"CYBER/USDT Long Trade Alert 🚀: Bull Flag Breakout and Retest A"CYBER/USDT Long Trade Alert 🚀

CYBER broke out of a Bull Flag Pattern and is currently retesting.

Entry: Current Market Price (CMP). Add more if it drops to $7.548.

Targets: $8.7, $9.45, $10.2, $11.5, $13.

Stop Loss (SL): $7.075 to limit potential losses.

Leverage: Use 5x to 10x cautiously.

R:R (Risk-Reward Ratio): 1:6 (Lucrative).

Use leverage wisely and be conservative to manage risks.

DYOR (Do Your Own Research). This is not financial advice. #CYBER #USDT #CryptoTrading"

Cybersecurity

CIBR: Cybersecurity Stocks Surge Into Year EndIt has been a record year... for cyber extortion. Orange Cyberdefense data, detailed in a Bloomberg article this week, reveal that there have been four straight quarters of increased corporate victims of hacks and financial blackmails. Major recent cyberattacks include those on MGM Grand, Clorox, Boeing, and China’s ICBC just this year alone. It is all good news for companies engaged in protecting against the increasing threat of large-scale ransomware attacks, among other tech-based crimes.

While shares of CrowdStrike and Palo Alto Networks have been strong lately, investors can play the trend at a higher level through the First Trust NASDAQ Cybersecurity ETF (CIBR). The $5.9 billion fund has a moderate 0.60% expense ratio, and it pays a modest 0.3% dividend yield. The issuer notes that the portfolio’s price-to-earnings ratio is lofty at 27.7x, but Morningstar reports that the ETF’s long-term earnings growth rate is respectable near 10%. To boot, you also get some semiconductor chip exposure, too.

For traders, CIBR’s momentum has been off the charts lately. Up seven weeks in a row, the basket of cybersecurity names has risen from the low $40s to the mid- FWB:50S as we head into 2024. A key thematic play, with fundamental strength (see CrowdStrike’s earnings late last month), I see the potential for CIBR to continue to rally, though shares have historically consolidated over the first 10 weeks of the year. As it stands, I see support between $47 and $48 with another layer of potential buying activity coming into play at $43. On the upside, keep your eye on the November 2021 all-time high just shy of $57.

The ETF successfully held its rising 200-day moving average earlier this quarter, and the breakout through $47 projects a measured move price objective to $58 based on the rounded bottom formation from Q2 this year to the December near-term breakout. With a daily RSI north of 86, we could see CIBR cool off, but the broader trend remains constructive in my view, and new all-time highs are certainly in play over the coming weeks.

#CTK/USDT 1D (ByBit) Descending wedge on supportShentu (a.k.a. CertiK) looks likely to reverse after printing that morning star with a dragonfly doji at the bottom.

Relative Strength Index (RSI) also bounced back on oversold territory, revisiting 100EMA resistance would make sense.

⚡️⚡️ #CTK/USDT ⚡️⚡️

Exchanges: ByBit USDT, Binance Futures

Signal Type: Regular (Long)

Leverage: Isolated (3.0X)

Amount: 5.4%

Current Price:

0.4665

Entry Zone:

0.4628 - 0.4384

Take-Profit Targets:

1) 0.5175

1) 0.5678

1) 0.6181

Stop Targets:

1) 0.3947

Published By: @Zblaba

$CTK #CTKUSDT #Shentu #CertiK #BSC shentu.technology

Risk/Reward= 1:1.2 | 1:2.1 | 1:3.0

Expected Profit= +44.5% | +78.0% | +111.5%

Possible Loss= -37.2%

Estimated Gaintime= 1-3 months

www.shentu.technology

CRWD - US cybersecurity play If this market will find traction and have a follow-through day, I will bet on CRWD being one of the next up-cycle leaders.

IBD 94 Relative strength and 99 Composite and EPS ratings are markers of a superb company. The industry group is 35 out of 197. High double and triple quarter earnings growth and stable 40+ sales growth for 3 qrts in a row; with stable 35+ ROE; Up/Down volume of 1.5; double digits analyst estimates of 24/25 EPS growth and increasing number of institution last qrt... all these make me call this stock a perspective leader.

From the technical perspective, notice how well the stock price holds and builds the high-handle close to 2023 highs, while general index (line above) is in a downward momentum being almost 10% of the highs. Unfilled gap-up on 31Aug (green circle) is also a sign of strength to me.

I want the price to subside more in volatility to the right side of the handle, creating a tight 3-4% risk pivot and maybe an inside day before breaking out above 172 pivot. That would signal and ideal entry point for my strategy with very tight risk. Although if price decides not to wait and will proceed with definite move above 172 pivot with supportive volume and will be hesitant to buy/add to the position, expecting the price to move to next resistance 194-206 target area.

