USD JPY - FUNDAMENTAL ANALYSISUSD/JPY has reversed from a high near 141, largely on the back of shrinking expectations that the Fed would hike in June. That is now priced with a 25% probability rather than a 70% probability attached to it last month. We have noted that the current environment should continue to see interest in carry trade strategies – where the Japanese yen scores poorly. However, USD/JPY looks overvalued relative to the terms of trade story – which is much better for the yen than a year ago.

In addition, there is still the risk that the Bank of Japan surprises on 16 June by further normalising its Yield Curve Control policy. That would be a yen positive. And thus it would not be a surprise to see speculator investors trying to re-position short USD/JPY above 140 – even if such a strategy has already proved painful this year.

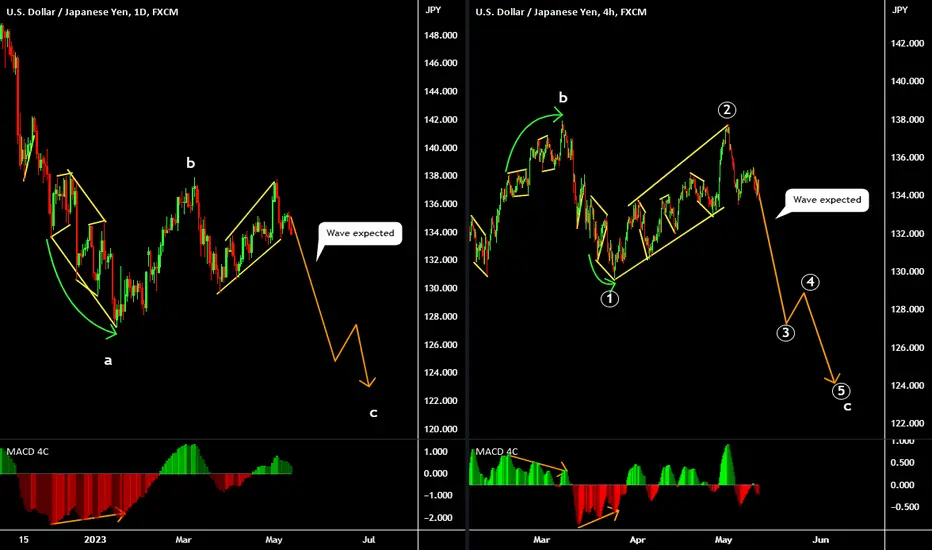

Dollar-yen

✨NEW: USDJPY ✨ SWING TRADE ✨SLO @ 144.05 ⏳

SSO @ 138.33 ⏳

TP1 @ 134.00 (shaving 25%)

TP2 @ 125.50 (shaving 25%)

TP3 @ 119.25 (shaving 25%)

TP4 @ 110.75 (shaving 25%)

TP5 @ 103.85 (shaving 25%)

BSO @ 101.66 ⏳

BLO @ 99.66 ⏳

ADDITIONAL INFO:

TP1 @ 134.00, before Pivot Low

TP2 @ 125.50, at Mid-Pivot

TP3 @ 119.25, at Major Support

TP4 @ 110.75, above Upper Demand

TP5 @ 103.85, above Lower Demand

BSO @ 101.66, after Price Action drops below

TECHNICAL ANALYSIS:

As of June 1, 2023, the USDJPY is trading around 139.80.

The RSI is overbought, which indicates that the market is due for a correction. The MACD is also starting to turn down, which could be another sign that the trend is about to change.

⚠️Be mindful that the moving averages are all sloping upwards, which is a bullish sign.

Overall, the technical analysis for the USDJPY is mixed. There are some bullish signs, however the bearish signs seem to be forging ahead. Traders should be cautious and wait for a clear downtrend to emerge before taking any short trades.

Here are some of the key levels to watch for:

* SUPPORT: 139.45

⚠️ For a more aggressive approach, you can place a Market Order to Sell once price opens and closes below Support

* RESISTANCE: 140.65

⚠️ For a more aggressive approach, you can place a Market Order to Buy once price opens and closes above Resistance

If the price breaks below the support level, it could signal a change in trend to the downside. If the price breaks above the resistance level, it could signal a continuation of the bullish trend.

