BYD Launches Flagship 'Han' EV in Costa RicaThe sedan also debuted in other Central American countries.

BYD announced today that it has launched its flagship sedan Han EV in Costa Rica, in partnership with local distributor Corimotors.

"This cooperation will drive down carbon emissions to reach Costa Rica’s net-zero emissions goal by 2050," said Pedro Dobles, the General Manager of Corimotors.

"As BYD's flagship NEV sedan, the HAN EV has incredible driving performance with safety guaranteed. In the future, more BYD new energy cars will be introduced to provide local consumers with more options," Dobles added.

BYD launched the Han models in China last July – including the Han EV, an all-electric version with an NEDC range of 605 kilometers, and the Han DM, a hybrid model with a range of 81 kilometers on pure electric power.

Figures released by the company earlier this month show that Han sold 11,087 units in China in October, up 47 percent year-on-year and up 8 percent from September.

The Han EV sold 8,287 units in October, up 63.9 percent year-on-year, and the Han DM sold 2,800 units, up 12.4 percent year-on-year.

Cumulative BYD Han sales in China have reached 131,679 units since deliveries began in July last year, according to CnEVPost.

Notably, BYD is already one of the biggest players in the Costa Rican NEV market.

Earlier this month, BYD delivered 29 YUAN Pro EVs to a local Walmart, making it the largest all-electric EV fleet in Costa Rica.

Since 2020, BYD has been the top-selling NEV brand in Costa Rica, with a 30 percent market share in the local EV market, according to the company.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

China

Xiaomi's Revenue Hits CNY 78 Billion in Q3 2021As of Q3 2021, Xiaomi has invested in more than 360 companies, with a book value of CNY 59.1 billion.

Xiaomi releases its Q3 earnings report for the period ended September 30, 2021, on November 23.

- Internet service revenue was CNY 7.3 billion, a 27.1% year-on-year increase, with 73.6 gross margin

- IoT and consumer products business revenue was CNY 20.9 billion.

- Net profit was CNY 5.2 billion, a 25.4% year-on-year increase.

- Global shipments of smartphones were 43.9 million units, ranking third in the world, with a 13.5% market share.

- The number of users of devices (excluding smartphones, tablets and laptops) exceeds 8 million, with more than 400 million devices connecting to Xiaomi Group's AIoT platform.

- R&D investment was CNY 3.2 billion, a 39.5% year-on-year increase.

So far, the company has built the world's largest consumer IoT platform, connected to more than 100 million smart devices, and entered more than 100 countries and regions around the world.

EVERGRANDE FIASCO - A New BeginningAs you probably know International investors are watching this like a hawk I can honestly see 20.21 call me crazy but you'll see.

If you can't find me on TV I'll more than likely be here - maverickpartners.wixsite.com

HKEX:3333

CAPITALCOM:3333

SP:SPX

SKILLING:SPX500

OANDA:SPX500USD

FOREXCOM:SPXUSD

TVC:SPX

Interesting Sityation The stock is approaching a strong support zone. Enter only on confirmation. At the moment the Chinese stock market is quite volatile, in particular the Alibaba Corporation itself. But securities of some Chinese companies are showing good growth right now

❤️ If you find this helpful and want more FREE forecasts in TradingView

. . . . . Please show your support back,

. . . . . . . . Hit the 👍 LIKE button,

. . . . . . . . . . . Drop some feedback below in the comment!

❤️ Your Support is very much 🙏 appreciated!❤️

💎 Want us to help you become a better Stock trader?

Now, It's your turn!

Be sure to leave a comment let us know how do you see this opportunity and forecast.

Is it time to invest in China?KWEB is a China technology based ETF.

Top 10 holdings by weight:

Tencent Holdings ~ 10.62%

Alibaba Group Holding ~ 10.32%

JD.com ~ 7.21%

Meituan ~ 6.99%

Pinduoduo Inc ~ 6.97%

NetEase Inc ~ 4.71%

Baidu Inc ~ 4.27%

Bilibili Inc ~ 3.83%

Trip.com Group ~ 3.82%

JD Health International ~ 3.32%

Fundamental Analysis

China’s stock market pullback this year has been in line with the average annual drawdown (approximately 30%); historically, this volatility has tended to produce double-digit annualized gains.

