GBP/JPY at the Edge! Bounce or Breakdown? The weekly chart of GBP/JPY reveals a highly volatile scenario, with a recent bearish expansion pushing the price back toward a key support zone between 185.00 and 188.30 — an area that has been defended multiple times in the past. After an attempted recovery toward the supply zone between 194.00 and 195.00, the pair encountered heavy selling pressure, failing to break out and sharply reversing.

From a technical perspective, the move suggests a possible swing failure above local highs, with the current weekly candle confirming a return below resistance. Price action is now within a critical area: if the current support holds, we could see a technical rebound with interim targets at 191.40 and potentially back toward 194.00. However, a breakdown below 185.00 would open the door to deeper correction, with possible extensions toward 182.00 and 180.00 — both zones marked by previous accumulation.

The RSI, after dipping into oversold territory, is now attempting a reaction, indicating that buyers are trying to regain control, though the structure remains fragile. Strategically, this phase demands caution: aggressive longs may seek confirmation of reversal above current lows, while bearish traders should closely watch for a confirmed breakdown below support. The 188.30 to 191.40 price range will be key to monitoring the next directional move.

Fed

GBP/NZD Breakdown Imminent? Smart Money and Seasonality Say YES!🧠 1. Price Action & Technical Structure

Price was firmly rejected from the monthly supply zone between 2.33 – 2.35, marked by strong bearish candles.

A bounce occurred at the weekly demand between 2.20 – 2.22, where accumulation and a short-term reversal formed (dashed white arrow).

Currently, price is trading near the lower bound of a compression range (2.22 – 2.26), sitting below a key intermediate resistance (dark teal zone).

RSI is in the neutral-to-low zone, with no major divergence, leaving room for further downside.

Technical Bias: Neutral to Bearish unless we get a weekly close above 2.26–2.27.

📊 2. COT Data

GBP

Asset Managers remain net short, though improving since January.

Leveraged Money sharply reducing long exposure since early April → Institutional bullish sentiment weakening.

NZD

Asset Managers have been heavily short for over a year, but shorts are being reduced since February → slight sentiment recovery.

Leveraged Money flat, with no clear long build-up yet.

➡️ Combined COT Outlook: The GBP's advantage over NZD is fading. This supports a sideways to slightly bearish outlook on GBP/NZD.

📅 3. Seasonality

April: Historically bearish for GBP/NZD (–0.2971 avg.), aligning with current downward move.

May: Also typically bearish (–0.2964 avg.) → suggesting potential continued weakness.

➡️ Seasonal Bias: Bearish through mid-to-late May.

🧠 4. Retail Sentiment

Around 70% of retail traders are long GBP/NZD → classic contrarian bearish signal.

Average long entry: 2.1800, current price: 2.2246 → many longs in profit.

Potential for profit taking or breakeven pullback adds to bearish pressure.

📌 Trade Plan Summary

Weekly Bias: → Bearish / Range-bound

📉 Short Zones of Interest:

2.26 – 2.27 → key resistance zone

Stop above 2.2850 (H4/H1 close above invalidates setup)

🎯 Targets:

2.2050 → recent demand re-test

2.1850 / 2.1650 → deeper demand zones visible on chart

🧠 Invalidation Level:

Daily close above 2.2850 → structure turns bullish

April 24, 2025 - Not getting fired (yet)Hello everyone, it’s April 24, 2025, welcome back to another wild episode of “Trumponomics: The Market Edition.” For the second day in a row, global markets are on the rise, and yes, it’s all thanks to the Trump playbook: slap tariffs everywhere, terrify the market, escalate tensions, then toss out a gesture of peace and voilà — rally mode engaged.

The key word this morning? Relief. Relief that Trump might chill out on China, and Powell isn’t getting fired (yet). But let’s not pop the champagne too soon — anyone betting against a weekend plot twist from Trump hasn’t been paying attention.