Here are some of the factors that could affect the USDJPY in the near future:

* The US Federal Reserve's interest rate decision on June 15.

* The Japanese government's economic data releases.

Traders should keep an eye on these factors and adjust their positions accordingly.

USD JPY - FUNDAMENTAL ANALYSISThe US dollar (USD) has staged a comeback against the Pound Sterling (GBP) and Euro (EUR) over the past few weeks, but foreign exchange analysts at MUFG still consider that medium-term depreciation is the most likely outcome.

The bank considers that the US Dollar exchange rates are overvalued, especially against the Japanese Yen (JPY) and net capital flows are likely to be less supportive.

It also considers that the Euro-Zone and Chinese outlooks are more favourable, especially given that gas prices have declined sharply.

MUFG also expects the Fed will cut rates before the ECB while the Bank of Japan will tighten policy.

Monetary policy will inevitably be a key aspect. Although the immediate debate is still surrounding the potential for further interest rate hikes, MUFG expects the debate will switch to the potential for a Federal Reserve policy reversal as the US economy deteriorates.

According to the bank; “ The Fed will be cutting rates prior to the ECB. Inflation in Europe is stickier due to energy and food prices and the Fed will have much more scope to respond once economic conditions in the US weaken further from here. ”

After an extended period of quantitative easing, MUFG also expects that the ECB quantitative tightening programme through bond sales will put upward pressure on longer-term yields and support the Euro.

Global Growth Trends Still Favourable

MUFG notes that previous forecasts of an extended UK recession have been revised away and the Euro-Zone has also been resilient.

As far as China is concerned it adds; “ Recent data has disappointed, in particular on the manufacturing side of the economy, but pent-up domestic demand likely has further to run which will act as a source of global growth this year. ”

Although market sentiment has been more cautious, it expects overall growth dynamics will not favour the US dollar as Asia rebounds.

A related issue is the key area of energy prices.

The jump in energy costs last year was a key reason why agencies such as the IMF and central banks were so negative surrounding the European economic outlook last year.

Gas prices have, however, declined sharply with a slump from over 90% from the peak and close to 2-year lows.

Gas storage levels are also at very high levels in historic terms ang MUFG expects storage levels will hit 100% in the summer.

In this context, lower gas prices will improve the growth outlook and strengthen the trade outlook.

The Bank of Japan has resisted tightening monetary policy, but MUFG notes that the economy is strengthening and inflation has increased.

According to MUFG; “ we maintain that YCC has passed its sell-by-date and while it remains unclear whether price stability at 2% can be achieved, the BoJ will still move to widen the band or scrap it completely. ”

The bank expects that the yen will strengthen sharply if the Bank of Japan lets yields increase which will drag the dollar lower.

Negative Long-Term US Debt Dynamics

The immediate focus is on the US debt ceiling and political brinkmanship ahead of early June when the US Treasury will run out of cash.

These short-term dynamics are mixed for the US dollar with concerns over the economy, but potential defensive support if risk appetite deteriorates.

MUFG focusses on the underlying debt dynamics and the potentially unsustainable situation.

MUFG notes that the budget deficit in the first seven months of fiscal 2022/23 amounted to $928bn from $360bn the previous year.

On a longer-term view, in considers the debt dynamics will be potentially negative for the US currency.

De-Dollarization Hype

Although MUFG considers that the de-dollarization rhetoric is rather more hype than substance, there is still the risk that long-term confidence in the dollar will decline with scope for some further increase in Euro and yuan central bank reserve holdings.

MUFG also notes that there has been strong central bank gold buying and it expects this trend will continue.

The bank also sees a risk that the US use of financial sanctions will discourage official players to hold reserves in the dollar due to fears over asset freezes.

MUFG notes that there has been an extended period of Wall Street out-performance, but expects this trend will reverse and net capital flows will be less supportive for the US currency.

It adds; “ We see a renewed drop in US equities as investors position more assertively for US recession. ”

Japan’s Nikkei 225 index has posted a 32-year high and the German DAX index has hit a record high.

