F Bearish Bias Again SHORTFORD ( F) on a weekly chart is in a falling wedge pattern. Fundamentally, it is challenged

by the EV vs hybrid dynamic, weak EV sales and the federal slowly ramping up MPG

requirements as potentially rising gasoline prices affecting consumer decisions away from the

gas consuming F-150 where the profits are the highest. Unless F can breakout of the falling

wedge, price could compress further in the wedge with a move down as far as 9.

At present F is testing the upper resistance descending trendline. The predictive algorithm

suggests it will be rejected and fall. I am entering a short trade here for a long term swing.

Earnings

GME potential buy setupReasons for bullish bias:

- Basic DOW theory

- Entry at HH breakout

- Bullish divergence

- Earnings post market today

Entry Level(Buy Stop): 16.16

Stop Loss Level: 12.81

Take Profit Level 1: 19.51

Take Profit Level 2: 22.86

Take Profit Level 3: Open

ETH WHALES VS RETAIL TRADERS (MUST SEE)ETH will fall to $2,816. Can be more. I will confirm very easy by looking at my METRICS RATE REPORT if more falling needs to happen. Order Blocks in tact measured by volume. ATR and PIPS agree with OB.

Fibonacci with correct settings on a 4hr TF.

Whales waited for Retail to make the first move, then the white trend crosses the whales yellow trend. Whales waited. Retail followed the Elliott waves to finally end it, then the whales manipulated.

Retail traders were controlling the game. Sadly it came to an end but will regain power.

Regression Trends with guides set to proper wicks along with 2 moving averages set to a correct measure to show trend will move up soon. Please see MA's from the beginning until the end. See how trend meets up with it.

LUV and Attendants love the Settlement LONGLUV on a 120 minute chart fell heavily on news of a looming strike by flight attendants 18 %

into a bear flag and support followed by a narrow range consolidation and a volatility

squeeze which broke on news of the settlement. I LUV Sowthwest and its travel mileage perks

and open seating. The NR7 indicator on watch was firing continuously. I am taking a long trade

here and now with adds at any dips found moving foward. It is hard to pass by an 18% sale.

This will be profitable and will subsidize travel on LUV.

GEHC topped out in an ascending channel SHORTGEHC is a new spinoff from General Electric. It has great success thus far with good earnings

reports and no dependency on debt and interest rates. It has been on an uptrend since

the November earnings. At present it is correcting. I will play this going short on shares while

hedging with a long term call options. I am in GE calls out into 2026. A long term call option

will yield a lower capital gains tax if closed beyond 12 months. Accordingly, I will go out 15-16

months as I typically want to close early to avoid the effects of time decay. I have high

expectations for GEHC. I do not think it will disappoint. When price reaches the running mean

anchored VWAP I will close the shares and run only the options.

DWAC shareholders & Trump approve merger then fake news LONGDWAC voted to merge with former presidental Trump social media enterprise. Then a CNBC staff

writer has an article:

Donald Trump told followers, “I LOVE TRUTH SOCIAL” — but shareholders in the newly merged company that will own that social media app might not feel so great.

The shell company Digital World Acquisition Corp. saw its share price plunge nearly 14% in the hours following shareholder approval Friday morning of a merger with the former president’s social media company to take it public.

The drop could reflect concerns about whether Trump Media & Technology Group, which is being merged with DWAC, can ultimately deliver significant revenue — and whether Trump will try to cash in on his share early because of his many legal problems.

My review of the chart is that DWAC underwent normal volatility going into a merger vote

without complications. The volatility is healthy and traders/investors are contesting fair

value. Share price is the same as it was two weeks ago. Astute traders may consider this a

discount move for a long position. Trump is a majority shareholder. Of course, a buy of shares

benefits both the buyer and Trump in stabilizing market cap which has slowly fallen. He

cannot sell shares to fund legal proceedings and their costs for six months. The writer

who I have not named, in my opinion only, does not know jack____. He is simply trying

to put up a headline gets some reading volume and capitalize on it. He should get

one of the stock analysts that consult on his network to give him an education and then

publish a retraction. The headline might be " This clueless writer but out fake news and

is now better informed. He apologizes to the subjects of that fake news"

Enough said.