Trading thesis is wrong if price moves bellow: 157 area

CYBER/USDT upward momentum? 👀 🚀 CYBER Today analysis💎Paradisers, turn your attention to CYBERUSDT as it showcases intriguing dynamics, especially after facing resistance, hinting at a heightened likelihood of a bullish resurgence.

💎 After recently breaking free from a descending channel, CYBERUSDT embarked on a bullish trajectory, only to face a hurdle at the resistance level of 6.518. Two potential outcomes lie ahead: Firstly, should it surpass this resistance, there's a strong probability it will approach the supply zone.

💎 Alternatively, the asset might harness bullish momentum from the demand level at 5.112. However, if it breaches this demand level, the scales tip towards increased downward potential, where the price might gravitate towards the support zone.

Cyber Big Breakout Cyberusdt

I am expecting the price to rise more and touch $10 soon.

It is a late entry; the best entry will be on a retest. Let's see.

It's not financial advice; do your own research.

CYBEY IN RULLY*-Technical Analysis 📈

Cyber come to high big renge and pullback to low level help to nexT jump.

*-Trade (Buy) 📊

5.92$ - 5.35$

*-Stop Loss 🔴

4.91$

*-Take Profit 🎯

7.04$ - 8.5$ - 12$

*-Risk Management 🚧

3%

👨🎓 Experience and Education: Our trading team has five years of experience in financial markets, especially cryptocurrencies

CYBR (Long) - Cybersecurity charts are too good right nowFundamentals

I have recently published a trade idea for another cybersecurity stock ( NASDAQ:QLYS ) and seems to have become a theme. The cybersecurity sector is rallying on the back of geopolitical tensions and some stocks, like NASDAQ:CYBR have put some lovely technical setups

The fundamentals here are not as pristine as in the case of NASDAQ:QLYS , but they are still robust

The revenue growth is strong and has remained robust and consistent; the sales have grown nearly 1500% in the past decade, from 47m to $700m

The company has a healthy balance sheet with a reasonable level of debt

The valuation is elevated , but that is to be expected for stocks with a lot of momentum. However, here I am attracted more to the technical setup

Technicals

Anyone who has seen my other trade ideas knows that a solid base with a high-volume breakout is a vital part of my analysis. Here, we have a base which has been forming over a three-year period . Usually, the longer the period, the more robust the base.

Last week, the base broke on a release of strong earnings followed by a higher-than-average volume, and most importantly, we have seen follow-through in price, suggesting the breakout likely has legs

Other indicators suggest continuing momentum and the overall sector is also remaining strong and in support of the rally

Trade

The price is a bit far off from the breakout point, so it currently does not offer the most ideal entry point. I would probably suggest waiting for a pullback or at least a consolidation as the stock is slightly extended on the daily.

However, for someone with a more long-term outlook , this price represents an entry as good as any

Suggested stop-loss is at the breakout point. A caveat would be if the stock fell back and through the breakout point.

One should also watch for the performance of the overall industry . For that, I can recommend the cybersecurity ETF AMEX:HACK

Follow me for more analysis & Feel free to ask any questions you have, I am happy to help

If you like my content, Please leave a like, comment or a donation , it motivates me to keep producing ideas, thank you :)

All set for 235?Its moving way from its weekly chart upwards. Looks like its going to meet 235 where it meets its weekly resistance. SL 175.

QLYS (Long) - Ideal time for a cybersecurity betFundamentals

With the Israel/Ukraine situation developing, countries and companies will certainly not mind some extra cybersecurity spending. Hence, companies like NASDAQ:QLYS are well-positioned to benefit

Any company making new all-time highs during a challenging time in the markets should catch your interest. This one just did it on impressive earnings and with a substantial buying volume.

I wish you could see the chart of revenue, which has grown by a consistent 20% year after year for the past decade (just a straight line up). Margins are fabulous with an 80% gross margin and a 23% profit margin .

The firm is incredible at handling its own capital with an ROCE of 41.7% (the industry average is 8.9%). The ROCE figure means that the firm has grown 309% over the last 5 years while using the same amount of capital - highly efficient

The firm has no debt (!) and earnings are expected to grow 10% next year.

I could go on and on, but I know that you all degenerates are here for the charts. Just to say, if you are thinking about something longer-term, this is a perfect pick

Technicals

What else to say than to just to look at the chart setup

Clean break on an earnings announcement. The base could be slightly better, but I do not feel like letting this one run away.

RSI pointing higher, good volume, relative strength is high and the industry is driven by various robust tailwinds

Strong growth, solid fundamentals and a lovely chart - William O'Neill would be proud

Trade

I entered the stock today; I wanted to wait for a better base, but I do not think this one will be waiting

However, the weakness in the market might drag it down a bit and offer a better entry

For the stoploss , I would suggest that if the stock falls back down back to the black line and below, that would be a clear sign of a failed breakout.

