EUR CAD - FUNDAMENTAL DRIVERSEUR

FUNDAMENTAL OUTLOOK: WEAK BEARISH

BASELINE

In recent weeks, the persistently high inflation has seen the ECB take a more hawkish turn with the bank hiking rates by 50bsp at their July meeting. Additional pressure on inflation from gas supply shortages and Rhine River levels in Germany means the ECB will be forced to continue hiking rates. But the bank quelled any hawkish excitement at their July meeting by explaining they are frontloading hikes and not signalling a higher terminal rate with their bigger than expected July hike. The bank also failed to ease spread fragmentation concerns with their new Transmission Protection Instrument (TPI) as the eligibility criteria means countries like Italy and Spain that will need the support the most might have a tough time qualifying. Combined with political concerns and additional inflation pressures, further spread widening looks likely for now. Right now, even though policy and spreads are important, the main story and driver for the EUR is the economic outlook. Recent growth data continues to surprise to the downside at a rapid pace and further stoking recession fears for the Eurozone. Even though the bias remains lower, a lot of negatives have been priced in from a tactical point of view so worth keeping that in mind.

POSSIBLE BULLISH SURPRISES

De-escalation or cease fire in Ukraine would open up a lot of EUR upside. Also keep Italian politics in mind where successful attempts to avoid a snap election could ease spread widening & support the EUR. Stagflation risks remains high and recent data has invigorated recession fears, but with lots of bad news priced any materially better-than-expected growth data could spark some relief. Spread fragmentation remains a concern, especially with Italian politics and the ECB’s failed attempt to reassure markets. Any TPI comments that convinces markets it can solve fragmentation issues should be supportive for the EUR. Energy supply is also in focus, which means watching gas flows from Russia. If Russia increases gas flows to more regular levels it should ease some supply concerns and see EUR upside. Rhine river concerns are one to watch, any good news on water levels and resumption of normal transport could be a bullish catalyst for the EUR.

POSSIBLE BEARISH SURPRISES

Any escalation in the Ukraine war that risks including NATO would be big negative risks. Also keep Italian politics in mind, where any failed attempts to avoid a snap election should add further pressure on the EUR. Recent data has invigorated recession fears. Even though lots of bad news is priced, any materially worse-than-expected growth data could spark further downside some relief. Spread fragmentation remains in focus, and if the ECB fails to act when we see big jolts higher in the BTP/ Bund spread, or if any TPI comment further concern markets about its effectiveness, it could trigger bearish reactions in the EUR. Energy supply is also in focus, which means watching gas flows from Russia. If Russia decreases gas flows even further, it should increase supply concerns and see EUR downside. Rhine river concerns are one to watch, any bad news on water levels and continued breakdown in transportation could be a bearish catalyst for the EUR.

BIGGER PICTURE

The fundamental outlook remains bearish with recent leading indicators pointing to a much faster economic slowdown than markets had previously expected. The current bearish drivers (geopolitics, stagflation, spread fragmentation, energy supply concerns) far outweigh the positives from a hawkish ECB. Recession risks have opened up a narrative change for the EUR which have seen markets adjust forecasts to reflect higher recession probabilities that continues to weigh on the EUR. With lots of bad news priced in there is risks in chasing the EUR lower, but the fundamental outlook remains bleak.

CAD

FUNDAMENTAL OUTLOOK: NEUTRAL

BASELINE

The CAD has enjoyed far more upside in the past few weeks than we anticipated. We’ve been cautious on the currency given Canada’s dependency on the US (>70% of exports) where the clear signs of a faster than expected slowdown and possible recession should deteriorate the growth outlook for Canada. Apart from that, the risks to the Canadian housing market can negatively impact consumer spending as interest rates rise higher at aggressive speed. Potentially damaging the wealth effect created by the rapid rise in house prices since covid. However, despite the risks to the economy and the outlook, markets still price in a very favourable growth environment for Canada, also supported by a big push higher in terms of trade due to the rise in commodity prices. Furthermore, despite clear warning signals, the BoC has chosen to ignore the negatives and has stayed surprisingly hawkish, hiking 1.0% in July. The market’s reaction after the 1.0% was quite telling though, with the CAD pushing lower afterwards. This suggests that those players that were long could’ve used the hike as a spot to take profit, or it could be the market pricing in a possible pause for the BoC in the months ahead because hiking so aggressive now means reaching a level to pause their cycle much faster. Either way, we remain cautious on the CAD and favour short-term catalysts that provide us with shorting opportunities.

