$CASA strongest Q4 with record wireless revenueIn the fourth quarter of 2020, Casa Systems' revenue rose 7% year over year to $120.5 million. Adjusted earnings increased from $0.15 to $0.27 per diluted share. Your average Wall Street analyst would have settled for earnings of roughly $0.11 per share on sales near $107.5 million.

The company booked 26 purchase orders for 4G and 5G wireless systems in the fourth quarter, making wireless products the largest revenue generator in this period at 42% of total sales. That's a significant shift from the year-ago quarter, where cable broadband equipment accounted for a leading 48% of Casa's total sales.

Wireless sales nearly doubled in fiscal year 2020, while fixed telco network sales posted even faster growth of 150%. The laggard in Casa's portfolio these days is the cable networking segment, which CEO Jerry Guo sees as a "steady and consistent" contributor rather than a growth driver.

www.fool.com

“We had one of our strongest quarters with record wireless revenue and a healthy backlog to support our top-line growth in 2021,”

finance.yahoo.com

Earningsanalysis

$JMP killer earnings $0.45 per shareJMP Group (NYSE:JMP) stock is soaring higher on Friday after releasing its earnings report for the fourth quarter of 2020 after-hours yesterday.

The most recent earnings report has JMP Group bringing in earnings $0.45 per share of on revenue of $53.62 million. Both of these are strong increases over the company’s EPS and revenue of 1 cent and $23.82 million from the same time last year.

Those positive results for the quarter are easily enough to explain why JPM stock is on the rise today. However, there’s more investors should note. It looks like the company is the target of investors looking to pump and dump it on the news. Talk on social media seems to back this idea up.

As a trader you have to understand the power of a catalyst. $JMP had killer earnings.

finance.yahoo.com

$VCRA provide outstanding Fourth Quarter 2020 Financial ResultsVocera Announces Fourth Quarter 2020 Financial Results

$VCRA Today reported total revenue of $56.6 million for the fourth quarter of 2020, an increase of 14% compared to last year.

GAAP net income of $0.1 million compared to a GAAP net loss of $(1.7) million last year

Non-GAAP net income of $9.7 million compared to $4.9 million last year

Adjusted EBITDA of $13.1 million compared to $6.9 million last year

Full-year bookings were $233.3 million, up 17% year-over-year

Deferred revenue and backlog combined of $173.9 million as of December 31, 2020, an increase of 28% over last year

Earnings per share were up 86.67% over the past year to $0.28, which beat the estimate of $0.20.

finance.yahoo.com

finance.yahoo.com

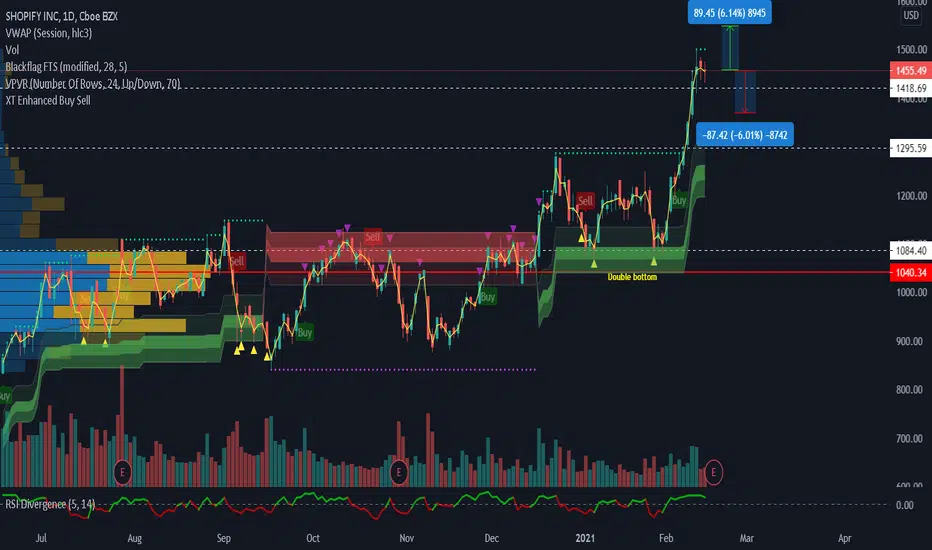

Evening star pattern, up 25% just in February prior to earningsSHOP has been a beast for along time! It has runup 25% just in February, so be careful for earnings on Feb 17th. The past 3 days show a bearish evening star pattern (not 100% perfect). I calculated the implied move to be 6% or $90 dollars. Options - 1068 in $1500 weekly calls, over 1600 in $1200 weekly puts. If you know how to play iron condor, I think that is best earnings trade o capture premium. They beat last earnings and raised expectations , its going to be hard to repeat, imo. Have a great long wknd!