It also sees scope for a sustained rebound in emerging-market equities after an extended period of under-performance.

It adds; “ A reversal of the current period of deep EM undervaluation poses downside risks for the USD in the medium-term. ”

Long-Term Peak, Dollar Overvalued

MUFG notes that the dollar last year reached the highest level for over 20 years.

It also notes that at the October peak the currency index was 2 standard deviations stronger than the average over the past 40 years.

It adds; “ Similar extreme levels of USD overvaluation were last recorded in the early 2000’s and mid-1980’s and subsequently proved to be long-term bearish turning points for the USD. ”

The bank also considers that the dollar is substantially overvalued, especially against the yen, increasing the likelihood of mean reversion.

USD JPY - FUNDAMENTAL ANALYSISForeign exchange analysts at Goldman Sachs still expect that the US Dollar to lose ground over 2023 as a whole, but expect this will take longer than expected previously due to US and global developments.

It notes; “Our underlying view for FX markets this year is that we are likely to see only a “bumpy deceleration” for the Dollar, because slack in the US economy is still limited, and we are still “waiting for a challenger.”

The 3-month Dollar to Yen (USD/JPY) exchange rate has been revised higher to 140 from 132 previously while the 6-month forecast has been revised to 135 from 125.

The 12-month forecast remains at 125.0.

From a longer-term perspective, Goldman still expects that the dollar will lose ground, but it considers that the short-term perspective has changed slightly.

It adds; “we think the recent rally in the broad Dollar more appropriately reflects the fine balance facing currency markets at the moment.”

Goldman points out that the US economy has performed more strongly than expected after the Silicon Valley Bank collapse in March.

According to Goldman; “In the US, recent data on credit conditions have been a bit better than feared. And cost pressures have eased somewhat but remain a top priority, so that a number of Fed officials have said they still see some risk that rates may ultimately have to rise further.”

Another key element for exchange rates is that dollar selling necessitates the buying of another currency.

In this context, Goldman is less confident that there are attractive alternatives. The narrative earlier in the year was of a strong rebound in China and notable resilience in the Euro-Zone.

Both these elements have come into doubt over the next few weeks.

The Bank of Japan has also not engaged in any shift in monetary policy with the ceiling for the 10-year yield held at 0.5%.

The delay in tightening policy has undermined the yen in global markets.

Goldman adds; “Dollar depreciation usually coincides with strong activity in the rest of the world, not US underperformance. We think recent developments all support this view, and should also support some further Dollar strength over the near term.”

The 3,6 and 12-month Euro to Dollar (EUR/USD) exchange rate forecasts are unchanged at 1.05,1.05 and 1.10 respectively.

USD JPY - FUNDAMENTAL ANALYSISThe US dollar has hit a fresh year to date high overnight against the yen at 138.87 as it continues to extend its advance from the low of 133.75 recorded on 11th May. Over that period the yen has been the worst performing G10 currency alongside the Scandi currencies of the Swedish krona and Norwegian krone which have declined by over 2% against the US dollar. The recent move higher in USD/JPY has coincided with the ongoing adjustment higher in US rates. 2-year and 10-year US government bond yields have closed higher for seven consecutive days which is the longest run of higher closing prices since September of last year. It was also a period of yen weakness when USD/JPY was breaking above the 140.00-level for the first time since the middle of 1998. According to the latest CFTC report, leveraged funds have been paring back the size of their short yen positions this month although they still remain close to levels from back in autumn of last year when USD/JPY hit its current cycle high. The BoJ’s ongoing reluctance to tighten monetary policy further in the near-term combined with recent adjustment higher in US rates has triggered renewed upward momentum for USD/JPY. The move higher in US rates was encouraged yesterday by reassuring comments following a meeting between President Biden and House speaker McCarthy on the debt ceiling. After the talks, House speaker McCarthy stated that “the tone was better than any other time we have had discussions”. Both President Biden and House leader McCarthy acknowledged that the talks had been productive although they have not yet reached an agreement. President Biden stated that “we reiterated once again that default is off the table and the only way to move forward is in good faith toward a bipartisan agreement”. House leader McCarthy expects to speak with President Biden on a daily basis until a deal has been reached. The developments support market expectations that a compromise agreement will be reached to raise the debt ceiling before the so-called “X-date”. If those expectations are seriously challenged in the coming weeks then it could trigger a squeeze of short yen positions and a sharp move lower in USD/JPY. At the same time, the move higher in US rates was encouraged yesterday by comments from Fed officials. St Louis Fed President Bullard stated that he is “thinking two more moves this year” to put enough downward pressure on inflation. He is a wellknown hawk and a non-voter on the FOMC this year. The hawkish comments from St Louis Fed President Bullard were partially offset by relatively more cautious comments from Minneapolis Fed President Kashkari who stated “we may have to go higher from here, but we may not raise rates quite as aggressively and as quickly as we have over the course of the past year”. He also believes it’s a close call as to whether the Fed raises rates further in June or skips that meeting. We would place more weight on his comments as he is a voter on the FOMC this year. June rate hike expectations have since edged higher again with the US rate market pricing in around 5bps of hikes.

