Visualize $TSLA CALL pricing skew due to the upcoming earningsLet’s take a look at our new tradingview options screener indicator to see what we observe, as the options chain data has recently been updated.

When we look at the screener, we can immediately see that NASDAQ:TSLA has an exceptional Implied Volatility Rank value of over 100, which is extremely high. This is clearly due to the upcoming earnings report on July 23rd.

As we proceed, we notice that Tesla's Implied Volatility Index is also high, over 70. This means that not only the relative but also the absolute implied volatility of Tesla is high. Because the IVX value is above 30, Tesla’s IV Rank is displayed with a distinguishable black background. This favors credit strategies such as iron condors, broken wing butterflies, strangles, or simple short options.

Next, let’s examine how this IV index value has changed over the past five days. We can see it has increased by more than 6%, indicating an upward trend as we approach the earnings report.

In the next cell, we see a significant vertical price skew. Specifically, at 39 days to expiration, call options are 84% more expensive than put options at the same distance. This indicates that market participants are pricing in a significant upward movement in the options chain.

The call skew is so pronounced that at 39 days to expiration, the 16 delta call value exits the expected range. This signifies a substantial delta skew twist, which I will show you visually.

We see a horizontal IV index skew between the third and fourth weeks in the options chain. This means the front weekly IVX is lower than the IVX for the following week, which may favor calendar or diagonal strategies. Hovering over this with the mouse reveals it’s around the third and fourth week.

In the last cell, we observe that there’s a horizontal IVX skew not just in weekly expirations but also between the second and third monthly expirations.

Now, let’s see how these values appear visually on Tesla’s chart using our Options Overlay Indicator. On the right panel, the previously mentioned values are displayed in more detail when you hover over them with the mouse. The really exciting part is setting the 16 delta curve and seeing the extent of the upward shift in options pricing. This significant skew is also visible at closer delta values.

When we enable the expected move and standard deviation curves, it immediately becomes clear what this severe vertical pricing skew in favor of call options means. Practically, market participants are significantly pricing in upward movement right after the earnings report.

Hovering over the colored labels associated with the expirations displays all data precisely, showing the number of days until expiration and the high implied volatility index value for that expiration. Additionally, a green curve indicating overpricing due to extra interest is displayed. Weekly expiration horizontal IVX skew values appear in purple, and those affected by monthly skew are shown in turquoise blue.

The 'Lite' version of our indicators is available for free to everyone, where you can also view Tesla as demonstrated. Pro indicators are available more than 150 US market symbols like SPY, S&P500, Nvidia, bonds, etfs and many others.

Trade options like a pro with TanukiTrade Option Indicators for TradingView.

Thank you for your attention.

Earnings

AUDUSD 15M ProjectionHello Billionaires!!

It looks like a good time to buy AUDUSD because the trend is going up. Just remember to keep an eye on the market in case things change.

Also, make sure to protect yourself by setting stop-loss orders below the support zone to avoid big losses if the market suddenly goes down. Its a Fibo Golden Technique FX:AUDUSD

