ES 4450 Late Chasers will be lit up: 4250 - 4150As Volumes begin to dry up and Seasonality begins to take hold as Euphoria

morphs quietly into "Fear" the ES will begin a large retracement.

Globex has been another Low Volume affair with the Retail Chasers continuing

to BTD with diminished conviction.

The chart remains in a Bull Trend, with extreme divergences.

We are preparing for a very nasty 10% correction, followed by another 9% @

minimum.

Ideally, and it is far too early to know - 3600/3800 Range should reduce the

appetite for the ES as Financials continue to fall apart.

Cohesion in Banking has been extraordinary. I have been an Chemical/Chase/JPM

Customer since 1991. This morning I received a notification from CHASE in which

they informed me I had not used my CHASE Credit Card in over 9 months - Citing

a lack of activity against a Large Revolving Line of Credit.

American Express, Member since 1991 - has dropped my credit score internally

from 835 to 717. The reason - an undisclosed Line of Credit, which I do not have.

My LOCs have not been reduced, although they appear to be creating causation.

Interesting times indeed for Money Center Banks.

Credit

Liquidity - Macro PerspectivveIn additional to Wells Fargo - more than one dozen additional Banks have

reduced Lines of Credit (LOCs) - the prior contraction in Personal Credit

occurred two weeks before the previous Retracement South.

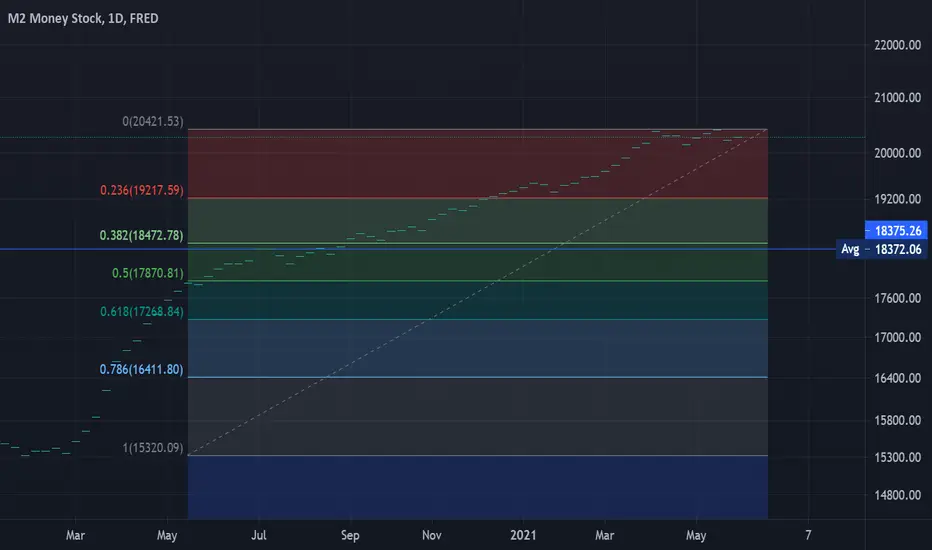

We anticipate the Net Effect will be Negative with an abrupt reduction in

M2 into the end of August.

$EDU short put vertical 73% PoP for credit at support$EDU short put vertical 73% PoP for credit at support

New Oriental Education & Tech Group had a big move and a big correction.

It's time to playing some bullish move.

Weekly timeframe:

Oversold on weeky and on daily too, sitting on the bullish trendline.

Daily timeframe:

Oversold too, bullish divergence.

Playing short put vertical here, because IVR is relative high: 60.

Max profit: $236

PoP50: 73%

Profit Target relative to my Buying Power: 30%

Max loss with my risk management: ~$150

Req. Buy Power: $764 (max loss without management before expiry, no way to let this happen!)

Tasty IVR: 60 (relative high)

Expiry: 24 days

Buy 4 EDU Jul16' 5 PUT

Sell 4 EDU Jul16' 7.5 PUT

Short put spread for 0.6cr each, because IVR is relative high.

COMMENT: Because of very low RSI and daily divergence it could be a good choice into my investment bag/portfolio too.

