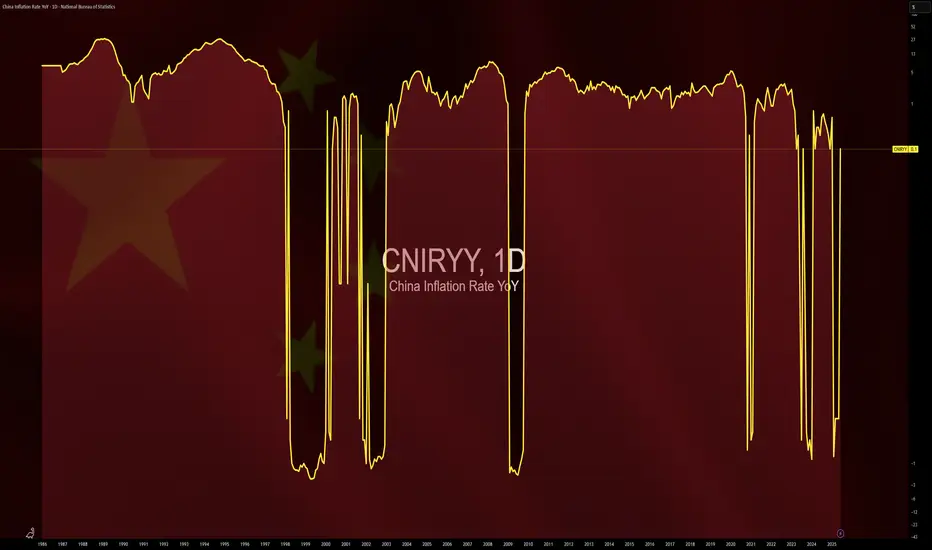

$CNIRYY -China's Inflation Data (June/2025)ECONOMICS:CNIRYY

June/2025

source: National Bureau of Statistics of China

- China’s consumer prices rose by 0.1% yoy in June 2025,

reversing a 0.1% drop in the previous three months and surpassing market forecasts of a flat reading.

It marked the first annual increase in consumer inflation since January, driven by e-commerce shopping events, increased subsidies for consumer goods from Beijing, and easing trade risks with the U.S.

Core inflation, which excludes volatile food and fuel prices, rose 0.7% yoy, marking the highest reading in 14 months and following a 0.6% gain in May.

On a monthly basis, the CPI fell 0.1%, after May's 0.2% drop, pointing to the fourth monthly decline this year.

Deflation

$CNIRYY -China CPI (May/2025)ECONOMICS:CNIRYY

May/2025

source: National Bureau of Statistics of China

- China's consumer prices dropped by 0.1% yoy in May 2025, matching the declines seen in the previous two months and slightly outperforming expectations of a 0.2% decrease.

This was the fourth straight month of consumer deflation, highlighting challenges from ongoing trade risks with the US, sluggish domestic demand, and concerns over job stability. Non-food prices were flat for the second month in a row, as increases in housing (0.1% vs 0.1% in April), clothing (1.5% vs. 1.3%), healthcare (0.3% vs 0.2%), and education (0.9% vs 0.7%) were offset by a sharper drop in transport (-4.3% vs -3.9%).

On the food side, prices fell at a steeper rate (-0.4% vs -0.2%), down for the fourth month.

Core inflation, which excludes volatile food and fuel prices, rose 0.6%, marking the highest reading since January and following a 0.5% gain in the prior two months.

On a monthly basis, the CPI declined by 0.2% in May, reversing a 0.1% gain in April and indicating the third monthly drop so far this year.

Futures on CME and Launch of XpFinance DeFi PlatformOn May 7, 2025, the XRP ecosystem received two major developments that signal a new chapter in its evolution. First, the Chicago Mercantile Exchange (CME) announced the launch of futures contracts for XRP. Shortly thereafter, developers behind the XRP Ledger unveiled XpFinance — the first non-custodial lending platform built on the network. These two events are poised to reshape XRP's market perception and could attract a wave of new investment.

XRP Futures on CME: A Leap Toward Institutional Adoption

Set to go live on May 19, the new CME product will enable investors to trade XRP through regulated futures contracts. This is a major milestone. With similar contracts already in place for Bitcoin and Ethereum, XRP becomes the third digital asset to gain such legitimacy in institutional markets.

