NVDA Multi-Asset Income StrategyRecently, I've been looking a lot at Yield Max ETFs and other options-based yield ETFS more generally such as QDTE, XDTE, RDTE, QQQI, SPYI, YQQQ (inverse), etc.

One possible way to outperform SPY & QQQ, may be to consider investing in such ETFs, though this is purely theoretical s tradingview does not provide a quality backtesting software for a complex multi-asset, multi-directional strategy like this. Nothing in this strategy should be considered financial advice and there are various factors to consider, such as beta decay, mismanagement of the ETFs, tax advantages/disadvantages, reinvestment risk, risks associated with options in income-based derivatives, risks with leveraged assets, and the obviously risks with inverse assets.

In this chart, we are looking at the leveraged ETF NVDL, which tracks NVDA. It's important to note that this asset will decay whenever NVDA trades sideways or goes down over substantial periods of time, and when NVDA goes down the negative % returns are multiplied. Therefore a trader or "sophisticated investor" (FINRA term) needs to not only optimize their position size for a trading period, but also optimize the timing of entry's and exits on multiple position. They will also want to model, volatility, decay, and reinvestment risk (arguably the hardest in this case. This post will not discuss the specifics of those and instead, these topics should be considered as a form of "homework" for you, the reader to think about and discuss in the comments as food for thought.

In this theoretical multi-asset income strategy, risk is managed through the use of income based ETFs that are either bullish or bearish, I think of this as " directional income ". In this case, NVDY is the bullish income asset and DIPS is the bearish income asset, both of which pay dividend monthly and their price performance behaves very similar to a leveraged ETF, in the sense that they only really increase when the underlying the underlying asset moves in the direction of the income derivative. Theoretically, by managing position size with the use of a modified Kelly Criterion which accounts for fed rates, the decay of the asset, and timing (through technical analysis, seasonality and quantitative analysis), I wonder if a trader could swing-trade between various income-based derivatives and leveraged assets, in order to optimize both income and grow irrespective of market conditions.

In truth, I'm still not sure if this is a completely degenerate idea no different to the way banks stacked bad loans together in 2008 and slapped a Grade A rating, and in the process over valued quantitative methods (see the book "Quants") as a sort of grad delusion to completely avoid risks, like a doctor wishing to delete pain from the world with an addictive pill, shilled by Big Pharma... Only in this case, instead of CMBS, it's ETF, leveraged ETFs, options on both, creating a derivative, then stacking more derivative on top of that...

Who knows, though... Maybe this could be a way to profit from this madness?

I honestly don't know.

What I do know is, I find the idea of " directional income " as a hedge more appealing than an inverse leveraged ETF and I'm curious how to apply this to either a single asset or multi-asset portfolio. It's a very interesting idea and I plan to spend the year exploring this idea at the cost of my own capital, rather than someone else's capital.

Directional

Options Blueprint Series Strangles vs. StraddlesIntroduction

In the realm of options trading, the choice of strategy significantly impacts the trader's ability to navigate market uncertainties. Among the plethora of strategies, the Strangle holds a unique position, offering flexibility in unclear market conditions without the upfront costs associated with more conventional approaches like the Straddle. This article delves into the intricacies of the Strangle strategy, emphasizing its application in the volatile world of Gold Futures trading. For traders seeking a foundation in the Straddle strategy, refer to our earlier discussion in "Options Blueprint Series: Straddle Your Way Through The Unknown" -

In-Depth Look at the Strangle Strategy

The Strangle strategy involves purchasing a call option and a put option with the same expiration date but different strike prices. Typically, the call strike price is higher than the current market price, while the put strike price is lower. This approach is designed for situations where a significant price movement is anticipated, but the direction of the movement is uncertain. It's particularly effective in markets prone to sudden swings, making it a valuable strategy for Gold Futures traders who face volatile market conditions.

Advantages of the Strangle strategy include its lower upfront cost compared to the Straddle strategy, as options are bought out-of-the-money (OTM). This aspect makes it a more accessible strategy for traders with budget constraints. The potential for unlimited profits, should the market make a strong move in either direction, further adds to its appeal.

However, the risks include the total loss of the premium paid if the market does not move significantly and both options expire worthless. Therefore, timing and market analysis are critical when implementing a Strangle in the gold market.

