Silver Holds Near $33.80 as Fed Rate Cut Bets Provide SupportSilver edged lower to approximately $33.80 during early Asian trading on Friday, losing momentum. However, the downside may remain limited, as softer U.S. consumer and producer inflation data could provide room for the Federal Reserve to consider an interest rate cut in June, offering some support for the metal.

Additionally, concerns over U.S. President Donald Trump's protectionist policies potentially pushing the world's largest economy into a recession could further support silver's appeal.

If silver breaks above $34.00, the next resistance levels are $34.85 and $35.00. On the downside, support is at $33.80, with further levels at $33.15 and $32.75 if selling pressure increases.

Dollar

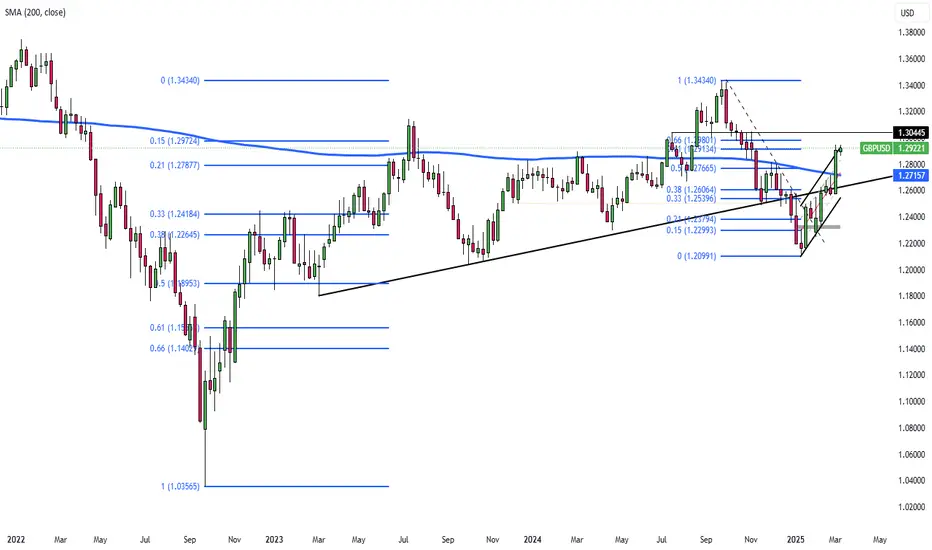

Sterling Struggles Amid Risk Aversion and US Tariff ThreatsGBP/USD extends its decline for the second consecutive session, hovering around 1.2940 during Friday's Asian trading hours. The currency pair faces difficulties as the Pound Sterling (GBP) weakens due to a negative risk sentiment, which has been further worsened by worries over global trade following US President Donald Trump's threat to impose a 200% tariff on European wines and champagne, creating market instability.

If GBP/USD breaks above 1.2980, the next resistance levels are 1.3050 and 1.3100. On the downside, support stands at 1.2860, with further levels at 1.2760 and 1.2660 if selling pressure increases.

Yen Slips Against USD as Tariff Concerns Increase the DollarThe yen fell below 148 per dollar on Friday, reversing gains as trade tensions increased the dollar. Trump reaffirmed plans for reciprocal tariffs starting April 2. Despite this drop, the yen remains near a five-month high, backed by expectations of BOJ rate hikes. Japanese firms agreed to wage increases for a third year, aiming to offset inflation and labor shortages. Higher wages may spur spending and inflation, giving the BOJ room for future hikes. While rates are expected to remain unchanged next week, policymakers may pursue hikes later this year.

Key resistance is at 149.20, with further levels at 152.00 and 154.90. Support stands at 147.00, followed by 145.80 and 143.00.

AUDUSD BUY NOW 120 PipsLooking at the monthly charts, it seems like we've hit a key level where the price has bounced back up nicely. This indicates a shift in the overall trend, making it look like there's potential for some upward movement. Since the DXY (which tracks the strength of the dollar) is weakening, we might be able to ride this wave up and take advantage of the positive momentum in the market. It’s all about following the trend and going with the flow!

Risk to reward is very lovely

Follow me for your support

Thank You

GBP/USD is leaning in favor of the dollar.GBP/USD is leaning in favor of the dollar.

Since 2008, we've seen five waves down, and now a correction is forming, potentially targeting the $0.98 - $1.036 range or even lower, given the bullish outlook for the DXY.

Right now, shifting into USD seems like the smartest move.

Confirmed Breakout!!! wait for the pullback on Gold!The price action I was looking for yesterday didnt happen till mid London session after i stopped looking. Now that we have confirmed bullish im looking for a pull back inside of a gap before taking any entry.

The Dollar Index has reversed upward.Hey everyone!

Looks like a solid entry for a DXY long and a good time to start ditching EUR and Gold (yes, I do think gold is heading down).

