THE WEEK AHEAD: CRM, ANF, HPQ EARNINGS; XOP, NFLX, FCX, EEMEARNINGS WITH A RANK >70/IMPLIED >50:

CRM (81/52): Announces on Tuesday after market close. The pictured defined risk setup pays a greater than a one-third of the wing width 1.89 with break evens between the expected and one standard deevy.

ANF (68/86): Announces Thursday before market open. The Dec 21st 16 short straddle was paying 3.04 as of Friday close; the 25 delta 14/19 short strangle, 1.19.

HPQ (85/41): Announces Thursday after market close. The Dec 21st 22/23 skinny short strangle is paying 1.45, which makes for a near nominal trade at 25% max (.36 profit). Look for background implied to ramp up to 50 plus; otherwise, pass on a play.

EXCHANGE-TRADED FUNDS WITH A RANK >50/IMPLIED >35:

USO (100/66): I tend to use this more as of oil volatility indicator than anything (although you can naturally look at that more directly with OVX). Here, it's saying "Sell premium in petro underlyings," which for me means XOP, XLE, or OIH.

UNG (96/104): With UNG, I'm waiting for a seasonality short, but think putting on something in December is likely to be too early. January, however, is coming into range (currently 54 DTE).

XOP (85/45): A smidge early to go out to January, but the 29/36 is paying a 1.52 in that expiry; the 32/33 "skinny," 3.58.

SINGLE NAME WITH A RANK OF >70/IMPLIED >50/EARNINGS IN REAR VIEW:

NFLX (78/59): It's still got juice ... . The Jan 18th 25-delta 220/225/300/305 iron condor's paying 2.13 at the mid (but the platform's showing wide markets, so that may not be as hot at NY open).

FCX (71/55): The Jan 18th 11 short straddle is paying 1.73.

BROAD MARKET:

EEM (71/27)

QQQ (66/28)

IWM (62/24)

SPY (39/21)

EFA (13/20)

EEM

EEM: Daily buy signal$EEM has now flashed a buy signal, together with $SPY, and offers a great chance to go long with low risk. Emerging markets might benefit from the rally in oil which I foresee here.

Good luck,

Ivan Labrie.

EEM trendlineI'm not so sure that 37 is the target... I can see it going to 33 if the rest of the market continue showing weakness.

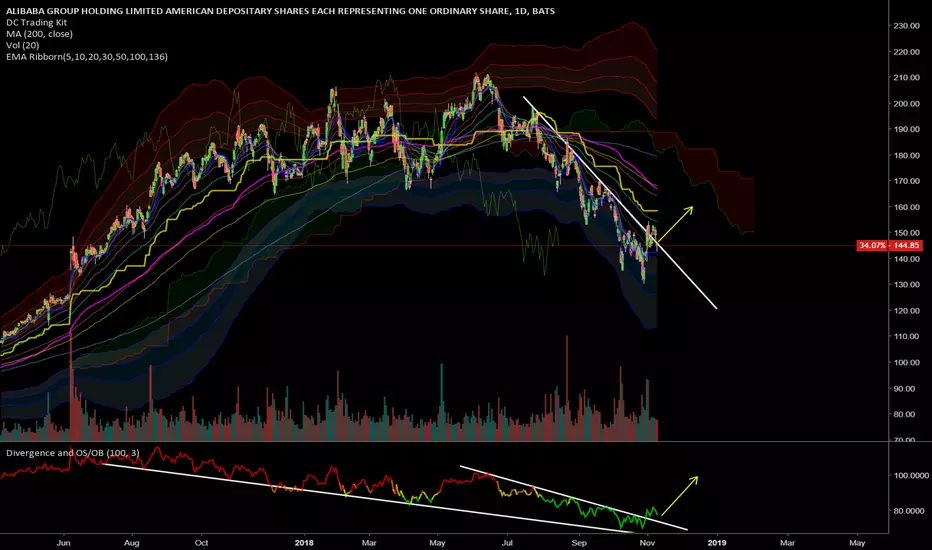

Long BABA to 155-160Best single day ever? yes.