In terms of seasonality, over the past 20 years, October has been amongst the strongest months for the Chinese stock market.

Technical Analysis

The 50sma has been tested as resistance 3 times before. A breakout above the 50sma could signal a significant change in trend.

The RSI has shown a positive divergence, as the last three times, we tested the horizontal line (blue arrow), in each case RSI is showing higher lows.

DXY threatens the marketsWell the DXY is again entering the area of extreme overbought and threatens to bring down not only commodity markets but also the global trade.

To be fair, this situation has been going on since late 2014, when a period of expensive DXY came, which led to pressure on commodity prices and frozen EM and is gradually coming back to the US through high inflation. Thus, a DXY slowdown is needed to save the Christmas rally.

✅ALIBABA LOCAL LONG/PORTFOLIO ADDITION🚀

✅ALIBABA is trading in a downtrend

Following the company's falling out of favor

With the Chinese Government

And fueled further by the Coming Evergrande collapse

That will drag China down with it

Today, the stock gapped and fell even lower

On the earnings news

However, a massive support level is ahead

At around 128$ per share, and I think

This might be a great local long

With the upside limited by the falling resistance

Also, with the stock trading with 60% discount

It might be a good place to start adding BABA to your long term portfolio

As it is clear that whatever economic storm is coming

Alibaba will be the one candidate to survive it

LONG🚀

✅Like and subscribe to never miss a new idea!✅

HUYA - Bearish Consolidation Strong base is forming and it might take few more months consolidating side ways. Breakout above 10.10 will make bullish trend, with key resistance level to watch at 10.52, 11.72, 13.15, 13.80 and 16.28. Upside potential of 36.53% in mid term.

IQ - Bearish Consolidation Failed forming potential inverse head and shoulder pattern. Expect this stock to further consolidate within the box. Short term trend is very bearish, won't surprise it will further break below current levels to test $6 or $5.

XPeng G9 First LookThe company will hold the third-quarter conference call on November 23.

XPeng Motors will unveil the G9 SUV, the company's fourth model and the first after its brand refresh, on November 19 at 11:00 a.m. Beijing time.

Photos of the model have already appeared in the XPeng app before the model was officially unveiled.

As previously reported by yiche.com, the new model will be based on the same Edward platform as XPeng's flagship sedan P7, which supports a wheelbase range of 2,800-3,100mm.

The model is expected to be priced at around CNY 300,000 (USD 47,000), equipped with a more advanced autonomous driving system with LiDAR and support for XPILOT 4.0, the report said.

Early last month, a Weibo user said that the XPeng G9 could be officially launched in the fourth quarter of 2022.

The car's wheelbase is between 3050-3100mm, which is longer than the NIO ES8 and Li Auto's Li ONE. But the car may be less than 5 meters long, possibly slightly shorter than the latter two, according to the blogger.

Its price may lie in the range of CNY 300,000 to 400,000, between the P7, which starts at CNY 229,900, and the P7 Wing edition, which costs CNY 409,900, the blogger said.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China

For the full article with the images, please visit the original link.

JD - Bullish Trend Mid to Long Term JD had recently hit double bottom and the trend has been reversed from bearish to bullish. As long as JD doesn't break below the inclining support line, we'll be in bullish trend. Also it recently hit resistance level, we might see some pull back to hit the support trend line, before breaking out big.

$BABA earnings analysis*This is not financial advice, so trade at your own risks*

*My team digs deep and finds stocks that are expected to perform well based off multiple confluences*

*Experienced traders understand the uphill battle in timing the market, so instead my team focuses mainly on risk management*

Today my team took a dive into Chinese online and mobile commerce company Alibaba $BABA. It has suffered an immense drop from its 52-week ranged high of $280.61. There are numerous events that factored into this sell-off, but we are not here today to discuss them. Instead we will focus on why $BABA is a hot earnings play for November 18, 2021.

To start, its strong cloud services will likely have shown improvement as they have implemented many new features the past few months to their cloud offerings. This is important because even if they miss earnings tomorrow investors/shareholders may still be encouraged if its cloud strength continues to show progressive results. Another factor that we are fond of is the apparent head and shoulders pattern that is being formed on its chart. This along with a pre-earnings dip of -4% has gotten us very interested in this play.