In the US, the Fed’s Beige Book (a.k.a. the economy’s mood diary) painted a picture that’s… let’s say “limp but not lifeless.” Only 5 of the 12 Fed districts saw growth, and even that was more “walker with tennis balls” than Olympic sprint. Inflation? Creeping in slowly, with companies sharpening their price-hike pencils just in case Trump cranks up the tariff heat again. Employment? Not awful, but nothing to brag about. And uncertainty? It was mentioned 80 times in the report. That’s not a joke.

Meanwhile, auto sales are up — not because the economy’s booming, but because Americans are panic-buying ahead of expected price surges from more tariffs. Business travel is tanking, and tourism’s taking a nosedive. Welcome to the “Not-quite-a-crisis-but-definitely-not-fine” States of America.

As for OANDA:XAUUSD , after a brief flirtation with $3,500, it’s cooled down to $3,337. BLACKBULL:WTI is holding at $62.86. And INDEX:BTCUSD ? It’s back in the spotlight at $92,000 and climbing — yes, people are talking about it again, which should tell you something about the vibe out there.

On the politics front, Trump hinted that the tariff moratorium could be revoked for some countries, and he’s back to pestering Powell to cut rates. Classic. Meanwhile, Wall Street is just trying not to get whiplash. NYSE:BA numbers came in better than feared, and NASDAQ:NVDA supply chain via INX looks solid despite wild swings.

Today’s economic calendar includes durable goods data and jobless claims in the CME_MINI:ES1! are down 0.2% — looks like investors are just bracing for the next Trump curveball.

TL;DR: Markets are riding the Trump-coaster, gold cooled off, crypto’s surging, and America’s economy is wobbling but still upright — for now. Keep your helmets on.

USDCAD at Risk? COT Turns Bearish📊 COT Overview – CAD & USD Futures

🇨🇦 Canadian Dollar (CAD)

Asset Managers: Still net short, but recovering fast → from -150K to nearly -50K.

Leveraged Money: Strong bullish reversal from -100K to -30K and climbing.

✅ Interpretation: Institutions are flipping bullish on CAD → Bearish pressure on USDCAD.

🇺🇸 US Dollar (USD)

Asset Managers: Cutting long exposure since March.

Leveraged Money: Losing conviction → neutral to slightly long.

⚠️ Interpretation: USD is structurally weakening → adding to the USDCAD bearish bias.

🧠 Technical Analysis

Price has returned to the key demand zone (1.3700–1.3850) for the third test.

Candles are compressing → signal of upcoming volatility.

RSI remains weak, no bullish divergence → no clear reversal yet.

📌 Key Levels:

Support: 1.3700 → A confirmed break opens space toward 1.3550–1.3480.

Resistance: 1.3950–1.4100

🎯 Trade Scenarios

🔻 Breakdown trade below 1.3700 → Target: 1.3480

🔁 Pullback short on rejection from 1.3950–1.4000 → SL above 1.4100

🔼 Long only with a bullish engulfing weekly close + RSI divergence

✅ Summary

COT Bias: Bearish USDCAD → CAD strengthening, USD weakening

Technical Structure: Support under pressure, breakout likely

Preferred Play: Short continuation on breakdown or pullback rejection

EUR/USD Explosion or Trap?EUR Futures

Asset Managers: Strongly net long and continuously increasing since December 2024 → a clear sign of institutional confidence in the euro.

Leveraged Money: Also rising, moving from net short to net long → sentiment reversal even from speculators.

✅ Interpretation: Both institutional categories are bullish on the euro, suggesting potential upward support for EUR/USD.

USD Index Futures

Asset Managers: Decreasing since the end of February → reducing long exposure on the dollar.

Leveraged Money: Recovering from net short, but still uncertain → mixed sentiment.

⚠️ Interpretation: The dollar is structurally weakening. This reinforces the bullish bias on EUR/USD.