Example: Consider a scenario where Gold Futures are trading at $1,800 per ounce. Anticipating volatility, a trader might purchase a call option with a strike price of $1,820 and a put option with a strike price of $1,780. If gold prices swing widely enough in either direction, the strategy could yield substantial profits.

Strangle vs. Straddle: Understanding the Key Differences

The Strangle and Straddle strategies are both designed to capitalize on market volatility, yet they differ significantly in execution and ideal market conditions. While the Straddle strategy involves buying a call and put option at the same strike price, the Strangle strategy opts for different strike prices. This fundamental difference impacts their cost, risk, and potential return.

Cost Implications: The Strangle strategy is generally less expensive than the Straddle due to the use of out-of-the-money options. This lower initial investment makes the Strangle appealing to traders with tighter budget constraints or those looking to manage risk more conservatively.

Risk Exposure and Profit Potential: Although both strategies offer unlimited profit potential, the Strangle requires a more significant price move to reach profitability due to its out-of-the-money positions. Consequently, the risk of total premium loss is higher with Strangles if the anticipated volatility does not materialize to a sufficient degree.

Market Conditions: Straddles are best suited for markets where significant price movement is expected but without clear directional bias. Strangles, given their lower cost, might be preferred in situations where substantial volatility is anticipated but with a slightly lower conviction level, allowing for larger market moves before profitability.

In the context of Gold Futures and Micro Gold Futures, traders might lean towards a Strangle strategy when expecting major market events or economic releases that could induce significant gold price fluctuations. The choice between a Strangle and a Straddle often comes down to the trader's market outlook, risk tolerance, and cost considerations.

Application to Gold Futures and Micro Gold Futures

Implementing a Strangle in the Gold Futures market requires a keen understanding of underlying market conditions and volatility. Given the precious metal's sensitivity to global economic indicators, political instability, and changes in demand, traders can leverage the Strangle strategy to capitalize on expected price swings without committing to a directional bet. When applying a Strangle to Gold Futures, selecting the appropriate strike prices becomes crucial. The goal is to position the OTM options in a way that balances the potential for significant price movements with the cost of premiums paid. This balance is critical in scenarios like central bank announcements or inflation reports, where gold prices can experience sharp movements, offering the potential for Strangle strategies to flourish.

Long Straddle Trade-Example

Underlying Asset: Gold Futures or Micro Gold Futures (Symbol: GC1! or MGC1!)

Strategy Components:

Buy Put Option: Strike Price 2275

Buy Call Option: Strike Price 2050

Net Premium Paid: 11.5 points = $1,150 ($115 with Micros)

Micro Contracts: Using MGC1! (Micro Gold Futures) reduces the exposure by 10 times

Maximum Profit: Unlimited

Maximum Loss: Net Premium paid

Risk Management

Effective risk management is paramount when employing options strategies like the Strangle, especially within the volatile realms of Gold Futures and Micro Gold Futures trading. Traders should be acutely aware of the expiration dates and the time decay (theta) of options, which can erode the potential profitability of a Strangle strategy as the expiration date approaches without significant price movement in the underlying asset. To mitigate such risks, it's common to set clear criteria for adjusting or exiting the positions. This could involve rolling out the options to a further expiration date or closing the position to limit losses once certain thresholds are met.

Additionally, the use of stop-loss orders or protective puts/calls as part of a broader trading plan can provide a safety net against unforeseen market reversals. Such techniques ensure that losses are capped at a predetermined level, allowing traders to preserve capital for future opportunities.

Conclusion

The Strangle and Straddle strategies each offer unique advantages for traders navigating the Gold Futures market's uncertainties. By understanding the distinct characteristics and application scenarios of each, traders can make informed decisions tailored to their market outlook and risk tolerance. While the Strangle strategy offers a cost-effective means to leverage expected volatility, it also necessitates a disciplined approach to risk management and an acute understanding of market dynamics.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Options Blueprint Series: Straddle Your Way Through The UnknownIntroduction

Options trading offers a dynamic avenue for investors to navigate the financial markets, and among the myriad of strategies available, the Straddle strategy stands out for its unique ability to capitalize on market volatility without necessitating a directional bet. This article, part of our Options Blueprint Series, zooms in on utilizing Options on S&P 500 Futures (ES) to employ the Straddle strategy. The S&P 500 index, embodying a broad spectrum of the market, presents a fertile ground for options traders to implement this strategy, especially in times of uncertainty or ahead of major market-moving events.

