Artificial intelligence: signs of acceleration in 2023“One final investment area that I’ll mention, that’s core to setting Amazon up to invent in every area of our business for many decades to come, and where we’re investing heavily, is Large Language Models (“LLMs”) and Generative AI. Machine learning has been a technology with high promise for several decades, but it’s only been the last five to ten years that it’s started to be used more pervasively by companies. This shift was driven by several factors, including access to higher volumes of compute capacity at lower prices than was ever available. Amazon has been using machine learning extensively for 25 years, employing it in everything from personalised ecommerce recommendations, to fulfillment center pick paths, to drones for Prime Air, to Alexa, to the many machine learning services AWS offers (where AWS has the broadest machine learning functionality and customer base of any cloud provider). More recently, a newer form of machine learning, called Generative AI, has burst onto the scene and promises to significantly accelerate machine learning adoption.”

Amazon.com CEO Andy Jassy1

When Amazon’s CEO makes such a statement, we pay attention. In 1997, Amazon.com had revenues of $147.8 million; in 2022, this figure was $434 billion for Amazon’s consumer business. Amazon Web Services was conceptualised in 2003, with the first services launched in 2006 and, in 2022, generated $80 billion in revenues.

Elsewhere, The Stanford AI Index Steering Committee, Institute for Human-Centered AI (one of the best annual resources on artificial intelligence), have also just released a new report. Artificial intelligence (AI) is, undoubtedly, a big topic in 2023, and this report provides an excellent resource for understanding how it is progressing. The full piece is almost 400 pages, but we wanted to highlight some key points.

ChatGPT was not the only big AI development of 2022

On November 30, 2022, ChatGPT was launched, but the Stanford AI Index report helps us remember other notable events in 2022. Our 5 favourites:

February 16, 2022: DeepMind trained a reinforcement learning agent to control nuclear fusion plasma in a tokamak2. While this doesn’t mean that fusion powerplants are immediately around the corner, it does show a notable use case for AI to help scientific research in a very, very difficult area.

April 5, 2022: Google released its PaLM large language model with 540 parameters. This was an important step, showing that one avenue to improve the performance of these models was to simply train them on more data. As of this writing, we do not know how this figure compares to the number of parameters in use for OpenAI’s GPT-4.

May 12, 2022: DeepMind showcased Gato, which is a model that can generalise across such activities as: robotic manipulation, game player, image captioning, and natural language generation.

June 21, 2022: GitHub makes Copilot available as a subscription-based service for individual developers. Copilot is a generative AI system that can turn natural language prompts into coding suggestions across multiple languages.

July 8, 2022: Nvidia uses reinforcement learning to design better-performing GPUs, accelerating the performance of its latest H100 class of GPU chips.

Insights on global corporate investment

AI has been one of the hottest areas for corporate investment, but Figure 1 shows the total level of investment shifted downwards, from $276.14 billion to a level of $189.59 billion in 2022 with the market volatility.

The two biggest categories comprising the level of AI investment recently has been ‘Merger/Acquisition’ and ‘Private Investment.’ Both of these categories dropped significantly from 2021 to 2022, but this is not surprising in that both of these would be expected to slow in a less certain economic environment with the US Federal Reserve quickly raising the cost of capital.

One of the most informative charts in the 400-page report is the specific focal areas of investment, and how they have changed.

‘Medical & Healthcare’ was the biggest focal area in 2022, after being second biggest in 2021, trailing only ‘Data Management, Processing and Cloud.’

‘Cybersecurity, Data Protection’ was the fourth biggest investment area in 2022 and the largest that saw an acceleration in investment, meaning investment in 2022 was actually larger than in 2021. The Russia/Ukraine conflict in 2022 created a big focus on cybersecurity.

There is little question, the first four months of 2023 have seen a massive focus on AI, and a massive focus usually leads to at least some hype and some risk of near-term overvaluation. Sometimes this is the nature of thematic investment—we all want something to get excited about, especially if economic growth and geopolitics are less positive. What is emphasised in the letter from Amazon.com CEO, Andy Jassy, and then measured in the 2023 Stanford AI Index report, is that the AI megatrend is continuing to grow and increase in its impact on society and on businesses.