The introduction of futures means greater liquidity, risk management tools, and a clear path for hedge funds, pension managers, and banks to engage with XRP — without needing to custody the underlying token directly. Analysts anticipate that this added market structure could drive up demand, especially if the rollout is smooth and met with trading interest.

XpFinance and the XPF Token: DeFi Comes to XRP Ledger

The second big announcement came from XpFinance, a new decentralized lending protocol. What sets it apart is its non-custodial model — users can lend assets and earn interest while retaining full control of their private keys. At a time when centralized platforms are under scrutiny, this approach appeals to security-conscious users.

XpFinance is powered by a new token, XPF, which will be used for staking rewards, fee payments, and governance. The pre-sale of XPF has already begun and is generating buzz, especially among XRP community members eager to participate in the first major DeFi initiative on the ledger.

Market Outlook and Analyst Forecasts

Reactions from analysts have been positive. According to a report from DigitalMetrics, if both the CME futures and XpFinance platforms gain traction, XRP could see a sharp upward move — potentially reaching $10 by summer 2025. That would represent a fourfold increase from its current price.

However, risks remain. Ripple Labs continues to face regulatory pressure in the U.S., and crypto markets overall remain volatile. Still, the general tone has shifted. With increasing institutional interest and expanding utility, XRP appears to be entering a new phase of growth.

Conclusion

The combination of institutional infrastructure and decentralized finance innovation makes May 2025 a pivotal moment for XRP. If these initiatives succeed, XRP could transition from a mid-cap altcoin to a primary digital asset in the eyes of both institutional investors and the broader crypto community. Whether this momentum will translate into long-term market dominance remains to be seen — but the foundation is clearly being laid.

End of the US Dollar ****** end of INFLATED USD

Deflation is coming.

Food for thought.

Because THE CYCLES EXIST and THEY RHYME.

$CNIRYY -China's CPI (March/2025)ECONOMICS:CNIRYY

March/2025

source: National Bureau of Statistics of China

- China's consumer prices fell by 0.1% year-on-year in March 2025, missing market expectations of a 0.1% increase and marking the second consecutive month of drop, as the ongoing trade dispute with the U.S. threatens to exert further downward pressure on prices.

Still, the latest drop was significantly milder than February’s 0.7% fall, supported by a smaller decline in food prices as pork prices accelerated and fresh fruit costs rebounded.

Meanwhile, non-food prices rose by 0.2%, reversing a slight dip of 0.1% in February, driven by increases in housing (0.1% vs 0.1%), healthcare (0.1% vs 0.2%), and education (0.8% vs -0.5%), despite a continued decline in transport costs (-2.6% vs -2.5%).

Core inflation, which excludes volatile food and fuel prices, rose 0.5% in March, rebounding from a 0.1% decrease in February. On a monthly basis, the CPI declined by 0.4%, a steeper fall than a 0.2% drop in February, marking the second straight month of contraction.

Why are Interest rates falling? Time to buy? We have seen an amazing fall in interest rates.

Bonds have looked to put in a local bottom.

Why are bonds showing signs of accumulation?

Is the bond market pricing in a recession?

I believe the recent decline in yields is due to commodity weakness.

Yields have soften because energy & base metals have become cheaper.

This drives the disinflationary narrative.

I think its to early to tell whether this decline is from demand or global weakness.

Is the market crashing? The SPY and IWM have completely diverged.

On the back of rate cut expectations, many investors are piling back into the junk and high beta names.

A clear relative strength move has occurred in small caps: IWM

Whilst the megacap stocks have been sold off.

The SPY sliced through the 50 MA yesterday and cofirmed the break below.

Although this is typically bearish, we are getting into an area of oversold support.

If the SPY gaps down tomorrow, I think traders will be buying the dip with both hands.

The IWM has blasted above the 50MA, basically moving the exact opposite of the S&P500.

The question remains....are small caps going to hold their gains inside of the weekly topping tail?

#HAWKISH #FED to remain until #US has positive real rates...Throughout US economic history

Only high real rates has brought down inflation

i.e Interest rates ABOVE the rate of inflation

obviously this will induce demand destruction and a decline in the earnings of companies

Lower p/e's and lower prices across the board.

