : China is the second economy in the world by nominal GDP. China is the main trading party for the US, Europe, and many other countries and regions.

Taiwan is the heart of semiconductor manufacturing for all industries around the world.

Bearing this in mind, recall that S&P 500 is a world barometer of economic health or a barometer of the capital markets financial system. The index has a diverse base of constituents representing the American economy. Companies from the index have business with China: manufacturing, trade, intangible assets, and financial transactions. Besides, Taiwan is the leading supplier for many American manufacturing companies working in consumer durables, communication, electronic technology, and producer manufacturing. The conflict would directly affect negatively on most American companies. It could slow economic growth (I think it would be a recession) and create much bigger supply problems than the 2021 supply chain crisis. Companies that heavily relied on Taiwan semiconductors would experience issues first. For instance, it could be Apple , Tesla , and AMD .

We do not know what kind of sanctions the US and its allies will impose on China. The next dropping wave of the index could happen if it is the anti-Russian-style sanctions. China is not only the biggest exporter of goods but the most prominent importer of commodities. Heavily relied on fossil fuels. For example, the US government may prohibit American oil and gas exports to China, causing damage to American O&G companies.

Regarding retail and non-durable, they also depend on imports from China. So I believe prices of utility stocks could be steady in a storm. I also thought about Air & Defence, but it could have heavily relied on Taiwanese and Chinese imports. Perhaps a few companies are not dependent on Asian supplies in the sector, but the whole industry is vulnerable. I do not want to bury deep into fundamentals cause the article is about the index.

Let's look at the chart. I estimate the potential conflict would hurt the index dramatically. The first target is 3700 ; semiconductor-dependent companies would drive the index drop by more than 10%. The following support is on 3200 . The best instruments for the trading idea are put options with the corresponding strikes. For futures traders, I suppose 4200 is a stop-loss. Timing for the trade matters much. I believe that options with an end-of-month expiration date could be good. The position holding period is 7 days to next Thursday. However, we do not know the date. Solely China knows the exact date if the plan exists. The risk could realize during the next 7 days or be postponed to next month or even later.

Here I will pause because it is hard to forecast how long Taiwan can fight and what sanctions will be imposed. I doubt that sensitive restrictions would be imposed during the first days. I also doubt that the US will impose harsh sectoral sanctions if China takes over Taiwan quickly.

I wish you peace!

Thank you for your reading, and have profitable trading! Comment your thoughts!

What Would Happen to Gold if China Attacks Taiwan?Since last week the media has published videos and Chinese politicians' statements about the Chinese military drills near Taiwan. Taiwan has also conducted military exercises and preparatory work with the civilian population in the event of an attack. On August 3, the NYT, quoting Chinese state media, published an article about the following Chinese military drills scheduled on August 4 and a place of exercises. Chinese media offered five swaths of the sea surrounding Taiwan. If true, it can be a hostile act, possibly igniting conflict between China and unrecognized Taiwan. Both countries are essential for the world economy, meaning the conflict would affect markets. I hope it will not happen . However, this risk urged me to start a series of posts 'What would happen to asset_name if China attacks Taiwan?'

A brief: China is the second economy in the world by nominal GDP. China is the top producer and buyer of gold in the world. It is the sixth largest gold holder, owning 1948 MT at the end of Q1 2022.

A possible conflict would drive the gold price to break the last resistance of $1790/oz t and move to the middle of the May-June range to $1840/oz t in the short term. The longer the conflict exists, the more sanctions I expect. I can't predict how long Taiwan can fight and what sanctions will be imposed. If the conflict lasts several months, developed nations could prohibit Chinese gold, as they have done with Russian gold. You could see it as a bullish sign. However, China could probit gold imports. The action will decrease demand and weigh on the price.

The position holding period is 7 days to next Thursday. Unfortunately, I do not see a good level for stop-loss. If the bad doesn't happen, it is better to close the long. However, we do not know the date. Solely China knows the exact date if the plan exists. The risk could realize during the next 7 days or be postponed to next month or even later. If the risk realizes later, I expect the same effect on the gold price, and only target adjustments could be needed.

I wish you peace!

Thank you for your reading, and have profitable trading! Comment your thoughts!

What Would Happen to Bitcoin if China Attacks Taiwan?Since last week the media has published videos and Chinese politicians' statements about the Chinese military drills near Taiwan. Taiwan has also conducted military exercises and preparatory work with the civilian population in the event of an attack. On August 3, the NYT, quoting Chinese state media, published an article about the following Chinese military drills scheduled on August 4 and a place of exercises. Chinese media offered five swaths of the sea surrounding Taiwan. If true, it can be a hostile act, possibly igniting conflict between China and unrecognized Taiwan. Both countries are essential for the world economy, meaning the conflict would affect markets. I hope it will not happen . However, this risk urged me to start a series of posts ' What would happen to asset_name if China attacks Taiwan? '

A brief: China is the second economy in the world by nominal GDP. Taiwan is the heart of semiconductor manufacturing for all industries across the globe.