Sources

1 Source: aboutamazon andy-jassy-2022-letter-to-shareholders

2 A tokamak, put simply, is somewhat of a doughnut in shape and is a device used to contain the plasma in a fusion reaction.

Cybersecurity

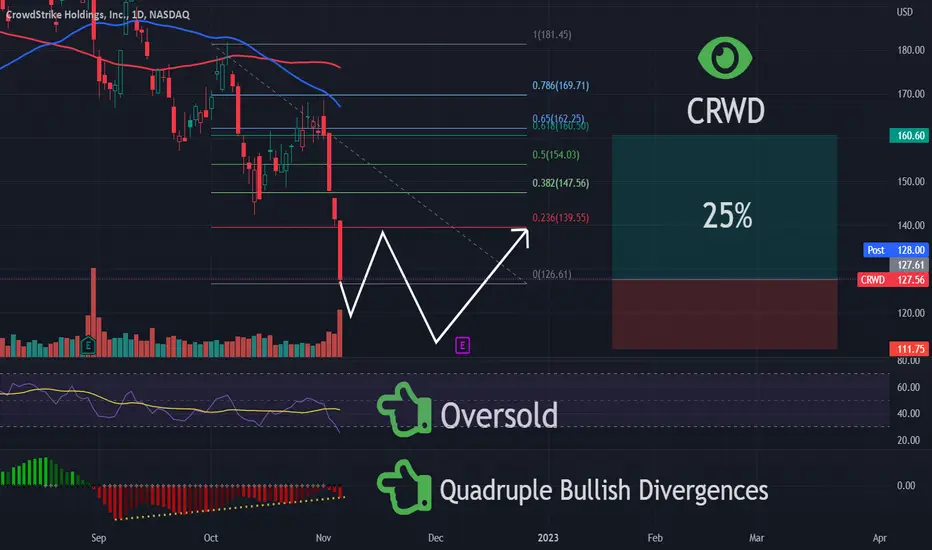

CRWD: Bullish setup points towards $240-270CRWD sits at the convergence of two mega trends: Cyber security and AI. Strong impulsive move off the low combined with a 3 wave pull back and subsequent break of the W1 high implies a low-risk entry point ahead of earnings. Ultimately expect CRWD to reach quadruple digits over the next few years.

RPD Rapid7 Options Ahead of EarningsAnalyzing the options chain of W Wayfair prior to the earnings report this week,

I would consider purchasing the 50usd strike price Calls with

an expiration date of 2023-5-19,

for a premium of approximately $3.65.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Looking forward to read your opinion about it.

PANW Palo Alto Networks Options Ahead of EarningsIf you haven`t bought PANW here:

Then Analyzing the options chain of PANW Palo Alto Networks prior to the earnings report this week,

I would consider purchasing the 190usd strike price Calls with

an expiration date of 2023-6-16,

for a premium of approximately $8.75

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Looking forward to read your opinion about it.

$ATDS: Potential Bullish DragonWe have Bullish Divergence at the second low of a Potential Double Bottom within a Bullish Dragon pattern and if it plays out we could see it go up to as high as 89 cents.

$RPD: 3 Rsing Valleys at the PCZ of a Bullish BatRPD has formed a 3 Rising Valleys pattern at the PCZ of a Bullish Bat Harmonic and is backtesting the Moving Averages as the 55 and 200 SMAs attempt to confirm a Golden Cross at the 0.886 PCZ.

$HACK: Cybersecurity is a good position to haveI like the idea of keeping 10% in this ETF, and periodically selling calls OTM each month as a way to generate extra yield on the capital allocated to it.

The recent Vulkan Files leak might serve as a short term catalyst, but the technicals were already favoring strong upside from this base before, and broad market conditions favor a bull market resurgence.

Best of luck!

Cheers,

Ivan Labrie.