My team started a long $BABA position today at $161 per share. We will add more shares if a drop occurs, which is possible considering that this is still a fairly risky play.

Our Entry: $161

Take Profit 1: $180

Take Profit 2: $193

If you want to see more, please like and follow us @SimplyShowMeTheMoney

The Ending of an Era - HSIOriginal Chart This is Based Off

2018 update

Original Trade Strategy Around This Chart

Everything should be self explanatory in the chart. Of course - this will work until it doesn't, but since the 1990, the HSI index hitting its upper resistance line has nailed every major global market top within a very short timeframe. You can see how perfect this has timed markets with the correlation to the SPX index in the lower chart. Hypothetically speaking, when you would hit the upper resistance line, you would short emerging markets to hedge against whatever is about to happen. Then when this hits the lower resistance line, you would go long major market indexes until you arrive back at the upper resistance line (SPX, etc).

2022 - End of an Era?

As most can see, this chart is a very very long narrowing wedge / channel. The volatility between drawdowns and rises was far greater the further back you go, and the drawdowns have all been proportionally smaller as we narrow within the channel bouncing off top and bottom resistance (and sometimes in between). With that said, narrowing channels like this indicate increasing fragility of the trend, and potentially suppressed volatility. Eventually, something has to give, and this will break the long term pattern.

I believe we're close to that point, and that's not a good sign for asian markets. I don't know exactly what would happen if this breaks to the downside, but I don't think it would be pretty. Stable systems such as this have a way of becoming extremely chaotic when the stability breaks. Chaotic markets = drawdowns / crashes, and given the current state of Chinese markets and politics, this shouldn't be too surprising that it could be possible. The ongoing Chinese real estate crisis is just getting going, and the party has so far remained committed towards deflating their real estate bubble. Fundamentally, Hong Kong is just as bad if not worse than China from a real estate speculation / valuation perspective, yet there are additional problems in HK with people fleeing the territory due to the Chinese takeover following the 2018 protests. Demographics are strongly against this market, valuations are strongly against this market, and the current economics of this look rather dire without any major positive windows into future development / growth.

From a technical perspective, this is also far weaker than every other time it's hit the bottom resistance line. Note that every other instance we hit the lower resistance line, we also were hitting the lower monthly bollinger band at the same time. Not included within the chart, but momentum indicators also are showing a lot of negative divergences. You can see this from simply looking at the chart and noting the covid recovery bounce has been far weaker than every other post-lower boundary recovery bounce. We didn't even make it up to the middle resistance line before retesting.

My guess and view is that this won't break easily, but it will break dramatically. I think there is a good chance we see another rally here back towards one of the resistance lines, but after that, momentum will have really worn off. I also think we could chop around the lower resistance for a while, but ultimately, we are likely going to break down here on a secular basis. Maybe Kyle Bass will actually be validated after being wrong for 10+ years (except he's probably already been stopped out of all his poorly timed trades)?

NetEase Releases Third Quarter 2021 Unaudited Financial Results"As an innovation-driven content creator, we will continue to deliver thoughtful premium content and products to our users across each of our carefully cultivated disciplines," said the CEO and director of NetEase, William Ding.

Third Quarter 2021 Financial Highlights

- Net revenues were CNY 22.20 billion (USD 3.4 billion), an increase of 18.9% compared with the third quarter of 2020.

- Online game services net revenues were CNY 15.9 billion (USD 2.5 billion), an increase of 14.7% compared with the third quarter of 2020.

- Youdao net revenues were CNY 1.4 billion (USD 215.3 million), an increase of 54.8% compared with the third quarter of 2020.

- Innovative businesses and other net revenues reached CNY 4.9 billion (USD 761.1 million), an increase of 25.7% compared with the third quarter of 2020.

- Gross profit was CNY 11.8 billion (USD 1.8 billion), an increase of 19.5% compared with the third quarter of 2020.

Total operating expenses were CNY 8 billion (USD 1.2 billion), an increase of 14.5% compared with the third quarter of 2020.

