China Tech: The Nightmare Could Be EndingThe last year for Chinese technology stocks has been nothing short of a nightmare. But now there could be signs of a turn in the KraneShares CSI China Internet ETF, which holds key names like Tencent and Alibaba.

The 8-day exponential moving average (EMA) was under the 50-day simple moving average (SMA) since March. But last week, that faster-moving line rose above the slower one for the first time.

Next, KWEB has stabilized around $45. This was near the high in June 2015 and the bottom of its consolidation area in April-May 2020, immediately before a 110 percent rally.

Third, notice the rounded bottom with a low near $46 in July, a deeper low under $44 in August and then a higher low near $45 again this month. That lack of a lower low suggests prices may have bottomed.

Fourth, KWEB ended September with an inside week and began October with a bullish outside week. Such price action is also consistent with a trend reversal (in this case, a six-month bearish trend).

Finally, the Chinese yuan is rising the most against the U.S. dollar today since the first session of the year. It seems to result from confidence that the property-developer debt crisis is easing. While it’s not directly related to the country’s technology sector, renewed strength in the yuan would also provide a tailwind for KWEB.

TradeStation is a pioneer in the trading industry, providing access to stocks, options, futures and cryptocurrencies. See our Overview for more.

Chinastocks

Go to the ATH!The paper has formed a good uptrend. A fixing above the support level 171 would give a positive signal for a long-term buy long.

Fundamentals are also good, Chinese companies start to recover, you can pick up with a good discount and wait for new ATH.

On targets: the nearest unloading I plan on the mark of 230 dollars (+35%).

❤️ If you find this helpful and want more FREE forecasts in TradingView

. . . . . Please show your support back,

. . . . . . . . Hit the 👍 LIKE button,

. . . . . . . . . . . Drop some feedback below in the comment!

❤️ Your Support is very much 🙏 appreciated!❤️

💎 Want us to help you become a better Stock trader?

Now, It's your turn!

Be sure to leave a comment let us know how do you see this opportunity and forecast.

BABABABA can be heating up here ..

As long as above 148 this one can maintain some steam back into the 200's and lead China stocks with it.. very oversold from highs -- can be looking at near 100% ROI back towards highs from here!

Over 170 -- 210 - 230 target is in tact.

Further R LVLs are 248 - 270.

Good buy along with NASDAQ:JD

( Pretty soon this account will become private for only paying subscribers.. to keep up with the plays subscribe to my newletter :) )

- nick

GXC: China Equities going to break out...The GXC Weekly chart is about ready to break out and take off... just did a best case projection.

This is on the back that the Evergrande saga endgame is delayed, which I think would likely be so... into 2022.

Watch the next two weeks or so, needs to break out of trend line/channel and clear the gap resistance area.

Futu Founder Leaf Hua Li Apologizes over System Failure"We are sincerely sorry, and we humbly accept all criticism and advice. We will make relevant improvements immediately." Future founder Leaf Hua Li publicly apologizes for the interruption of the morning of October 9, 2021.

"We are sincerely sorry, and we humbly accept all criticism and advice. We will make relevant improvements immediately." Future founder Leaf Hua Li publicly apologizes for the interruption of the morning of October 9, 2021.

On October 11, 2021, Futu Holdings Ltd. founder Leaf Hua Li issued a signed article, apologizing to the public for the transaction interruption in the early morning of October 9, 2021. He highlighted three points in his apology.

Several brokerages, including Futu, experienced network failure in their engine rooms due to power stoppage. Futu contacted the operator for repair and was able to resume core services within two hours.

First, Hua Li addressed the compensation issue for near-exp options' value zeroing. Futu has already started contacting its clients regarding this issue and will negotiate and make customized compensation plans.

Second, Leaf Hua Li addressed the problem with the disaster recovery system. Hua Li emphasized that Futu's system implements disaster recovery and a dual-channel redundancy design, from market quotation to transaction, server to transaction gateway to network transmission.

Leaf Hua Li said, "This incident took hours to fix, which provided us with a lesson and much insight." In addition, he made it clear that Futu will prepare and include a backup solution that deals with transaction performance, order delay and supports cross-IDC. If a similar incident does happen, Futu could shorten the repair time to minutes.

Leaf Hua Li made the last point about the asset display issue. Many clients could not see their position and asset data during the interruption. The system failure severed the connection between the MooMoo APP and the background data, which caused panic as the interruption zeroed users' front-end display. Hua Li promised to improve the performance of the MooMoo App and its relevant services.

More Details of XPeng's New SUV RevealedThe vehicle, which is based on XPeng's Edward platform like the P7 sedan, could be available in the fourth quarter of 2022.

After spy photos of XPeng Motors' new mid-size SUV were revealed in late July and late August, new photos as well as specs have been revealed showing more details of the model.

According to Weibo user, the car, which is based on XPeng's Edward platform like the P7 sedan, could be called XPeng G9 and could go on sale in the fourth quarter of 2022.

The car's wheelbase is between 3,050-3,100mm, longer than the NIO ES8 and Li Auto's Li ONE. But the car could be less than 5 meters long, possibly slightly shorter than the latter two, according to the blogger.

It is not certain if the car will have a third row of seats, the blogger said.

It has a full glass roof, similar to a Tesla. It features bezel-less doors as well as hidden door handles, according to the blogger.

In terms of body materials, the model uses a lot of aluminum, involving the front hatch, front and rear doors, and the front bumper.

The model comes with an advanced autonomous driving system and LiDAR with XPILOT 4.0 support, the blogger said, adding that the layout of its LiDAR seems to indicate that the supplier is still Livox, incubated by drone maker DJI.

Its price could lie in the CNY 300,000 (USD 46,600) to 400,000 range, between the XPeng P7, which starts at CNY 229,900, and the P7 Wing edition, which costs CNY 409,900, the blogger said.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

As Crackdown Looms, Chinese Insurtech Waterdrop Enters Next GrowThe company's widening losses come along with the user base expansion.

Waterdrop Inc. (WDH:NYSE), a Tencent-backed Chinese online Insurtech company, as well as a crowdfunding platform, released its Q2 2021 financial report on September 8. It has consistently attracted international attention since going public this May.

One of the leading insurers in sales innovation, Waterdrop has been favored by the capital market since its establishment in 2016, completing six rounds of financing for over CNY 4 billion in 4 years. The company's current market value is merely USD 973 million.

The lackluster stock performance

Despite a great deal of attention from investors, Waterdrop has been performing poorly. Since debuting on the New York Stock Exchange at USD 12 per share on May 7, 2021, the price of the insurance technology platform has been slumping dramatically. On October 8, the closing price was only USD 2.47, tumbling almost 80% in two quarters. The company has seen an increasing net loss: it was CNY 655.8 million in Q2 2021 versus just around CNY 19,000 in the same period of 2020.

In addition, the policy crackdowns and industry overhauls also count. In an interview with Reuters, Peng Shen, founder and CEO of Waterdrop, expressed the intention to focus more on user growth instead of prioritizing profitability, at least in the short term.