$S - SentinelOne, Inc.RSI ( Relative Strength Index ) Positive & Bullish Divergence from the beginning of November 2022 continues to be in play. Sentinel One ( $S ) is continuing to see upward price action doing into earnings which are in about two weeks.

Are cloud computing companies offering a second bite Are cloud computing companies offering a second bite at the cherry?

On 18 December 2022, Jason Lemkin posted a blog titled “Right Back to Where We Were 3 Years Ago.” It caught my attention or those of us who have been following the performance of software-as-a-service (SaaS) cloud computing companies. It tells us, quite clearly, that the impact of the ‘pandemic pull-forward’ of demand for software consumption is completely removed from the 3-year performance number.

To us, it means that it is time to ask a simple question: is the market giving us a ‘do-over’, meaning that we can now access companies at something similar to ‘pre-pandemic’ levels, or is the jig up and the cloud business model doomed to fade away into the sunset?

SaaS companies have evolved significantly since 2019

In Figure 2, we wanted to look at valuation over the same period. Even if the share price performances of the underlying companies have run up and then fallen back in most cases—leading to the observed performance of the BVP Nasdaq Emerging Cloud Index—we have not been seeing companies reporting widespread negative year-over-year revenue growth. Instead, we’ve tended to see the revenue growth ranges shifting downwards, with the median figure for the Index now closer to the 30% level, whereas it was higher than 40% for a period of time ending roughly one year ago.

If prices have dropped but sales have continued to grow, it’s possible to see that the valuation opportunity at present is better than it was in December of 2019, 3-years ago. In Figure 2, we see that the price-to-sales ratio was 7.0-8.0x during this period, whereas presently it is below 4.5x. We agree that these stocks should be less expensive today, in that the risk today is higher and the cost of capital is also higher. We can’t know with certainty if the current price levels perfectly encapsulate this risk, but it is simply important to know that the risk does look like it is being accounted for.

In our opinion, within software-as-a-service companies, one must always marry looking at valuation with looking at revenue growth. Many of these firms, as yet, do not carry through positive net income to the bottom lines of their income statements, so if one can look at a reasonable fundamental, sales seems to make the most sense at this point in the development of the megatrend. We do view this as a megatrend, which means the time horizon we are thinking about is not the next 12 months or couple of years, but something that should unfold over a decade.

Growth, on the other hand, has come down more slowly than valuation. Now, this is ‘revenue growth’, not earnings growth or cash flow growth, but we note that companies are still growing, and some are still delivering results ahead of Wall Street’s expectations. If the Nasdaq 100 is growing something close to 10% and the BVP Nasdaq Emerging Cloud Index is growing something close to 30%, is this a worthwhile trade-off? The Nasdaq Index represents, predominantly, proven, established businesses, with some of the world’s most valuable companies, measured by their market capitalisations, getting the top weights. This risk profiles of these groups of stocks should be quite different, but if we are able to think not of the next 12 months but rather the next 10 years, does the difference in risk potentially make sense?

We do feel comfortable to conclude there is a better chance to make sense at the present valuation trade-off than it did at the near-term market high observed in November 2021, even if it’s impossible to know the future with certainty.

Where the rubber meets the road: what do SaaS companies do?

In our opinion, no discussion of cloud computing or SaaS companies is complete without giving some treatment to what the companies do. SaaS is just a business model—a way to provide/consume software that competes with other ways to provide/consume software. Do people prefer subscription models, or would they want to go back to a world where they need to buy a DVD and physically hold and use their own copy? If the software is necessary and valuable, and the company can execute their strategy, we have confidence in the long term. If, on the other hand, the software is discretionary and more ‘nice-to-have’ than needed, then there could be more risks. We see the following functional groupings as a starting point:

Cybersecurity: companies like CrowdStrike, SentinelOne, Cloudflare, Zscaler and Darktrace focus on cybersecurity. Subscribing to cybersecurity protection makes sense because we know that the attackers are always evolving. Stagnant protection would eventually lead to limited protection. Many SaaS cybersecurity firms are not necessarily trading at single digit price-to-sales multiples, but it’s also the case that cybersecurity has received massive attention from investors in 2022, largely due to the Russia/Ukraine conflict.