POSSIBLE BULLISH SURPRISES

As an oil exporter, oil prices are important for CAD. Catalysts that see further upside in Oil (deteriorating supply outlook, ease in demand fears) could trigger bullish CAD reactions. The correlation has been hit and miss in recent weeks though. As a risk sensitive currency, and catalyst that causes big bouts of risk on sentiment could trigger bullish reactions in the CAD. Even though lots of tightening has been priced for the BoC, any overly hawkish comments from the BoC or big upside surprises in econ data could trigger short-term upside, but with a 100bsp providing no upside, risks are titled to the downside.

POSSIBLE BEARISH SURPRISES

As an oil exporter, oil prices are important for CAD. Any catalyst that triggers meaningful downside in oil (deteriorating demand outlook, ease in supply shortage, less supply constraints) could be a negative catalyst for the CAD as well. As a risk sensitive currency, and catalyst that causes big bouts of risk off sentiment could trigger bearish reactions in the CAD. With a lot of tightening priced into STIRs, and a 100bsp hike providing no support for the CAD, we think risks are skewed lower, and any big downside surprises in econ data could offer decent shorting opportunities for the CAD.

BIGGER PICTURE

The bigger picture outlook for the CAD remains neutral for now. Given the clear risks to the growth outlook due to the slowdown in the US, as well as rising risks to the consumer and the housing market, and potential negative impact for commodities like oil, we remain cautious on the currency (even though it’s moved much higher than we anticipated from the start of the year). With a lot of good news priced in, our preferred way of trading the CAD is lower on clear short-term negative catalysts.

EUR-CAD

EURCAD SellSelling Directly in line with the short trend after a bullish push up on the US trading session open. We have entered in short around 1.21600 and will look to hold back to 1.31000 flat. good luck

EURCAD to the 0.618? 🦐EURCAD on the 4h chart is trading below a resistance level .

The price after the long bearish trend creates a DOUBLE BOTTOM and is now looking for a retracement ato the upside.

How can i approach this scenario?

I will wait for a potential break of the structure and in that case, i will look for a nice long order according to the Plncton's strategy rules.

--––

Follow the Shrimp 🦐

Keep in mind.

🟣 Purple structure -> Monthly structure.

🔴 Red structure -> Weekly structure.

🔵 Blue structure -> Daily structure.

🟡 Yellow structure -> 4h structure.

⚫️ Black structure -> <4h structure.

Here is the Plancton0618 technical analysis , please comment below if you have any question.

The ENTRY in the market will be taken only if the condition of the Plancton0618 strategy will trigger.

EURCADGreat confluence on 1.32 price which I shorted, EMA 200 + WK lv resistance + Fibonacci .618 + outer parallel channel retest = Short

already fell 100 pips

looking for lower price 1.305 area

EURCAD Trade with break-outsThe EURCAD pair has been trading within a long-term Channel Down since the September 20 2021 High. Right now it is consolidating after the July 13 Low, being below the 1D MA50 (blue trend-line) since June 28. Also below the 0.5 Fibonacci retracement level, this calls for extended selling to new Lower Lows as it happened two times before within the Channel Down.

However a break above the 1D MA100 (green trend-line), should initiate a short-term push to the 1D MA200 (orange trend-line), as it happened on February 03. Similarly, a candle close above the 1D MA200, should signal a complete long-term trend shift from bearish to bullish.

--------------------------------------------------------------------------------------------------------

Please like, subscribe and share your ideas and charts with the community!

--------------------------------------------------------------------------------------------------------

EURCAD: EUROPE heading towards recession and potential downsidesHey traders, in today's trading session we are monitoring EURCAD for a selling opportunity around 1.321 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.

EURCAD on a double bottom 🦐EURCAD on the 4h chart is trading below a resistance level .

The price after the long bearish trend creates a DOUBLE BOTTOM and is now looking for a retracement to the upside.