Update on UAA Earnings play (Original was published on Feb 4)Here is an update on the most recent earnings play of Under Armour.

Look below at the original analysis, that was done about a week before earnings was released.

NLS post earnings movesAdjustments made from my previous chart. NLS could end up moving a little faster than I thought.

Just adding a faster move into the chart

PEIX vs Ethanol Futures (Chicago)Pacific Ethanol doing a reversal up with COVID spike and Ethanol Futures change. Awaiting this going to target $10-11 on short term with another positive earnings and 3rd plant running more to market need. Announcement also selling into more profitable libations market of low calorie seltzers and other consumer driven markets of STAY AT HOME during COVID-19.

MA (MASTERCARD INCORPORATED) LONG SET UP (EARNINGS)TITLE/(DATE)- Buy LIMIT MA

ASSET- MA

PLATFORM- MT4

ORDER TYPE- Market first entry / Buy limit second

Time Frame- 1D

ENTRY PRICE 1- $314.50 (Market)

ENTRY 2- $307.50 (Pending)

STOP LOSS- $300.50 (140 PIPs)

TAKE PROFIT 1- $328.50 (140 PIPS)

TAKE PROFIT 2- $342.50 (280PIPS)

TAKE PROFIT 3- $356.50 (420 PIPS)

TAKE PROFIT 4- $370.50 (560 PIPS)

STATUS: ACTIVE

Aug-27-20 Initiated Mizuho Buy $400

Jul-21-20 Resumed Daiwa Securities Neutral $314

Jul-14-20 Initiated Goldman Buy $364

$CTLT Touching the minimum line of the Drift ConePositive Under-reaction for CTLT and touches the minimum line of the Post earning Announcement drift.

$COUP Strong Momentum and pointing up $COUP Strong Momentum and pointing up but stock already above Post-earning announcement drift. Expect more upside with slight downside short term.

HSBCOverall opinion is to SELL ..

A lot of confluence technical factors :

200 ema price down , trendline in place and price has closed consistently below

37.87 ( Engulfing Bar) and formed a critical Swing High /rejected and closed below 38.48.

We are currently trading below the crucial 52day low 19.70 , so cautiously looking for a stable level of support to BUY, complimented by key fundamentals.

Also consecutive drops in revenue over the last few quarters.

XRPUSD Daily EarningsFollow,Watch And Enjoy Your Earnings...

I Wish You Lots Of Earnings My Traders Friends

CATCup and Handle pattern and trend line support with a resistance area of 140-141. The resistance was tested a few times and rejected but CAT is remaining well pithing the support. Earnings are coming up this week (Fri. Jul 31), however the overall market seems to be staying flat during this big earnings week, and this may suppress a possible ER run-up. Very mixed signals as the 20SMA crossed above the 200SMA, but showing a decline in the ATR, which may indicate a false move. Regardless of earnings, still look for any breaks of the support or resistance for a move up or down.

CARMAX ($KMX) 🏎️ | Save Your Marriage Using Only Carmax🚗 CarMax (KMX) slayed it last earnings season. While projections are grim this quarter due to the COVID slowdown, the longterm bull trend of CarMax and its general performance as a company ultimately has us looking for more upside.

Not only does CarMax have a strong presence in the in-person used car economy, but it also has a strong presence in online car sales (which one would think helped it sustain COVID better than others; we'll know when the numbers come out).

Another bullish thing CarMax has going for it is that some smaller used car dealers are having issues getting credit for customers, while bigger players like CarMax don't have this issue.

Given all that we are betting on bullish continuation after finding support, although there is a path for the bears here if this CarMax run turns out to be lemon.

Hit that 👍 button to show support for the content we produce every day and to help us grow 🐣

Support:

Our first notable support for KMX is the S1 bullish S/R flip, orderblock, and gap-fill cluster. There is a lot going on here, and all that confluence makes it a logical spot for the bulls to find support.