Software development: companies like Twilio, Atlassian and New Relic are involved with running platforms useful to software development. Twilio and Atlassian have faced challenges in their share price performance during their most recent quarterly earnings reporting periods. However, we believe that the service they provide for software development remains critical.

Business services: a company like Bill.com is very interesting, in that it is an example of a service that helps small and mid-sized firms manage their expenses. It’s a good case to remember because companies will tend to employ services like this to create efficiencies and save costs and time. We couldn’t ever say this company (or others like it) would be immune to recessionary pressures, but we find it important to note that it also may not be the first subscription to cut either.

Cloud computing and software-as-a-service companies do not have long histories of operation where we can look back at their performance during the Global Financial Crisis of 2008-09, and we’d have to assume that, if they were around in 2001 and 2002, their performance as the ‘tech bubble’ burst would have been significantly negative. To say these companies are completely resilient to recession is not a thesis that has been proving out in 2022. However, we’d note that their revenues are still growing, so it’s not the case either that these companies immediately reverted to negative revenue growth and collapsing fundamentals. If people view this as a megatrend, as we do at WisdomTree, the current period in the coming months could be a much more interesting entry point than anything we have seen recently, even if near-term performance could still be challenging.

CRWD SoS IncomingCRWD has same pattern as rest of cyber names, needs to finish up accumulation before markup:

Breakout level 106.80

- Initial target 113 by 1/30/2023 (this will be the sign of strength)

- Backup/retest to find support at 106-107 by 2/8/2023

- First Markup target will be 123 by 3/1/2023

Gap to fill from 118-136

Resistance at 109-116

CISO | Good Time to Enter | LONGCerberus Cyber Sentinel Corporation operates as a security services company in the United States. Its cybersecurity services include managed security, cybersecurity consulting, compliance auditing, vulnerability assessment, penetration testing, disaster recovery, and data backup solutions and cybersecurity training services, as well as security operations center set-up and consulting services. The company was founded in 2015 and is headquartered in Scottsdale, Arizona.

BB | Great Opportunity to Enter | LONGBlackBerry Limited provides intelligent security software and services to enterprises and governments worldwide. The company operates through three segments: Cybersecurity, IoT, and Licensing and Other. The company offers BlackBerry Cyber Suite, which provides Cylance AI and machine learning-based cybersecurity solutions, including BlackBerry Protect, an EPP and available MTD solution; BlackBerry Optics, an EDR solution that provides visibility into and prevention of malicious activity; BlackBerry Guard, a managed detection and response solution; BlackBerry Gateway, an AI-empowered ZTNA solution; and BlackBerry Persona, a UEBA solution that provides authentication by validating user identity in real time. It also provides BlackBerry Spark Unified Endpoint Management Suite, such as BlackBerry UEM, a central software component of its secure communications platform; BlackBerry Dynamics that provides a development platform and secure container for mobile applications; BlackBerry AtHoc and BlackBerry Alert secure and networked critical event management solutions; and SecuSUITE for Government, a multi-OS voice and text messaging solution, as well as BBM Enterprise, an enterprise-grade secure instant messaging solution. In addition, the company offers BlackBerry QNX, which provides Neutrino operating system and BlackBerry QNX CAR platform, and other products; BlackBerry QNX, an embedded system solution; BlackBerry Jarvis, a cloud-based binary static application security testing platform; BlackBerry Certicom cryptography and management products, and BlackBerry Radar asset monitoring solution; and BlackBerry IVY, an intelligent vehicle data platform, as well as enterprise and cybersecurity consulting services. Further, it is involved in the patent licensing and legacy service access fees business. As of February 28, 2022, it owned approximately 38,000 worldwide patents and applications. BlackBerry Limited was incorporated in 1984 and is headquartered in Waterloo, Canada.

DiscountInitial target is 109 by as early as Jan 20th, but might want to play out to March 2023. Bullish options activity at the 115-120 strikes big money.