Financial highlights

In opposition to increasing net losses, the company has a surging growth in operating revenue, which reached ten times the 2018 figures in 2020. The company generated CNY 3.03 billion (USD 464 million) in the first half of 2021, surpassing the all-year-round revenue in 2019.

The commission fee paid by insurance carriers is cited as the main booster for Waterdrop's improvement. As of December 31, 2020, the company had collaborated with 62 insurance carriers to offer health and life insurance products online, among which Anxin Insurance (19.9%), China Taiping Insurance (24.9%) and Hongkang Life Insurance (11.1%) are three major contributors in terms of percentage to total operating revenue.

On the other hand, the company's net loss topped CNY 1.02 billion for the six months ending June 30, 2021, which was almost equivalent to the previous three years' sum. The soaring sales and marketing expenses, especially the expenses on paying third-party user acquisition channels marketing fees, are deemed as the core factors, accounting for nearly 70% of the total operating costs and expenses. In 2020 only, the marketing services fee paid to Tencent reached CNY 187 million.

While the marketing expenditure saw an over 20% growth, the R&D investment kept shrinking to 6% during the period from 2018 to H1 2021. The increasing marketing expenditure reflects the company's ambitious sales goal and innovations, but a lack of focus on product or technological advancement so far.

Business breakdown

Starting from Waterdrop Medical Crowdfunding and Waterdrop Mutual Aid Platform, the company has strengthened marketing strategies with social attributes. Backed by Tencent, Waterdrop can utilize the huge user base that comes with WeChat and its related ecosystem to further extend business reach to low-income markets (sometimes also the Tier 4 cities and below), a relatively under-explored market. The strong social stickiness of WeChat Moments, QQ groups and other social media enable Waterdrop to gather health-focused people at a lower customer acquisition cost. With the traffic generated by crowdfunding and the public's increasing awareness of investing in insurance, Waterdrop has generated profits in the commercial insurance market, benefiting from the technology-powered scheme. At this point, a complete business closed loop is formed, with three market segments complementing each other to achieve further business growth.

I. Medical crowdfunding

Waterdrop first came into the public spotlight as a crowdfunding platform in July 2016. It enables people to initiate crowdfunding campaigns and share campaign information through social networks. Backed by Tencent and the huge traffic platforms it owned, Waterdrop has received development support and gathered the community with mutual assistance and development.

The company does not charge any fees for crowdfunding campaigns. In other words, Waterdrop has positioned this platform as a charity campaign. It performs the educative role in raising participants' health protection awareness, after which they may seek more comprehensive insurance coverage. This is how its ability to attract traffic works. As of June 30, 2021, approximately 372 million people donated an aggregate of over CNY 42.8 billion to around 2.1 million patients through Waterdrop Medical Crowdfunding, according to the Q2 2021 financial release.

The comprehensive risk management and anti-fraud measures are conducted to protect donors on Waterdrop Medical Crowdfunding, such as rigorous vetting, public disclosure and independent accounts at a custodian bank. However, the underlying trust crisis and the resulting compliance concerns have still plagued the company's next stage move.

III. Insurance marketplace

As the core profitable business, Waterdrop's insurance campaign has adopted quick changes and fast development. The cumulative number of paying insurance consumers soared from 1.7 million in 2018 to 19.2 million in 2021, achieving over CNY 14 billion first-year premium (FYP), 13.8 times larger than that in 2018. The FYP generated through the Waterdrop Insurance Marketplace for the second quarter of 2021 reached CNY 5.36 billion, representing an increase of 94.1% year on year. For the upcoming quarter, the company expects the FYP generated through the service to be in the range of CNY 4.3 billion to CNY 4.6 billion.

The comprehensive product offerings increased FYP and broadened paid user base, helping the company to achieve exponential revenue growth. Besides, the company's advanced technology and differentiated data insights are critical to its success. As an insurtech company, Waterdrop leverages online service capability and artificial intelligence to enable effective consumer conversion, providing intelligent underwriting, claim management, risk control and a series of other solutions to its insurance value chain.

The 'H' in Waterdrop's ticker 'WDH', its health business, was partly attributed to its accumulated data assets through the insurance marketplace, which reduces the customer acquisition cost and thus integrates upstream and downstream resources to reach the healthcare ecosystem. According to the founder, Waterdrop has aimed to become the Chinese UnitedHealth Group, and to expand further into the healthcare industry to achieve a state of diversified income. To be more specific, Waterdrop Health, which provides both basic health management services as well as medical treatment services, is on the right track. At present, top players on this track include but are not limited to Alibaba Health (0241:HK), JD Health (6618:HK), Ping An Good Doctor (1833:HK) and ZhongAn Online (6060:HK) – it was never going to be an easy job for Waterdrop to win.

Bottom line

Waterdrop faces challenges on multiple fronts, from pending regulatory changes that could halt core operations to widening losses. But it is telling a new story to the capital markets: starting from insurance and technology, it is heading towards the prosperous track of building a one-stop 'insurance+healthcare' platform. This path contains sizable opportunities, although Waterdrop’s future may not always be roses and rainbows.

For the full article with the charts, please visit the original link.

Denial of Contagion is futile.The China market is very dependent on several industries: Technology, Real Estate, Manufacturing.

Chip Shortage, Evergrande defaults and Power Outages directly opposes the rise in these industries. Triple Whammy.

Luckin Coffee: Back on Track?The tech-powered coffee chain may soon be ready for another public listing.

The Chinese coffee pioneer went on to achieve positive revenue growth despite the expected surge in its settlement fees and continued operating losses. More financial data from Luckin will be worth paying attention to in the near future.

Unexpected revenue improvement

On September 21, 2021, Luckin Coffee (LKNCY:US) filed its annual report of 2020 with the US Securities and Exchange Commission (SEC), which took much longer than many market participants anticipated. Although the fraud in 2019 astonished the China tech world and the company was expected to experience a wide range of store closures and steep revenue decline, its 2020 results surprisingly improved.

In the consolidated financial statement, the previous inflated revenue of CNY 5.10 billion in 2019 was adjusted to CNY 3.02 billion. The net revenue in 2020 reached CNY 4.03 billion, a 33.3% growth rate year-on-year. Operation expenses rose by 6.2%, which was largely contributed by the CNY 475 million of losses related to fabricated transactions and restructuring, reaching a total of CNY 6.62 billion. The company continued to be loss-making, with a net loss of CNY 5.59 billion. Yet, the figure includes CNY 2.40 billion of provisions for settlements (for SEC & equity litigants). The non-GAAP net loss, which ignores the above-mentioned expenses, was CNY 1.97 billion, an improvement from a CNY 2.79 level in 2019.