- Net income attributable to the Company's shareholders was CNY 3.2 billion (USD 493.8 million). Non-GAAP net income attributable to the Company's shareholders was CNY 3.9 billion (USD 598.7 million).

Basic net income per share was USD 0.15 (USD 0.74 per ADS). Non-GAAP basic net income per share was USD 0.18 (USD 0.90 per ADS).

Third Quarter 2021 and Recent Operational Highlights

- Expanded games portfolio with new games in more diverse genres, including:

Naraka: Bladepoint, which broke the sales record of buy-to-play games by Chinese developers and led the Steam top-sellers chart, remaining in the top 5 for weeks following its global launch in August.

Harry Potter: Magic Awakened, which led China's iOS top grossing chart and top download chart following its launch in September.

- Exciting new titles in China such as Ace Racer, Infinite Lagrange and Nightmare Breaker.

Launched The Lord of the Rings: Rise to War in Europe, the Americas, Oceania and Southeast Asia.

Extended solid popularity of franchise titles including the Fantasy Westward Journey and Westward Journey Online series.

- Enriched dynamic game development pipeline with exciting advancements to upcoming games including The Showbiz: Dream Chaser, the console version of Naraka: Bladepoint, Diablo® Immortal™, as well as Ghost World Chronicle, and Harry Potter: Magic Awakened in international markets.

- Progressed Youdao's capabilities as an education technology provider, with steady advancements in STEAM courses, adult learning and smart learning hardware devices.

- Expanded NetEase Cloud Music's content ecosystem and product innovation capabilities to strengthen its highly-engaged music-enteric community, delivering a solid financial performance.

Revenue Reaches CNY 31.9 Bn as Baidu Announces Q3 2021"Baidu Core delivered another solid quarter, powered by our AI cloud revenue growing 73% year over year," said Rong Luo, CFO of Baidu. "With a diversified AI portfolio, including cloud services, smart transportation, smart devices, self-driving, smart EV and robotaxi, we are well-positioned for long-term growth."

Total revenues were CNY 31.9 billion, increasing 13% year-on-year.

Revenue from Baidu Core was CNY 24.7 billion, increasing 15% year-on-year; online marketing revenue was CNY 19.5 billion up 6% year-on-year and non-online marketing revenue was CNY 5.2 billion, up 76% year-on-year, driven by cloud and other AI-powered businesses.

Revenue from iQIYI was CNY 7.6 billion, increasing 6% year-on-year.

Cost of revenues was CNY 16.1 billion, increasing 26% year-on-year, primarily due to an increase in traffic acquisition costs, content costs and cost of goods sold related to new AI business.

Research and development expense was CNY 6.2 billion increasing 35% year-on-year, primarily related to personnel-related expenses.

Operating income was CNY 2.3 billion. Baidu Core operating income was CNY 3.7 billion and Baidu Core operating margin was 15%. Non-GAAP operating income was CNY 4.7 billion. Baidu Core non-GAAP operating income was CNY 5.8 billion and Baidu Core non-GAAP operating margin was 24%.

For the fourth quarter of 2021, Baidu expects revenues to be between CNY 31.0 billion and CNY 34.0 billion, representing a growth rate of 2% to 12% year-on-year, which assumes that Baidu Core revenue will grow between 5% and 16% year-on-year.

The COVID-19 situation in China is evolving and business visibility is limited. The above forecast reflects Baidu's current and preliminary view, which is subject to substantial uncertainties.

iQIYI Releases Q3 2021 Financial ResultsMr.Yu Gong, founder, director, and CEO of iQIYI, commented the Q3 performance was a 'softer than expected top-line performance'.

According to iQIYI's financial announcement for the third quarter of 2021:

- The total revenues achieved CNY 7.6 billion (USD 1.2 billion), showing a 6% increase from the same period last year.

- The operating loss was CNY 1.4 billion (USD 212.3 million) and the operating loss margin was 18%.

- The net loss attributable to iQIYI was CNY 1.7 billion (USD 268.4 million), compared to CNY 1.2 billion in the same period last year.

- As of September 30, 2021, the total number of paid subscribers of iQIYI was 103.6 million, or 103.0 million excluding individuals with trial memberships.

- Membership service business continued to be the largest business pillar with the revenue increased by 8% and accounting for 57% of the total revenue.