USD JPY - FUNDAMENTAL ANALYSISDerek Halpenny, Head of Research, Global Markets, EMEA & International Securities at MUFG, suggests that the recent trend seeing a weaker Japanese Yen (JPY) may not last, due to the changing dynamics that drove the currency weaker in 2022.

"We remain unconvinced that the trend in yen weakness can persist. The dynamics that drove the yen weaker in 2022 are changing and that will mean upside scope will be far less going forward," says Derek Halpenny.

He further emphasises the significance of Japan's shifting trade data influenced by falling energy prices.

"The turn in the energy markets that has seen the huge negative energy terms of trade shock start to reverse...we saw Japan’s trade deficit continue to shrink helped by falling energy prices," he adds.

Japan's Trade Data

Halpenny also details the notable decline in Japan's total imports, which fell 2.3% in April, the first drop since January 2021.

"A shrinkage in the trade deficit was further helped by a 2.6% increase in exports. Japan’s energy import bill is now falling sharply – the annual change was -17.7% in April which contributed to 5.0ppts of decline in overall imports," says Halpenny.

He also addresses the influence of US rate expectations on the yen, implying a potential reversal in the USD/JPY trend when this momentum fades.

"Of course this underlying change for the yen will play second fiddle to rate expectations in the US which is the current driver of the move higher in USD/JPY but will add potential impetus the other way when the US rates momentum fades, which it inevitably will do going forward," Halpenny adds.

USD JPY - FUNDAMENTAL ANALYSISThe FRB’s cycle of rate hikes could reach a turning point given global financial uncertainties and concerns about

stagflation in the US. The dollar/yen pair’s topside will probably grow heavier as US interest rates slide.

USD JPY - FUNDAMENTAL ANALYSISThe US Dollar to Yen (USD/JPY) exchange rate has rallied on Thursday, amid hopes surrounding the US debt ceiling talks, strong US job data, and upbeat US data releases.

Derek Halpenny, Head of Research, Global Markets, EMEA & International Securities at MUFG, suggests that the recent trend seeing a weaker Japanese Yen (JPY) may not last, due to the changing dynamics that drove the currency weaker in 2022.

"We remain unconvinced that the trend in yen weakness can persist. The dynamics that drove the yen weaker in 2022 are changing and that will mean upside scope will be far less going forward," says Derek Halpenny.

He further emphasises the significance of Japan's shifting trade data influenced by falling energy prices.

"The turn in the energy markets that has seen the huge negative energy terms of trade shock start to reverse...we saw Japan’s trade deficit continue to shrink helped by falling energy prices," he adds.

Japan's Trade Data

Halpenny also details the notable decline in Japan's total imports, which fell 2.3% in April, the first drop since January 2021.

"A shrinkage in the trade deficit was further helped by a 2.6% increase in exports. Japan’s energy import bill is now falling sharply – the annual change was -17.7% in April which contributed to 5.0ppts of decline in overall imports," says Halpenny.