If the bulls can't hold S1, they will have to be cautious as the bears will have a path to victory in front of them. Both bulls and bears will be looking at the S2 cluster for direction. Does a test of S2 give us a dead cat up to previous support as resistance? Or, can the bulls take the S2 momentum and run with it? We won't know unless we get there, but the bulls should be hoping we never have to find out.

Resistance:

The first resistance for the bulls is the R1 orderblock and gap fill at the prior swing high. The logic here is simple, we are likely to find resistance at the previous top.

Speaking of previous tops, the R2 orderblock cluster at the All-Time High (ATH) is bound to see a reaction if and when we test it. Of course, testing this level is something the bulls are hoping for, and there isn't much for the bears to do if we do.

Summary:

CarMax has been bullish for about a decade, we aren't rushing to bet against this one, to say the least. Still, a bit more correction before the bulls continue their stampede isn't out of the question. Does S1 hold? Bulls better hope so, because things get a lot less bullish below S1.

Resources:

www.earningswhispers.com + www.caranddriver.com

FUELCELL ENERGY ($FCEL) 🔋 | Will Fuelcell Bulls Give em' Hell?⛽📱Fuelcell energy expectations going into earnings tomorrow are poor to mixed. However, green energy stocks have been performing rather well recently, and there is a solid chance FCEL will continue to benefit from that sector-wide momentum.

While we aren't ready to open a long position on this one ourselves, we will take a look at some potential levels of interest to watch depending on the market's reaction to earnings tomorrow. This outlook will be geared toward the bulls, because of the general strength in FCEL and the Green Energy sector.

Support.

The S1 bullish orderblock could act as support if the overall market stays bullish and earnings are good but FCEL pulls back for any reason. The S2 S/R flip is another logical level to look for support, perhaps if the market/sector pulls back with more intensity or there is an earnings upset. The S3 orderblock and S/R cluster is the last hope for bullish momentum, as it offers the chance for a higher low in the uptrend. S4 and S5 meanwhile should act as support if the uptrend is lost. Here S4 is of particular note as it is acted as a major price pivot point previously.

Resistance.

The R1 bearish orderblock represents the current price pivot point. Breaking this level is the bull's first order of business. The next level of interest is the R2 bearish S/R flip. If R1 is broken, R2 becomes the logical target.

Summary.

There are lots of important support levels for the bulls, and many chances to hold the uptrend. It is logical assuming the market and sector keep moving that even a fair earnings report will be enough to keep FCEL moving up. We don't have a clear long setup here, but these are the levels to watch.

Resources: www.earningswhispers.com + www.h2-view.com

💹 Drop a comment asking for an update, we do NEW setups every day 💹

Like & Follow to help the community grow! 🐣

WINGSTOP still looks extremely bullish going into earningsLook for the next candle on the MACD to be a lighter red color take the buy

seems like it might get created on Monday morning around 10am

If Wingstop sells off a bit and a new MACD lighter red candle gets created

buy in

more than likely its going to beat earnings and gonna keep skyrocketing

as long as people are inside and Q2 earnings for every other company is on the downside then youre good on buying WING for earnings and until Q3

when a sell off might happen IF people start going back their jobs and this whole corona virus is over by Q3 earnings around September

to make a long paragraph short, Buy WING until Q3 announcements or when states start opening up again

then when everything begins to start going back to normal, sell everything and expect a huge sell off

Update on Clorox this is just an update, after the market opening,.... check previous update for explanation

Clorox Company (CLX) Clorox Company will be releaseing earnings in a few hours.

As far as technicals, clorox has been in a decent uptrend

price has respected the lower trend line

It respected the fib level 38.2 fib

From a fundamental view standpoint, one would think with the coronavirus pandemic going on they should blow earnings out of the water....

DXYLooking to hold my WLL till about 3p, dollar looks strong. Knowing my luck they will crush earnings & I will totally regret that trade, but with $DXY breaking up seems risky.

MMM; Has Coronavirus helped 3M enough to keep them above water?!MMM; Has Coronavirus helped 3M enough to keep them above water?!

✨ We provide charts every day ✨

Like and Follow to help us grow family! 🎉

---

Let's Go! Time to see the much-anticipated earnings report from our savior 3M. We are hoping they are good and the chart may show this first hand already!

---

1. Fractal Trend showing an uptrend (Green background color) for MMM on the 1 hour chart. We are hoping this is not a false breakout like we saw previously.