Business expanded despite upheavals

Another surprise came from Luckin's growing store number under the cloud of fraud, COVID-19 lockdowns, delisting and management team upheavals. As of July 31, 2021, the firm had 4,030 self-operated stores and 1,293 partnership stores. The former store type almost stayed unchanged (from 3,929 in 2019) in terms of numbers while the latter increased by 47.9% from 2019. The report also shows that the coffee chain closed many under-performing stores, most of which were self-operated. This might be a hint for the brand's determination on cost-saving and a switch to a franchise model. With the closing of stores, Luckin was no longer larger than Starbucks, but the coffee brand is still the second-largest since no other coffee chain can surpass it yet, in terms of the number of stores.

Amid intensifying competition, self-operating store expansion failed to improve per-store revenue

Though it was actively scaling up its business in previous years, evidence shows this strategy did not lead to improvement in per-store revenue for Luckin. In 2020, this problem was still haunting the coffee brand, as its intensive growth factor for self-operated stores (revenue per store per day) significantly underperformed, going negative (-10.1%). Nonetheless, the company's structural adjustment to focus on franchising might be promising, as the intensive growth factor (+106.5%) for partnership stores approached the extensive growth factor (+146.6%), implying that the brand's attempts in opening more partnership stores was advancing side by side with improvement in unit economics.

Chinese consumers, especially those from first- and second-tier cities, have developed a habit of drinking coffee, providing a fertile ground for the enlargement of the fresh-brewed coffee market. Interestingly, brought up by the trend the success of Luckin created, novel domestic coffee brands such as Manner have started to emerge, and foreign coffee houses such as Tim Hortons that covet China's coffee 'blue sea' have entered as well. Soon, Luckin should expect an even more competitive industry landscape.

In addition, the company was relying heavily on its coupons to acquire customers and expand its business. In the short term, this strategy is cash-burning and requires a vast capital backup, and in the long term it may be unsustainable if their products are not favored by the target consumers, especially now that company is delisted, short of fingertip capital support.

Last notes

Yet, Luckin's omnipresence in China is still unchallenged by other native and international brands except for Starbucks. Business-wise, it seems the firm is also reacting to the sustainability problem by cutting down its coupon expenses. In 2020, its sales and marketing expenses took up only 13% of the total expenses compared to 20% in 2019 and 31% in 2018. With opportunities yet to be explored in this coffee blue sea, it would be interesting to track the future release from this troubled Chinese coffee leader that survived all the internal and external adversities.

For the full article with the charts, please visit the original link. [/ b]

GDX and probably GXC rising to the occasionThe GDX was in close watch and it is time... Technicals are favourable for a bull run, and so is the broad equity market. Also had broken out of the Buy Zone!

GXC the China ETF is just about ripe based on technicals. Similarly, broad equity market drift should hold in supportm and the immediate gap should be closed for a run up.

ETHPERP LONGWith BTC recovering quickly from the china feud.

Maintaining above 3400 is critical, without interference of wale activity, we can expect ETH to touch 3600 resistance area. Current Target area is set for 3700-3800.

Gaotu Hints at Vocational Education Shift Due to the recent introduction of the 'double reduction' policy by the state to regulate the country's expensive private education industry, Gaotu is looking to adjust its focus.

The Chinese edtech firm Gaotu released its Q2 earnings report for the period ended June 30, 2021, on September 23 2021.

- Net revenue was CNY 2.23 billion, a 35.3% year-over-year increase.

- Net revenues of online K-12 courses increased 51.0% year-over-year to CNY 2.09 billion.

- Gross billings were CNY 2.69 billion, a 12.2% year-over-year increase.

- Gross billings of online K-12 courses increased 17.2% year-over-year to CNY 2.57 billion.

- Paid course enrollments increased 4.1% year-over-year to 1,631 thousand.

- Paid course enrollments of online K-12 increased 4.5% year-over-year to 1,563 thousand.

- Net loss was CNY 918.8 million, compared with a net income of CNY 18.6 million in the same period of 2020.

- Non-GAAP net loss was CNY 763.9 million, compared with non-GAAP net income of CNY 72.7 million in the same period of 2020.

- Deferred revenue was CNY 1.97 billion, compared with CNY 2.73 million as of December 31, 2020.

Larry Chen Xiangdong, Founder and CEO of Gaotu, said in the financial report that Gaotu has adjusted its organizational structure, transformed its focus to vocational and STEAM education instead and would further work on digital products and vocational education.

Shen Nan, CFO of Gaotu, further expressed that in exploring vocational education, the public service examination has maintained a high level. The number of paying users of financial certificates has increased fourfold year-on-year, Shen said, "In the future, we will focus on areas strongly supported by the government and create a multi-faceted interactive platform covering all education categories to achieve lifelong learning."

17EdTech Hits USD 104 Million in Revenue for Q2 2020The Chinese edtech firm’s K-12 tutoring service contributes 98.7% of its revenue

17EdTech released its Q2 earnings report for the period ended June 30, 2021, on September 23.

- Net revenue was CNY 671 million, a 147.2% year-over-year increase.

- Net revenues of K-12 tutoring service increased 163.9% year-over-year to CNY 662 million.

- Paid courses enrollment reached 1.18 million, a 131.1% year-over-year increase.

- A 68.3% increase in operating expense year-over-year consists of CNY 307 million in S&D and CNY 230 million in R&D.

- Net loss was CNY 218 million, narrowing down by 73% compared to Q1 2021.

- Cash and cash equivalent CNY 2.16 billion, an 23% decrease from last fiscal year.

- Monthly average users reached 1.65 million, a 24% decrease year-over-year

17EdTech also announced that Co-founder Mr. Xiao Tong resigned from the board of directors due to personal reasons effective from September 23, 2021. Since the uncertainty in the supervision of the firm and the operation circumstances 17EdTech did not release the performance guideline for the next quarter.

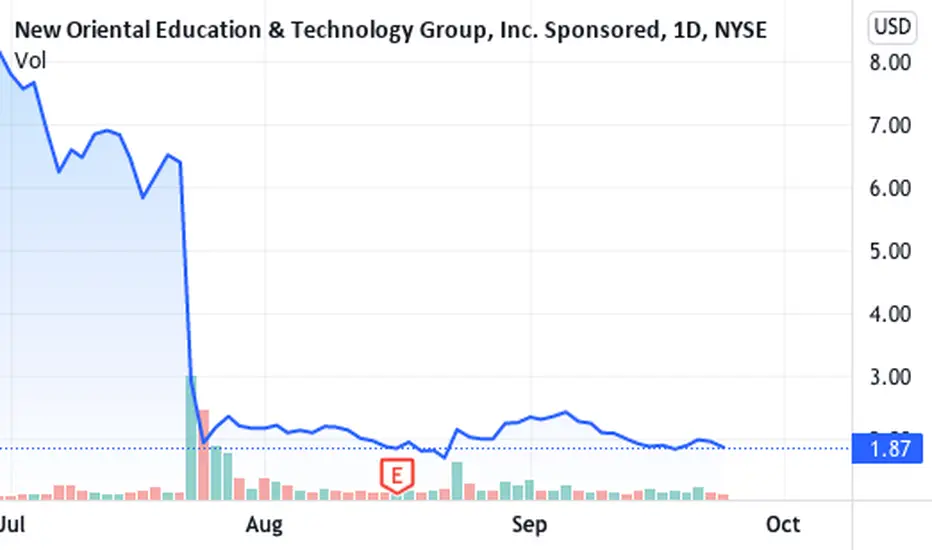

New Oriental Records USD 4.27 billion Revenue in FY 2021AccordinAccording to the latest regulatory developments, it plans to shut down a certain number of learning centers in the fiscal year 2022.