Understanding S&P 500 Futures Options

Options on S&P 500 Futures offer traders and investors a versatile tool for hedging, speculating, and portfolio management. These options grant the holder the right, but not the obligation, to buy or sell the underlying S&P 500 Futures at a predetermined price before the option expires. Trading on the Chicago Mercantile Exchange (CME), these instruments encapsulate the market sentiment towards the future direction of the U.S. economy and stock market. Their popularity stems from the leverage they offer, alongside the efficiency and liquidity provided by the CME, making them an effective instrument for executing sophisticated strategies like the Straddle.

The Core of the Straddle Strategy

The Straddle strategy in options trading is a powerful method to exploit volatility. It involves simultaneously buying a call and put option on the same underlying asset, with identical strike prices and expiration dates. This non-directional strategy is designed to profit from significant price movements in either direction. For S&P 500 Futures options, this means traders can position themselves to benefit from market swings without trading the trends. The beauty of the Straddle lies in its simplicity and the direct way it captures volatility, making it a commonly used strategy in times of economic reports, earnings announcements, or geopolitical events that can trigger substantial market movements.

Executing the Straddle Strategy on S&P 500 Futures Options

Implementing a Straddle with S&P 500 Futures options involves a calculated approach. The first step is selecting the right expiration date and strike price, typically at-the-money (ATM) or near-the-market values of the ES options, to ensure a balanced exposure to price movements. Timing is crucial; initiating a Straddle ahead of anticipated volatility spikes can be more cost-effective, as option premiums tend to rise with increased uncertainty. Utilizing TradingView's comprehensive analysis tools, traders can gauge market sentiment, identify potential volatility catalysts, and choose the optimal entry points. Managing the trade requires vigilance, as the key to maximizing profits with a Straddle lies in the ability to respond adeptly to market shifts, possibly adjusting positions to mitigate risks or capture emerging opportunities.

Market Analysis for Straddle Execution

For a successful Straddle execution on S&P 500 Futures options, thorough market analysis is indispensable. Volatility, the lifeblood of the Straddle strategy, can be assessed using various technical indicators available on TradingView, such as the Average True Range (ATR) or the CME Group Volatility Index (CVOL). Economic indicators and scheduled events also play a crucial role. Traders should closely monitor the economic calendar for upcoming reports or news that could sway the market, adjusting their strategies accordingly. By analyzing past market reactions to similar events, traders can better predict potential price movements, enhancing their Straddle trade's effectiveness.

Implied Volatility and CVOL

Understanding Implied Volatility (IV) when trading Straddles is essential. IV reflects the market's expectation of a security's price fluctuation and significantly influences option premiums.

Since the S&P 500 Futures is a CME product, examining CVOL could provide an advantage to the trader as CVOL is a comprehensive measure of 30-day expected volatility from tradable options on futures which can help to understand if options are underpriced of overpriced at the time of the trade.

Strategic Risk Management for Straddle Trades

Risk management is paramount in options trading, especially with strategies like the Straddle that involve multiple option positions. Setting predefined exit criteria can help traders lock in profits or cut losses, ensuring that one side of the Straddle does not negate the other's gains. It's also vital to consider the time decay (theta) of options, as it can erode the value of positions as expiration approaches. Utilizing stop-loss orders or adjusting the Straddle to a more defensive setup, like transforming it into an Iron Condor, are ways to manage risk. Moreover, traders must keep an eye on liquidity to ensure they can adjust or exit their positions without significant slippage.

Case Study: Navigating Market Uncertainty with a Straddle on ES Options

Let's examine a hypothetical scenario where a trader employs a Straddle strategy on S&P 500 Futures options ahead of a potential major expected movement as the S&P 500 gaps up significantly after making a new all-time high which may lead to an unsustainable market condition. The trader selects ATM options with a 50-day expiration, expecting a sharp price movement in either direction.

Key S&P 500 Contract Specs

Tick Size (Minimum Price Fluctuation): 0.25 index points, equivalent to $12.50 per contract.

Trading Hours: Nearly 24-hour trading, starting from Sunday evening to Friday afternoon (Chicago times) with a 1-hour break each day.