On the daily chart, we can see that we've completed five waves down and are now forming a reversal.

EUR/USD and GOLD/USD have already started reacting, Index Dollar (DXY) hitting the 61.8% Fibonacci retracement level.

Now the climb begins, with the first target around 125 for the Dollar Index.

The potential peak?

144, though we’ll likely see corrections along the way.

Buckle up—volatile times ahead... 🧐🧐🧐

DXY in 1 H timeframeDXY Analysis on RTM Style

Here’s an analysis of the **U.S. Dollar Index (DXY) on the 1H timeframe** based on the **RTM (Read The Market) style** and your drawn arrows:

Previous Trend & Break of Structure (BoS)**

- The market has been in a strong downtrend, forming **Lower Lows (LL) and Lower Highs (LH)**.

- After breaking the **105.485 level (0.5 Fibonacci retracement)**, the bearish momentum continued down to the **103.5 support zone**.

Liquidity Zones & Potential Reversal**

- The price is currently consolidating around **103.5**, indicating a possible reaction from buyers.

- A **Higher High (HH)** is marked, suggesting a potential shift in market structure.

Possible Scenario Based on the Arrows**

- A short-term **accumulation phase** is expected between **103.5 - 104**.

- If the price breaks above **103.998**, bullish momentum may drive it toward the **105.5 - 106.7 zone (Fibonacci 0.5 & 0.786 retracement levels)**.

- If this resistance is broken, the final target could be **107.27**, a strong resistance level.

- The market is at a **key support level** and may form a bullish structure.

- Confirmation of a **Higher High** and a break above **103.998** could trigger an upward move.

- **Re-Accumulation** is expected before a strong bullish continuation.

- **Bearish Alternative**: If the **103.5 support** fails, the price may drop further to **102.1**.

This analysis is suitable for publishing, but I recommend adding an alternative scenario in case the support fails, giving a more well-rounded outlook.

Weakness of Dollar Could Be Over SoonTextbook Head & Shoulders pattern is underway on DXY chart.

Price is close to the target of 101.91.

Watch how price will react there as weakness of dollar could be over soon

Fed Expectations Increase Silver PricesSilver surged to nearly $33 as the US Dollar fell sharply, with the DXY dropping to 103.35, its lowest in four months. Concerns over Trump’s tariff policies and their impact on the US economy fueled the dollar’s decline, supporting demand for silver.

Investors now await US CPI data for February, which could influence Fed rate expectations. A slower inflation rate may increase the likelihood of a May rate cut, with odds rising to 51% from 37% in a day, further supporting Silver’s appeal as a non-yielding asset.

If silver breaks above $32.75, the next resistance levels are $33.15 and $33.80. On the downside, support is at $31.00, with further levels at $30.20 and $29.75 if selling pressure increases.

Recession Fears Support Gold's StabilityGold held steady above $2,910 per ounce, maintaining a 1% gain. Investor sentiment shifted after Trump reversed his plan to double tariffs on Canadian steel and aluminum, just hours after the announcement. Ontario Premier Doug Ford also paused a 25% surcharge on US electricity exports.

Trade uncertainties and US recession fears continued to support gold, though geopolitical tensions eased as the US restored military aid to Ukraine following a 30-day ceasefire agreement with Russia. Markets now focus on upcoming US CPI data for clues on the Fed’s rate outlook.

Key resistance stands at $2,923, with further levels at $2,955 and $3,000. Support is at $2,860, followed by $2,830 and $2,790.

Eurozone Spending Plans Boost EuroThe euro surged past $1.09, its highest in four months, gaining 5% since early March. This rally was driven by Eurozone plans to expand deficit spending, stimulating growth prospects. Germany pushed for a €500 billion infrastructure fund, while France and Italy supported joint EU funding for economic and military initiatives.

The ECB signaled a shift toward a less restrictive policy after last week’s rate cut, suggesting the easing cycle may be nearing its end. Meanwhile, US economic concerns pressured the dollar, further lifting the euro.

Key resistance is at 1.0950, followed by 1.1000 and 1.1050. Support stands at 1.0800, with further levels at 1.0730 and 1.0650.

Fundamental Market Analysis for March 12, 2025 USDJPYThe Japanese yen (JPY) continued to lose ground against its US counterpart for the second day in a row and moved away from the highest level since October, reached the previous day. Fears that US President Donald Trump may impose new tariffs against Japan have proved to be key factors undermining the safe-haven yen. Nevertheless, a significant Yen depreciation still seems unlikely amid hawkish expectations from the Bank of Japan (BoJ).

Data released today showed that Japan's annual wholesale inflation, the Producer Price Index (PPI), rose by 4.0% in February, indicating that inflationary pressures are intensifying. In addition, hopes that the sharp wage increases seen last year will continue into this year support the market's growing confidence that the Bank of Japan will raise interest rates further. This, should serve as a tailwind for the low-yielding yen and help limit losses.