Follow me for more analysis & Feel free to ask any questions you have, I am happy to help

If you like my content, Please leave a like, comment or a donation, it motivates me to keep producing ideas, thank you :)

POSI - Russian leader in cybersecurity The actuality of cybersecurity for Russia in the absence of global brands becomes even sharper and provides unique opportunities for the best local provider to capture growing market share.

Stock price technical perspective still illustrates strong up-trend, with some caution signals to be mindful about if one decides to trade it.

On a weekly time-frame, price is solidly supported above the 10w MA, that is crucial for me to consider trading the upside of any stock. Although, I cautious about important fibonacci resistance levels at 2500 area. I price will not be able to follow-through its recent break-out attempt from 5 weeks flat base and move above 2500 zone, than I have hard times considering wave 4 finished, and will expect more deep and long correction (probably to 2070-1850 support zone).

That being sad, in my trading, I try not to forecast, but to follow the price and volume dynamics. And when the set-up is favourable and I have positive traction in my personal portfolio, I will take it without any hesitation.

Thesis : Above 2415 line and I expect price to follow-through and move towards 2600-2800 resistance zone. Below this line and I am out, and wait either for more tight entry set-up or stepping on the sidelines at all.

CrowdStrike going up!A bit unusual for me to try and make a idea about a specific stock, but here goes!

Crowdstrike has always been a darling for me and I have been in-and-out of the stock a couple of times, but this time im in it for the long run!

Clear upwards trend, with a nice couple of close support/resistance levels.

The current one we are at now from 168-169. Should go higher, based on their incredible earnings.

TP 1 - just above the 180-level, should be reached start-mid November and should hold that support.

TP 2 and 3 will be commented later!

Follow and keep track of the stock!

Good luck!

BB: Is at the PCZ of a Bullish Gartley and a Bullish Deep CrabBlackBerry is attempting a spring-and-back-test-of-spring at the bottom of the range that it's been trading within since 2012, and the level happens to align with the PCZ of a huge Bullish Deep on the left, to which it has reacted once before, and on its way to testing the zone a second time and back testing the spring. It's also formed a smaller, more localized Bullish Deep Gartley with some hidden Bullish Divergence on the MACD. If it manages to get back above $5 and stay above $5 in the active session, we would then have room to see it pump all the way up to $24.89 really fast as that is the next major level above and near the 200-Month SMA, but if things really want to get serious, we could see BB complete a Full Measured move of this range which would take it all the way up to the 50% retrace up at around $45.39

Shorting CyberUsdtShorting CyberUsdt from 8.2 as i think its peak...Dont think has potential to go above 11

Cyber dump#cyber, In last analysis, We informed you if price breaks the red trendline then it will dump. So red trendline break downs. Bullish scenario is invalid. A retest to red trendline is expected then further dump.

PANW Palo Alto Networks Options Ahead of EarningsIf you haven`t bought PANW`s Double Bottom here:

or before the earnings here:

Then analyzing the options chain and the chart patterns of PANW Palo Alto Networks prior to the earnings report this week,

I would consider purchasing the 230usd strike price Calls with

an expiration date of 2023-9-15,

for a premium of approximately $7.65.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Looking forward to read your opinion about it.

Fortinet FTNT Overreaction - What now?Slightly after earnings Fortinet Gapped down. Which are my favorite kind of stocks to trade because 9 times out of 10 Gaps close.

Fortinet had many analyst reiterate Bullish price targets some up to $70. I'm looking for a retest at $60.

Forecasting out to nov 2nd. The next earnings should be interesting.

Williams, MACD, & RSI are all showing Oversold in this situation. This could be a solid entry for someone to start a small position.

This is not financial advice.

Trade Responsible,

#TradeTheWave 🏄🏽♂️🌊

CSCO - Rising Trend Channel [MID -TERM]🔹POSITIVE signals rectangle formation with breakout at 52.14 resistance, next resistance at 55.

🔹RSI bearish diverges against the price, indicating downward reaction.

🔹Technically POSITIVE for the medium long term.

Chart Pattern;

🔹DT - Double Top | BEARISH | 🔴

🔹DB - Double Bottom | BULLISH | 🟢

🔹HNS - Head & Shoulder | BEARISH | 🔴

🔹REC - Rectangle | 🔵

🔹iHNS - inverse head & Shoulder | BULLISH | 🟢

Verify it first and believe later.

WavePoint ❤️

NET - Horizontal Trend Channel🔹Rectangle formation between support at 40.60 and resistance at 68.20.