The Chinese edtech giant released the audited performance report for the fiscal year 2021 on September 24

Revenue was USD 4.27 billion, a year-on-year increase of 19.5%.

The net profit was USD 230 million, a year-on-year decrease of 35.03%.

The net profit attributable to shareholders was USD 334 million.

The revenue of New Orientals plans and services in the fiscal year 2021 was USD 3.93 billion, accounting for 92.1% of the total revenue while the revenue of books and other services was recorded as USD 340 million, accounting for 7.9% of the total revenue.

The firm's business is mainly divided into seven categories, including K12 after-school counseling, examination preparation courses, adult language training, kindergartens, primary and secondary schools, textbook development and distribution, online education, overseas study consultation, overseas study tour and other services.

- New Oriental's revenue from K12 after-school counseling, test preparation and other courses was USD 3.66 billion, accounting for 85.8% of the total revenue, an increase for three consecutive years.

Online education revenue was USD 211 million, accounting for 4.92% of the total revenue, with a year-on-year increase of 37.91%.

- The revenue of kindergartens, primary and secondary schools, textbook development and distribution, study abroad consultation, overseas study tour and other services was USD 399 million, accounting for 9.33% of the total revenue.

- In terms of the number of students, as of the reported period New Oriental has 6.723 million students participating in extracurricular counseling courses for middle school and high school students, and 5.348 million students participating in extracurricular counseling courses for kindergarten and primary school students. There are about 390000 students enrolled in the preparatory courses, including 198000 overseas preparatory courses and 193000 Chinese preparatory courses. About 5000 students enrolled in the adult English course.

- In terms of the number of teachers, the financial report shows that as of May 31, 2021, New Oriental has employed 54200 teachers, mainly full-time teachers, followed by contract teachers.

In terms of expenses, the total operating costs and expenses of New Oriental during the reporting period were USD 4.159 billion. Among them, the revenue cost was USD 2.037 billion, the sales and marketing expenses were USD 600 million, the general and administrative expenses were USD 1.49 billion, and the impairment loss of intangible assets and goodwill is USD 31.79 million.

- In this report, New Oriental believes that the measures taken to comply with the 'double reduction' policy will have a significant adverse impact on the firms' business, financial condition, operating performance and prospects.

New Oriental said that it may take further actions on discipline counseling services in the stage of compulsory education in the near future to ensure its legal compliance, including closing some learning centers and layoffs when necessary, so as to maintain continuous operation.

The Evergrande Crisis ExplainedIn this post, I'll be providing an easy yet comprehensive explanation on the Evergrande crisis, and why it's important for us to understand the situation.

Disclaimer: This is not investment advice. This is for educational and entertainment purposes only. I am not responsible for the profits or loss generated from your investments. Trade and invest at your own risk.

What is Evergrande?

- Evergrande is China’s second largest property developer, founded in 1996.

- To understand the size of this company, here are some numbers:

- Evergrande is running more than 1300 projects in over 280 cities.

- They’ve had success with real estate, so they also expanded horizontally, acquiring an electric vehicle company as well as Guangzhou F.C.

- They own a lot of other smaller companies, but their main focus and main business is in the field of real estate.

The Problem with Evergrande

- The main problem with Evergrande is its liabilities.

- The only thing you need to understand is that the company is in a lot of debt - specifically, $310 Billion.

- The company is also going through hard times with insolvency issues, and underperformance in terms of revenue.

- When the Chinese government put a list of companies that could pose a threat to the market and lead to its collapse, Evergrande was also on the list

- It was also recently revealed they begged the government for help in their backdoor listing plan as well.

Evergrande's Stock and Bond Prices

- Overall, Evergrande's stock fell close to 90% from its all time high levels, and over 80% since the beginning of this year

- The company’s dollar bond’s price has also dropped over 70%.

- What’s also concerning is how the bonds of Evergrande’s real estate counterparts are also dropping sharply, and signaling a potential crash.

Evergrande's Debt

- Out of Evergrande’s $310B debt, about $85B comes from bonds and loans from banks.

- These are the liabilities for which Evergrande actually pays interest on.

- $67B comes from shadow banking systems; money from shady sources.

- The rest of the $158B is actually the most important part. This is the amount of accounts payable.

- When Evergrande is does business and they’re developing real estate, they need to buy the materials and resources needed.

- But when they bought whatever they needed from their suppliers, they didn’t pay in cash.

- It all went down as accounts payable, which basically means that they owe the suppliers money.

The Anatomy of a Market Crash

- Financial institutions and suppliers rely heavily on Evergrande, and a lot of companies could go bankrupt if they’re not paid.

- This is essentially a domino effect of the entire Chinese market, with Evergrande at the center of it.

- Not only that, we also need to think of Evergrande’s employees.

- The company has over 123,000 employees alone, and that doesn’t include the number of construction workers who are hired for each of their projects.

China's Real Estate Market Situation

- China's real estate market is the biggest in the world

- The market also accounts for 10% of China's entire economy.

- Taking this into consideration, a complete collapse would cause devastating repercussions to not only the Chinese economy, but also the stability of the CCP, and the global economy as well.

Why the Chinese Government is Capable of Bailing Evergrande Out

- If we take a look at the numbers, it could also be said that they might get a government bailout.

- While their liability amounts to $310B, the interest they actually need to pay imminently, amounts to $669m

- This is also still a lot of money, but much more manageable than $310B.

- So while Evergrande is having a hard time with insolvency, if the government were to help out just a little bit, they might just be able to get back on their feet.

- And with investors gathering up in front of the Evergrande building and the probability of a political risk increasing, $669m might be a small sacrifice for the stability of the regime.

China's Indirect Intervention

- The Global Times, a media that directly reflects the stance, position, and opinion of the Chinese government, said that Evergrande was "not too big to fail".

- But, China’s central bank injected $14B in cash in Sep. 17, and another $15B today through Open Market Operations (OMO).

- And since the liquidity they provided was the most they’ve done in the past 8 months, it’s safe to say that they had Evergrande in mind

Expert Opinion on the Matter

- Michael Burry, founder of Scion Capital LLC, shared a tweet by @INArteCarloDoss, who states some important points.

- The 3 redlines, which are the debt related restrictions, began last year.

- China has been lifting the real estate market by leveraging a lot of debt, and the government wants to deleverage.