#FinancialRESET

#HOUSING

#Nasdaq

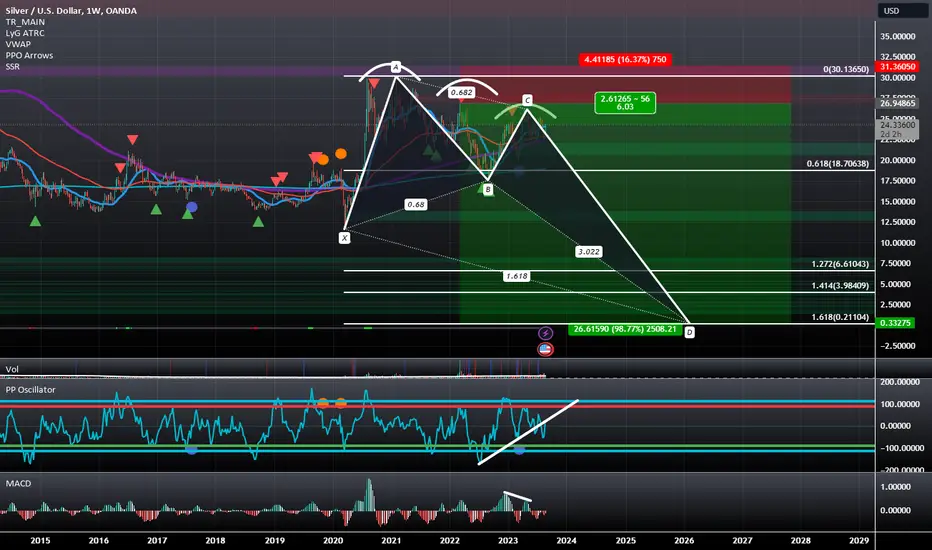

Silver is Setting Up to Drop Down to as Low as 21 Cents.Silver, after confirming Partial-Rise, has also formed 3 Falling Peaks and looks to be preparing to drop back below the bottom end of the range at 18 dollars. When it does this, it will enter a Butterfly BAMM Wave Structure that ends at the 1.272-1.618 Fibonacci Extensions. As a result of this new price action, I am lowering my price target to $6.61-$0.21 from my original $13 target.

Gold to Repeat the 80s by Undoing 20+ Years of Price ActionGold seems to be on track to completing a fractal of the mid 70s to Late 90s where it resets over 20 years of Price of Bullish Price action by way of losing over 70% of its value after a previous inflation fueled rally. Now we can see that we have the 20 Year Trend Line, A bearish Alt Bat, Bearish PPO Confirmation, and Bearish Divergence all as we head back towards trend where we will likely break and begin what will probably a long and slow decline down until we reach the 20-30 year lows at around $253.

This is basically a followup to my last 2 macro gold charts that I will provide in the related idea section below.

As Deflation Hits the Economy The Price of TIPs Should FallEarlier in 2022 I got some Bullish Exposure to Deflation by positioning Bearishly against TIPs (Treasury Inflation-Protected Securities) as can be seen here:

Fast-forward to today and we can now see the CPI declining and the TIPs declining even faster, This ETF Tracks the price of these TIPs and we can see that it is breaking through support even though the CPI has only retraced half way. If the CPI continues on this path and the Bond Market continues to price in Long Term Deflation, we should then see the pricing of this TIPs based ETF come down crashing in a big way. If that does happen, I would target at least the 1.618 Fibonacci Extension.

Inflation vs Innovation Can the Markets Handle the HeatGlobal markets face contradictory forces in 2023. Inflation still simmers as central banks tighten money supply worldwide. Geopolitical friction continues while economic growth likely slows ahead. Yet technological transformation charges ahead, with artificial intelligence poised for explosive improvements. Investors and policymakers must stay nimble in this uncertain environment.

After plunging painfully in 2022, stocks have rebounded with vigor so far this year. This despite raging inflation and the Federal Reserve's hawkish stance on interest rates. Hefty liquidity efforts in China likely buoyed prices. Investors may also have grown too pessimistic amid still-sturdy corporate profits. But sentiment could sour again if supply chain snarls resurface.

In bond markets, yields continue reflecting dreary growth expectations after last year's surge. The inverted yield curve especially screams pessimism on the near-term economy. Meanwhile, the Fed's bond portfolio shrinkage has yet to rattle markets. This implies the Fed's quantitative easing and tightening have limited impact on actual money supply, defying popular perception.

On inflation, early 2023 figures show it easing from 40-year heights but still well above the Fed's 2% bullseye. The Fed remains leery of declaring victory prematurely. Taming inflation sans triggering severe recession is an epic challenge. Geopolitical wild cards like the Russia-Ukraine war that evade the Fed's grasp will shape the outcome.