In addition, lingering concerns over the possible economic consequences of Trump's trade policies and a global trade war should support the JPY. The US Dollar (USD), on the other hand, is near multi-month lows amid expectations that a tariff-induced slowdown in the US economy will force the Federal Reserve (Fed) to cut borrowing costs several times this year. This should help limit the USD/JPY pair's rise.

Trade recommendation: SELL 148.35, SL 148.95, TP 147.35

We shall Continue with Bullish activity on GOLD?Looking for a bullish play as I seen the Dollar broke its weekly level. Looking for it to continue but need to see a pullback for entry first. We must wait for the killzones for sure.

EurUsd ShortEUR/USD Short Idea

The EUR/USD pair is approaching the 1.09700--1.09940--1.10204 resistance level, which aligns with a significant supply zone and a potential area for bearish reversal.

Key Analysis:

Resistance Zone:

The 1.09700--1.09940--1.10204 levels marks a critical resistance where selling pressure has previously emerged.

Technical Indicators:

RSI is approaching overbought conditions, indicating limited upside potential.

Bearish divergence may form if momentum weakens near this level.

Fundamental Context:

A stronger USD due to hawkish Fed sentiment or economic data could pressure EUR/USD downward.

Eurozone economic uncertainties may add to bearish bias.

Entry: Short positions around 1.09700--1.09940--1.10204

This setup offers a favorable risk-reward opportunity in a high-probability reversal zone.

Trade Uncertainty and Fed Stance Keep Silver Prices ElevatedSilver held at $32.50 per ounce after a 4.4% weekly gain, as trade tensions and U.S. inflation data kept investors cautious. Uncertainty grew after Trump warned of new tariffs on Canadian dairy and lumber, following a U.S. delay on 25% tariffs for Canadian and Mexican goods. Canada upheld retaliatory measures, while China’s tariffs on U.S. agriculture took effect. Concerns deepened after Trump avoided recession and inflation questions in a Fox News interview. Fed Chair Powell signaled no rush for rate cuts despite rising economic risks.

If silver breaks above $32.75, the next resistance levels are $33.15 and $33.80. On the downside, support is at $31.00, with further levels at $30.20 and $29.75 if selling pressure increases.

UK Budget Forecasts and GDP Data Set to Shape Pound’s Next MoveThe pound hovered around $1.29, staying near a four-month high as dollar weakness persisted amid U.S. economic concerns and tariff risks. Sterling remained supported by expectations that UK interest rates will stay high, with traders adjusting BoE rate cut forecasts to 52 bps for 2025. Investors now await January GDP data for economic insights, while the UK’s budget watchdog will release updated economic and borrowing forecasts on March 26, potentially influencing market sentiment.

If GBP/USD breaks above 1.2920, the next resistance levels are 1.2980 and 1.3050. On the downside, support stands at 1.2860, with further levels at 1.2760 and 1.2660 if selling pressure increases.

USDCHF BUY NOW!!Nice wyckoff distribution, we can see price now heading higher, structure indicate buying pressure is coming in the market!!!

Nice risk to reward!!! see you later

Waiting for GOLD to Act right!Looking for a bullish play but waiting for price to get the shakes out. It is stuck inside of rotational value on a much larger scale. Need to see it break outside of that Value.

Gold looks ready for a sell off toward 2860Currently, the price of gold is at the Point of Control (POC) level, which suggests that we may see some weakness in the market. Based on my analysis, I expect a pullback towards the 2860 level. This is supported by a Wyckoff distribution pattern that indicates sellers are gaining strength, especially since we've observed a lower high around the 2906 level.

Stay tuned for more updates!

SHORT ON GBPUSDGBPUSD has reached a key supply area and has given a change of character from up to down on the hour timeframe.

There is plenty imbalance/fvgs to the downside that I expect price to go and fill.

The Dollar Index is currently shifting to up from down, this should aid in this pair falling.

I will be selling GBPUSD to the next demand level for 300 pips.

Omnichart presents - NIFTY/(USDINR) long term trend Nifty's performance when compared to US dollar (vs its base currency i.e. Indian Rupee) broke above a long term since 2007 resistance through Dec 2020. As you can see it broke above the blue line in Dec 2020 and has been outperforming the dollar - to -rupee. What this means is that investing US dollars to buy Nifty started becoming more profitable in Dec 2020 vs just keeping the wealth in US Dollars (not converting to INR). This is in a long term uptrend - what this means is that investing US dollars in NIFTY long term is a profitable strategy.

DXY will be fine (95)The dollar index expects to fall into the 95 area. Regardless of who wins tomorrow, the dollar will fall until 2025. The new government's realization of how sad everything is now will delay the process of a sound market. Vote!