- It’s almost certain that Evergrande’s bankruptcy is a matter of time, but the question is how severely other companies and financial institutions will be affected.

- Of course the Chinese government will provide liquidity in the market, but won’t directly intervene and solve the problem for Evergrande.

- Overall, it could be said that Michael Burry agrees with this thread that says Evergrande’s bankruptcy is inevitable, and that the Chinese government will indirectly intervene, if it does decide to intervene at all.

- So a crisis in some form will certainly take place, it’s a matter of the degree to which it takes place.

- On the other hand, we have @BaldingsWorld

- Christopher Balding is a professor at Peking University

- His logic is that we won’t see a financial crisis because we’re applying the logic of the free market to a country’s market that is actually completely under control of its government.

- So this professor believes that a bailout for Evergrande is inevitable.

How to Prepare for a Potential Crash

- Since nothing is set in stone yet, the best we can do as investors is to keep my eyes open and look at how the Chinese government might directly or indirectly solve the issue.

- Depending on how the situation deteriorates, increasing one's cash holdings might be prudent in case the US stock market also is affected.

- This is especially important as the S&P500 index is currently testing the 60 Simple Moving Average (SMA) on the daily. (chart below)

Conclusion

Evergrande's debt situation might have greater implications than we can anticipate. Regardless of whether the Chinese government intervenes or not, and whether it does in an indirect or direct manner, there will be repercussions to the Chinese economy. As such, it's important to keep an eye on how the situation may unfold and affect the US stock market as well.

If you like this educational post, please make sure to like, and follow for more quality content!

If you have any questions or comments, feel free to comment below! :)

Evergrande and the Cryptocurrency Market Selloff ExplainedIn this post, I'll be providing an explanation on a theory regarding the potential connection between China's giant real estate developer, Evergrande, and Tether.

If you aren't familiar with Evergrande and the crisis it's currently going through, make sure to check out my previous post below:

Disclaimer: This is not investment advice. This is for educational and entertainment purposes only. I am not responsible for the profits or loss generated from your investments. Trade and invest at your own risk.

Evergrande's Shadow Banking Funds

- In my previous analysis, I mentioned the existence of Evergrande's $67B liability from shady sources.

- People, including renowned investors like Michael Burry, are posing doubts as to whether this liability has connections with Tether, a company that offers stablecoins in the cryptocurrency market.

About Tether

- Tether offers $USDT, a stablecoin that is convertable for 1 USD.

- Essentially, what it does is not so different from what banks used to do, and continue to do today.

- During the gold standard, when you took $500 to the bank, they'd give you an ounce of gold.

- Tether guarantees that they'll provide 1 USD per 1 USDT

- But, some say that Tether is faced with a bank-run like situation, looking at its reserves.

- According to their March 2021 Reserves update, commercial paper accounts for 65% of Tether's cash reserves.

- For those of you who don't know, commercial paper, or CP, is a way to finance extremely short term loans at a very cheap rate.

- Tether did not disclose whose CPs they were, in order to protect their partner's privacy.

Tether's Commercial Paper

- Back in July this year, Tether’s CTO and general counsel had an interview with CNBC, and made a few important points.

- They said that they have about $30B in AA rated International Commercial Paper, and these were rated AA by S&P and Fitch.

- The point that some people are making is that Tether’s commercial paper might actually be Evergrande’s commercial paper.

- This may seem like a conspiracy theory, but there are certain points that line up.

Reason #1

- First, Tether currently has $30B in commercial papers, and that’s an insane amount of money.

- Reuters reported that Shengjing Bank, the bank affiliated with Evergrande, is under investigation for providing illegal loans up to $20B.

- Considering that even a more renowned company like JP Morgan can’t write $20B loans, there is plausible reason to doubt that the capital may have come from Tether.

- So taking into consideration the size of the loan, some say that it’s highly likely that the capital flowed into Chinese real estate companies.

Reason #2

- Secondly, even after Bitcoin peaked in mid April, Tether continued to print more USDT. To be precise, they printed $15B between mid April and early June.

- In case you don’t know what bitcoin has to do with this, there have been claims that Tether has been arbitrarily printing USDT.

- This USDT would be used to manipulate the price of Bitcoin, and the overall cryptocurrency market in general.

- While Tether has been printing money like crazy, and as soon as Evergrande CPs defaulted on June 7, they stopped printing USDT.

- Now this is a chicken or egg question where we don’t know if Evergrande’s liquidity problem caused Tether’s collateral to impair, or whether Tether’s cutoff caused the liquidity issues at Evergrande, but something sure smells fishy.

How the Market Structure Would Break

- Tether claims that they don’t hold any Evergrande commercial papers, but we don’t know anything for sure yet.

- If it turns out that Tether was lying, and we see a domino effect take place, it would look something like this:

- Evergrande, along with other real estate developers in China, would go default.

- Tether, who lent them money in the form of commercial paper, could also go default.

- And with tether going default we would see the cryptocurrency market take a huge hit.

Where is Bitcoin Headed?

- So at this point, you may be wondering: where would Bitcoin be headed with this absolute mayhem of a situation?

- While Bitcoin and the overall crypto market crashed, we did manage to close above $40.7k on the daily.

- This would indicate that the overall uptrend remains intact, despite the awful news.

Conclusion

So many answers still remain unanswered. Where does Tether put its billions? Who issues $30B in AA International Commercial paper, willing to pay anything? Why did Tether stop printing money as soon as Evergrande’s liquidity died? As I've said in the previous post, the best thing we can do as investors is to prepare for all probable situations. In my personal opinion, the Chinese government seems willing to indirectly solve the issue by injecting capital via open market operations, so it's more likely that this situation will be settled at one point, as opposed to leading to the entire global financial market collapsing.

If you like this educational post, please make sure to like, and follow for more quality content!

If you have any questions or comments, feel free to comment below! :)

BABABABA looks to be in real trouble here and most likely will land around $84 long term to finish the massive H&S pattern

NIO: to Boost Its Battery Swap Stations' Coverage Along HighwaysThe company also has 341 supercharging stations with 2,176 supercharging piles, 515 destination charging stations with 2,878 piles and access to more than 400,000+ third-party charging piles.

The Chinese Lunar New Year holiday is a peak travel time for the public, and NIO wants to significantly expand its battery swap stations' coverage along highways before then to make it easier for its customers to travel by car.

The electric vehicle company announced Tuesday that it will have a battery swap network covering eight major highways and four densely populated metropolitan areas by the Chinese New Year in 2022.

The next Chinese New Year will come on February 1, 2022, and no official schedule has been released, but the holiday is usually seven days.

The holiday is typically a time for people working in major cities to return to their hometowns and will also see one of the world's largest population migrations, although it has waned in size in recent years due to Covid-19 concerns.

According to NIO's plan, the company hopes to complete a battery swap network along five north-south highways and three east-west highways by then.