And my indicator broke out the triangle and its retesting right now. Expect a move for 5-10% upside.

THE WEEK AHEAD: NVDA, AMAT EARNINGS; MJ, USO, SLV, EEMAs of Friday close, NVDA and AMAT appear to have the volatility metrics I'm looking for in earnings-related volatility contraction play (>70 rank/>50 implied).

NVDA (70/67) announces on Thursday after market close. The iron condor pictured here pays 1.73 credit with break evens wide of the expected move.

AMAT (68/48) announces on Thursday after market close, with the Dec 21st 31/37 short strangle paying 1.64 (50% take profit of .82) and the 34 short straddle paying 3.89 (25% take profit of .97).

On the exchange-traded front: USO (100/35), SLV (99/22), EEM (85/26), XOP (76/38), and OIH (75/36) round out the top symbols by rank, with USO, XOP, and OIH being no surprise given the beating oil has take over the past several weeks. Although I am mostly selling premium in XOP here, I could see also taking a bullish directional shot in OIH, which has broken through long-term horizontal support; XOP and XLE have yet to close in on the bottom of their long-term ranges. Alternatively, I could see doing a similar, bullish assumption play in one of the higher volatility petro underlyings that have earnings in the rear view mirror: OXY (75/30), COP (74/33), or BP (70/36), for example.

ASHR (74/33) is worth a passing mention here, but if I'm going to play China, it's going to be via the more liquid FXI (65/28).

MJ (--/64)* is also worth an honorable mention, with the more recognizable cannabis underlyings -- CRON, CGC, and TLRY -- all announcing earnings this week. The currently unfortunate thing about MJ is that it's not getting decent volume yet, so options liquidity isn't the best for those who'd rather not be on the single name roller coaster.

As far as the majors are concerned, some volatility came out of the broad market post-mid-term elections: SPY 30-day's now at 15.3%; QQQ at 24.6%; and IWM at 22.8%, so if I'm going to add broad market short premium here, it's going to be in the Q's and/or RUT/IWM.

Lastly: UNG. Last week marked a kind of WTF, weather forecast-related spike in natty, with UNG printing a new 52-week high. I was previously looking at 27.5 as an area of interest for short with 31-ish being the next stop, but thought November was too early in the natural gas seasonality cycle to be putting on a short play (usually, a downward put diagonal (See Post Below)* with the back month in April or later). Now that it's whipped through 31 in three seconds flat, I'm going to be patient here and see if it grinds higher throughout December, even though forecasts are generally calling for a "meh" winter temperature-wise.

* -- It doesn't currently have a 52-week rank, since it hasn't been around that long.

** -- Naturally, that setup's no longer good. I'll post a revised setup here shortly.

EEM. Emerging Index Fund. Possible map of WXYThis is how I see the map for EEM.

It contradicts with the news background as EM countries are under pressure now.

But this is how I see the wave count now.

The wave 5 to the upside is pending and we could see some relief for EM...temporarily.

Invalidation for this count is below the 38.32 when the wave 1 will be broken

Short HYG (High yield bond) How can you bullish equities?HYG clear clear cannot be more clear cup and handle. How can you be long equities now, super risky.

USDCNH (Chinese yuan has a lot to weaken)Triangle breakout and retest. The distance calculation will bring USDCNH to 7.5+, well above the 2015 high. Don't be surprised for global selloff and panic.

Emerging Markets Lead U.S. Inflation $EEMOn of the biggest calls leading into 2018 was to get ahead of the consensus and go bearish on emerging markets, particularly China, Turkey and Brazil.

Typically, in higher inflation environments, money flows head to emerging market assets; and it's particularly why EEM has had such a great run since China induced the largest stimulus known to man in 2016. When taking this into account, we'd expect continued money flows into emerging markets and that tends to keep interest rates elevated.