Not Fin Advice

THIS is when you should be bottom fishing ! In this video, I've gone over the setup of generac and how there's a realistic 80-90% ROI potential over the next 2 months.

CyberSec/Computing Industry Q4 '22 Overview and CommentaryIt may just be that the market deities have heard our prayers. After unceasing YTD losses for NASDAQ, Q4 has provided a dose of much-need upside for embattled tech investors. Over the past month, QQQ is trading +6% in what sets a bullish baseline for the rest of NASDAQ. The broader rally in US tech equities is likely motivated by a number of factors, including a recent slowdown in Fed Reserve rate hikes, a surge in consumer spending around the holiday season, and a slight improvement in macroeconomic sentiment. Given these nascent yet promising signals, I want to examine their impact on an assortment of equities in the cybersecurity and computing industries.

Clustered around QQQ's trendline are a number of cyber mainstays that have closely tracked the market's recovery over the past month. For instance, Palo Alto Networks (PANW) is +4.33% and Hub Security (HUB.TA) is +4.71%, whereas cyber ETFs like BUG (+3.4%) and CIBR (+5%) all witnessed bullish price action movement. Though these players came in slightly behind QQQ's monthly performance, their single-digit gains are a strong testament to both retail and institutional demand for cyber security equities, particularly in today's world of increasingly sophisticated and frequent cyber attacks. HUB specifically has tracked impressive growth over recent weeks due to forward regulatory progress regarding its impending SPAC listing on NASDAQ via RNER.

The outlier of the field is CrowdStrike (CRWD), which slumped some 20% on Nov 30th in response to disappointing Q3 financials. A general conclusion we can draw from these findings is that overall, investors remain bullish on cyber security in the LT even if they are feeling more skittish about underperformers in the ST.

For the sake of comparison, I threw Nvidia (NVDA) and Taiwan Semiconductor (TSM) to see how things look a bit higher up the supply chain. Whereas cyber was up between 3-5%, NVDA and TSM both saw +22% gains over the past month. In my view, we're seeing this strong recovery as a delayed response to the volatility induced by the CHIPs Act gets finally priced in. For the uninitiated, the CHIPs Act was was passed this summer and represents a major federal subsidy to stimulate domestic chip and computing manufacturers. After weathering their fair share of volatility in Q3, chip staples like NVDA and TSM are already bouncing back strong.

Though cybersecurity and computing investors may be enjoying some relief, the market's response to new CPI and FOMC announcements this week may determine the direction NASDAQ assumes through end-Q4. In sum however, cyber and computing equities maintain bullish LT outlooks, and potential dips moving forward present strategic opportunities for industry-specific and tech investors.

S | Dollar Cost Average Into This One | WATCHINGSentinelOne, Inc. operates as a cybersecurity provider in the United States and internationally. The company's Extended Detection and Response (XDR) data stack that fuses together the data, access, control, and integration planes of endpoint protection platform, endpoint detection and response, cloud workload protection platform, and IoT security into a centralized platform. Its Singularity XDR Platform delivers an artificial intelligence-powered autonomous threat prevention, detection, and response capabilities across an organization's endpoints; and cloud workloads, which enables seamless and automatic protection against a spectrum of cyber threats. The company was formerly known as Sentinel Labs, Inc. and changed its name to SentinelOne, Inc. in March 2021. SentinelOne, Inc. was incorporated in 2013 and is headquartered in Mountain View, California.

Have you experienced ‘Tool Sprawl’ in Cybersecurity?We recognise we have a diverse array of readers, probably some individual business owners, some employees of large companies, some employees of smaller companies and possibly even some people who are retired or between jobs.

Whatever your situation—how many different cybersecurity tools are you aware of that you interact with? A password manager? A single-sign-on interface? A specialist tool focused on email? Another specialist tool focused on accessing a cloud computing infrastructure?

The fact of the matter is that the more you learn about cybersecurity, the more you are awakened to a large number of providers that each specialise in different types of protection. We saw the term ‘tool sprawl’ used to describe the 2022 cybersecurity landscape—we thought it painted an informative picture1.