🧠 Technical Analysis – EUR/USD Weekly Chart

Current price: 1.13150, right in the middle of a weekly/monthly supply zone, marked by upper wicks → clear seller presence.

Price has made a strong rally from 1.03600, breaking through all intermediate supply zones.

RSI: Slightly declining after previously reaching overbought territory.

📌 Key levels:

Major support: 1.1000–1.1080

Structural resistance: 1.1350–1.1450 (current zone)

🧠 Technical Scenario:

If price holds above 1.1250, we could see an extension toward 1.1500.

If it breaks below 1.1200, a pullback toward 1.1080–1.1000 is likely.

✅ Trade Summary:

COT bias: Bullish EUR/USD → strong EUR, weakening USD

Technical: Watch price behavior in the 1.1350 zone → if rejection continues, expect a technical retracement before potential continuation.

🎯 Potential Setups:

Long on pullback toward 1.1080

Breakout long above 1.1450 → targeting 1.1600

Short-term short if bearish price action appears in the current zone

Trump vs. Powell: 4d Gold Price Roller Coaster📊 Summary of Recent 4 Trading Days

During the ongoing US-China trade war, President Trump has ramped up his public criticism of Federal Reserve Chair Jerome Powell. Though he lacks the authority to remove Powell directly it seems, Trump's frustration with the Fed’s independent policy direction has led to an apparent institutional power struggle.

This conflict hasn’t gone unnoticed by the markets. Just the mention of removing Powell caused the gold price to spike, as stock market money got squeezed out, amplified by tensions in the trade war. The Federal Reserve’s credibility is high, so such remarks naturally trigger significant volatility.

After Trump's initial outburst, gold surged $216. But when he softened his tone, the price reversed just as dramatically—falling about $240 (with the trading day still ongoing at the time). Hopes for progress in trade negotiations also played a role in this sharp reversal.

⚠️ Warning Signs of Market Distortion

Statements from the US President now function almost like market-moving events in addition to normal news. For gold traders, this creates an unstable environment where typical technical setups may fail.

The past days showed signs of manipulated or artificial movements—with potential insider activity. One notable example: Gold looked set to break higher after a 1-hour candle closed above the EMA 20 line. But a sudden $12 bearish candle in the last 30 seconds erased the setup. It felt orchestrated—possibly by institutional players defending key levels.

💡 Trader’s Takeaway

Don’t blindly trust technical signals in this environment.

Watch for political noise—it’s louder than usual.

Prefer quieter markets if you’re risk-averse.

Expect $100+ daily ranges and frequent price whipsaws.

🗣 What’s your take?

Is Trump really influencing the gold market on purpose—or just creating chaos? Let’s discuss below. 👇

-------------------------------------------------------------------------

This is just my personal market idea and not financial advice! 📢 Trading gold and other financial instruments carries risks – only invest what you can afford to lose. Always do your own analysis, use solid risk management, and trade responsibly.

Good luck and safe trading! 🚀📊

GOLD heading to $3,450 or a bull trap ahead?XAUUSD has shown a strong bullish reversal from the key zone at $2,832, with a series of high-volatility, full-bodied weekly candles that completely absorbed the supply in the $3,050–3,140 area. The breakout of previous weekly and monthly highs confirmed a bullish structural shift, with a natural technical target around $3,450—its recent all-time high. Price reacted precisely to previously tested demand blocks, suggesting that buy-side pressure may still have room to expand.

However, a deeper look at COT data reveals a more complex picture: Money Managers’ net positions on GOLD have been declining sharply for months, diverging from price action. This may indicate a rally driven more by retail flows or ETFs than by institutional strength, making it potentially unstable. Additionally, the COT report on the Dollar Index shows growing net long positions among leveraged traders, signaling USD strength—historically a headwind for gold.

In summary, gold remains technically bullish with room to climb to $3,450, but COT data raises a red flag: if institutional positions don’t realign with the move, this rally could turn out to be a bull trap. From a trading perspective, there’s room for aggressive longs, but only with tight risk management.