The five north-south highways are G1 Beijing-Harbin Expressway, G2 Beijing-Shanghai Expressway, G4 Beijing-Hong Kong-Macao Expressway, G5 Beijing-Kunming Expressway, and G15 Shenyang-Haikou Expressway.

The three east-west highways are the G30 Lianyungang-Horgos Expressway, the G50 Shanghai-Chongqing Expressway, and the G60 Shanghai-Kunming Expressway.

The four metropolitan areas the company hopes to cover are Beijing-Tianjin-Hebei, Yangtze River Delta, Guangdong-Hong Kong-Macao Greater Bay Area, and Chengdu-Chongqing.

William Li, founder, chairman and CEO of NIO, said Tuesday that the company's number of battery swap stations covering the highway now stands at 99 and will increase to 169 by the Chinese New Year.

Notably, NIO has previously built battery swap networks covering the G2 Beijing-Shanghai Expressway and the G4 Beijing-Hong Kong-Macao Expressway.

On September 20, the company announced the completion of its battery swap network covering the G1 Beijing-Harbin Expressway, making it the third fully connected expressway battery swap network.

The G1 Beijing-Harbin Expressway is 1,229 kilometers long, and NIO has provided 10 battery swap stations along its route, one every 120 kilometers on average.

In addition, NIO announced on September 16 that with three new battery swap stations in highway service areas in operation, it has completed its network of battery swap stations in highway service areas from Beijing to all major cities in the surrounding area.

The network consists of 12 highway battery swap stations, centered on Beijing, covering the service areas in Hebei and Tianjin on seven highways: Beijing-Chengde, Beijing-Harbin, Beijing-Lhasa, Beijing-Chongli, Beijing-Shanghai, Beijing-Hong Kong-Macau, and Beijing-Qinhuangdao.

According to CnEVPost database, as of September 21, NIO had 484 battery swap stations in China.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

For the full article with the charts, please visit the original link.

XPeng Says P5 Had 6,159 Orders in 24 Hours of Official LaunchThe company said that 54 percent of those orders were for the LiDAR-equipped models.

XPeng Motors said Friday that it accumulated 6,159 orders for its new sedan, the P5, in the first 24 hours of its official launch.

The company announced Wednesday evening Beijing time that the P5 became available for order in China in six configurations with a subsidized price range of CNY 157,900 (USD 24,500) to CNY 223,900, and deliveries will begin in late October.

XPeng said today that 90 percent of these new orders are for models that support XPILOT 3.5 and XPILOT 3.0, its autonomous driving assistance system.

It's worth noting that this does not mean that all of these customers are subscribed to the XPILOT system, as they will need to spend additional money. XPeng did not disclose the percentage of customers who subscribed to the service.

XPeng debuted a new naming scheme for the P5 model, with the P representing the model's highest level of intelligence, followed by the E and G. The numbers in the names of the different models represent their NEDC ranges.

The P series, with the highest intelligence rating, offers a choice of 550 km and 600 km NEDC ranges, while the E and G series both offer a choice of 460 km and 550 km ranges.

Among these models, only two models of the P series are equipped with LiDAR, priced at CNY 199,900 and 223,900 respectively.

They can allow users to pay for a subscription to XPILOT 3.5 at a standard price of CNY 45,000, and users will be able to enjoy a discounted price of CNY 25,000 if they subscribe before delivery.

The two E series models are priced at CNY 177,900 and CNY 192,900 respectively. They allow users to pay for a subscription to XPILOT 3.0 at a standard price of CNY 36,000, and users will be able to enjoy a discounted price of CNY 20,000 if they subscribe before delivery.

The two models of the G series are priced at CNY 157,900 and CNY 172,900 respectively and do not support the XPILOT system.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

Dada Nexus Beats Q2 2021 Earnings Estimates, Growth AcceleratesCreating extra value for JD.com's 530 million active users will be the company's next strategic endeavor.

With the tumultuous unfolding around China's major New York-listed tech companies, plenty of mid-cap stocks have been affected as well, losing their market value in 2021. In some cases, however, investors' fear has little to nothing to do with the firms' real fundamentals.

Dada Nexus (DADA:NASDAQ) may be one such company. The Chinese operator of on-demand delivery and retail platforms recently posted its Q2 2021 financials. This time, the key results slightly exceeded both the analyst consensus and the firm's own projections, showing a pro forma revenue growth of 81.3% (the revenue recognition model was changed in April) and CNY 549 million in net loss – the Street's average expectation was CNY 615 million.

Dada was founded in 2014 as an "open local on-demand delivery platform" and took its present form after a merger with JD.com's (JD:NASDAQ) spinoff JDDJ in 2016; since the completion of that deal, it has been developing around a duo of products, boosting the core services' scope and building adjacent businesses and partnerships. In June 2020, the firm went public on Nasdaq, raising funds vital to stay competitive in the ongoing battle for Chinese consumers.

A growth-stage company, Dada is scrambling for a larger market share while moving towards profitability. Throughout the June quarter, its expansion continued.

This article looks at the key indicators' dynamics to analyze Dada Now and JDDJ's performance within those three months. We first crunch the newly reported data, then calculate key ratios to track the progress in financials and unit economics. To top it off, we provide a glance at Dada's tech initiatives beyond the two platforms.

"JD's over 530 million users" and COVID-19

In the twelve months through June 2021, the number of JDDJ's active users reached 51.3 million, increasing by 58.8% year-on-year. Dada relates this growth, among other things, to its cooperation with JD.com. During the earnings call, the company's executives stated that it "continued to win customers' trust" and is going to proceed with the "in-depth cooperation with JD to better serve the omnichannel and on-demand needs of JD's over 530 million active users." In addition, a new tool is being constructed at the intersection of the two digital ecosystems: 'Fujin', the former's entry point within the latter's app, has been tested in a handful of cities, including Shenzhen and Shanghai.

The duet's convergence is happening amid a post-COVID boom in the Chinese on-demand retail market. The number of users in the space has lately skyrocketed and is projected (link in Chinese) to grow at a 31% CAGR from 2019 to 2023. Consumers have changed their shopping habits forever.

It's also crucial that despite the magnitude of new possible outbreaks in China, this trend will remain strong, as the fix-cost-burdened offline stores are embracing online traffic. And Dada is among the country's top platforms that drive brick-and-mortar players' online sales, accelerating their adoption of digital tools.

From the ESG perspective, COVID-19 has pushed Dada Group to shoulder more social responsibility. Its executives stated that the company had worked "closely with local governments to provide the daily supplies and the on-demand delivery for the customers," and, as a result, "received recognition from the government."

More merchants, new partners and categories

Users are just a part – although the most critical one – of the story. The supply-side matters as much. As per the company, this quarter, JDDJ made significant progress in category expansion.

In retrospect, Dada started its business with groceries and has now covered a number of areas, such as pharma and apparel. By now, it has been taking the lead in the supermarket category and seeking partnerships with big chains. By the end of Q2 2021, hands had been shaken between Dada and "80 chains out of China's top 100."