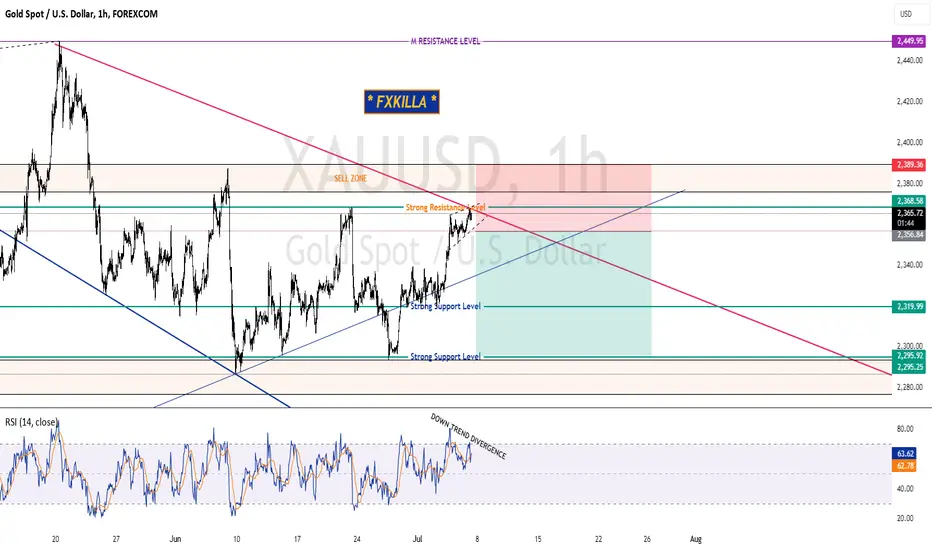

XAUUSD GOLD HIGH PROBABLITY SELL SETUP SOON 🚨XAUUSD HIGH PROBABILITY SELL SETUP SOON🚨

* Here We Can See Clearly The Next Potential Move For XAUUSD In Coming Hours.

* Gold Is Inside Rising Wedge Pattern.

* Down Trend Divergence On The RSI Indicator.

* NFP Is Due In Today.

* Keep Your Eyes Close On your Trading Positions.

* Happy PIP Hunting Traders.

* FXKILLA *

Planning for Next Earnings Season: DFSNYSE:DFS has a platform trend since the highs and lows are very consistent, suggesting controlled buying over time. It had a compression pattern before the pop out of the box white candle and a small gap up candle as the first attempt to break out to the upside. The stock may drop back into the platform range but if it holds, it's a good indication that earnings have improved. This is an example of a good pattern to watch for a pre-earnings run setup with potential to swing trade to earnings. Discover reports July 17th.

Talaat Mostafa Group Stock, only higher.

For those interested in the Egyptian Stock Exchange market, here's a technical analysis of Talaat Mostafa Group's stock. I recommend placing two buy limit orders and two sell limit orders for quick profits. In the long run, the stock is expected to reach higher levels. The fundamentals also support an upward move due to the inauguration of the new Southeast project next Sunday.

IndiaMART InterMESH Limited: A Fortune-Friendly Investment OpporI am excited to share my analysis of IndiaMART InterMESH Limited's (BSE: 542726, NSE: INDIAMART). The company's business model, financial performance, and future prospects make it an attractive investment opportunity.

Business Model:

IndiaMART InterMESH Limited is a leading e-commerce company in India, operating a business-to-business (B2B) e-commerce platform that connects buyers and suppliers. The company's platform enables businesses to source products and services from a vast network of suppliers, thereby reducing costs and increasing efficiency.

Financial Performance:

The company's financial performance for FY 2023-24 is impressive, with a revenue growth of 15.6% year-on-year (YoY) and a net profit growth of 21.4% YoY. The company's revenue from operations has increased from ₹1,434.4 crore in FY 2022-23 to ₹1,655.6 crore in FY 2023-24, driven by the growth in its B2B e-commerce platform.

Ratios to Consider:

Return on Equity (ROE): 23.4% (FY 2023-24)

Return on Assets (ROA): 14.5% (FY 2023-24)

Price-to-Earnings (P/E) Ratio: 35.6 (FY 2023-24)

Dividend Yield: 1.2% (FY 2023-24)

These ratios indicate that IndiaMART InterMESH Limited is a profitable company with a strong financial position. The ROE and ROA ratios suggest that the company is generating significant returns from its equity and assets, respectively. The PEG ratio indicates that the company's stock is trading at a premium, reflecting its growth potential. The dividend yield is relatively low, indicating that the company is retaining its earnings to invest in future growth.

Technical Analysis: Support, Resistance, and Predicting Prices

Technical analysis is a method used by many traders to analyze price charts and identify potential trading opportunities. It involves studying historical price movements, trading volume, and various technical indicators to make predictions about future price movements.