IND penny IT with the earnings beat no more cash drain LONGIntellicheck validates identities for financial services, fintech companies, BNPL providers, e-commerce, retail commerce businesses, and law enforcement and government agencies across North America. Intellicheck can be used through a mobile device, a browser, or a retail point-of-sale scanner.

Volume, Volatility and Price Breakout on the 60-minute chart. Relative Volume was beyond 10X

The predictive algo has a continuation for Monday with a momentum fade over 4.25 topping at

4.5

I will take an intraday trade here potentially buying in the premarket. The target is the high

pivot forecasted by the algo about 30& upside. I will set a 7.5% stop loss and risk 0.01% of

capital in the trading account. I will take off 25% upon reaching 4.0 another 50% at 4.50 and

the remaining 25% with a 5% trailing stop loss to ride the momentum fade.

This is probably not shortable. The April monthly options pumped 6x to 30x on the earnings

report. They will have continuation on Monday 3/26 after that the put options will be in play.

The small call options chain is embedded in the chart. Earnings come again in May.

I will reenter this trade until after the current pop and drop is completed.

Then in late April to look I will reenter looking for a repeat of the present price action.

JPM a financial rockstar in stampede mode LONGJPM on the daily chart has plain and obvious consistent momentum albeit with corrections.

The markets are expected to thrive in this lection year and three rate cuts are projected

in the net 8 months. The best time to buy JPM was both March 22 and October 23. I suggest

the next best time is now before the forecasted rate cuts are factored into price ahead of

the cuts. I just got notified of unusual options volumes for a price of 220 for the July 24

expiration which is not a surprise and is the month of the presidential nominating conventions.

That is 10% above current price and suggests the options buyers are expecting price to be

in that money by July meaning maybe a target for price is 225-250. No matter, I am getting

mine now before the prices rise.

PHAT Phantom Pharma to moonshot from upgrade LONGPHAT is now targeting 25-34 according to analysts. I am not surprised. It has a pipeline and

is pending approval for a medication product to treat a stomach bacteria that causes chronic

infection and symptoms are often refractory to long and elaborate treatment protocols. The

product is already in Asia and doing well in YoY reports. PHAT has partnered with another

pharma company to make regulatory and marketing inroads in the European market. My

portfolio is already heavy with medtech and pharma but this one is far to promising

with the great upside it presents. I will hit this one hard trying to get the low of day in

pieces and build a position.

$DFH it's a dreamIt's a dream finding a dream home but this stock has pushed beyond ITS IPO price and is All Time High. Looking for an entry. Good fundamentals.

Ford Motors and Forever 21 Collaborate on Capsule CollectionFord Motors (NYSE: NYSE:F ) emerges as a beacon of resilience and innovation. While the automotive industry faces uncertainty, Ford's strategic initiatives and overlooked strengths position it for long-term success.

Ford's Collaboration with Forever 21 Marks Strategic Diversification Efforts

One such initiative is Ford's collaboration with fashion giant Forever 21, marking a bold foray into the world of apparel. The recent launch of a capsule collection featuring nostalgic iconography of classic Ford cars demonstrates the company's commitment to diversification and tapping into new markets. By leveraging its iconic brand image, Ford (NYSE: NYSE:F ) aims to connect with consumers beyond the realm of automobiles, tapping into the intersection of fashion and automotive culture.

Ford's Strengths in Commercial Business and Return on Invested Capital (ROIC)

Despite prevailing pessimism surrounding the automotive industry, Ford's commercial business, particularly Ford Pro, stands out as a lucrative segment. With impressive earnings and revenue growth, Ford Pro's success highlights the company's ability to capitalize on emerging opportunities in the commercial vehicle market. Moreover, the continued growth of Ford Pro's software subscriptions and mobile repair services further solidifies its position as a key driver of future profitability.

Ford's Strong Dividend Yield and Financial Discipline

Furthermore, Ford's commitment to improving return on invested capital (ROIC) signals a proactive approach to enhancing operational efficiency and financial performance. With targeted efforts to streamline operations and optimize costs, Ford aims to elevate its ROIC from 14% to 20% in the coming years, underscoring its commitment to creating long-term value for shareholders.

In addition to its operational prowess, Ford's strong dividend yield offers investors a compelling opportunity for income generation. With a forward yield of nearly 5% and a robust dividend distribution policy, Ford provides shareholders with attractive returns even amidst market volatility. The company's solid adjusted free cash flow further reinforces its ability to sustain dividend payments and deliver value to shareholders.

