Short Brasil (EWZ)Super China bear here looking at a lovely technical setup. The rally has gotten way too far ahead of itself. The 50month MA and a decade long trendline as well as the .50 fib level from the 2014-2016 move all acting as resistance.

EWZ

An inverse trip to BrazilBrazil is known for nice beaches, women and carpirinhas.

The beautiful Christ the Redeemer is placed high above Rio.

Raging high is also the price of EWZ which is stretched more than 30 % above its 200 DMA.

It has reached 1.618 of its previous intermediate top and it is due for an intermediate cycle low correction soon.

It has met a big resistance level and its RSI indicates heavily overbought conditions.

Wait for "double top" and take position in BRZS which is 3x inverse EWZ. Recommend start with 50% position and increase by 50% after first confirmation.

EWZ weekly - triple resistance - 10/18/2016Expect some pullback and higher volatility from here. Note weaker RSI and MACD relative to price. Buy a retested breakout if occurred.

Short Idea for PBR

On daily chart, it's 3rd day outside from the upper Bollinger Band. It means a calling for a interesting correction.

On hourly chart, an overbought is present on RSI & Stochastic. MACD & Histogram shows a little weakness.

On hourly chart, its target in 10.75 from a triangle breakout has been reached.

EWZ weekly - short term be cautious - 9/30/2016It has been stalled for 7 weeks, MACD turns negative and RSI rising wedge breaks. Price is still holding well but I am watching the blue support line carefully.

Overall up trend is intact given the rising 40 week moving average, any drop less than 20% should be seen as a healthy correction and should be bought given the up trend bias.

EWZ weekly - still looks healthy - 9/1/2016It has some overbought fatigue but overall still looks healthy. Buy new high if it can make it.

TRADE IDEA (PREMIUM SELLING): EWZ OCT 21ST 29.5 SHORT PUTHere, I'm just looking to sell a little premium in the highest implied volatility, broad market underlying there is out there at the moment -- the Brazil exchange-traded fund, EWZ. The Olympics, after all, are over, and no doubt body parts will be washing up again soon on Copacabana beach, PBR will be undergoing yet another corruption/fraud/you-name-it scandal, and there is, of course, that whole impeachment thing ... .

Metrics:

Probability of Profit: 71%

Max Profit: $107/contract (at the mid)

Breakeven: 30.46

Notes: I'm basically selling the ~30 delta strike here. I'll look to roll the option down and out for duration and credit if the price of the option equals 2x what I received in credit for it. Otherwise, I'll leave it alone and look to cover the trade at 50% max profit. Naturally, there's a lot of air below the strike, but I'm mentally prepared to have to roll it down and out for a period of time to get it to "work out" ... .

RSX ready to take offFor whatever reason, Russia is not tied to oil price from the technical analysis point of view, could it be geopolitical issue at play? A Trump win in Nov could lift the sanction? I don't know.

Nonetheless, RSX is poised to run toward 21

EWZ weekly - broke out of rising wedge - 7/30/2016A breakout from a rising wedge is very bullish. Highly likely the pink line can be hit soon ($37 level). Red line should provide solid support.

EWZ monthly - may be targeting the pink line - 6/30/2016EWZ finished the month with a strong tone, made a higher high, issued a long term buy signal ( based on 5/10 MMA cross).

Technicals favor a bullish case.

A new rally could give a good trading opportunity - #ProfitingMeHI,

This Fund can still pay a lot of money in the next months and years by the drop.

A new spike on EWZ could give a good trading opportunity. very interesting.

I am trader of profiting.me

Thank you

Girolamo Aloe

EWZ weekly - bounce from 20 DMA - 6/17/2016It is consolidating in the blue triangle. Will have to break out or break down.

EWZ - ISHARES MSCI BRAZIL SHORT SETUPThe price seems to build an H&S pattern, not very perfect in shape. A strong support to break is the 27$ level. Look for a breakout confermation in that level for shorting opportunities. Possible target 23$ level. Risk reward ratio 4,7. Possible gain 14,9%.

EWZ weekly - up trend unchanged - 5/7/2016EWZ failed to break out and lost about $2 from last week's close. All indicators are still healthy (so far).

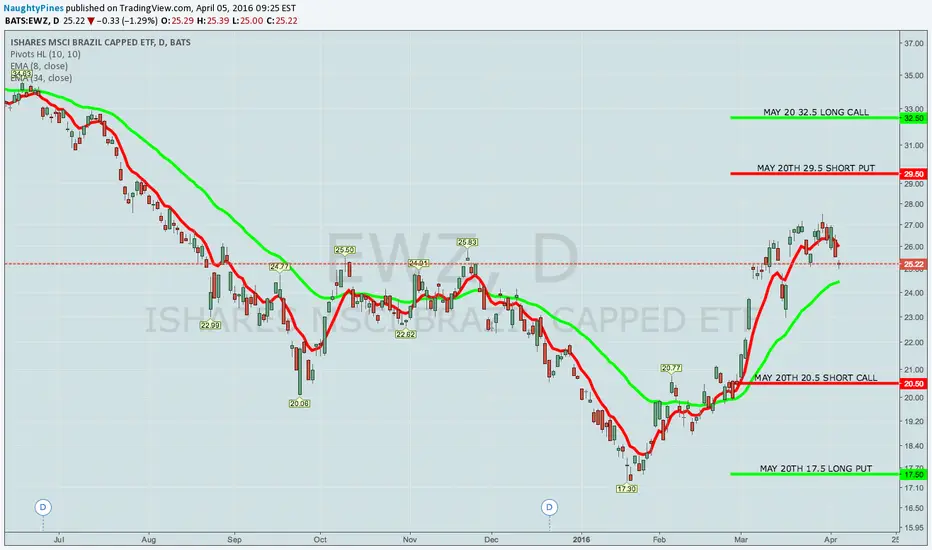

SOLD TO OPEN EWZ MAY 20TH 17.5/20.5/29.5/32.5 IRON CONDORGoing to where the volatility is to sell premium, and that's in EWZ (implied vol rank >70/implied vol is >50). (Plus, I'm kinda ticked that I screwed up closing out that rolled EWZ setup without checking the trade chain ahead of time ... ).