Support and Resistance Lines

Support and resistance lines are two of the most basic and widely used technical indicators. A support line is a horizontal line drawn at a highly moved mid price level where the price has bounced back up from several times in the past. This suggests that there may be buying pressure at this level, as investors see it as an attractive price to buy the asset.

A resistance line is a horizontal line drawn at a highly moved mid price level where the price has been rejected several times in the past. This suggests that there may be selling pressure at this level, as investors see it as a good price to sell the asset.

Linear Regression

Linear regression is a statistical technique that can be used to fit a straight line to a set of data points. In technical analysis, linear regression can be used to identify the trend of a price chart and to predict future prices. The slope of the regression line indicates the direction of the trend. A positive slope suggests an uptrend, while a negative slope suggests a downtrend.

Using Support, Resistance, and Linear Regression Together

Traders can use support, resistance, and linear regression together to develop a trading strategy. For example, a trader might look for opportunities to buy an asset when the price is near a support line and the linear regression line is sloping upwards. Conversely, a trader might look for opportunities to sell an asset when the price is near a resistance line and the linear regression line is sloping downwards.

Other Criteria:

Management Team: The company has a strong management team with a proven track record of driving growth and profitability.

Industry Trends: The B2B e-commerce industry in India is growing rapidly, driven by the increasing adoption of digital technologies and the need for businesses to optimize their supply chain operations.

Competitive Advantage: IndiaMART InterMESH Limited has a strong competitive advantage due to its large network of suppliers, robust technology platform, and extensive market reach.

Valuation: The company's stock is trading at a reasonable valuation, considering its growth potential and financial performance.

Conclusion: IndiaMART InterMESH Limited is a fortune-friendly investment opportunity that offers a unique combination of growth, profitability, and dividend yield. The company's strong financial performance, robust business model, and competitive advantage make it an attractive investment opportunity for long-term investors. I recommend that investors consider IndiaMART InterMESH Limited for their portfolio, especially those looking for exposure to the growing B2B e-commerce industry in India.

ASX:OFX – A Rare Gem with Perfect Piotroski Score and Breakout PFundamentals :

OFX Group, listed on the ASX under the ticker OFX, presents a compelling investment opportunity this week. The company boasts a perfect Piotroski F-Score of 9, an exceptionally rare achievement that underscores its financial strength and operational efficiency. Currently trading at its fair value, OFX has turned profitable over the last 12 months and is poised for continued profitability this year. ASX:OFX ASX:OFX

Technicals :

From a technical standpoint, OFX has achieved a significant 52-week breakout, further enhancing its investment appeal. The stock has formed a rounding bottom pattern, a classic technical signal indicating the potential for a strong upward movement. Analysts project a potential upside of 30%, making this a promising candidate for growth.

A potential Setup:

• Entry: Current Market Price

• Stop Loss: $2.00

• Potential Upside: $2.90F

$AEO Tilted Cup and HandleI am seeing a not so perfect cup and handle for $AEO. Rationale that is a bullish stock is because fundamentals says so as their EPS diluted growth rate is more than 100%. Let's observe.

Ka-ching!

Dixon Technologies (India) LtdKeep it on your radar. A correction on way after a huge rally

RSI & MACD are in over brought zone possible we could see some selling pressure as PE IS 188

Stock is trading at 40.7 times its book value

Note*- Based on personal opinions/observations. Please do your own research/analysis before making any trading/investing decisions.

I am not a sebi registered investment advisor

Found a HIDDEN BULLISH DIVERGANCE: Here is a hidden bullish divergence that is still in process. Show to complete by today at 5 PM PT.

MY custom RSI has not completed its lower low yet and will by today at 5 PM PT. This means the bullish reversal from a LL will start making its way up.

Then hopefully the BULL gets released.

J symbol for the month of JUNE and numerics for the day of the month. Days are separated by each tick of 5 days.

This is a thorough detailed idea that shows in my opinion to come next with very little to say.