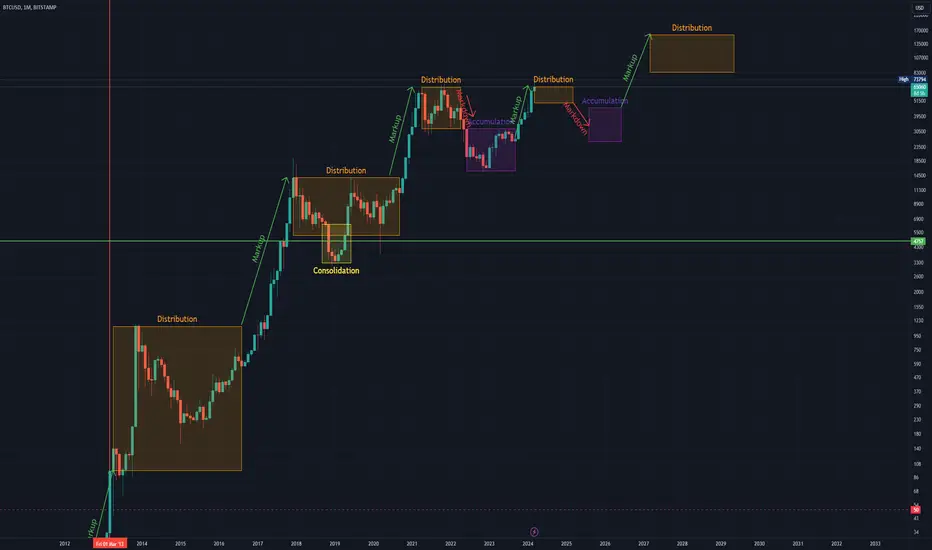

Possible (roughly estimated) Wyckoff cycle on BTCUSDThis is what I think may happen with BTCUSD based on Wyckoff cycles. I haven't checked the fibs or anything, so prices may be a bit inaccurate, but basically it works like this. Note that the prices here haven't been checked at all, and at the end of the day they don't really matter aside from the fact that market-movers know people look at them and use them to try to predict the market, which is nearly impossible unless you have enough money to set the market in your favor.

The people controlling the price (whales, institutions) can set walls wherever they want. They can cause the price to either oscillate within a range, to go up, or to go down. They are counting on human emotion (FOMO/ FUD) to drive the price one way or another.

Note also that, during cycles of Accumulation or Distribution, they are still accumulating during the lows of the Distribution cycles or the highs of the Accumulation cycles. So within these cycles are cycles of a lower magnitude.

The point is, the price is going to keep going up, because the asset has a fixed supply. They can prey on human emotion and lack of market education to predict what "most people" (the fish) will do. At the same time, they hold enough to setup walls and keep the price within certain ranges, allowing them to sell at the highs of that range and buy back in at the lows of the range.

This sounds stupid, because it literally is "sell high / buy low". In this case though, it isn't really all that stupid, because they can set the high and lows by creating buy and sell walls wherever they want to. Only a more powerful whale can really break their ranges, but that's pointless because it is in their best interest to work together and take the money from people trading on the daily, hourly and even sub-hourly oscillations. After all, they aren't counting on something going "to da moon" to pay their bills. They have enough money to survive a crash, or to capitalize on a "breakout" (which is when they stop selling and keeping the price within a range).

Most of these prices will look random, which they kind of are. But it's like putting 5 metronomes on a platform with a couple of cylinders beneath it - eventually the metronomes sync up. So their goal is less to "make money on this next day" than it is to "figure out a range that works in our best interest, and keep it going for as long as the little guys keep playing ball". Once smaller-time investors (people who have to go to work or are counting on good trades to pay their bills) dry up, they simply stop holding the price down and let people continue to buy. These are the people you should be following, because ultimately, they control the price.

That's the beautiful thing about Bitcoin. Its value is not predicated upon who has the most missiles, or who is developing some groundbreaking new technology. It is only predicated upon the assumption that it works, which it does (as a means of transferring value from one individual to another in a secure manner).

Altcoins are typically people trying to "print more bitcoin" by piggybacking off of the crypto movement in general and hoping enough fish bite the hooks. There are very, very few altcoins that have any intrinsic value which Bitcoin doesn't already have. I can't even think of one right now, so if you can please let me know.