2. We are currently in a quite parabolic move to the upside, thankfully we have a trailing stop riding behind this move to attempt to lockin as much profit as possible.

3. We are looking for a reaction at the R1 bearish orderblock where we hope to see Breakaway Scalper go neutral so we can get in on this tear!

4. If R1 can't hold, we will be looking at R2 and R3 as expected resistance going forward.

5. S1, S2, and S3 are all acceptable levels we are keeping an eye on but any lower and well... you guys know the rest.

Do a Sensata Selloff at $40 TargetFirst off, please don't take anything I say seriously or as financial advice. As always, this is on opinion basis. Now that we got that out of the way, let me get into my insights. Sensata recently had quite a disappointing earnings report. Revenue, operating income, and earnings per share all decreased at all fronts. This leads me to believe a sell target for $40 should be reasonable as a bearish potential may be quite imminent.

Daily Review: GOOG, AMD, and MSFTU.S. markets began the week on a strong note, led by small caps. The Russell 2000 Index finished the day up nearly 4% while the Nasdaq 100 lagged behind notching 0.5% at the end of the session.

This week represents a pivotal point of the rally as earnings season hits full swing with big cap tech reporting this week. Some names on deck later this week are TSLA, FB, AAPL and SHOP of which I will be reviewing on later posts this week. Today, we search for some market clues with GOOG, AMD and MSFT.

Tech Flexing

It's tough to bet against tech these days. Despite a global economic shutdown, large cap tech stocks have been resilient…on the charts. It will be interesting to see how they look on the balance sheet! We begin today with Alphabet, Inc (GOOG) on a weekly view.

GOOG has staged an impressive rally off the March 23 low making up nearly half its losses from its all-time high, $1532.11. At first glance, GOOG appeared to have broken through critical long term trendline support, but after review, GOOG has found support on a trendline drawn from the 2015 lows.

GOOG is heading into 2020 earnings after delivering strong 18% increase of revenue year over year. However, there are questions on whether the internet advertising giant will be able to impress this time around. The COVID-19 pandemic has definitely had an impact on whether businesses invest in online advertising, a large share of GOOG's revenue. Whether the magnitude of the impact shows up in Q1 earnings is yet to be seen.

Overall, GOOG bulls have enjoyed the past months worth of gains. However, there is reason to be cautious going into earnings as market strength and price begin to divert while overhead weekly resistance remains. Bias: Bearish .

Technically, Beautiful

Advanced Micro Devices, Inc. (AMD) has been the semiconductor darling for over a year ever since breaking out from a year long cup and handle pattern on October 2019. AMD is now up 100% since that breakout and COULD be poised for more upside. I emphasized could on purpose, because on the weekly chart AMD is knocking into resistance at $59.27. Any break higher may also be met with RSI divergence. AMD in my opinion is a tough buy at these levels as the risk reward is not favorable going into earnings.

On the plus side, AMD is a beneficiary of being partnered with Sony and Microsoft who are both scheduled to be releasing brand new gaming consoles later this year. How these schedules are impacted by COVID-19 is yet to be seen. Nevertheless, I would not be surprised if AMD pulled back a bit before heading higher. Overall, I like the stock long term from a technical and fundamental perspective, but on the short term I'll be waiting on a dip. Bias: Bearish .

Trillion Dollar Baby

Above is the daily view of Microsoft Corporation (MSFT). Trading 8% below its all-time high, MSFT is going into earnings in potentially in a make or break position for the broad market. MSFT makes up the largest percentage weight of the Nasdaq 100 (NDX) and today the index was lagging behind throughout the trading session. Either, MSFT and big tech have run out of gas or this is a healthy pause before marching back into all-time highs.

If MSFT does pull back, there is not much support. The rally has been a straight shot up from the lows. MSFT is a tough buy here especially after the discouraging performance of the NDX at the start of the week. Bias: Bearish .

Pivotal Week Ahead

With MSFT, AAPL, GOOG, AMZN and FB all reporting fiscal year Q1 2020 earnings this week, we should get a better grasp of how the market will trade in the months ahead. We must also assume that companies will be doing their best to lay down the framework to ease in the harsh reality of Q2 earnings, which undoubtedly will more accurately reflect the impact of the global economic shutdown. Tomorrow we have Tesla, Facebook and Apple. Have a great evening!