In my opinion, Bitcoin today is a risk appetite indicator, which regularly mimics or outpaces changes in the notable stock indexes, e.g., S&P 500 and Nasdaq Composite. The risk realization would trigger risk aversion pushing the BTC price to the last local support level of $19000. The stop-loss is the previous local high of $24500. However, the level can slightly differ from the spot price. The main risk is conflict duration. The longer the conflict exists, the more sanctions I expect. I can't predict how long Taiwan can fight and what sanctions will be imposed. I doubt that sensitive restrictions would be imposed during the first days. I also doubt that the US will impose harsh sectoral sanctions if China takes over Taiwan quickly. If the conflict would last several months, I suppose bitcoin could drop significantly to $14000. The position holding period is 7 days to next Thursday. If the bad doesn't happen, it is better to close the short position. However, we do not know the date. Solely China knows the exact date if the plan exists. The risk could realize during the next 7 days or be postponed to next month or even later. If the risk realizes later, I expect the same effect on the BTC, and only target adjustments could be needed.

Additionally, the potential conflict would seriously weigh on crypto mining activity because of semiconductor manufacturing termination in Taiwan. A probable semiconductors' deficit leads to the rise of GPU's price in the midterm, elevating mining costs. Miners would have to adapt to the new reality.

I wish you peace!

Thank you for your reading, and have profitable trading! Comment your thoughts!

$BABA longterm entry 👁🗨*This is not financial advice, so trade at your own risks*

*My team digs deep and finds stocks that are expected to perform well based off multiple confluences*

*Experienced traders understand the uphill battle in timing the market, so instead my team focuses mainly on risk management

Entry: $90

Take profit: $180

If you want to see more, please like and follow us @SimplyShowMeTheMoney

Slowing Chinese economy sends US dollar higherEUR/USD 🔽

GBP/USD 🔽

AUD/USD 🔽

USD/CAD 🔼

XAU 🔽

WTI 🔽

Yesterday, the latest Chinese Industrial Production readings recorded a 3.8% growth - falling short of the 4.6% forecast, and raised concerns of a possible recession. On the same day, the Chinese central bank lowered its interest rate from 3.70% to 2.75%, in order to stimulate the economy while dealing with the pandemic.

As such, a weakened global demand saw WTI oil futures fall to $89.41 a barrel. Meanwhile, safe-haven demand is increased with growing recession signs, the US dollar gained much momentum, USD/CAD rose and stabilized at 1.2904, gaining over 100 pips.

The Reserve Bank of Australia has released its meeting minutes this morning, expecting to raise rates even further to “normalize monetary conditions over the months ahead”. The Aussie almost dropped a full 1% against the greenback, declining and slowing at 0.7020, to a closing price of 0.7022.

Euro and Pound both suffered noticeable losses, EUR/USD slid to 1.016, and the GBP/USD pair closed at 1.2054. Gold futures went below the $1,800 level to $1,798.1 an ounce.

More information on Mitrade website.

YINN China 3X Leverage ETF Reverses off the bottom Swing Long

AMEX:YINN YINN is now in an uptrend with an increasing cloud score

and upgoing BB boundaries. Stop Loss at the double bottom

while the first target is the recent consolidation period

with about 15% upside to that take profit and about a

2.5 Reward to Risk

All this makes YINN a candidate for a swing long trade

TSLA versus F - Stock Price and so Market CapThis DAILY chart shows the RATIO between Tesla and Ford stock and so comparisons

between market cap.

A rising ratio indicates that TLSA is gaining market cap compared with F while a decreasing

ratio shows the opposite.

A long-term investor who wants to own either TSLA or F or a blend of the two could use

a chart like this to make trade decisions.

When the ratio is high and approaching the upper BB with high relative strength, such

the hypothetical investor may want to either sell TSLA or buy F.

When the ratio is increasing lower with the value approaching the lower BB and

confirmation with low relative strength he/she might want to buy TSLA or Sell F

or some combination.

This strategy might be back-tested vs an equal proportion of F and TSLA.

without any share swapping.

One caveat moving forward is TSLA has China headwinds, with COVID lockdowns

and the geopolitical uncertainty of the Taiwan situation; F not so much could

easily trump technicals. Additionally, it could help explain why Musk liquidated

$ 6 Billion in shares. NASDAQ:TSLA

YINN China Bear #X Leverage ETFAMEX:YINN

China has had lockdowns, trade wars, delisting and

so on yet it hangs in there,

The YINN ETF downtrend is in early reversal.