TSHA a medtech penny stock pumps on news and earnings LONGTSHA is a gene technology medical company which reported on its clinical trials for Rett

Syndrome which is a neurobehavioral disorder separate from others like autism or

schizophrenia. This could be a breakthrough medication for those who suffer from Rett.

TSHA102 could be heralded as a miracle treatment ( not a cure). Price had trended up

in February and then down in March and is now situated at the mean anchored VWAP.

Relative volumes are 5-10X the running mean. I am taking a sizeable position here based

also on my background as well as the forecasts of medical technology stocks as being hot right

now especially small caps. Risk is definitely on. TSHA has been selling off parts of its pipeline

to fortify its core. This tells me leadership is realistic and has a survival plan which is a big plus

in the world of young and small medical technology companies. The earnings report from

yesterday showed a big earnings beat and a transition from cash burning to positive earnings.

Part of this is from selling off part of its future. Nonetheless, that future may be very bright

with what remains. I believe that TSHA will consolidate and gain consensus as to fair value

but then resume bullish continuation. This may be a buy and hold until the next earnings while

watching for clinical trial news that will give a hint as to the growth path.

DOWNTREND REJECTION-MOVING UP Regressions showing us guidance along with two VWAPS. Orange VWAP moving along uptrend regression. Downtrend rejected now moving along the uptrend regression.

ASO - Bad earnings can mean potential buy opportunitySee why here! Market is about to open so rushing through this one but hope this was helpful to keep an eye out for

Happy Trading :)

VINC a speculative biotech penny stock LONGVINC went from 1.5 to 3.0 in less than three hours with 12X relative volume in the afternoon

after a month of a slow climb from a news release that really did not amount to much. Insiders

are 25% of the shareholders and that may be the story here. This could be manipulation at its

finest. I have to wonder how many insiders bought how many shares and when the rug pull.

This is a high tight bull flag pattern which typically results in another leg higher of the same

magnitude. I suppose that is in clean trading without any manipulation.

If this takes off again it might be worth trying with a small position so long as the trader

can hit a button to close the full position when the sudden reversal occurs. I will trade

this long with a group of moving averages to make alerts for crossing lines and slopes

levelling out and see if it can go anywhere.

FIBONACCI with BREAKOUT--CYPHER Possible Target $78, 295Resistance with support level by Fibonacci. Retest breakout at $70,271. Cypher Harmonic three targets to as highest $78,295, possible target. ATR with percentage in price at 2059.7. Pips target is set to $ 73,732

I'm buying V calls!Visa has been in a sustained uptrend. Recently, it's established an even steeper uptrend! Couple that with the fact that it has a history of running UP into earnings (an average of 3.75%) and options volatility is at a near all-time low... sounds like the reasons are stacking up in favor of buying calls and riding them into earnings!

WM Waste Management ( Garbage Collector / Recycler ) LONGWM on a 180 minute chart shows a trend up since the October earnings. The January earnings

substantially beat the earnings from the October report and the uptrend accelerated. The chart

shows both VWAP band and volume profile breakouts persisting over 5 months. I have added to

my long-term position in WM with call options for January 2026 striking $200. These have

expensive premiums but I believe there is high value showing on the chart. I have taken partial

significant profits from the $190 calls for January 2025 and am rolling the remaining a year

forward. I will also buy a lot of shares now and hold them for about 4 weeks closing out most

of the position a few days before earnings and hold the remainder through the earnings.

Profits will be used to buy another call option.

CSCO LongEarning 11/15/2023 GAP Down,

12/11 Gap up above consolidation,

Long 49.3

Stop 45

Target 58

Risk management is much more important than a good entry point.

I am not a PRO trader.

In my trading plan, the Max Risk of each short term trade should be less than 1% of an account.

BuyToOpen 2024 Jun Call spread C52.5/60

Limit 1.54

SellToOpen 2024 Jun Put P42.5

Limit 0.87

Total cost 0.77, if price stays between 42.5 and 53.2, max loss 0.77x $100.

Stop below 39, max loss about $4.2 x100.

DLTR - earnings buy ideaToday DLTR gapping down around 7% and I see here a potential long opportunity.

I want the price to confirm 138 support and show bullish momentum.

First potential resist can be 50MA, but the price should break through easily.

If 50MA won't be a problem - first targets are: 143-146.