In any event, here are the metrics for the setup:

Probability of Profit: 74%

Max Profit: $66/contract

Buying Power Effect: $234/contract

Notes: I'm continuing to go with small defined risk setups here. EWZ has been "hot" volatility wise, and I may want to layer on additional setups going forward in the instrument, dispersing risk over several expiries. I also want to keep powder dry for broad market premium selling plays and/or additional long volatility setups, depending on which way the market goes ... .

EWZ weekly - golden cross - 4/29/2016EWZ had a golden cross (10 week MA above 40 week MA). And it appears to be closed above the blue resistance (a small breakout?) RSI and MACD all broken out.

BOUGHT EWZ MAY 27TH 22.5/31.5 SHORT STRANGLE TO CLOSEOriginally opened for a $104 credit, I closed this out today for a $60 debit, yielding a $40.92/contract profit after fees/commissions ... .

THE FORCE BEHIND BRAZIL'S RECENT BULLISHNESS (ANALYSIS ON EWZ) If you've been paying attention to headlines about Brazil recently, the term "impeachment" seems to be all over the place. But what's really driving prices upwards in the country's stock market? Is it the daily swaying impeachment probability or something else?

Today's instrument to be analysed is EWZ, the ETF that seeks to track the investment results of the MSCI Brazil 25/50 Index. The fund generally invests at least 95% of its assets in the securities of its underlying index and in depositary receipts ("DRs") representing securities in its underlying index. The index, which consists of stocks traded primarily on the BM&FBOVESPA, is a free float-adjusted market capitalization-weighted index with a capping methodology applied to issuer weights so that no single issuer of a component exceeds 25% of the underlying index weight, and all issuers with weight above 5% do not cumulatively exceed 50% of the underlying index weight. The fund is non-diversified. (source: finance.yahoo.com)

The chart's left side is late October 2014, when president Dilma Rousseff got re-elected. As can be seen, EWZ price has since then maintained a close correlation with the price of other Emerging Market ETFs and Indexes

2015 was a perfect storm for Emerging Markets. With China's slowdown, a commodity crash, the strong dollar, a Fed rate hike, the light at the end of the tunnel was nowhere to be seen.

Commodities

Many emerging markets depend on commodities like oil, iron and copper in order for their economies to do well.

Commodity prices tumbled in 2015, with Crude Oil hitting a 7-year low in December. Oil and other commodities are not set to boom in 2016, but they likely won't tumble as much as they did last year, specially if OPEC agrees on setting production quotas again.

China's Slowdown

China is transitioning to a consumer-led economy from one led by manufacturing and construction, meaning its demand for all those commodities has plummeted.

China has been cutting rates, weakening the currency and pumping money into the economy to counteract the slowdown.

Many experts believe China's growth may slow down more in 2016, but not at a faster pace. A more stable China should help the countries that depend on it.

Strong Dollar and Rate Hike

The good news is that a weak currency lets emerging markets sell products abroad more cheaply, making them more attractive to foreign buyers. That eventually boosts exports and, in turn, economic growth.

The bad news is that emerging markets have to pay off some debt in U.S. dollars. In total, there's $3 trillion of emerging market debt denominated in dollars, according to Wells Fargo. As the dollar rallies, that debt gets more expensive to pay back.

The rate hike makes the US Bonds more attractive and attract foreign money to the US. This money has to be exchanged into US Dollars and ends up boosting the currency.

Many leaders in emerging markets are actually glad the Fed finally raised rates. So much uncertainty surrounded the first rate hike, and now that it's done, that gives emerging markets more clarity.

With all this in mind, it's silly to say Dilma's possible impeachment is the main responsible for the upwards drive in Brazil's stock market prices...

TRADE IDEA: EWZ MAY 27TH 22.5/31.5 SHORT STRANGLEI already have a couple EWZ premium selling setups on, but with an implied volatility rank of 95 and implied volatility of 59, I'm going to put some more on here. I'm going small and using multiple expirations for setups to disperse my risk, while taking advantage of this fairly low priced underlying to haul in some pretty good credit.

Here's the metrics:

Probability of Profit: 73%

Max Profit: $105/contract

Buying Power Effect/Max Loss: ~$271/contract; undefined

Notes: I'm going short strangle here due to the limited buying power effect, as well as better metrics over an iron condor, where the long options "drag" on max proft. As with all my short strangles, I'll look to take this off at 50% max profit.

PREMIUM SELLNG: NEXT WEEK REMAINS A "WASTELAND"Another week of wasteland for premium selling, with EWZ again topping the volatility charts for non earnings plays, although I may go small with an IWM setup in the May monthly (it's the most volatile amongst the index ETF's, which ain't saying much). I've got one more short-term RUT/IUX setup on that I will need to address, but other than that, it's going to be a light week trading wise from where I'm sitting right now.

Although you can naturally dip your toe into some of the more volatile individual underlyings pre earnings, my preference is to keep powder dry until the actual announcement is upon us before diving in, and there simply isn't anything on next week's earnings calendar that meets my standards for "options playability."

So, in the absence of some monumental sea change here, I'm going to be mostly hand sitting for the week on options plays, but may dabble with scalping /ES intraday and/or look for another opportunity to go long volatility in a VIX derivative, assuming we get to around VIX 13-ish.