There is a strong relationship of these flows into EMs and Chinese monetary policy. When policy remains loose and accommodation, EMs get a boost and inflationary pulses spread. When they tighten, the opposite happens.

However, given the outlook on many EMs, I knew that U.S. inflation was likely playing out its late cycle movement. The problem now is China is trying to deleverage their banking system, which is roughly 400 percent to GDP, while loosen enough to keep the economy from a tail spin.

Here's the kicker: EEM peaks, on average, 6.5 months prior to U.S. inflation peaking which is how I top-ticked headline inflation at 2.9 percent.

EMs peaked in January, and headline inflation peaked in July. It's now down three consecutive months to 2.3% My call is it falls below two percent by the end of Q4-2018.

Just take a look at me calling the top in oil too:

twitter.com

twitter.com

twitter.com

EEM (The moment of truth)EEM the emerging market index ETF. there are two possible routes at this point. It is the moment of truth for this sector. Monthly breakout now retesting the break out TL. If it breaks below the trendline this month, it will go straight down, auch, brutal. However, I see this is low possibility, because I can see SPY bouncing (see my other post). So I would expect EEM take a break and go higher from here (just pray dollar dont go to the roof). After a bounce, we may well go straight down as we are in the 9th inning of the cycle.

EEM vs PA and AutosEEM vs PA and Autos

Palladium follows EMs and Autos.

Palladium has diverged due to tight supply?

Risky BUY: EEM (Emerging Markets) on touch of parallel channel Risky BUY EEM upon touch of lower boundary of parallel channel. Stop loss at today's minimum and target at last gap down. Attractive loss to gain ratio.

THE WEEK AHEAD: TWTR EARNINGS; USO, EEM, IWM, UNG, XOPTWTR announces earnings on Thursday before market open, and with a rank of 92 and a 30-day implied of 70, it presents ideal metrics for a earnings announcement volatility contraction play.

As of Friday close, the November 16th 25/34 short strangle is paying 1.57 (.79 profit at 50% max), with a net delta of .39 and a theta of 6.45, and break evens of 23.43/35.57 (wide of the expected move).

For those willing to bet a little more strongly on its not moving much more than the expected move: the November 16th 29 short straddle is paying 4.47 (1.12 profit at 25% max), with break evens of 24.26/33.74.

On the exchange-traded fund front: USO (73/30), EEM (67/25), and IWM (66/22) round out the top three underlyings when sorted by rank. UNG (42/41); EWZ (56/38); and XOP (53/32) are the top three when sorted by 30-day implied.

Possible Trades:

A USO December 21st 14.5/15 skinny short strangle* is paying 1.10 at the mid price with break evens of 13.40/16.10. Given the fact that this is basically a short straddle setup where I would shoot for 25% max, 1.10 isn't exactly compelling on a 1-contract basis (.28 at 25% max), but its small size makes it ideal for layering on setups over time in order to generate a worthwhile, multiple contract position that has some juice in it.

An EEM, December 21st 39/40 skinny short strangle is paying 2.68 at the mid price with break evens of 36.32/42.68. Go 25-delta short strangle -- the 37/42, and you bring in 1.24 in credit with 35.76/43.23 break evens. For defined risk, there's the double diagonal, (See Post Below). The December 21st 35/37/41/43 iron condor pays .70; going three-wide won't pay at least one-third unless you bring in the wings to a 35/38/41/44, which is paying 1.33.

An IWM December 21st, 16 delta, 139/165 short strangle is paying 2.43 with break evens of 136.57/167.43, which encompasses much of the last 52 week's range between 142.50 and 173.39. A delta neutral 141/145/162/165 iron condor pays 1.40; the slightly narrower 142/145/162/164 pays 1.05.

With UNG, I've had my eye on a short setup, (See Post Below), but don't want to pull the trigger too early. We're winding into winter, after all, which generally means increased natural gas usage and draw downs of current supplies. That being said, the notion behind the setup is that even if my timing is slightly off, a setup with a long-dated back month will eventually benefit as we emerge from winter, so I'm looking at putting the back month out in time and in an expiry when seasonality favors natty weakness. Unfortunately, the only available post-winter expiry is April, and I'd rather have an early to mid summer back month, so I'm fine with being patient here.