$CINF and $AFG long investmentUPDATE: The image I embedded in the TV chart for this idea was somehow rejected on the post. So I posted it on Imgur instead.

+++++++++++++++++++++++++++++++++++++++++++++

The chart I present for this idea doesn't look like a normal TradingView chart. The reason is that this is not a trade, based on chart technicals, but an investment, which I intend to hold for years. So, I don't care quite so much whether the stock wiggles upward or downward or sideways over the next two weeks. If you're looking for a trade, stop reading now. This idea is not for you.

If you're still reading, you're waiting for an explanation of the above chart. I I'll get to that, but first I want to step back a bit further.

I spent the last week looking through US-listed insurance companies for a candidate to invest for the long haul.

Why?

First: Real yields are at 2.5%, a level not seen since the GFC. This favors owning low-risk bond portfolios -- the kind insurance companies have. Both NYSE:AFG and NASDAQ:CINF have about $1.50 in investments for every dollar in market cap.

Second: As rates plateau, the AOCI losses that depress the tangible equity of insurance companies can gradually reverse, becoming a value creation tailwind. AOCI is 6% of NASDAQ:CINF 's tangible BV, and 14% of NYSE:AFG 's. This is very modest. Other insurance companies ($LNC...) ignored duration risk and had their portfolio bludgeoned half to death. From a short-term point of view, that makes NYSE:LNC perversely intriguing. If that stock survives its could get quite the bounce. But owning insurance stock shouldn't be a thrilling experience.

Third: Insurers are raking in big rate increases as they reprice catastrophe risks, inflation, and "social inflation". Florida homeowners know what I'm talking about.

And lastly: NASDAQ:CINF has a beta of 0.65, NYSE:AFG has a beta of 0.8. In other words these are "defensive" stocks, unlike banks, say. In uncertain times, insurers may suffer less than other industries. Though, the record is a bit uneven on that: During the dotcom crash they did well, in the GFC and pandemic, not so much.

So, to finally get to the chart: What even is the Tangible Value Creation Ratio? It's a modification of a key metric that NASDAQ:CINF uses to manage their business. Here's their definition :

“Value Creation Ratio” means the total of 1) rate of growth in book value per share plus 2) the ratio of dividends declared per share to beginning book value per share.

I prefer tangible book value to book value, so that's what I use. But that quibble aside, I really like this metric: It captures what I am truly interested in as an investor: Dividends and growth in the value of common shareholder's tangible equity. And the ratio also doesn't penalize companies for their choices with respect to dividend policy, capital structure, stock splits, and so on. It simply holds management responsible for the outcome to common shareholders. So, I calculate that ratio on a quarterly basis, aggregate it over multi-period spans and then annualize it. I think this ratio is particularly suited for a long-term analysis, since there's a certain variability in the short term, due to catastrophe losses and/or rate fluctiations. I actually did create the chart for a full 20-year span. If anyone wants to see it, let me know. But NASDAQ:CINF 's executive team came on in 2011, and it seems that the performance of the company has improved substantially since then.

Obviously, Berkshire Hathaway is the biggest insurer in the group. And based on this chart it looks very fairly priced for its excellent long-term performance. So why don't I want it? It's not that I don't trust Buffett & Munger, or their eventual replacements. I am more concerned about investors' reaction to these legends passing the baton. Whenever and however that might happen. To me, this just seems like a big event risk. As for NYSE:PGR , I'd love to own it, if it ever comes back from the valuation stratosphere. NYSE:RLI also seems like a very well-run insurer. But the slight edge in long-term performance doesn't seem to justify the huge bump in valuation.

A word about my data: I calculated these metrics programmatically, using financial statements downloaded from public sources. I did verify some of the data and calculations, but the testing is limited at this point. If anyone wants to compare notes, I am happy to.

As a last note: NASDAQ:CINF will report earnings after the close today. (Thursday, 2023-10-26). I bought some yesterday. But I doubt that the stock will jump in a meaningful way after earnings, even if they turn out to be brilliant. This thesis will likely take several years to play out one way or the other.

Zalando could go up with low risk tradeThis isn't any advice, this is just how I see situation.

Zalando can break downtrend and go up to 30 per share. So watch it and when price break trendline there is possibility to trade with low stop loss and high reward

Moreover Zalando just releases news that they will buy a lot of it's own shares from the market. Good news then :)