How many tools are customers using?

Enterprise customers may be managing portfolios of 60-80 tools, with those on the extreme higher end of the spectrum possibly managing up to 1402. Imagine managing all of these tools over the course of a normal business operation.

One reason why the current environment is characterised by so many tools could relate to the progression of the Chief Information Security Office (CISO) role. 10 years ago, the way a ‘good CISO’ was defined largely had to do with buying and deploying tools. The CISO in 2022 is now much more a top priority for a company’s board and C-suite, and now a ‘good CISO’ is evaluated based on outcomes rather than deploying tools3.

A survey conducted by Gartner found that 88% of Boards of Directors view cybersecurity as a ‘business risk’ rather than a ‘technology risk4.’

Of course, the attack surface in 2022 has also massively expanded, and frequently companies may be launched around new types of artificial intelligence and machine learning techniques, to use one example that could also lead to the proliferation of companies.

Dealmaking is already taking off in 2022

Through 18 August 2022, private equity sponsors and their portfolio companies have backed 162 cybersecurity deals worldwide, valued at $34.9 billion. If this pace continues, it could surpass 2021’s tally of $36.4 billion across 308 transactions5.

One driver—valuations. 2020 and much of 2021 saw the most newly public cybersecurity companies, many of which were focused on the cloud, experience massive multiple expansion and therefore premium valuations. The growth was strong, but the prices were not inexpensive in an environment where the cost of capital had been very low for a very long time.

With the rise of inflation and then the shift in policy of many central banks going from expansionary support of growth, many of these companies experienced dramatic multiple compression. This allows private equity players focused on building consolidated product offerings to pick up interesting companies at much lower prices.

Thoma Bravo is one such player that has been quite active. Just in the identity space, Thoma has done deals to acquire Ping Identity for $2.8 billion and SailPoint for $6.9 billion6.

Consolidation is a big desire from customers—possibly a response to the ‘tool sprawl’ that we mentioned earlier. There is a feeling in the market that there might already be too many companies, so it’s not just about more innovation but also building integrated platforms so customers can go to one place and get more services.

Option3 is an example of a firm that has shifted from funding new firms to acquiring late-stage middle-market companies for buy-and-build strategies. They are planning to raise a $250 million buyout fund dedicated to a platform acquisition strategy7.

Private equity firms are attracted to cybersecurity companies for many reasons, but it is noted that they have exhibited lower churn rates than other Software-as-a-Service (SaaS) businesses. They also have tended to generate high margins.

What about the slowing economic environment?

As is the case with many things, historical comparisons can only take us so far. If we think about the state of cybersecurity in 2007-2009, encompassing the ‘Great Recession’, it was totally different. Cybersecurity budgets are much different in 2022 than they were in 2007 heading into that significant slowdown8.

One doesn’t need to look too far to see quotes from experts indicating that even if cybersecurity spending could be impacted by a slower economic environment, it most likely wouldn’t be as impacted as other areas. There are many things that are regulatory requirements or viewed as ‘table stakes’ to the ongoing operation of companies, which make them that much more difficult to cut.

Regulators are also upping the ante. The Securities and Exchange Commission in the US has explored a rule that would require disclosure of a ‘material cybersecurity incident’ in a public filing. Disclosure would also have to be quite quick after the event—possibly a response to certain types of attacks and breaches like SolarWinds, where months after the fact the scope of potential damage was growing and growing9.

Even if regulators do not mandate spending more on cybersecurity, their pursuit of certain types of rules would be likely to have that impact.

Conclusion: a megatrend for all seasons?

Norges Bank Investment Management, the world’s largest sovereign wealth fund at $1.2 trillion, recently indicated that cybersecurity is their biggest current concern, citing that it faces an average of three serious attacks each day. The fund sees roughly 100,000 attacks per year, and they classify about 1,000 of them as serious10.

Firms operating in the financial industry have been increasingly targeted, and firms operating in the Nordic region feel the proximity to Russia during the Ukraine conflict quite tangibly.