How can i approach this scenario?

I will wait for a potential break of the structure and in that case, i will look for a nice long order according to the Plncton's strategy rules.

--––

Follow the Shrimp 🦐

Keep in mind.

🟣 Purple structure -> Monthly structure.

🔴 Red structure -> Weekly structure.

🔵 Blue structure -> Daily structure.

🟡 Yellow structure -> 4h structure.

⚫️ Black structure -> <4h structure.

Here is the Plancton0618 technical analysis , please comment below if you have any question.

The ENTRY in the market will be taken only if the condition of the Plancton0618 strategy will trigger.

EURCAD SHORTHere is a possible Short set up for EurCad. We are in a weekly range between 1.32900 & 1.29700. Ill be looking to short EurCad from 1.32150 down to 1.29700, if 1.29700 is breached we can expect to see 1.21450. We have been in a downtrend for 700 days now and I believe this will continue for the rest of this month. Please contact me if you have any other ideas for this pair.

@thepipvault

EURCAD LONGEUR/CAD Triple bottom

1) Reversal indication on RSI - Convergence

2) Price at 1.299 acting as strong support.

3) I would like to see price come back down to that level, then price action (bullish engulfing candle) to display before entering for a long.

Small SL with good R:R Ratio

1 : 5.22 ~ Risk : Reward

EURCAD Potential downsidesHey traders, in the coming week we are monitoring EURCAD for a selling opportunity around 1.304 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.

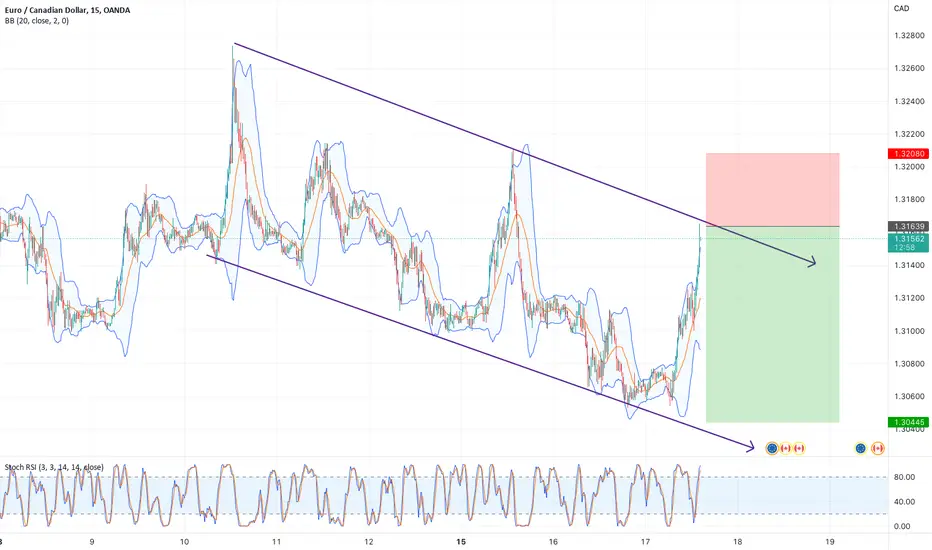

EURCAD Bearish Flag and BoC Hiking Rates.Hey traders, in today's trading session we are monitoring EURCAD for a selling opportunity around 1.306 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.

EURCAD ShortHey traders, in the coming week we are monitoring EURCAD for a selling opportunity around 1.322 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.

💡Don't miss the great buy opportunity in EURCADTrading suggestion:

". There is a possibility of temporary retracement to the suggested support line (1.3090).

. if so, traders can set orders based on Price Action and expect to reach short-term targets."

Technical analysis:

. EURCAD is in a range bound, and the beginning of an uptrend is expected.

. The price is below the 21-Day WEMA, which acts as a dynamic resistance.

. The RSI is at 57.

Take Profits:

TP1= @ 1.3221

TP2= @ 1.3307

TP3= @ 1.3398

TP4= @ 1.3526

TP5= @ 1.3768

SL= Break below S2

❤️ If you find this helpful and want more FREE forecasts in TradingView

. . . . . Please show your support back,

. . . . . . . . Hit the 👍 LIKE button,

. . . . . . . . . . Drop some feedback below in the comment!