XOP has been double whammered with broad market weakness on top of oil weakness and is now at the bottom of the range between 40 and 45.50 it's been in since mid-April and a bit above the middle of its 52-week range between 31 and 45.50 with the low set in the early February sell-off. To me, that suggests "directionally neutral": the December 21st 40 short straddle pays 4.16 with break evens at 35.84 and 44.16; the 36/44 short strangle in the same expiry pays 1.40 with break evens at 34.60/45.40.

* -- The reason I would go with a skinny short strangle here instead of a short straddle is because price was 14.72 as of Friday close, which is in between the 14.5 and 15 strikes.

OPENING: EEM NOV/JAN 36/40/40/44 DOUBLE DIAGONAL... for a 1.38/contract credit.

Metrics:

Rank/Implied: 68/29

Max Profit on Setup: 1.38/contract

Max Loss/Buying Power Effect on Setup: 2.62/contract

Delta: -9.51

Theta: 2.06

Notes: I've done a few of these before. The way I look at them is that they offer the flexibility of a naked, while keeping your risk defined. An additional small benefit is that you don't have to leg in and out of the longs if you want to reuse them, saving a smidge in fees, assuming that you don't have to adjust the long strangle aspect too much to keep your risk where you want it. Will look to take profit on the short straddle at 25% and then reuse the long strangle ... .

THE WEEK AHEAD: AA, NFLX EARNINGS; USO, GDX, XLB, EEM, IWMWith broad market volatility ramping up over the past week here (see VIX, VXN, RVX), premium sellers can afford to be picky here, since the board is alight from here to Sunday with implied volatility ranks in the 70's for ... well ... a ton of stuff.

For earnings, my eye is on AA and NFLX with nearly ideal rank/implied metrics for volatility contraction plays.

NFLX (rank 64/implied 61), a perennial earnings-related volatility contraction fave, announces earnings on Tuesday after market close. Due to its size and its having a tendency to move bigly around earnings, I would go defined: the November 16th 285/290/385/390 is paying 1.87 with a buying power effect of 3.13; a ten-wide with the same short strikes, 3.53, with a buying power effect of 6.47.

AA, announcing on Wednesday after market close: 93/52. In my mind, small enough to go full on naked: the November 16th, 71% probability of profit 31/40 short strangle is paying 1.72 with a 50% max take profit of .86; the at-the-money skinny, quasi short-straddle -- the 35/36, 3.78, with a 25% take profit of .95.

Alternatively, it's been somewhat hammered here and is within 5% of 52-week lows which may make it suitable for a bullish assumption play: the 32/39/40 Jade Lizard is paying 1.00 on the nose with no upside risk and a low side break even of 31, a 13% discount over where the underlying is currently trading.

On the non-earnings front: the top five funds in terms of implied volatility rank are USO (81/30), GDX (71/32), XLB (68/27),* EEM (66/27),** and IWM (63/26); the top five ranked by 30-day implied: EWZ (58/44), UNG (36/41),*** XOP (52/36), OIH (56/36), and GDXJ (60/34).

* -- Possible bullish assumption directional; new 52-week low.

** -- Possible bullish assumption directional candidate: new 52-week low.

*** -- Possible bearish assumption directional candidate: new 52-week high.

Long term buy EEM on pullback to broken downward trend lineLong term buy EEM on pullback to broken downward trend line. Wave 3 imminent.

Shooting Star time eza, short emerging marketsanother short for EZA, told you lads back in March this was a layup

Emerging markets is extremely bearishBearish shooting star pattern right into channel resistance and just below major resistance line. You'd have to off your rocker to buy EEM exposure here, not with Fed day next week.

Going MACRO GLOBALI will be going officially global markets are changing its in the charts so be prepared!.