Cash Settlement: No physical delivery of goods; contracts are settled in cash based on the index value.

Margin Requirements: Traders must post an initial margin and a maintenance margin, set by the exchange as a recommendation, to hold a position. These margins can vary based on market volatility and changes in the index value. Currently: $11,800 per contact.

Trading Venue: S&P 500 Futures are traded on the Chicago Mercantile Exchange (CME).

Access and Participation: Available to individual and institutional investors through futures brokerage accounts.

Leverage and Risk: Futures offer leverage, meaning traders can control large contract values with a relatively small amount of capital, which also increases risk.

Long Straddle Trade-Example

Underlying Asset: E-mini S&P 500 Futures (Symbol: ES1!)

Strategy Components:

Buy Put Option: Strike Price 5200

Buy Call Option: Strike Price 5200

Net Premium Paid: 195 points = $9,750

Micro Contracts: Using MES1! (Micro E-mini Futures) reduces the exposure by 10 times

Maximum Profit: Unlimited

Maximum Loss: Net Premium paid

Conclusion

The Straddle strategy, when applied to S&P 500 Futures options, offers traders a potent tool to potentially profit from market volatility without taking a directional stance. By understanding the nuances of the S&P 500 Futures options market, meticulously planning their Straddle setups, and employing rigorous risk management practices, traders can navigate the complexities of the options landscape with confidence. Continuous learning and practice, particularly in simulated trading environments, are essential for refining strategy execution and enhancing trade outcomes.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Options Blueprint Series: Iron Condors for Balanced MarketsIntroduction:

In the nuanced world of options trading, the Iron Condor strategy stands out as a sophisticated yet accessible approach, especially suited for markets that exhibit a balanced demeanor. This strategy, belonging to the "Options Blueprint Series," is designed for traders who seek to harness the potential of stable markets. Iron Condors offer a way to generate profit from an underlying asset's lack of significant price movement, making it an ideal choice for periods characterized by low volatility.

Understanding Iron Condors:

An Iron Condor is a non-directional options strategy that aims to profit from a market that moves sideways or remains within a specific range. This strategy involves four different options contracts, specifically two calls and two puts, all with the same expiration date but different strike prices. It combines a bull put spread and a bear call spread to create a profitable zone.

To construct an Iron Condor, a trader sells one out-of-the-money put and buys another put with a lower strike price (forming the bull put spread), while also selling one out-of-the-money call and buying another call with a higher strike price (forming the bear call spread). The essence of this strategy is to collect premium income from the options sold, with the trade being most profitable if the underlying asset's price remains between the middle strike prices of the calls and puts sold.

The Iron Condor is lauded for its ability to generate returns in a stagnant or mildly volatile market, making it a preferred strategy among traders who anticipate little to no significant price movement in the underlying asset. However, it requires precise execution and an understanding of the underlying market conditions to mitigate risk and optimize potential returns.

Market Analysis:

The current financial landscape often presents scenarios where markets exhibit balanced behavior, characterized by low volatility and minor price fluctuations. In such environments, traditional directional trading strategies might not always offer the desired outcomes due to the lack of significant market movements. This is where the Iron Condor strategy shines, serving as an ideal tool for traders aiming to capitalize on market stability.

Balanced markets are typically observed during periods of economic uncertainty or when major market-moving events are anticipated but have yet to occur. Investors' wait-and-see attitude during these times results in a trading range where prices oscillate within a relatively tight band. Utilizing Iron Condors in these scenarios allows traders to define a price range within which they believe the market will remain over the life of the options contracts. Successfully identifying these ranges can lead to profitable trades, as the sold options will expire worthless, allowing the trader to retain the premiums received.

Implementing Iron Condors under such conditions requires a keen understanding of market indicators and trends. Traders must analyze historical volatility, forthcoming economic events, and overall market sentiment to gauge whether the market conditions are conducive to this strategy. This analysis is crucial in setting the strike prices for the options contracts, determining the width of the Condor's wings, and ultimately, the trade's risk-reward profile.

Introduction to Silver Futures:

Silver Futures represent a standard contract for the future delivery of silver, a precious metal with both investment appeal and industrial applications. Trading on the COMEX exchange, these futures provide a crucial tool for hedging against silver price volatility and speculating on future price movements.