While many investment themes might be a bit discretionary or susceptible to delays in a slowing economic environment, cybersecurity is not one of them. We may not know the exact companies or services that will grow the fastest but backing away from focusing on security is not an option.

Sources

1 Source: Alspach, Kyle. “Thanks to the economy, cybersecurity consolidation is coming. CISOs are more than ready.” Protocol. 17 June 2022

2 Source: Alspach, 17 June 2022.

3 Source: Alspach, 17 June 2022.

4 Source: “Gartner Survey Finds 88% of Boards of Directors View Cybersecurity as a Business Risk.” Gartner. Press Release. 18 November 2021.

5 Source: Shi, Madeline. “PE dealmaking thrives in cybersecurity sector.” Pitchbook. 23 August 2022.

6 Source: Shi, 23 August 2022.

7 Source: Shi, 23 August 2022.

8 Source: Alspach, Kyle. “Cybersecurity spending isn’t recession-proof. But it’s pretty close.” Protocol. 6 June 2022.

9 Source: Alspach, Kyle. “’Game-changer’: SEC rules on cyber disclosure would boost security planning, spending.” VentureBeat. 10 March 2022.

10 Source: Klasa, Adrienne & Robin Wigglesworth.” Financial Times. 22 August 2022.

Cyber Security Players Under- and Outperforming $QQQAs we all know, its been a particularly volatile year for NASDAQ and tech equities across the board. At its lowest YTD (on 11.3), QQQ was down nearly 35%. A 7% intraday rally picked NASDAQ up from its bottom, but the trend is clear: with rising inflation, shrinking consumer savings, and broader downturns in the global macroeconomic environment, investors are losing their appetite for risker tech plays. Despite the gloom and doom that has fallen over many over course of what is one of US equity markets worst years on record, cyber security is one industry that has remained competitive, largely in response to two mega trends: 1) an uptick in the frequency and sophistication of cyber offensive operations, and 2) increased public scrutiny of cyber security as a consequence of the ongoing Russia/Ukraine war.

So which cyber security companies are outperforming baseline indices and which ones are falling short? At the top of our list are HUB.TA (+2.48% over past 3mo) and PANW (+1.24%) over the same time frame. Palo Alto Networks is a staple of many blue chip tech funds, and the company remains one of the leading names in the date security field. Despite significant volatility in both markets and supply chains, PANW has continued to post strong financials as it tracks modest gains amidst double-digit losses.

The MVP of the past 3 months is HUB Security, currently traded on TASE as HUB.TA but is eyeing an imminent NASDAQ listing via SPAC merger with RNER under the symbol HUBC. Driving HUB.TA's strong recent performance is anticipation over its US listing. Just in recent days the SEC released an amended F4, signifying that the final regulatory hurdles are being tackled prior to HUB's delisting from NASDAQ and simultaneous NASDAQ listing. HUBC will start trading at $10/share for an initial capitalization of ~$1.3b, so keep this outperformer on your watchlist.

Underperforming QQQ are other cyber blue chips that have struggled to eke out price action gains over the past quarter. Microsoft, Intel, Radware, and Crowdstrike are all underperforming the NASDAQ baseline due to a number of reasons. INTC is still struggling to finds it footing after the passage of the CHIPs Act in August, which fundamentally reorganized the domestic chip and computing manufacturing ecosystem. RDWR missed its Q3 earnings forecast, potentially contributing to its recent drop. Despite its poor recent performance, CRWD still retains the trust and admiration of analysts, who have flagged its an undervalued stock ready for gains given a change in the macro backdrop.

Its been quite the year for equity traders and investors, but I for one am looking forward to a bullish 2023. This is not financial advice, just some personal commentary. Trade responsibly.

CRWD | Good Entry Point | Swing TradeCrowdStrike Holdings, Inc. provides cloud-delivered protection across endpoints and cloud workloads, identity, and data. It offers threat intelligence, managed security services, IT operations management, threat hunting, Zero Trust identity protection, and log management. The company primarily sells subscriptions to its Falcon platform and cloud modules through its direct sales team that leverages its network of channel partners. It serves customers worldwide. The company was incorporated in 2011 and is based in Austin, Texas.