🔹Support 52 and next resistance 130.

🔹Technically NEUTRAL for the medium long term.

Chart Pattern;

🔹DT - Double Top | BEARISH | 🔴

🔹DB - Double Bottom | BULLISH | 🟢

🔹HNS - Head & Shoulder | BEARISH | 🔴

🔹REC - Rectangle | 🔵

🔹iHNS - inverse head & Shoulder | BULLISH | 🟢

Verify it first and believe later.

WavePoint ❤️

ZS - Falling Trend Channel [MID TERM]

🔹Broken the ceiling of the falling trend in the medium long term,

🔹Support at 142

🔹Volume has previously been low at price tops and high at price bottoms.

🔹Technically neutral for medium-term long-term.

Chart Pattern;

🔹DT - Double Top | BEARISH | 🔴

🔹DB - Double Bottom | BULLISH | 🟢

🔹HNS - Head & Shoulder | BEARISH | 🔴

🔹REC - Rectangle | 🔵

🔹iHNS - inverse head & Shoulder | BULLISH | 🟢

Verify it first and believe later.

WavePoint ❤️

CRWD - Rising Trend Channel [MID TERM]🔹CRWD is in a rising trend channel in the medium long term.

🔹Next resistance 160.

🔹Weakening rising trend signals potential break early.

🔹Overall assessed as technically neutral for the medium long term.

Chart Pattern;

🔹DT - Double Top | BEARISH | 🔴

🔹DB - Double Bottom | BULLISH | 🟢

🔹HNS - Head & Shoulder | BEARISH | 🔴

🔹REC - Rectangle | 🔵

🔹iHNS - inverse head & Shoulder | BULLISH | 🟢

Verify it first and believe later.

WavePoint ❤️

PANW - Rising Trend Channel [MID TERM]🔹FTNT is in a rising trend channel in the medium long term.

🔹Supports at 192 in negative reaction.

🔹Short-term momentum is positive with RSI above 70.

🔹Technically positive for medium-term long-term.

Chart Pattern;

🔹DT - Double Top | BEARISH | 🔴

🔹DB - Double Bottom | BULLISH | 🟢

🔹HNS - Head & Shoulder | BEARISH | 🔴

🔹REC - Rectangle | 🔵

🔹iHNS - inverse head & Shoulder | BULLISH | 🟢

Verify it first and believe later.

WavePoint ❤️

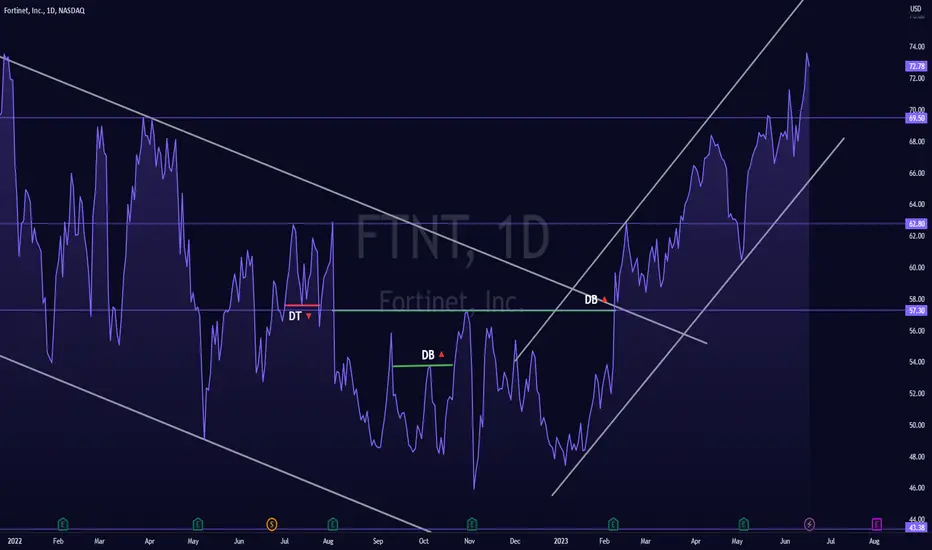

FTNT - Rising Trend Channel [MID TERM]🔹FTNT is in a rising trend channel in the medium long term.

🔹FTNT surges after double bottom formation break through resistance at 57.16.

🔹supports at 69.50 for negative reaction.

🔹Overall assessed as technically positive for the medium long term.

Chart Pattern;

🔹DT - Double Top | BEARISH | 🔴

🔹DB - Double Bottom | BULLISH | 🟢

🔹HNS - Head & Shoulder | BEARISH | 🔴

🔹REC - Rectangle | 🔵

🔹iHNS - inverse head & Shoulder | BULLISH | 🟢

Verify it first and believe later.

WavePoint ❤️