Stop/my risk management : Closing immediately if daily candle is closing BELOW the box, max loss in my calculations in this case could be 150$. Probability of loss in this way: ~27% .

Take profit strategy: 65% of max.profit in this case with auto sell order at 0.20db. Probability of profit this way: ~73%.

Of course I'll not wait until expiry in any case!

If you liked this article, check my other ideas.

Anyway: HIT THE LIKE BUTTON BELOW , and for fresh option ideas FOLLOW ME( @mrAnonymCrypto ) on tradingview !

Credit - TLT ShortIdea for TLT:

- Short downtrend which retested median line high.

- PT: 112

GLHF

- DPT

Credit - Mortgage Backed SecuritiesIdea for MBS:

- Mortgage Backed Securities bubble is about to pop.

GLHF

- DPT

Credit - LQD ShortIdea for LQD:

- Investment Grade Credit possible Head & Shoulders.

- Short PT 111.

GLHF

- DPT

Credit - HYG ShortIdea for HYG:

- Top of the range, rising wedge.

- Short TP1: 77.

- PT 67.

GLHF

- DPT

Credit - IEF ShortIdea for IEF:

- Short the downtrend, Head and Shoulders likely.

- TP1: 108

- PT: 100

GLHF

- DPT

Bullish Iron Condor with 64% PoP for 41% profit at eventMax profit: $291

Probability of Profit: 64%

Profit Target relative to my Buying Power: 41%

Max loss with my risk management: ~$200

Req. Buy Power: $709 (max loss without management at expiry, no way to let this happen!)

Tasty IVR: 53 (high)

Expiry: 43 days

Buy 1 SQ Jun18' 190 Put

Sell 1 SQ Jun18' 200 Put

Sell 1 SQ Jun18' 290 Call

Buy 1 SQ Jun18' 300 Call

Bullish Iron Condor for 2.91cr with +4.82 delta

Stop/my risk management : Closing immediately if daily candle is closing outside the box, max loss in my calculations in this case could be 200$. Probability of loss in this way: ~20% .

Take profit strategy: 65% of max.profit in this case with auto sell order at 1.02db. Probability of profit this way: ~80%.

Of course I'll not wait until expiry in any case!

If you liked this article, check my other ideas.

Anyway: HIT THE LIKE BUTTON BELOW , and for fresh option ideas FOLLOW ME( @mrAnonymCrypto ) on tradingview !

€3000 by 21.05.21 ?What an amazing week it has been for ETH and the Ethereum Community, there has been some serious shockwaves with the announcement of adoption by major banks to use the ETH2 protocol as a transport layer between private blockchains and CBDC's, the European Investment Bank just announced they are using Ethereum smart contracts to issue €100m bonds in conjunction with JP Morgan, Santander, Credit Agricole while the protocol is evolving using technology like Hyperledger Besu and Consensys Quarum to connect the banks to the blockchain. This new has of course created lots of retail action some incoming from BTC, FOMO is starting to kick in, can ETH get to €3000 by 21.05.21 or maybe sooner?

Watchlist Breakdown & Trade IdeasWatchlist Breakdown and Trade Ideas

- AAPL

- AMZN

- ZM

- CRM

- Slack

- AMD

Increased Bullish Pressure on EU and the PoundUS Consumer credit has fallen significantly, representing telltale signs that debt-intensive purchases have been falling signalling within North America that growth is beginning to show serious signs of depressed growth, of those similar to the '08 crisis. Because the US Yearly GDP is fueled by roughly 68% consumer-based debt/spending, this may be the beginning of a significant deterioration of the dollar as we head into wave 2 of COVID globally. This coupled with a looming presidential election does not bode well for the US dollar. We are beginning to witness the significant effects in the inherent damages of a global pandemic on the 'mighty-US' economy. This is a very short-term forecast, I believe DXY will rally into the Asian-Session while selling off into Late-London and Early-New York.

Investors will turn to 'neutral-risk-on' currencies such as EURUSD, GBPUSD as New York opens tomorrow. However, it is to note that significant news weighs on the pound as Brexit talks falter. Further analysis will be provided on the majors before NY open tomorrow.