He also addresses the influence of US rate expectations on the yen, implying a potential reversal in the USD/JPY trend when this momentum fades.

"Of course this underlying change for the yen will play second fiddle to rate expectations in the US which is the current driver of the move higher in USD/JPY but will add potential impetus the other way when the US rates momentum fades, which it inevitably will do going forward," Halpenny adds.

Joe G2H Trade@ Buying USDJPYTrade Idea: Buying USDJPY

Reasoning: Pullback into newly formed support on the daily.

Entry Level: 138.104

Take Profit Level: 139.58

Stop Loss: 137.50

Risk/Reward: 2.4/1

Disclaimer – Signal Centre. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis , like all indicators, strategies, columns, articles and other features accessible on/though this site is for informational purposes only and should not be construed as investment advice by you. Your use of the technical analysis , as would also your use of all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

USD JPY - FUNDAMENTAL ANALYSISYen Undervalued, Yuan to Lose Ground

Danske Bank continues to expect that the Bank of Japan will tighten monetary policy this year, although the timing remains very uncertain.

While a key argument against the Euro is that the currency is overvalued, it considers that the Japanese currency is substantially undervalued.

According to Danske; “Overall, USD/JPY seems fundamentally overvalued and combined with potential monetary policy tightening; we expect the cross to drop below 130 on a 6-12M horizon. If inflationary pressures in Japan continue to persist, it will increasingly build pressure on the ultra-dovish stance that the BoJ has.

Danske expects the Chinese yuan will lose ground due to broad dollar gains. A weaker Chinese currency would also act as a barrier to Euro gains.

USD JPY - FUNDAMENTAL ANALYSISBOJ governor Kazuo Ueda is a scholar, so if the BOJ does conduct a review, he will probably be forced to recognize the impossibility of the BOJ’s current monetary policy. With the phase of rate hikes also coming to an end in the US, the dollar/yen pair’s topside will gradually grow heavier from here on.

EURJPY Short Setup H1EUR/JPY is currently presenting a bullish setup, meaning that the price is rising towards 149 where a supply zone is located, providing a short setup as identified by the Forex48 strategy for entering a short trade. The objective here would be to wait for the price to reach this zone and then enter with a target of 148.

Let me know what you think.

Happy trading to everyone.

Forex48 Trading Academy

USD JPY - FUNDAMENTAL ANALYSISJapan: High expectations for Q1 GDP, with persistent inflation concerns

Japan’s preliminary GDP for Q1 is due on Wednesday and will provide the latest insight into the health of the economy. Bloomberg consensus expects an improvement to 0.8% Q/Q annualized from 0.1% in Q4 when the economy narrowly avoided a recession. While a broader reopening of the economy in the first quarter and the return of some Chinese tourists may have meant a further uptick in the services sector, exports and manufacturing likely remained weak on the back of weakness in global demand. If domestic consumption weakens substantially despite the government travel subsidies and high winter bonuses, it could continue to highlight the risk of a recession.

April CPI will also be released on Friday which will likely confirm that price pressures remain concerning. Tokyo CPI for April had come in above expectations despite the falling commodity prices and the base effect. Bloomberg consensus expects national CPI for April to come in at 3.5% for the headline from 3.2% previously while the core-core measure (ex-fresh food and energy) is expected to rise to 4.2% from 3.8% in March.

USD JPY - FUNDAMENTAL ANALYSISJapan: High expectations for Q1 GDP, with persistent inflation concerns

Japan’s preliminary GDP for Q1 is due on Wednesday and will provide the latest insight into the health of the economy. Bloomberg consensus expects an improvement to 0.8% Q/Q annualized from 0.1% in Q4 when the economy narrowly avoided a recession. While a broader reopening of the economy in the first quarter and the return of some Chinese tourists may have meant a further uptick in the services sector, exports and manufacturing likely remained weak on the back of weakness in global demand. If domestic consumption weakens substantially despite the government travel subsidies and high winter bonuses, it could continue to highlight the risk of a recession.