An entry point may be soon RSI provides

confirmation.

looking the balance with Yinn after a yang yearThis ETF, is starting a bull trend, you just have tu buy and wait for more than 100%

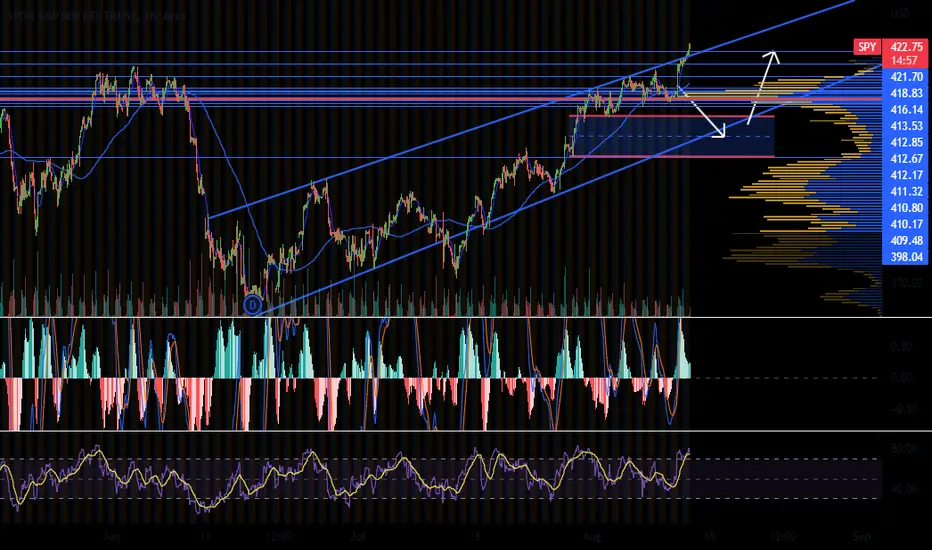

SPY is overextended again Spy is above the channel, I simply don't believe it is BTC time YET. Remember YET. We could be facing a pump then dump then takeoff from 19k BTC. But with all this negative talk about China's entire economy about to fail because of the real estate overbet, there's no way USA stocks don't face that value effect. China and Russia look like idiots. I expect some turmoil. Patience is key.

Chinese Real Estate -8% TodayJust FYI, an equally price-weighted basket of large Chinese real estate companies is down 8% today. Rumor is going around lots of companies in this sector are not paying interest payments and are on the verge of default. Maybe it could spill over into global markets? Dare I say it could be an outbreak in the market flu?

These companies are much larger than Enron. Evergrande (HKEX:3333) by itself has 120,000 employees, about 6 times as many as Enron had. Maybe something to think about.

Here is the symbol if you want to view it yourself:

'1918'/2.912+'0960'/2.862+'2202'/2.623+'2777'/1.112+'3333'/1.527+'2007'

I hope this was somehow useful. Good luck and don't forget to hedge your bets!

BREAKING NEWS The Real Estate and Banking Crisis in China!

The Real Estate and Banking Crisis in China Is Spreading to Other Aspects of the Chinese Economy!

A lot of information is coming out that the Citizens can't get any money from their banks.

We have seen that before! Never ends very well.

Apart from China's problems, Tesla has been experiencing problems in China.

1. The cameras on the Cars, that they can't be used anymore.

China thinks they could SPY on Them!

Good luck with a Tesla without cameras ¿?

2. Tesla reduced vehicle production at its Shanghai factory this week due to parts shortages caused,

in some measure, by a supplier's Covid lockdown nearby.

According to research by JL Warren Capital, Tesla specifically stopped production lines for its crossover electric vehicle,

the Model Y, at its Shanghai Gigafactory

3. Tesla faced multiple accusations of brake failure in China

4. China helps NIO to become the number one Electric Car for sure.

Made in China is always better for the Chinese Government.

5. China and USA aren't getting closer because of the Ukrainian War and Nancy Pelosi's visit to Taiwan.

SPY needs wave 5Maybe China can trigger wave 5? Does the world's chip factory belong to China? Or is the paper dragon in its death blows of a major debt crisis. Either way I see a wave 5 coming.

MP Rare time to buyThis has been a despointing few weeks I think this has a shot way oversold. has an uphill battle of resistance along with MA if it can change trend and move past 200 id be a happy man

China ETF GXC - Bounce off support?It has been a really long time since GXC was updated. Previously, an imminent breakout was expected, but it failed, in an epic fashion, to find itself the bottom support of the triangle.