In the long-term, I believe we will continue to witness this deterioration until the market fully digests the chosen presidential candidate and a vaccine is in the distribution phase within the USA. (4-6 month forecast)

As always, use proper risk management practices, matching your risk tolerance. This is solely an opinion, not financial advice.

Trade safe.

Auto industry likely to inflect downward from hereManufacturing has been a red-hot sector lately, and the CARZ auto ETF has been a beneficiary of that boom. The latest manufacturing data out today show continued outperformance by this sector, which I suppose is why CARZ is up today:

Empire State index: 17

Price of imported industrial supplies: +3.6%

Manufacturing output: +1%

When you drill into the data, however, it doesn't look as good for automakers. While overall manufacturing output is up 1%, output for auto manufacturers was down 3.7% in August. Another relevant data point from the August CPI report is that the price of used cars rose 5.4% in August. So it looks like the growing number of permanently unemployed workers, now deprived of stimulus checks and unemployment benefits, are starting to tighten their belts and reduce large expenditures. August credit card spend deteriorated in August, -13% YoY vs -12.3% the previous month. Consumer lending has tightened up as well, with banks opting to buy bonds rather than make loans.

HYG Bearish RSI Divergence 9/6/2020HYG or junk bonds at the daily view.

This is a project that my trading team and I are conducting. This is 9 of 9 charts (available on Trading View) that searches for clues for an imminent correction by using both June and September 2020 cases. It's a comprehensive overview that connects the charts volatility , trends, divergences, credit, and currency strength.

It seems that the credit markets had a bearish RSI divergence since August. It was too hard to see with candles. However, putting it as a line shows where the closing prices and closing RSI levels were. It seems that bearish RSI divergence finally played out in September's correction. Had I saw this earlier, I would've scaled in more VIX longs.

Not sure how far this will go. However, HYG is at a critical level where it needs to maintain the trend supports or it's going to fall like a rock. If traders and the Fed are the sword (to prop the markets up), the credit markets are the shield that protects the major indices from selling off even more. If corporate credit breaks their vital supports, we might get more than just a small correction within the ES, NQ, and RTY.

Splitit ready yet to take over the IPO high? 2+The high that was created by the hype during its IPO is ready to get taken over by the hype that's created from a cashless society.

TA,

- MACD daily golden cross

- MACD volume increasing

- Demand volume increasing

- Broke out of bullish pennant

- Bullish Moving averages

Hoping for some consolidation at this level due to 2 massive supply tails at 1.915.

Watch for the break of 1.915 and 2.00

FA,

- BNPL hype

- Pent up demand over the weekend. No, really that's a thing now. People hate weekends cause the casino is only open from Monday-Friday.

- Visa, Mastercard, Stripe partnerships

- Founder Brad Paterson :Former VP marketing at Intuit, Director for emerging products ANZ for Visa, Head of new ventures for Paypal

- 460% revenue growth

- MSV 260% (Creating win-win situations for merchants and SPT)

- Gives the customer more options with 3,6,12,24 months unlike other BNPL's.

- Allows the use of existing credit without interest rates. Less credit risk and easier to integrate with Visa/Mastercard ?

Capital One -- Not in My WalletAlthough Capital One is involved with more than consumer credit cards, it doesn't feel like a great place to be with record unemployment -- while unpopular, I am taking the gamble that the longer term trend is closer to '08 style credit crisis. The indicators line up, as well as the exact price levels. If this sells off (starting with poor earnings next week?) and was to do an exact length match to the bottom as in '08, it would be 17 monthly candles, or in this case roughly December 2021. COF broke through its 200 day moving average, and I don't see the earnings impressing.

American Express suggests continuation of downtrendThanks for viewing,

I'll give my technical and fundamental view briefly;

Technical;

- After the sharp drop from February highs AMEX has under-performed the market - dipping ~51%,

- This compares to an over 80% drop in 2009,

- The dip was followed by the formation of a rising wedge, which normally indicates continuation of the trend preceding the pattern (which is down),

- Elliot Wave seems to also suggest continuation - with wave (5) down possible,

- The 55 EMA showing resistance,

- I see potential support below at $60, $57, and the $50 - but if the stock equals its 2008-9 drop in % terms we are looking at sub-$25.