$HUB.TA Jumps >20% after Bosch Collab, Tech Market Lags BehindWhereas September proved to be one of the worst months in the history of equities markets, the volatility and ongoing uncertainty October has delivered thus far has been little reprieve. One outperformer amidst all of the red is Hub Security (TASE: HUB), a confidential computing and cyber security disruptor that is going public on NASDAQ via SPAC merger with RNER for an expected Q4 listing. Just last week Hub announced the submission of an updated F4 to the SEC, indicating that the company is checking off the final regulatory agenda items before the listing can take place.

My tech portfolio has been in danger zone for about the past 6 months, but HUB is a rare outperformer despite today's bearish conditions. Over the past month, HUB.TA +22% whereas both market baselines are down (NDX -5%, TA90 -7%) and sectoral ETFs (BUG -5.3%, HACK -4.9%). That's a differential of nearly 30%, and its in response to a clear though quiet catalyst.

On October 12th, HUB announced a collaboration with Bosch (NYSE: BSWQY), a major global producer of automotive products with a nearly $500bn market cap. Hub is providing cyber security for Bosch data centers in Hanover Germany in a pilot project that showcases the need for advanced solutions for critical infrastructure manufacturers. The data centers in question are for Bosch's cutting edge hydrogen fuel cells, meaning that collaboration testifies to both companies' dedication to ESG and net neutrality.

This latest partnership is the latest in a series of high-profile deals inked by Hub in the leadup to its NASDAQ debut. In recent months the company has entered engagements with both public and private sector actors ranging from MoDs to central banks and big-cap listed companies. The Bosch deal exerted a little reported though double-digit impact on Hub share price, and this is exactly the type of accumulation investors should be looking for on the heels of a listing.

Main Expected Path & Alt PathMapped out the most likely (solid green) and 2nd most likely (dashed black) trajectories:

Most likely:

174 by 10/19/2022

152 by 10/21

204 by 10/31

184 by 11/3

216 by 11/9/2022

2nd most likely/alt. (would take longer to play out than main path, see dates on chart):

195

162

247

215

267

Blackberry Fibo levelsFibo levels:

AB=0.61 XA

BC=0.61 AB=$6.65

0.78 XA=$63

1.6 BC=$70

0.88 XA=$94

2 BC=$120

2.24 BC=$169

1.13 XA=$250

2.6 BC=$288

1.41 XA=$763

3.6 BC=$1189

1.6 XA=$1752

FTNT Rolling LowerFortinet is a big player in cybersecurity with strong revenue growth and rapidly growing demand for its services. In the very Long-term, Fortinet should do well.

However, FTNT's technicals are signaling weakness on a more medium-term basis. The last year of FTNT price action has led to a rounded top formation. One could also argue that Fortinet shows signs of a head and shoulders pattern during the aforementioned period. Fortinet as of the past 7 months is now trading in a downward channel. The recent low recorded last week of 47.5 helps to confirm the continuation of bearishness in future trading. MACD on monthly/weekly/daily all are signaling further pain. The Weekly MACD is especially bearish, currently residing at its most negative level in FTNT's history.

Global market conditions are poor, and seemingly getting worse. Unfortunately, history has taught us that during periods of slowed economic activity amid monetary tightening great companies often sell off alongside their less successful peers (although not to the same degree).

To conclude: FTNT is experiencing a troubling technical outlook combined with a slowing economy/beaten-down consumer, I do not believe FTNT will be able to stay at such a high valuation with a p/e of 60, despite continued high demand. In the near term, I am looking for a move to 44.3 where the 50% fib retracement level sits. Looking further out, I expect a move down to the 30.2-27.1 range which has been an area of previous strong support as well as a 78.6% fib level. From there a rebound or consolidation period for Fortinet is likely.

As always this is not financial advice. Good luck!