Has it bottomed out and ready for a bounce?

Early game, but just want to put in the observation that it might bounce for the next attempt to breakout of the triangle. The weeks ahead will be clear that up...

Conversely, a break down of the triangle would be bearish!

Watch this space... IMHO, worth to watch China equities.

Market comments #1Hello everyone. I tried to put out regular market updates in the past, but I failed to do so for different reasons. This time, my idea is to gather the best tweets, articles, charts, etc., and add some brief comments. I will post these out regularly as long as I have decent material.

1. Sentiment is still very bearish, which means more upside is still possible. twitter.com

2. Soft landing team seems to be doing well so far... Until it eventually won't be doing so. I believe a scenario like 1989 is possible for markets, though I am slightly less optimistic than Jared. www.bloomberg.com twitter.com

3. Valuations can get out of hand as multiple market forces drive stocks. Stocks could trade higher and higher despite bad earnings. twitter.com

twitter.com

4. The US has low unemployment, but its labor market is nowhere near as strong as it was before Covid or before the 2008 GFC twitter.com twitter.com

5. Jobs are a lagging indicator; however, as the Fed is working with lagging data, they could hike more than they should. Good news now = bad news later; therefore, the market suffers now on good news, as it 'sees' the future. twitter.com twitter.com twitter.com

6. The yield curve inverting doesn't mean we will have a crash. A recession is guaranteed at this point, but remember that the recession comes many months after the inversion. twitter.com

7. So far, this is a worse situation than 2012, 2015, and 2018; however it is nowhere near as bad as 2008 or 2020. Could it get that bad? I doubt it for now. Of course, with new data, I am ready to change my mind if I have to. twitter.com

8. Some interesting comments by Jared Dillian with whom I agree: twitter.com twitter.com

9. My main worry is what happens between the US and China in the next few months, especially in October, as I think it would be tough to avoid an invasion. Heightened tensions alone can create a lot of problems... twitter.com

10. The Turkish Lira is heading yet for another collapse. No idea what could stop the Turkish economy from falling off a cliff in the next few years. www.zerohedge.com

There's something about ChinaC H I N A - There's something about China.

They like number go up. So do we.

Case closed.

⚡️ #BTCLIVE - 04.08 ⚡️⚡️ #BTCLIVE - 04.08 ⚡️

60:40

Bullish:Bearish

Current Status:

At the bottom of a symmetrical triangle - bouncing twice recently with relatively level volume showing distinct signs of ranging. Longer term Bullish Divergence is now in play. Unfilled CME Gap sitting at 23.7k to 23.9k along with the POC, both bullish. On a more macro level currently sat in the middle of a longer term range that is effectively a bear flag with a high of $25.5k and a low of $21.5k. Expecting to see a break out of this consolidation triangle over the next 24hours - direction unconfirmed.

News:

- Coinbase X BlackRock Partner for institutional investment > Bullish on BTC & ETH

- Coinbase starts Ethereum Staking > Bullish on BTC & ETH

- META introduces Coinbse Wallets to platform > Bullish on BTC

- Options Expiry Friday > Heavy Volatility

- China x Taiwan FUD/Conflict > Bearish on all markets

On-Chain

Growing supply in older age bands - This signifies that both HODLers be HODLing, AND that they are not spending their cold storage coins.

Declining supply in younger age bands - literally the equal and opposite reaction.

Generally speaking - this is what we want and are starting to see for a bear market floor

Bullish Scenario

Breaking and retesting $23.4k will see a short term target of approx. $24k and a bigger term target of $25.5k

Bearish Scenario

A Break down and retest of $22.7k will likely start the descent to $21.5k at the lower range of the longer term - breaking down on that will spell major bloodshed.

XAUUSD 4H TA : 08.03.22 (Update)As you can see the price reacted positively after it reached to its Bullish Breaker Block and now is consolidationg above 1760$ ! if the price can stablize above this price we can expect another bull run , but if the prie penetrates below 1752$ , we can expect another fall to 1720$ ! Let's See ... !

Follow us for more analysis & Feel free to ask any questions you have, we are here to help.

⚠️ This Analysis will be updated ...

👤 Arman Shaban : @ArmanShabanTrading

📅 08.03.2022

⚠️(DYOR)

❤️ If you apperciate my work , Please like and comment , It Keeps me motivated to do better ❤️

Gold is waiting for a climb signalIt is not yet likely to see a further drop for gold

Tensions between the United States and China over Taiwan, and fears of recession flirt with dollar sellers after its recent recovery, which was behind the current decline in gold

I'm watching 1800 dollars