Amidst these crosscurrents, technological forces advance relentlessly. The frantic digitization around COVID-19 now gives way to even more seismic innovations. The meteoric success of AI like ChatGPT provides a mere glimpse of the transformations coming for healthcare, transportation, customer service and virtually every industry.

The promise appears gargantuan, with AI generating solutions and ideas no human could alone conceive. But the warp-speed pace also carries perils if ethics and safeguards fail to keep up. Mass job destruction and wealth hoarding by Big Tech could ensue absent mitigating policies. But wisely harnessed AI also holds potential to uplift living standards globally.

For investors, AI has already jet-propelled leaders like Google, Microsoft, Nvidia and Amazon powering this tech revolution. But smaller firms wielding these tools may also see jackpot gains, as costs plunge and new opportunities emerge across sectors. That's why non-US and smaller stocks may provide superior opportunities versus overvalued big US tech.

In conclusion, the global economic and financial landscape simmers with familiar threats and novel technological promise. Inflation may moderate but seems unlikely to vanish given lingering supply dysfunction and distortions from massive stimulus. Stocks navigate shifting sentiment amid rising rates and demand doubts. And machine learning progresses rapidly into a future we can now scarcely envision.

Nimbly navigating such turbulence requires flexibility, tech savviness and philosophical courage. Responsibly steering AI's development is a herculean challenge, to maximize benefits and minimize pitfalls. Individuals need to stay skilled while advocating protections against job disruption. Policymakers face wrenching tradeoffs between growth, inflation and financial stability - all compounded by geopolitics.

Yet within uncertainty lies opportunity for those poised to seize it. The future remains ours to shape, if we summon the wisdom and will to guide technology toward enriching human life rather than eroding it. The road ahead will be arduous but need not be hopeless, if compassion and conscience inform our creations.

The end of the tightening cycle is nighThe decline in the US inflation rate to more than a two-year low, marks a major step towards the end of the Fed’s historic monetary tightening cycle1. We believe key deflationary forces are in play – (1) weaker commodity prices (2) improvement in global supply chains (3) moderation in demand (4) lower inflation expectations. Therefore, the June decline in inflation is just the start of a series of decreases.

Softer than expected inflation report

As highlighted in the chart below, the details for June were also better than expected with key measures of underlying inflation coming in below forecasts. The inflation report suggests that some of the stickier components of inflation such as used cars and airline fares are also moderating.

It’s important to note that most of the rise in the June CPI can be attributed to housing, however because of the way it is calculated it tends to lag current conditions. The S&P Case Shiller Home Price Index which tends to lead CPI shelter by roughly a year, is already flat which highlights US inflation is likely headed lower. Inflation for labour intensive services such as restaurants, recreation and personal care remained higher in June reflecting the pass -through of higher wages and robust services demand2. Potential further softening in the labour market could bring these categories back to target consistent levels. Softening in the labour market was evident in June’s employment report (nonfarm payrolls rose by 209k versus consensus 230k) which was weaker than expected for the first time in 15 months3.

US Producer Prices confirmed a similar deflationary theme. The US Producer Price Index (PPI) inflation for June was softer than expected with headline and core PPI advancing 0.1% over the prior month4. Business surveys are also pointing to weakening pricing power, such as the Institute of Supply Management (ISM) services index which ties in with a lower inflation backdrop.

US inflation can’t prevent the July rate hike

While expectations for the July rate hike of 25Bps remain firmly in place, the market has scaled back expectations for a second hike – with 21bps / 3bps / 3bps of hikes priced for the July / September / November FOMC meetings5. The disinflation trend increases our belief that the Fed is close to, or will be, at the end of the current rate hike cycle.

Earnings take centre stage for the next leg of the rally

The key question now remains whether the market continues to trade off expectations of an easing narrative. Central bank policy has been the biggest drag for equities last year. The timing of the easing narrative comes at the heels of a volatile Q2 2023 earnings season. The S&P 500 Index earnings in the Q2 2023 are expected to decline 6.8% y/y, worse than the decline of 3.9% in the Q1 20233. This would be the largest earnings decline since the pandemic-fuelled 31.6% y/y decline in the Q2 2020. Earnings will be the key deciding factor for an extension in the current rally.

Investors will be keen to hear from management whether they are looking to adopt a leaner cost structure and ways they are looking to remove excess capacity. Investors will be looking for guidance on productivity and efficiency gains rather than the financial engineering we have witnessed over the past decade.