April CPI will also be released on Friday which will likely confirm that price pressures remain concerning. Tokyo CPI for April had come in above expectations despite the falling commodity prices and the base effect. Bloomberg consensus expects national CPI for April to come in at 3.5% for the headline from 3.2% previously while the core-core measure (ex-fresh food and energy) is expected to rise to 4.2% from 3.8% in March.

USD JPY - FUNDAMENTAL ANALYSISJapanese yen strength over time.

While the yen underperformed during the global monetary tightening phase, in our view, the currency has scope to outperform later this year. We now believe the BoJ will take advantage of a tactical opportunity to further tweak its policy settings in Q4-2023 to further normalize the government bond market. Such a policy move adds to our constructive medium-term outlook for the yen. Yen outperformance over time should also be supported by the end of central bank tightening and a transition toward easing, as well as a U.S. recession in the second half of 2023.

USD JPY - FUNDAMENTAL ANALYSISJapanese yen strength over time.

While the yen underperformed during the global monetary tightening phase, in our view, the currency has scope to outperform later this year. We now believe the BoJ will take advantage of a tactical opportunity to further tweak its policy settings in Q4-2023 to further normalize the government bond market. Such a policy move adds to our constructive medium-term outlook for the yen. Yen outperformance over time should also be supported by the end of central bank tightening and a transition toward easing, as well as a U.S. recession in the second half of 2023.

USD JPY - FUNDAMENTAL ANALYSISJapanese yen strength over time.

While the yen underperformed during the global monetary tightening phase, in our view, the currency has scope to outperform later this year. We now believe the BoJ will take advantage of a tactical opportunity to further tweak its policy settings in Q4-2023 to further normalize the government bond market. Such a policy move adds to our constructive medium-term outlook for the yen. Yen outperformance over time should also be supported by the end of central bank tightening and a transition toward easing, as well as a U.S. recession in the second half of 2023.

USD JPY - FUNDAMENTAL ANALYSISJapanese yen strength over time.

While the yen underperformed during the global monetary tightening phase, in our view, the currency has scope to outperform later this year. We now believe the BoJ will take advantage of a tactical opportunity to further tweak its policy settings in Q4-2023 to further normalize the government bond market. Such a policy move adds to our constructive medium-term outlook for the yen. Yen outperformance over time should also be supported by the end of central bank tightening and a transition toward easing, as well as a U.S. recession in the second half of 2023.

Looking to buy USDJPYOur trade relies on fundamental analysis, and technical analysis only serves as our entry point.

Currently, the US is undergoing a process of quantitative tightening. The upcoming FOMC meeting is expected to result in a 25 basis point rate increase.

A rate increase of 50 basis points or continued rate hikes would be seen as a hawkish signal.

Meanwhile, Japan is maintaining its monetary easing policy, and the new BOJ governor, Ueda, announced in a recent speech that they plan to slowly continue their yield curve control to support a healthy economy.

This has led us to take a long-term dovish stance on the JPY.

Shifting our focus to the technical analysis,

We are currently awaiting a retracement to the 61% Fibonacci level.

However, we should remain vigilant as there is a possibility that the price may reject the 134.78 level.

We are also waiting to retest the trend line and the demand zone.

USD JPY - FUNDAMENTAL DRIVERSThe dollar is expected to fall and the yen rise.

Risk aversion prevailed in March on credit concerns about US regional banks and a major European bank, with the dollar/yen pair trading with a heavy topside to drop below 130 yen. Excessive concerns about the US financial system then eased on news that some regional banks would be bought out, so the dollar was bought again. However, the pair’s rally was quite muted compared to its rally towards 135 yen after the release of the US February consumer price index (CPI) data. With President Biden also saying the banking crisis was still not over, it seems this rally was merely due to a slight withdrawal of ‘excessive concerns,’ with investors still worried that tougher banking regulations might act as a new risk-off factor. Furthermore, though FRB chair Jerome Powell has said he envisages one more rate hike this year, the markets are split evenly when it comes to pricing in another hike, so it seems there are concerns about the negative impact of tightening on the financial environment. The Bank of Japan (BOJ) will also be meeting to set policy for the first time under its new structure at the end of April. Most observers believe the BOJ will stick to the status quo for now, but it is also possible the BOJ might announce a policy shift. Investors are starting to focus on FRB rate hikes, so if a BOJ policy shift does seem more likely, market participants will then focus on a future shrinkage of Japanese/US interest-rate differentials. Based on the above, it seems the dollar/yen pair will be susceptible to more downward pressure in April.