- Online advertising revenue decreased 10% year-over-year to CNY 1.7 billion primarily due to less premium content launched during the quarter and the challenging macroeconomic environment in China.

- The content distribution revenue achieved a 68% growth on year over year basis to CNY 627.1 billion, which was primarily driven by more content distributed to other platforms during the quarter.

- For the fourth quarter of 2021, iQIYI expects total net revenues to be between CNY 7.08 billion and CNY 7.53 billion, representing a 5% decrease to 1% increase year-over-year.

TAL Education Says Goodbye to K9 Academic AST ServicesTAL Education will explore quality-oriented education from multiple aspects.

On November 13, Zhang Bangxin, CEO of TAL (TAL:NYSE) issued an internal letter to all employees, indicating the new strategic direction for the future and the personnel adjustments made in accordance with the new direction.

According to the announcement, TAL plans to cease offering academic subjects to students from kindergarten through grade nine ('K9 Academic AST Services') in the mainland of China by the end of December 2021. Any course services users have signed up for would be guaranteed.

Zhang expressed that the company's business focus will be transferred from the subject training to quality-oriented training, aiming to cultivate the ability that will bring children lifelong benefit. Several trials have been made: on one hand, humanities and aesthetic education, scientific puzzles, programming and other subjects; on the other hand, it may actively explore music, sports, art and other categories.

The internal letter also mentioned that TAL will further increase investment in research and development for education technology, referring to science and technology to promote educational progress. Besides, TAL will promote overseas business with great patience, continuing to build overseas business models, brand awareness and operational capabilities in the next five to ten years or even more. Finally, TAL will continue to incubate new business, regarding it as a driving force for new organizational capacity. It said that the company would do more in digital content publishing, education hardware, hosting services and other aspects to be well-prepared for the future.

Zhang said that, although the main business has experienced huge changes, the unchanged initial motivation of education, the core management stability, the solid research and development accumulation and deep-rooted brand consciousness should help the company to locate its own position. It will continue to create value for customers, employees and the whole society.

Tesla, NIO, More EV Charging Ecosystems To Fully Enmesh in ChinaBy October 2021, members of the China EV Charging Infrastructure Promotion Alliance have built 1.06 million public charging piles.

Tesla landed its 1,000th charging station in China's mainland on November 1 in Shenzhen. In the meantime, NIO erected its 600th swap station. The two EV innovators have chosen different ways of providing charging services. Tesla rejected swap stations for high costs before NIO vindicated them. The latter's idea is to make it a part of the multi-layer charger system, which the NEV industry is hammering hard to build, based on different speeds. Moreover, this market has been designing faster solutions. The great leap of NEV facilities has caused low asset utilization that will likely stimulate charging networks to be open to each other.

A structural revolution

China's EV charging facilities are experiencing a structural revolution. In the early stage of mobility shifting to NEV, companies must roll out home charge suites to persuade consumers to buy EVs. But the speed can’t satisfy consumers that use cars frequently. Thus, many companies build their multi-layer charging networks, including fast direct current (DC) charges. The most typical companies that have two layers of charging networks include XPeng, Li Auto and BYD. They give consumers free seven kilowatts for home charging piles and supercharging stations that support 120 to 180 kW charging. But investing in DC infrastructure is costly, which stops some companies being able to afford hyper-charging stations. Instead, they leverage this service through third-party charging specialists such as TELD or Starcharge. Nowadays, buying cars from nascent brands like VOYAH, GAC Aion, or Weltmeister means one is free to use their networks.

More subtly, Tesla gives clients an additional solution destination charging stations that offer low-speed charging (22 kW) in places like hotels.

Among complicated charging network designers, NIO is an epitome. Apart from three ways of charging, it offers 20 kW home charging piles for selections and swap battery services. The inception of swapping batteries starts with the separation of vehicle and battery whereby consumers don't need to pay battery cost in front. The station can store a dozen batteries and finish the swapping process in five minutes.

Except for NIO, a few brands are also building swap stations. BAIC's fourth-generation swap station can reserve 60 batteries and swap faster than NIO's. Geely's future electric truck will support battery swap as well. Not only OEMs, but the government also supports and unifies the development of the swap station industry. As part of the big scheme of shifting to EV, the Ministry of Industry and Information Technology of the People's Republic of China has pushed several cities to test swap stations for future deployment.