AMSC Computer medium cap beats earnings LONGAMSC on the daily chart has went 3X in 7-8 months on the strength of earnings beats and

the tailwinds of the AI supertrend. I see this as an excellent swing long trade to hold into

the next earnings in 3-4 months. AMSC is currently at its ATH and going higher means no

overhead resistance.

Blum Project Analysis!!!Today, I want to introduce you to another Tap-To-Earn project and see if it is worth your time.

In the previous articles, I explained Notcoin and the Hamster Kombat project. If you have time, take a look at these articles.

The name of this project is Blum .

Please stay with me.

-----------------------------------------------------------------------

What is Blum?

The Blum Token is a cryptocurrency associated with the Blum Crypto Project on Telegram . While specific details about the creators and core team might be limited, the project focuses on community engagement, utility, and promoting blockchain adoption. The token serves various purposes within the project’s ecosystem, from facilitating transactions to enabling governance and rewarding community participation

-----------------------------------------------------------------------

Now, let's check the Blum project with the help of SWOT ( Strengths-Weaknesses-Opportunities-Threats ).

What is the SWOT !?

SWOT (Strengths-Weaknesses-Opportunities-Threats) analysis is a framework used to evaluate a company's competitive position and to develop strategic planning. SWOT analysis assesses internal and external factors, as well as current and future potential.

🔸 Strengths : The game's style makes it difficult for the bot to jam every token_The active Telegram community currently has 11 million followers Blum selected by Binance labs team as featured airdrop

🔸 Weaknesses : No whitepaper _ Poor website _ Boring game _ The total number of tokens is not clear - the distribution method may not be fair _ the development team is unclear_The goal of the project is very general_ Low number of followers compared to other competitors on X platform _ Currently, you can become a member by invitation only_ It only has roadmap until the end of 2024_ The game environment is very simple.

🔸 Opportunities : Hard Forks to improve the Blum project_ Willingness of big investors to invest _ Improving the website and white paper_ Improve the game environment

🔸 Threats : High number of miners _ Emergence of Whales _Unspecified fee_ Hackers _ Competitors_Laws and regulations of countries

Can you add other parameters to the options above or not!?

-----------------------------------------------------------------------

Conclusion : Due to the fact that there are more Tap-to-Earn games these days, we should be a little careful in choosing the game, because no matter what you like, you will eventually have an income for the time you spend.

According to the description above, if you want to enter the BLUM project, you should only consider it a hobby and not spend a lot of time on it because it has many ambiguities and weaknesses.

Please do not forget the ✅' like '✅ button 🙏😊 & Share it with your friends; thanks, and Trade safe.

Iron Condor Nike. for 28 June'24Relatively safe bet (no loss on upside) to profit from stable price before earnings on 27 June

Profit ratio is 26.8%.

expires in 14 days

Buy Put 83

Sell Put 89

Sell Call 103

Buy Call 104

On Cloud Just Got Even More Interesting - I'm Watching CloselyI have been watching On Cloud and love their shoes. I wear them all the time now. In-fact, I bought some shares a while ago simply because I enjoyed wearing them so much. The chart above highlights some other levels I am watching if this trade can keep up:

1. The company's resurgence above its IPO price indicates a renewed investor interest, suggesting a positive sentiment towards its growth prospects.

2. Moreover, its expanding presence in the US markets signifies a broader consumer base and potential for increased revenue streams. This widening adoption could be indicative of a strong market position and strategic initiatives driving market penetration.

3. One of the standout factors contributing to On Cloud's appeal is its transition into a premium brand. Establishing oneself as a premium brand in a competitive market is no easy feat, highlighting the company's ability to deliver superior products and capture consumer loyalty.

This shift not only enhances brand value but also opens up opportunities for higher margins and sustained growth over time.

However, despite these positive indicators, there are key technical aspects that investors should monitor closely including the following:

1. The need to surpass a recent prior high, maintain controlled volume levels, and ensure the upward slope of moving average ribbons are all critical factors that could validate On Cloud's bullish trajectory.