Key Features of Silver Futures:

Contract Specifications: A standard Silver Futures contract on the COMEX division of the New York Mercantile Exchange (NYMEX) typically involves 5,000 troy ounces of silver. The price quotation is in U.S. dollars and cents per ounce.

Point Values: Each tick (0.005) movement in the silver price represents a $25 change in the value of the Silver Futures contract. This point value is critical for calculating potential profits and losses in silver trading.

Trading Hours: Silver Futures are traded almost around the clock (23 hours per day) in electronic trading sessions, providing opportunities to react to global economic events as they unfold.

Margin Requirements: Trading Silver Futures requires a margin deposit, a form of collateral to cover the credit risk. The initial margin is set by the exchange and varies with market volatility. The current recommendation set by COMEX is $8,000 per contract.

Options on Silver Futures:

Options on Silver Futures offer traders the right, but not the obligation, to buy (call options) or sell (put options) the futures contract at a specified price before the option expires. These instruments allow for strategies like Iron Condors, providing additional flexibility in managing silver price exposure.

Applying Iron Condors to Silver Futures Options:

Implementing Iron Condors within the realm of Silver Futures Options requires a strategic selection of strike prices that reflect a balanced market's expected trading range. By capitalizing on Silver's historical volatility patterns and current market analysis, traders can construct Iron Condors to optimize their chances of success.

Trade Setup:

Underlying Asset: Silver Futures (Symbol: SI1!)

Market Conditions: Anticipation of a stable to mildly volatile market environment.

Strategy Components:

Sell Put Option: Strike Price $22.50

Buy Put Option: Strike Price $21.95

Sell Call Option: Strike Price $23.85

Buy Call Option: Strike Price $24.30

Net Premium Received: 0.2680 points = $1,340

Maximum Profit: Net Premium Received $1,340 per contract

Maximum Loss: Difference between strike prices minus net premium received = 0.55 / 0.005 x 25 – 1,340 = $1,410 per contract

Trade Rationalization:

This trade setup is designed to profit from a range-bound market, where the price of silver is expected to remain between key support and resistance price levels until the options' expiration. The selected strike prices reflect a balanced view of the silver market, aiming to maximize premium income while limiting risk exposure. The trade's success hinges on silver prices staying within the defined range, allowing all options to expire worthless and the trader to retain the collected premiums.

Trade Management:

Managing risks associated with Iron Condors involves closely monitoring silver prices and being prepared to adjust the strategy in response to significant market movements. This may include rolling out positions to different strike prices or expiration dates, or closing out the position to mitigate losses. Understanding the nuances of Silver Futures and their options is crucial for effective risk management in this strategy.

Risk Management:

Effective risk management is paramount when employing Iron Condors, particularly in the volatile commodities market. The Iron Condor strategy, by design, limits the maximum potential loss to the difference between the strike prices of the inner options minus the net premium received. However, market conditions can change swiftly, leading to potential challenges that necessitate proactive risk management techniques.

Monitoring Market Conditions: Continuous observation of market dynamics is essential. Significant economic announcements, geopolitical events, or changes in supply and demand can impact silver prices drastically. Traders should stay informed and ready to act if the market moves against their position.

Adjusting Positions: In the event of unfavorable market movements, traders may need to adjust their positions. This could involve closing out the position early to cut losses or 'rolling' the strategy to different strike prices or expiration dates to better align with the new market outlook.

Use of Stop-Loss Orders: While not always applicable in options trading, setting conditional orders to exit positions can help limit losses. For Iron Condors, this might mean closing the trade if the potential maximum loss is approached.

Diversification: Employing Iron Condors as part of a broader, diversified trading strategy can help mitigate risks. No single trade should expose the trader to disproportionate risk.

Conclusion:

The Iron Condor strategy offers a prudent approach for traders looking to capitalize on balanced markets, such as those often encountered with Silver Futures and Options. By selling options with strike prices outside the expected range of movement and protecting the position with further out-of-the-money options bought, traders can receive premium income while having a clear understanding of their maximum risk exposure.

This strategy thrives in environments of low to moderate volatility, where the underlying asset—silver, in this case—is expected to fluctuate within a predictable range. The inclusion of Silver Futures and Options in this strategic framework not only illustrates the versatility of Iron Condors but also underscores the importance of comprehensive market analysis and robust risk management practices.