USD/JPY in Free Fall: What’s Behind the Break Below 140?🔍 Technical Analysis – USD/JPY

The weekly chart shows a sharp rejection in the macro zone between 155–158, where strong supply is present (highlighted in red). After brushing historical highs, USD/JPY experienced a vertical drop down to 140, decisively breaking through the key zone at 148–146.

Price has now broken the weekly structure and is approaching an area that previously triggered significant rallies (blue zone between 138–141). Monthly support is in danger, with the RSI deeply in oversold territory, but no clear reversal signals just yet.

📊 COT Report – USD Index

Asset Managers: Slight recovery on long positions, but still in neutral territory.

Leverage Money: Increasing net shorts, indicating speculative bets against the dollar.

The divergence between the falling USD Index and speculative positions confirms a growing lack of confidence in the greenback.

📊 COT Report – JPY Futures

Asset Managers: Strong increase in long positions on the yen since December 2024.

Leverage Money: Reinforcing long bias since February 2025.

This confirms that institutional players are accumulating yen, possibly anticipating BoJ interventions or a broader flight-to-safety.

💥 Trade Outlook

USD/JPY is in full bearish breakout mode. If the 140 level breaks decisively, the next technical targets are:

137.00 → historical mid-level support

134.00 → base of the 2023 structure

Keep an eye on the RSI: a bullish divergence with strong volume could trigger a technical rebound. But as long as the overall sentiment remains strongly risk-off, every rally is a selling opportunity.

Noise, S&P Scenario, Gold BubbleThank you to the tradingview community for engaging and supporting my content.

After another rough start to the week, we have a bit of a crossroads ahead for the S&P

1) We revisit the April 7 lows and poke lower with bear trap opportunities

2) We hold Monday April 21 lows and grind back up to gap fill and revisit 5400-5500 resistance

3) We go nowhere with a lot of intraday volatility and noise (between the April 7 low and the April 9 high)

The markets are on high alert

DXY

Gold

Bitcoin

US Bonds vs Treasuries (yields rising)

Trump is more vocal about threatening the FED or firing Powell and the concern is truly unprecedented

Trade War pause is still ongoing, China is being vocal as well to make sure countries don't simply line up to support the US. For all of this to calm down, US and China have to play nice. China is likely able to hold the line longer than the US in the near-term

Thanks for watching!!!

What if Kid Rock ran the Fed?Gold has broken above $3,400 for the first time, setting a new all-time high as investor confidence in the United States continues to decline.

Citi forecasts gold could reach $3,500 within the next three months. However, this projection might be underestimating Trump’s potential to further undermine confidence in the US.

On Monday, President Trump intensified pressure on Federal Reserve Chair Jerome Powell, calling him a “major loser” and demanding immediate interest rate cuts. Last week the President said, "Powell's termination cannot come fast enough,".

A move to dismiss Powell would likely trigger significant market volatility. Markets generally view Powell as a stabilizing figure, and history shows that a less independent central bank is less effective at keeping inflation under control.

I think it might be fair to wonder what a Federal Reserve Chairman Kid Rock would do for the price of gold.

USDCAD Ready to Collapse? COT Signals a Bearish Storm!🔎 1. COT Context – Canadian Dollar (CAD)

Asset Managers: Consistently net short for most of the period, but since January 2025, there's been a strong recovery—net positions have become progressively less negative. By mid-April, they’re still short, but significantly less so.

Leveraged Money: Also heavily short in December 2024, but showing a clear bullish reversal starting in early 2025, with net positions turning increasingly positive on CAD.

✅ Interpretation: There's been a clear sentiment shift from bearish to bullish on CAD starting late 2024. This adds downward pressure on USDCAD.

💵 2. COT Context – US Dollar Index (USD)

Asset Managers: Consistently long, but reducing their net exposure since late March 2025.