2. Keeping an eye on these metrics will be essential for investors to gauge the sustainability of On Cloud's upward momentum.

3. Additionally, with established giants like Nike, Under Armour, and possibly Adidas in the mix, On Cloud's ability to carve out a distinct market niche will be a key factor in its long-term success and investment attractiveness. This is a competitive space.

I look forward to updating this chart 1+ year from now.

This is a LONG TERM trade.

Mind the gap! What next for Broadcom?Broadcom (AVGO) has been a major beneficiary of the AI boom, with its stock soaring 53% since the beginning of 2024 and more than doubling year-to-date. While not reaching the astronomical heights of NVIDIA (NVDA), Broadcom's performance remains remarkable.

The company's Q2 revenue report was a resounding success, showing a 43% year-over-year increase, while EBITDA grew 31% year-over-year. This strong performance prompted Broadcom to announce a 10:1 stock split on July 15th, a move that will make the stock more accessible to smaller retail investors.

The sustainability of this growth in the rapidly evolving AI landscape remains a key question for any AI-related company. However, Broadcom's forward P/E ratio of 35 appears relatively modest compared to its AI peers like NVIDIA (50), CrowdStrike (95), and AMD (46). This suggests that Broadcom may still have room for further valuation expansion.

Following the impressive earnings report, the stock surged 12% on June 13th and continued to trade higher in after-/pre-market activity. The technical picture is also positive, with the price comfortably above its short, mid, and long-term moving averages, indicating strong momentum. The recent surge in volume, reflected in the Volume Oscillator, further underscores the heightened interest in the stock.

While the Relative Strength Index (RSI) is currently in overbought territory at 79.23, this is not unusual following a major earnings announcement. Importantly, the RSI's moving average has been trending upwards since early May, suggesting that the bullish momentum behind AVGO may not be exhausted yet.

Furthermore, the overall market sentiment towards AI remains positive, which could continue to support Broadcom's growth trajectory. Yet it remains important to monitor Broadcom's competitive position in the Semiconductor Solutions & Infrastructure Software market, as the landscape is constantly evolving.

Risk Management: Despite the positive outlook, investors should be mindful of potential risks, such as a slowdown in AI adoption or increased competition, and employ appropriate risk management strategies.

BB set up for a move higher pre-earnings LONGBB on the 15 minute chart has earnings in three weeks. Price has been meandering sideways

for two weeks after some significant volatility in mid-May. I believe it is now due for a change

of phase/cycle as the earnings approach. I will place a long trade here targeting initially 3.10

just below a significant level to the left being the consolidations before and after the

volatility of mid-May. These is the likely level where traders will again make trades in BB.

The upcoming earnings should add some extra volatility into the price action which could

translate into profit.

NVDA earnings stats NVDA earnings stats based on the last 10 earnings days close to following day close.

11/17/21

293 - 317

+ 24 = + 8%

2/16/22

265 - 245

- 20 = - 9%

5/25/22

170 - 179

+ 9 = + 5%

8/24/22

172 - 179

+ 7 = + 4%

11/16/22

159 - 157

- 2 = - 1%

2/22/23

208 - 237

+ 29 = + 14%

5/24/23

305 - 380

+ 75 = + 25%

8/23/23

471 - 472

+ 1 = na %

11/21/23

499 - 487

- 12 = - 2%

2/21/24

675 - 785

+ 110 = + 16%

5/22/24 ?

10 earnings

average = + 6%

high = + 25%

low = - 9%

5/24/24 expiry options data:

Put Volume Total 144,889

Call Volume Total 221,403

Put/Call Volume Ratio 0.65

Put Open Interest Total 145,386

Call Open Interest Total 180,269

Put/Call Open Interest Ratio 0.81

Highest OI Call strike = 950

Highest OI Put strike = 920

IV implied move = +/- 9%

Quality never fails the publicLooking at the financials of the Woolworths here in this South Africa the brand is staple to high middle income class groups, year on year the company's EPS has been steadily improving after Covid. Just waiting for price to fall to a suitable price before the earnings reports are out in September. Looking at price, I am also waiting for clear Elliot Wave count to complete (near the R5100 - R4900 per share) and clear price candle confirmation.