By meticulously crafting their positions, monitoring market conditions, and being prepared to make adjustments as necessary, traders can effectively navigate the complexities of the commodities market, harnessing the potential of Iron Condors to enhance their trading portfolio.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Analysis of this currency TFUEL USDT 1DFor long-term purchase and holding, this currency has growth potential

XU switch clutch DAY 2Tuesday was choppy but after 10:10am price started falling as projected.

Price formed an ascending channel on the 5 Min TF, PRICE faked out and then dropped.

Anticipating a drop I entered once price rejected going above the horizontal arrows!

Happy Tuesday Traders!

Large head and shoulders on Bitcoin MonthlyI have been unhappy with the projections of where Bitcoin is headed. Nobody seems to really know. There seems to be a heavy sentiment of downward, capitulation and some of the usual calls for ATH, which makes sense but I haven’t seen a pattern that looks strong. On the monthly I noticed a pattern that I like. The 5 EMA (yellow) - is about to make the right shoulder of a head and shoulder pattern.

It is an interesting pattern because it is neither capitulation, nor is it new all-time high. Price would need to climb to about 57000 to fully form the shoulder before it drops. This is my first idea so thanks for reading.

One Swing trading Equity Option -APOLLOHOSPAPOLLO HOSP sell below 4293

SL above 4350/4450 (depending on your target)

Target- 4250, 4225, 4205, 4142, 4050

Option strategy :- +1x 26MAY2022 4300PE - ₹ 185.2

-1x 26MAY2022 4200PE - ₹ 138.2

Max. Profit ₹ +6,625 (35.19%)

Max. Loss ₹ -5,875 (-31.21%)

Max. RR Ratio 1:1.13

Breakevens 0-4253.0

Directional analysisPresented is a 1 hr simple directional analysis pending a break through channel resistance or support.

A break and close out above 1.07400 followed by a bullish bar may indicate bullish movement to retest next resistance of 1.0800.

A break and close out below support 1.07100 followed by a bearish bar may indicate continuation to retest next support of 1.06400.

Pending the outcome out RSI and MACD will react. Bearish movement will trigger MACD/SIGNAL to reverse just under 0 line while RSI breaches below 50. Bullish movement will trigger MACD/SSIGNAL line to cross through 0 line while RSI breaches 50 with continuation.

Be patient on entry. Please comment with comments and ideas. Thank you.

FIVE. Rising wedge, turned normal wedge. Outcome TBD.Trade in the direction of the move out seems to be the best answer.

This is really not as difficult as it's cracked up to be sometimes.

Once I can cure myself of the overwhelming desire to use the markets as entertainment instead of simply checking in and checking out... I think I might actually make a lot of money.

------

Ok, have a good day everyone.

Biogen - Pivot Point - Beware EarningsHey traders, I was searching for potential pivot points for long call opportunities and I came across Biogen NASDAQ:BIIB and thought to myself "Hey! This looks good!"... that is until I saw they're expected to report earnings tomorrow. But otherwise, take a look at the chart above. One thing you will see...is that its been trading within a range. I highlighted this range on the chart using the labels Support and Resistance. The other thing to notice is where the stock price is relative to the Bollinger Bands. If earnings wasn't tomorrow, I would be more inclined to purchase a call here because the stock price is holding at the lower BollingerBand at 2 standard deviations. Stock price has a tendency to move back towards the 8 EMA on the daily chart above, so if we are playing the odds, this trade would be in favor to the upside. But this trade is invalidated since we have a major news event happening tomorrow.

So... let's see what happens. In my experience, if a stock breaches the lower Bollinger Band after an earnings report, it's no longer a valid long call trade. In the past, I have made the mistake in thinking with 2 standard deviations... I have a 95% chance that price will fall back within the BollingerBands within the lifespan of the trade. But often what ends up happening is the stock price moves in a "L shaped" pattern where the vertical end of the "L" is the drop after the major news event and the horizontal side of the "L" is the sideways price action the stock experiences for days ( sometimes weeks ) following the news event.