However, the US also released some firm economic indicators in March. Inflationary pressures also remain high, as evinced by a comment by a FRB official that “inflation is still too high.” US interest rates rose and the dollar was bought at the start of March on hawkish comments by FRB chair Jerome Powell. Controlling inflation remains the FRB’s number one priority. With Mr. Powell also commenting that “the ultimate level of interest rates is likely to be higher than previously anticipated,” some observers believe it is too early to start talking about rate cuts. With concerns about the financial system smoldering away, market participants will be focusing on comments by FRB officials ahead of the May FOMC meeting as they try to gauge the direction of monetary policy.

USDJPYMy view anticipates a potential short on USD/JPY. I have identified a very strong supply zone where the price has attempted to break twice without success, creating spikes that I have highlighted with circles. An hour ago, the price created another supply within the strong resistance zone, and I will wait for a possible retracement to enter a short position.

Let me know what you think in the comments:

Have a nice trading day!

USD JPY - FUNDAMENTAL DRIVERSThe dollar is expected to fall and the yen rise in April.

Risk aversion prevailed in March on credit concerns about US regional banks and a major European bank, with the dollar/yen pair trading with a heavy topside to drop below 130 yen. Excessive concerns about the US financial system then eased on news that some regional banks would be bought out, so the dollar was bought again. However, the pair’s rally was quite muted compared to its rally towards 135 yen after the release of the US February consumer price index (CPI) data. With President Biden also saying the banking crisis was still not over, it seems this rally was merely due to a slight withdrawal of ‘excessive concerns,’ with investors still worried that tougher banking regulations might act as a new risk-off factor. Furthermore, though FRB chair Jerome Powell has said he envisages one more rate hike this year, the markets are split evenly when it comes to pricing in another hike, so it seems there are concerns about the negative impact of tightening on the financial environment. The Bank of Japan (BOJ) will also be meeting to set policy for the first time under its new structure at the end of April. Most observers believe the BOJ will stick to the status quo for now, but it is also possible the BOJ might announce a policy shift. The Japanese March CPI data is also set for release on April 21. If this points to stronger-than-expected inflationary pressures, a policy tweak/shift will become a more realistic possibility. Investors are starting to focus on FRB rate hikes, so if a BOJ policy shift does seem more likely, market participants will then focus on a future shrinkage of Japanese/US interest-rate differentials. Based on the above, it seems the dollar/yen pair will be susceptible to more downward pressure in April.

However, the US also released some firm economic indicators in March. Inflationary pressures also remain high, as evinced by a comment by a FRB official that “inflation is still too high.” US interest rates rose and the dollar was bought at the start of March on hawkish comments by FRB chair Jerome Powell. Controlling inflation remains the FRB’s number one priority. With Mr. Powell also commenting that “the ultimate level of interest rates is likely to be higher than previously anticipated,” some observers believe it is too early to start talking about rate cuts. With concerns about the financial system smoldering away, market participants will be focusing on comments by FRB officials ahead of the May FOMC meeting as they try to gauge the direction of monetary policy.

USD JPY - FUNDAMENTAL DRIVERSJapanese yen strength over time. While the yen underperformed during the global monetary tightening phase, in our view the currency will likely outperform as tightening cycles eventually come to an end and central banks turn to easing. Yen outperformance over time should also be supported by U.S. recession in H2-2023 as well as recent actions by the Fed, which have made U.S. dollar liquidity more readily available. And while the likelihood of a hawkish Bank of Japan (BoJ) monetary policy shift has perhaps diminished a little, if the global financial sector proves surprisingly resilient, the risk of a further policy adjustment from the BoJ could still reinforce the outlook for yen gains over the medium term as well.