Leveraged Money: Opposite of CAD – heavily short in December 2024, now recovering, though without strong momentum. Positions are hovering around neutral.

⚠️ Interpretation: While CAD grows stronger, USD shows signs of indecision or profit-taking. This amplifies the bearish bias on USDCAD.

📉 3. Technical Analysis – USDCAD

Current Price: 1.38369, right near a strong demand zone between 1.3700 – 1.3830, which has already been tested multiple times.

The current weekly candle is forming a doji or pin bar, hinting at a potential technical bounce.

Key Resistance: 1.45215 (monthly high).

Key Support: 1.3700. A breakdown below this could trigger a move toward 1.3480.

RSI: Neutral to slightly bearish, no major divergences observed.

🧠 Technical Outlook:

If the 1.3700–1.3830 zone holds, we might see a corrective bounce toward 1.4000–1.4100.

If that zone breaks, expect a bearish continuation toward 1.3580–1.3480.

📊 Trade Summary

Fundamental Bias (COT): Bearish USDCAD → Strong CAD, weakening USD.

Technical Bias: Neutral to bearish, potential for short-term bounce before continuation.

🧭 Trade Plan

🎯 Short on pullback toward 1.4000–1.4100 with stop above 1.4150, targeting 1.3600–1.3500.

🎯 Breakout trade below 1.3700 → Enter on daily close confirmation, target 1.3480.

XAUUSD - When will the gold trend reverse?!Gold is above the EMA200 and EMA50 on the 1-hour timeframe and is in its ascending channel. A downward correction of gold towards the demand zone will provide us with the next buying position with a good risk-reward ratio. We expect a fluctuation of $10-15 in each range.

The global gold market has experienced notable shifts in trade flows following the removal of retaliatory tariffs on metals imposed by the Trump administration. According to data, a significant portion of gold that had been moved to New York since December is now being returned to Switzerland, its original destination.

Swiss customs data reveals that gold imports from the United States surged to 25.5 metric tons in March—the highest level in 13 months—up from just 12.1 tons in February. In contrast, gold exports from Switzerland to the U.S. dropped by 32%, falling to 103.2 tons.

For the first time in over 14 months, Comex-approved warehouses, part of the CME Group, have recorded consistent outflows of gold. These outflows indicate a reduction in U.S. futures premiums and a decline in trader anxiety following the removal of tariffs.

Switzerland has once again emerged as the primary destination for gold leaving American vaults, reaffirming its central role in global gold refining and logistics. Nevertheless, a portion of the gold stored in U.S. warehouses continues to serve as a hedge against market uncertainties.

In an average year, the U.S.consumes around 115 metric tons of gold in the form of physical coins and bars. Current data suggests that kilobar inventories held in CME warehouses are sufficient to meet this demand for nearly 12 years.

The gold market remains heavily influenced by geopolitical and economic factors. These developments highlight Switzerland’s importance in refining and transportation, as well as the United States’ significant role in gold storage and resource management.

Meanwhile, a growing number of economic forecasts are warning that the U.S. may be entering a period of “stagflation”—a situation characterized by stagnating economic growth coupled with persistently high inflation. Tariffs have the potential to drive up consumer prices while simultaneously slowing growth, placing financial pressure on households, particularly if the labor market deteriorates.

Central banks face serious challenges in responding to stagflation through monetary policy, as efforts to address one side of the issue often exacerbate the other. Even if the U.S. economy avoids a recession triggered by tariffs, many economists foresee rising risks of a painful stagflationary period.

While economic experts remain divided on whether former President Trump’s trade wars will ultimately tip the economy into recession, a large number of recent forecasts underscore the increasing threat of prolonged inflation combined with sluggish growth. Numerous analysts, including Federal Reserve officials, argue that tariffs are likely to hamper economic expansion and weaken the labor market, all while elevating consumer prices.