The most recent attempt in the consumer electronics arena was emphasized a couple of times in the investor conference. As on-demand retailing has gradually been recognized by smartphone manufacturers, Dada has partnered with hundreds of distributors and established cooperation with Apple and vivo, among other major brands. Besides, the company stepped further into the PC category, cooperating with Microsoft, Asus, Dell and Alienware, among others. In response to an analyst's question, the executives disclosed that the potential of some new categories, including home appliances and cosmetics, will be further explored.

User acquisition at full pelt

In Q2, Dada's total expenses have added to around CNY 2.21 billion. The sales and marketing cost grew from CNY 386 million in Q2 2020 to CNY 824 million in Q2 2021. According to the unaudited financial results, this boost was mainly driven by the rising "incentives given to JDDJ consumers" and "referral fees paid to retailer store staff and third parties" to attract new users to the platform. Considerable investment was also directed to R&D, showing the intention to build comprehensive tech products on top of the company's commercial network. (One is Haibo.)

The operations and support expenses reached CNY 1.14 billion, compared with CNY 1.10 billion in the same quarter of 2020. The rise in rider cost stemming from the increasing intra-city delivery order volume mainly contributed to the accretion of this category; but this was partially offset by the decrease of rider-related costs incurred by the last-mile delivery business model upgrade – "effective since April 2021, the cost of riders for last-mile delivery services has been directly paid through third-party companies instead of through the company."

Even though the company experienced massive revenue growth in Q2, the spending on market expansion has kept the net profit margin at low levels. On a sequential basis, though, Dada improved its net profit margin, thanks to the efficiency gain in operations and consumer incentives.

Unit economics steadily improving

Positive dynamics in absolute figures, be it revenue or user pool growth, are never enough to claim success for a pre-profit platform economy enterprise. Dada's key business ratios, nonetheless, show some progress, too.

The trailing-twelve-months (TTM) revenue of JDDJ jumped from CNY 1.10 billion in Q4 2019 to CNY 2.97 billion in Q2 2021. In the meantime, the number of the platform's new users has been growing steadily, from 24.4 million to 51.3 million, up by 110.2%. The average revenue per user (ARPU) thereby rose from CNY 45.20 to CNY 57.90.

Using Meituan's Q2 2019 number (53.6%) as a proxy for quarter-on-quarter user retention rate (as opposed to customer churn) and the only assumption in this analysis, we found that JDDJ's user base may not only grow on the TTM basis, but the speed might have been accelerating continuously over the past eight quarters, which was perhaps caused by the platform's significant word-of-mouth marketing potential and effective referral system.

New tech, no red flags

Reporting a financially solid three-month period, Dada announced a few other updates this time. For one thing, it included an extra 1,000 stores into SaaS Haibo's network. The company is also developing an open autonomous delivery operation system, enabling on-demand retail applications for various hardware providers. The system has been tested and reportedly adopted by JD's SEVEN FRESH and Yonghui Superstores.

Both projects are narratives to keep tabs on. Those are highly likely to become key differentiators in the upcoming maturity phase of the on-demand delivery and retail market.

Over the past quarters, Dada Nexus has been growing at high double digits; good fundamentals and a balanced tactical arsenal are set to protect its market position.

For the full article with the charts, please visit the original link.

Pinduoduo: Stellar Performance Reinforces Industry PositionChina's largest e-commerce company is transforming its development strategy.

Pinduoduo turned losses into gains in the second quarter of 2021, defending its leading position in the Chinese e-commerce area with 849.9 million annual active buyers.

Pinduoduo mainly focuses on lower-tier cities' customers and follows a 'universal social welfare' way to expand its business.

Agricultural products and reinforcing networks among farmers and customers may become the next profit points for the company.

Dazzling financial results

On August 24, 2021, Pinduoduo (PDD: NASDAQ) held it's Q2 2021 earning call, showing rather impressive financial results. Its stock surged over 20% at the beginning of that trading day.

Pinduoduo turned losses into gains for the first time in the second quarter of 2021. In Q2 2021, the company achieved revenue of CNY 23.05 billion, up 89% year-on-year. Its operating profit reached nearly CNY 2 billion (with non-GAAP operating profit of CNY 3.19 billion), compared with an operating loss of CNY 1.64 billion. In the remarkable quarter, the company received gains (net income attributable to ordinary shareholders) of CNY 2.41 billion, which is a big move compared with a net loss of CNY 0.90 billion in the same quarter of 2020. The company's basic earnings per ADS increased to USD 0.30, and diluted EPS reached USD 0.27. At the same time, its annual active buyers reached 849.9 million as of June 30, 2021, and average monthly active users (MAUs) increased to 738.5 million, accounting for 87% of its annual active buyers, defending its leading position in China's e-commerce area.

Analyzing the financials, we found that Pinduoduo's cost control contributes the most to the result. Due to increased promotion and coupon expenses, the company's sales and marketing expenses only increased 14% to CNY 10.39 billion. In comparison, general and administrative costs only increased 10% to CNY 0.43 billion, compared with the same quarter in 2020. Its operating margin and the net margin reached a historical high in the past three years, accounting for 8.7% and 17.9%, respectively. Notably, its sales and marketing expenses ratio has been cut to 45%, compared with 81% and 73% for the same quarter in 2019 and 2020, showing its consistent cost control efforts.

When dissecting its revenue structure, we found online marketing services still act as the primary resource of its revenue, which reached CNY 18.08 billion, up 64% year-on-year. According to the earnings call, this was due to the continued increase in merchant activities while merchants are exploring new ways to engage with users. Meanwhile, revenues from transaction services reached CNY 3.01 billion, surging 164% year-on-year, owing to the fulfillment and services provided in the new Duo Duo Grocery platform. As for the revenues from merchandise sales, as a temporary way to meet user demand for specific products, the income from this section was CNY 1.96 billion.

Agriculture may become the key to its future

As one of the fastest-growing e-commerce companies globally, Pinduoduo has focused on lower-tier markets' consumption demand, becoming famous for value-for-money goods. Consumers can purchase products at a lower price as a group on its merchandise platform. In this way, consumers are allowed to share feedback regarding products on their social media accounts, further amplifying the advertising influence of the company at the same time. Pinduoduo only needed two years to gain CNY 100 billion GMV (in contrast, Ali Group and JD used five and ten years, respectively). The company went public on Nasdaq in July 2018. Then in March 2021, it became China's most prominent e-commerce giant in terms of MAU.

The company is infamous for some of its products' poor quality. Even though most of them are cheap, the quality is often worse than it's desired by consumers. To resolve this issue, here are two solutions: the company could build a higher quality sub-platform, or a more 'universal-type social welfare' platform, with which it can gather profit from a broader population. Pinduoduo chose the second one. In April 2019, the company launched a critical transformation, building the Duo Duo Farms platform to help farmers in China's impoverished counties create new online sales channels. In traditional ways, farmers sell primary products to dealers, and dealers trade themselves. When customers purchase the product, the price has been increased much higher than its cost, which harms both farmers and customers. Then, when PDD becomes the mediator, it connects farmers directly with consumers across the country and applies customer-to-manufactory (C2M) to help them build their brands, forming a win-win situation. By the end of 2020, the platform has helped over 1.13 million farmers to sell over 2.06 million tons of agricultural produce.