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Brent.Medium-term forecastSeries of 1-2 1-2 can lead brent price to 30 dollars area . It seems impossible today , but in the end of 2019 before the crash " everything was good " Recession , Deflation , liquidity problems will prices down . Everyone hopes on light recession , but everything will be much more worse

EUR/USD. Go dowm to 0.7 ?When all investors are sure that prices will continue to grow ( or decline) , It means reversal looms. The dollar is in the same situation . Everyone predicts inevitable weakness of dollar . They can offer many reasons and each of them look like a 100% signal . Something may change instantly . We are on the verge of this transformation.

The long—term target for EUR/USD remains the same - 0.7 . In the near future, they should do (or have already done) at least an annual cycle on the dollar index. This situation can be used as an opportunity to set a dollar position probably to all currencies.

VIX: VIX is at historic lows. won't go lower in this crisisVIX: VIX is at historic lows. won't go lower in this crisis. Will reach above 100s.

Daily and Weekly Rejection. 200 Billion Calls and market flat.Daily and Weekly Rejection. 200 Billion Calls of worth and market flat.

The US bought 200 billion worth of options is 200 billion of stocks to sell to get the market flat.

Lower highs and weekly and daily rejections on Friday. see the market getting its recession on Monday,

Delta in options across the board was at yearly highs. DAX rallied with EU meeting. But didn't make a new high.

Created a lower high and volume didn't make a new high on Friday. Many facts to see the market as topped out.

Options data with market analysis. See the market crash by about 50-70%. Because of the deflation cycle coming, we need.

The dollar needs to come back up and inflation needs to hit negative numbers to have expansion room for the future.

Best Regards

Robin,

TLT the play of the year?looking at TLT cloned the 5 wave ABC pattern and inserted it into now aligning it with the June rate decision to support a bullish move towards the long term 50% Fibonacci retracement level this could be the play of the year during a recession or deflation Bonds should rise

#BOND crisis to fuel monetary expansion The Fed is damned by inflation if they print, damned by bank runs if they dont print. And with recession on the way, history shows we could plumb to new lows if the Fed only prints enough to backstop banks and pensions. Early 2000s and early 1930s were two such cases where the Fed aggressively lowered rates for well over 18 months but markets continued to trend lower anyway. But 2008 ushered in central bank quantitative easing, so with QE at the Fed's disposal, it is more likely the growth of M2 will accelerate which will keep inflation stubbornly high if not higher.

A new factor that wasn't present before is that we have increasing M2 from China and Japan which has been a large driver of the market bounce we've seen in stocks and crypto since the start of the year.

The 2-yr and 10-yr rates are heading lower in a hurry. CME Fed futures currently predicts one more 25 bps hike to a terminal rate of 500-525 then three consecutive drops of 25 bps. Higher inflation would become the standard as the Fed would be forced to accept a higher inflation target well above 2% which Ray Dalio had predicted in one of his published pieces.

CAT - Technical Breakdown on watchCaterpillar is on the verge of triggering a bearish topping formation.

This stock has been a powerhouse during the rising rate environment.

if this market leader breaks down its signaling weakness in the economy and likely the industrial sector.

SIVB Meltdown- Canary in the Coal mind?Today we saw a systemic risk in the financial sector. The regional banks were hit extremally hard and as a result the Major banks saw sell side liquidation.

Where there's one cockroach, there's usually another.

Risk in the banking sector is the worst type of risk investors can ask for. Credit liquidity crisis is not something to mess around with.

SIVB looks like its in serious trouble potentially being exposed to fraudulent crypto loans that will likely default as well as failed speculative startups in the tech and health care space.

Lumber & Stocks DivergeLumber is signalling disinflation.

Stocks are signaling inflation.

There has bee a high correlation with stocks and lumber for about 18 months. Is this correlation officially breaking or does it imply we will see some weakness in stocks?

Right now lumber is showing weakness.

Christmass delivery projection.I welcome you and wish you good luck in these times.

Today, I made some sketch, how should, or would be strong year ending.

While I still stay sceptic fundamentally and also on technicals .

It due to downtrend, recession and upcoming deflation waiting in 2023.

Never hold you money at any exchanges ;- )

There's more options and sites like Fixed Float, or directly in self custody wallets.

Yours Emvo.

*This is not any financial advice.