A long way to go

Although the swap stations have accelerated the process of replenishing energy, they also face many problems. A critical one is that the sector lacks non-standard batteries that enable cars to switch the battery in stations of other brands.

Swapping stations place huge capital pressure on OEMs. For instance, building a swap station costs USD 300,000 compared with USD 100,000 for a hyper-charge station. According to Orient Securities' estimation, in China, the sector needs to invest over USD 2 billion in 2022 to build enough swap stations. The figure is projected to reach USD 11 billion by 2025.

Besides, OEMs are developing ultra-fast charging solutions. Tesla is said to be preparing to upgrade the current supercharging network to 300 kW. Xpeng has disclosed (link in Chinese) an 800-volt platform.

The fast-evolving industry is facing some problems. Low asset utilization is a critical one. China's EV industry started ten years before, and supported facilities emerged at the same time. According to the investigation published on d1ev.com (link in Chinese), a specialized auto portal focusing on the Chinese market, some charging facilities located in the suburb are badly maintained, charge high parking fees, which made them vacant most time. Although NEVs got popular in recent years, this problem still exists.

The openness of various chargers can be improved. According to CAAM (link in Chinese), the utilization rate of charging piles is 3% to 5% and 10% is the threshold for the industry to profit. Unharmonized infrastructure is intensifying the issue. Charging stations of various brands do support other brand cars to plug in. But this isn't always the case. For example, Tesla V3 charging isn't accessible for NIO, XPeng cars, which these two are compatible with each other. As these NEV companies build more charging stations, vacant piles appear and NEV players must collaborate to increase utilization. Therefore, it's very likely for them to open charging facilities to each other fully.

For the full article with the charts, please visit the original link.

$BABA Renko Idea Trying out the renko chart with geomath application, as renko does not included time as a factor ----> (C) 255.50 x 12/15/22

maybe chine give us present 4 new year?we broke downtrend channel and i see double bottom

maybe rocket to the moon

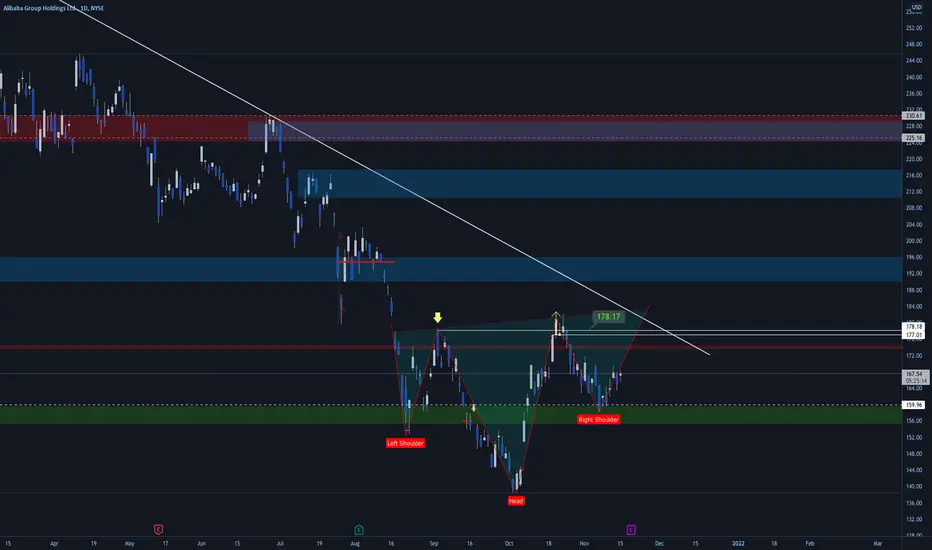

$BABA POSSIBLE HEAD AND SHOULDers? daily chart, showing bullish momentum lately... ahead of earnings?

BIDUBAIDU has corrected more than 55% from top and is consolidating in range bound in a box. Need to take out previous triple top at 182.6 and then 191.55, to fill the gap at 197. If it breaks below the box, downside support at 117