❤️ Your support is very much 🙏 appreciated!❤️

💎 Want us to help you become a better Forex / Crypto trader?

Now, It's your turn!

Be sure to leave a comment; let us know how you see this opportunity and forecast.

Trade well, ❤️

ForecastCity English Support Team ❤️

💡Don't miss the great buy opportunity in EURCADTrading suggestion:

". There is a possibility of temporary retracement to the suggested support line (1.3090).

. if so, traders can set orders based on Price Action and expect to reach short-term targets."

Technical analysis:

. EURCAD is in a range bound, and the beginning of an uptrend is expected.

. The price is below the 21-Day WEMA, which acts as a dynamic resistance.

. The RSI is at 57.

Take Profits:

TP1= @ 1.3221

TP2= @ 1.3307

TP3= @ 1.3398

TP4= @ 1.3526

TP5= @ 1.3768

SL= Break below S2

❤️ If you find this helpful and want more FREE forecasts in TradingView

. . . . . Please show your support back,

. . . . . . . . Hit the 👍 LIKE button,

. . . . . . . . . . Drop some feedback below in the comment!

❤️ Your support is very much 🙏 appreciated! ❤️

💎 Want us to help you become a better Forex / Crypto trader ?

Now, It's your turn !

Be sure to leave a comment; let us know how you see this opportunity and forecast.

Trade well, ❤️

ForecastCity English Support Team ❤️

EURCAD moving to the 1.32 ? 🦐EURCAD on the 4h chart is testing the support area at the 1.34 level.

The price has tested the level a few times and a break below can be expected.

How can i approach this scenario?

I will wait for a potential break of the level and in that case i will set a nice short order according to the Plancton's academy rules.

--––

Follow the Shrimp 🦐

Keep in mind.

🟣 Purple structure -> Monthly structure.

🔴 Red structure -> Weekly structure.

🔵 Blue structure -> Daily structure.

🟡 Yellow structure -> 4h structure.

⚫️ Black structure -> <4h structure.

Here is the Plancton0618 technical analysis , please comment below if you have any question.

The ENTRY in the market will be taken only if the condition of the Plancton0618 strategy will trigger.

EURCAD Reversal?Triple bottom with RSI divergence.

Nice RR for a swing trade with a TP around the 1.38 level.

Note 50 cross on the RSI at time of publish.

An overdue pullback on spot oil prices will strengthen this idea, so worth keeping an eye on that market too.

Cheers !

Bearish downtrend. Target S5I am looking to short this thing.

85 percent of retailers are long on EURCAD. We go the opposite way.

For educational purposes only!

EURCAD approaching the bottom of its Channel Down.The EURCAD pair has been trading within a Channel Down pattern since September 2021 Triple Top. Such Double/ Triple Top Resistances are important as even in the one time the price broke above the pattern, it got rejected (February 07) on the Resistance of the previous High (Double Top), which also happened to be where the 1D MA200 (orange trend-line) was.

On the short-term, we can buy and target the 0.5 Fibonacci retracement level (around 1.33800). Only a break above the previous (Lower) High (1.37200) can turn the long-term trend around.

--------------------------------------------------------------------------------------------------------

Please like, subscribe and share your ideas and charts with the community!

--------------------------------------------------------------------------------------------------------

EURCAD longEURCAD Long

TP1 and move SL to BE

It's possible that I'll use different entry points, take profits, and tactics, but my trades will respect the direction as shown on the chart.

Trade at your own risk, I'm not a financial advisor.

OANDA:EURCAD

EURCADPENDING 📈 (Buy limit)

Pending ⏳ #EURCAD

Entry point (Entry point) : 1.32294

SL (8pips): 1.32214

TP (111pips): 1.33412

EURCAD Possible SellEURCAD broke Daily support and retested, showing some strenght to the downside, im gonna short from here.

EURCAD: Head and Shoulders pattern and Positive CAD dataHey traders, in today's trading session we are monitoring EURCAD for a selling opportunity around 1.339 zone, once we will receive any bearish confirmation the trade will be executed.

Trade safe, Joe.