Did You See What GameStop Just Accomplished?I must say, and as I wrote the other week ( see here ), the winners of the GameStop resurgence was GameStop itself. They now have $4 BILLION in cash on their balance sheet. That's right – a strong community can do wonders for a brand, its backing, and the company itself. Between Roaring Kitty, Ryan Cohen, and everyone on Reddit, they just created a viable business with an entirely new fundamental outlook.

Let me explain:

- They eliminated all of their debt, thus zero debt!

- They now have about $4 billion in cash.

- Market cap is nearing $10 billion.

- They do about $3.2 billion per year in revenue.

- They have 3x PS ratio, but many startups for for 5x or even 10x. But keep in mind that a majority of that is in cash. If we back out the cash from the market cap, the PS ratio is more like 1.5.

If you think they are on the verge of rebuilding and recreating their story, they have the revenue and balance sheet to do it.

Well worth watching…

By the way, I still can’t believe some 25%+ of the float is still short and public about it in available data.

I currently do not have a position, but as someone who appreciates fundamentals, a sound business, it surely has me watching it more closely than I have in prior years. The road will be long and difficult, and they have to execute flawlessly, but if they can, the vision is to become a gaming giant that'll be a value add to the gaming world.

EURGBP BUY SIGNAL EURGBP

I neither trade the news nor any SMC or chart patterns, etc. I trade solely and exclusively based on algorithmic structure. According to the algorithm, a long swing trade is warranted here. I have mentioned the entry level and TP (Take Profit) and SL (Stop Loss) below.

BUY

ENTRY = 0.84345

STOPLOSS = 0.84042

TARGIT 1 = 0.84991

TARGET 2 = 0.85400

TARGET 3 = 0.86016

Cigna Has Pulled BackCigna hit new record highs in March. Now, after a pullback, some traders may see opportunities in the health insurer.

The first pattern on today’s chart is the March low around $330. CI has held that level for more than a week, which may suggest support is in place.

Second, the current stabilization is occurring at the 100-day simple moving average. That may reflect a bullish trend over the longer term.

MACD is also starting to turn up. That may reflect increasing bullishness over the short term.

Finally, CI jumped after its last three quarterly reports, which each beat estimates. (It failed to hold after the most recent.) That could suggest investors are positive on its fundamentals.

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options and futures. See our Overview for more.

Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options or futures); therefore, you should not invest or risk money that you cannot afford to lose. Online trading is not suitable for all investors. View the document titled Characteristics and Risks of Standardized Options at www.TradeStation.com . Before trading any asset class, customers must read the relevant risk disclosure statements on www.TradeStation.com . System access and trade placement and execution may be delayed or fail due to market volatility and volume, quote delays, system and software errors, Internet traffic, outages and other factors.

Securities and futures trading is offered to self-directed customers by TradeStation Securities, Inc., a broker-dealer registered with the Securities and Exchange Commission and a futures commission merchant licensed with the Commodity Futures Trading Commission). TradeStation Securities is a member of the Financial Industry Regulatory Authority, the National Futures Association, and a number of exchanges.

TradeStation Securities, Inc. and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., both operating, and providing products and services, under the TradeStation brand and trademark. When applying for, or purchasing, accounts, subscriptions, products and services, it is important that you know which company you will be dealing with. Visit www.TradeStation.com for further important information explaining what this means.

Iron Condor - Dollar Tree. in 5 daysThis is a short term and risky Iron Condor for 7th June, going over earnings on 5th June, but with high premiums.

Iron Condor =

Buy Put 105

Sell Put 117

Sell Call 126

Buy Call 137

Strangle DLTRThis Condor ending 7th June, reached its target (just) with 100% profit and allowing to keep the full premium.

Iron Condor =

Buy Put 105

Sell Put 117

Sell Call 126

Buy Call 137