Fundamental;

- Credit Card (and charge card) Companies have a licence to print money, all payments made on credit expand the monetary supply (inflationary) - until debt is extinguished (deflationary). Over the past 10 years, they have been able to borrow at negative real rates and pocket the spread. But when the economy turns down, these Companies are hit hard by defaults,

- Even in good times, retailers balk at being charged 6% per charge card transaction,

- What are air miles gained on transactions worth these days when no-one is flying?,

- From the last recession, I read one consumer credit exec talking about the increase in defaults in terms of MULTIPLES of the rise in unemployment www.forbes.com). They didn't say what multiple, but If the multiple is just 1, then the default rate (which would impact shadow banking, consumer credit, and unsecured lenders first and worst) could jump to 20-25% of all outstanding debt balances (pre-crisis unemployment below 4% and estimated to exceed 30% by Goldman Sachs). Even a 1.5 multiple would yield 35% default rates. Who knows how things will shake out,

- It will all depend on the underwriting standards over the past few years, if newly signed-up customers are among the most credit-worthy, then things won't be so bad (data suggests that default rates even among CC customers with FICO scores above 740 have tripled recently www.forbes.com). If, when times were good cards were sent to anyone with a pulse then things won't be as great,

- The Fed is buying distressed ABS and MBS securities, apparently without regard for the creditworthiness of the underlying security, it is feasible that all this credit card debt packaged up and sold as an asset backed security has/will be been sold to the Fed at 100 cents on the dollar as it started to show signs of rising defaults in the underlying assets. This is a positive factors for the Company - I have doubts if it is positive for the economy down the line,

- CC Companies are offering repayment holidays - possibly in part to defer incurring defaults - this will of course impact on profitability.

- It all depends how you see this crisis - as being better or worse than 2008-9. My view is that this is many times worse, but that is just me. There are many reasons to expect higher defaults as compared to 2008-9 in an economy that has stopped on a dime,

- Today's dividend yield of 1.79% seems insufficient to compensate investors for the higher risk associated with holding equities - considering the stock is down over 30% from Feb highs. This is my view in general as well, a lot of stocks are "growth" stocks, which do not pay (in my view) a high enough risk-adjusted dividend to be worth owning. This is all gravy when the stock is rising, but when the dividend is below inflation AND the stock is losing value, there is less incentive for an investor to hold firm. If you combine this with a tendency of this stock to significantly underperform the market in recessions then you understand the basis for my bearish view.

So, overall, this stock rides high when times are good and has a history of being impacted more than the average. I don't see why that wouldn't still apply.

Cheers, and protect those funds

PayPal Holdings is forming "CUP" $PYPLPYPL is forming a deep cup and buy point is holding above $124.45. However, there is a negative divergence may pull back after hit pivot resistance till $113 or $110. Additionally EPS results also will affect the direction.

WTI / -46$ : What Really Happened and What it Changes ?Hope this idea will inspire some of you !

Don't forget to hit the like/follow button if you feel like this post deserves it ;)

That's the best way to support me and help pushing this content to other users.

Kindly,

Phil

CANADIAN BUSINESS IS GOING TO IMPLODE!80% OF CANADIAN BUSINESSES WERE CASH-FLOW NEGATIVE...BEFORE THE LOCKDOWN BEGAN!

IT'S THE LOONIE'S VALUE OR CANADIAN CORPORATE BOND VALUE...YOUR CHOICE BANK OF CANADA!

CYCTB? American Express CO. Hello friends,

I feel in this time, it is important to document.

With that being said, I have always felt in the past I was always calling the bottom.

With this chain of posting I will post my thoughts on what I think the bottom will be.

Most companies are over sold and over leveraged.

Hope this finds you well.

Happy trading.

Disclaimed - This is NOT financial advice - Its chart speculation.