In this situation, the stock usually comes back within the 2 standard deviation range... but not until Theta decay has eaten up your call option's premium. So even if you eventually get the direction right, time will not be kind to your long call position. This is where applying the Put Credit Spread strategy comes in handy. With Put Credit Spreads, you are an option seller, rather than an option buyer. Time will erode the premiums of the spread making it cheaper to buy back later. What's even better, is if the stock moves up... then the Delta will negatively affect the puts making them cheaper to buy back.

Anyways, let's follow Biogen tomorrow and see if they beat or miss earnings and how the stock price reacts to the news. If it heads lower, we'll follow up in next weeks idea regarding the put credit spread setup.

Liking the XLM/BTC bullish look!The bounce off the 61.8% Fibonacci retracement support was key and a great sign for the bulls. The Average Directional Index (ADX), which measures the strength of trend momentum, is maintaining strength for the bulls.

Since the green positive directional index line did not cross the red negative directional index line the 61.8% level becomes a nice floor.

I am looking to buy on dips with a stop below the marked support level. New highs expected.

Happy trading!

Thoughts?

EUR/USD - INTRADAY TRADING TOOLS AND IDEASBull trend is still in place so far so the best probability remains to buy every retracement to follow the flow.

Always calculate the cost of the stop to properly size your trade (cost should not exceed 5/6% of your account)

Feel free to ask if you need more details about my trading tools and ideas.

This graph and comments can be updated during the european session

Good day!

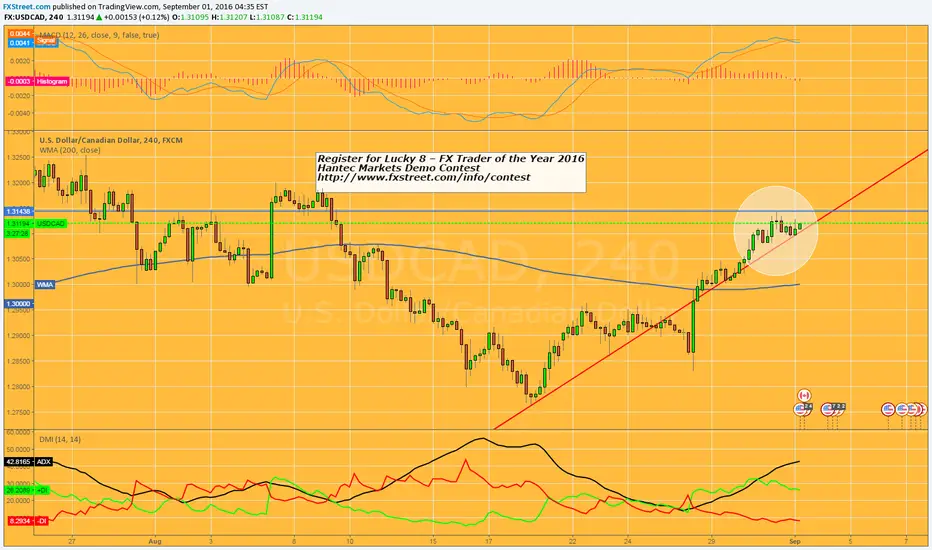

FORECAST: USDCADThe price action in the area of resistance at 1.3143, indicate the strategy. When the PMI and record as certain price, better to be outside. Once, trend, closing, stop in relative defined above.

For the price target, we use trend, mommentum, heikin Ashi, Price Action, that with you to feel more comfortable.

Great Trading.

www.fxstreet.com

Resistance Broken & Stong UptrendResistance has been broken and a strong uptrend is occuring. Watching the DMI to see when the trend slows down, long until then.

DRE DUKE REALTY Important trendline test from above= more UP?DRE has been in the news as a strong performer in the recent months, and has outperformed the S&P on a larger time frame. Zooming in, we can see a small HNS on the 15min, that should bring us to test the red longer time frame trendline.

This is a great spot for a long again around 24.55 to see if we continue to the upside, however, if this breaks, shorting down to the 24.32 retest of support should work nicely

Bi-directional Trade IdeaIt seems like we are likely to form a pennant here.

Give it some time before it breaks out / down.

Keep an eye on volume for confirmation.

Meanwhile if you are not patient enough you can try to catch the local tops & bottoms in the pennant, but only in the early stage. Once it gets squeezed further it just becomes unprofitable.

Other annotations on the chart.

Cheerz : ]