We think Pinduoduo's transformation had a positive impact on its business operations. Before 2020, Pinduoduo had adopted a low-cost publicity model to convert the advertising fees payable to the media into rewards for users who introduce new customers. However, at this stage, we believe that since user numbers are gradually approaching the ceiling (as over half of the people in China are Pinduoduo's users), the model of wildly attracting new customers may no longer be suitable for the company and is difficult to bring profit growth. Facts have also confirmed our idea that the growth rate of the company's MAUs has been gradually slowing down since 2019. So Pinduoduo turned its developing direction to retain its users and add more value instead of attracting more users. Focusing on China's most prominent supply side is a good strategy – after all, it is a blue ocean with few competitions.

Hence, we are optimistic about the long-term development of Pinduoduo and believe that its agricultural focus might generate new opportunities.

Valuation and bottom line

We used EV/revenue and P/B ratio to value the company. Considering that the company has been able to turn losses into profits and its competitors have much lower ratios, we decided to use the adjusted historical average method. From the chart, it is obvious that the ratio is at a low level, which we think is mainly caused by the regulation changes in China recently. Based on its current financial performance, momentum, and competitive landscape, we calculated that 13.5x EV/revenue and 17.5x P/BV is an appropriate valuation for Pinduoduo in 12 months, which corresponds to a target price of USD 141.52.

Key risks

1. Pinduoduo's largest risk comes from possible conflicts with registered merchants. The company provides a favorable discount at the expense of downtrodden platform merchants. Besides, the merchants are the primary resources that benefit most of Pinduoduo's promotion activities. Small-scale merchants find it difficult to survive on this platform. In the long run, we think it will lead to the weakness of the supply side and harm the whole platform.

2. Another risk is that the problem of low-quality products still exists. Since the Pinduoduo platform has more razor-thin margins than other platforms, many merchants chose to sell defective goods in Pinduoduo while selling better goods on Tmall and JD.com. We think it is not conducive to the original impression transformation of the company in the long term.

For the full article with the charts, please visit the original link.

XPeng Launches P5 Sedan with Starting Price around USD 24,500The company has secured a supply partnership with SK Innovation (SKI), a South Korean power battery supplier, which will provide it with high nickel-based Li-ion batteries with 80% nickel content.

After two months of pre-sales, XPeng Motors' new sedan, the P5, officially went on sale on September 15 at prices several thousand CNY lower than the pre-sale prices.

XPeng announced at a press conference on Wednesday that the P5 is immediately available for order in China in six configurations with a subsidized price range of CNY 157,900 (USD 24,500) to CNY 223,900, and deliveries will begin in late October.

The exact post-subsidy pricing for these models is as follows:

600P CNY 223,900

550P CNY 199,900

550E CNY 192,900

460E CNY 177,900

550G CNY 172,900

460G CNY 157,900

For comparison, XPeng's flagship sedan, the P7, has a starting price of CNY 229,900. The P5 went on pre-sale on July 17 with a price range of CNY 160,000 (USD 24,700) to CNY 230,000.

XPeng debuted a new naming scheme on the P5 model, with P representing the model's highest level of intelligence, followed by E and G. The numbers in the names of the different models represent their NEDC range.

The P series with the highest intelligence level offers 550 km and 600 km NEDC range options, while the E series and G series both offer 460 km and 550 km range options.

The battery for the 460 km range model is a lithium iron phosphate battery, while the 550 km and 600 km versions are ternary lithium batteries.

XPeng previously boasted that the P5 is the world's first LiDAR-equipped model, but it is worth noting that only the P Series is equipped with this component, while the E Series and G Series models are not equipped with LiDAR.

In terms of intelligent configuration, the P series comes with XPILOT 3.5 driver assistance system, the E series comes with XPILOT 3.0, while the G series does not offer this system.

The XPILOT 3.5 enables the extension of NGP (Navigation Guided Pilot) from highways to city roads.

The standard price of XPILOT 3.5 is CNY 45,000, and subscribers will be able to enjoy a limited-time discounted price of CNY 25,000 if they subscribe before delivery. The standard price for XPILOT 3.0 is CNY 36,000 and 20,000 if users subscribe before delivery.

The urban NGP will allow high precision navigation and assisted driving, adapted to China's challenging urban road conditions.

NGP will also be upgraded to NGP-L - a highway NGP with LiDAR - to enable safer and more capable assisted driving on China's highways and expressways, the company said.

XPeng's existing ACC and LCC systems will also be upgraded and enhanced to ACC-L and LCC-L status in P5, which incorporates LiDAR to enable P5 to identify congested vehicles earlier and stationary vehicles more accurately.

"With the P5, we have delivered a new level in sophistication and technological advancement for smart EVs in China, at a competitive price point," said He Xiaopeng, Chairman and CEO of XPeng.

"We believe this is an age of intelligence, and that intelligence will redefine mobility as a whole. Now we have made the best-in-class smart family sedan available at the CNY 200,000 price range, bringing some of the most advanced driver assistance functionality to China's vast and fast-growing middle-class consumer base," He said.

"We have drawn inspiration from customers' feedback, especially during the pandemic, and from the best models in the conventional family sedan and recreational vehicle (RV) class, while taking functionality and features to a whole new level," He added.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

XPeng Says Its Supercharging Stations Reach 400XPeng expects to expand its supercharging stations to dozens of cities, including Taiyuan, Tangshan, Nantong and Luoyang, within the next three months.

XPeng Motors said Tuesday it put 102 new supercharging stations into operation in August, bringing the total to 400, covering 101 cities in China.

Sixteen of those superchargers are located in highway service areas, bringing it to 27 superchargers in highway service areas, XPeng said.

The company added 36 new destination charging stations in August, bringing the total to 81, it said.

To date, the total number of XPeng-branded supercharging stations and third-party supercharging stations where users can enjoy a certain amount of free charging benefits is 1,596, the company said.

In comparison, XPeng's local counterpart NIO put 87 new battery swap stations into operation in August. It also added 56 supercharging stations and 73 destination charging stations in August.

In addition, NIO added one NIO House, 13 NIO Spaces, and three NIO Service Centers in August.

As of September 13, NIO had 445 battery swap stations, 300 fast charging stations, and 502 destination charging stations, according to CnEVPost database.

XPeng announced on July 12 that it is reducing the free charging allowance of 3,000 kWh per year offered to subscribers to 1,000 kWh per year as of August 1.

As XPeng customers continue to expand, the reduction in the free charging allowance is to ensure that the XPeng supercharging system can provide better and sustainable replenishment services to customers, the company explained, as quoted by sznews.com.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.