However, Lindsey Piegza, chief economist at Stifel Financial, is among those who believe the labor market and consumers remain resilient enough to help the economy steer clear of a full-blown recession—assuming recently announced tariffs are eventually scaled back.

GBP/USD in terminal phase? This zone could flip everything!📊 Technical Analysis

Price is currently trading in a strong weekly/monthly resistance zone around 1.3390–1.3400, marked by a dense multi-layer supply area. Historically, this level has caused sharp rejections.

From the lows, price completed a steep bullish leg, breaking through several structures. However:

Momentum seems overstretched.

RSI shows potential overbought signals.

There's a likely bearish target zone between 1.2950 and 1.2850, which is a key demand area.

📌 Trade Setup:

I’m watching for exhaustion signals or bearish confirmations on H1 to short from the current resistance, targeting the grey and turquoise zones below 1.30.

🧾 COT Report – GBP

Large Speculators (Asset Managers) still hold a net short position, although they've reduced exposure in recent months.

Leverage Funds remain slightly long, but without strong conviction.

💵 COT Report – USD

Leverage Funds have turned significantly net long on the dollar (strong green line upward since March).

This supports a bearish view on GBP/USD, as USD strength returns.

📉 Summary:

Price is at a key decision zone. A technical correction is possible. COT data supports this view:

GBP remains weak on the institutional side.

USD is regaining strength.

EUR/NZD About to Explode? Traders Are Watching THIS Level!📊 General Analysis of EUR/NZD (Higher Timeframe)

1. 📌 Price Context

The price had a strong bounce from a demand zone (highlighted in light blue) around 1.85.

It then broke through multiple supply zones (gray and maroon) to the upside and is currently hovering near 1.91874.

🔍 Key Zones

🔵 Demand Zone (Support)

Range: 1.8430 – 1.8712

This zone has been tested multiple times, with long wicks to the downside → indicating strong buying interest.

A powerful bullish move originated from this area.

🔴 Supply Zone (Resistance)

Current resistance: 1.9187 – 1.9450

This is where the price is currently paused → potential rejection area.

Monthly upper zone (1M): 1.96 – 2.00

A strong long-term resistance. If reached, we might see profit-taking or even a reversal.

🕯️ Candles & Momentum

The large green candle represents a strong bullish breakout.

The weekly candle (labeled "1W") shows indecision → this could be a pause before continuation or the beginning of a pullback.

🔮 Possible Future Scenarios

✅ Bullish Scenario

If the price decisively breaks above 1.9187, the next target is 1.9600 – 2.0000.

⚠️ Bearish Scenario

If price gets rejected at current levels, it may fall back into the support zone 1.8712 – 1.8500, which has previously shown strength.

📈 Lower Indicator (Likely RSI or Wavetrend)

Currently bouncing from an oversold area.

No clear overbought signals → there’s room for more upside.

🧭 Conclusion

Current trend: Bullish (especially in the short to mid term).

Key levels to watch:

Resistance: 1.9187 and 1.96–2.00

Support: 1.8712 and 1.85

ECB lowers rates, Euro edges higherThe euro is showing little movement on Friday. In the European session, EUR/USD is trading at 1.1369, up 0.09% on the day.

The ECB lowered its deposit facility rate on Thursday by a quarter-point, bring the rate to 2.25%. This marked the seventh rate cut since the ECB started its easing cycle in June 2024 and interest rates are now at their lowest since December 2022. The markets had expected the rate cut and the euro showed limited movement in response to the move.

The ECB's rate cut was largely a response to the chaos around US tariff policy. US President Donald Trump has sharply attacked the EU over its trade policy and slapped 25% tariffs on steel and aluminum imports into the US. The EU retaliated with counter-tariffs but suspended those measures for 90 days after Trump suspended a second round of tariffs on EU goods. The sides are negoatiating but the US has threatened new tariffs on pharmaceutical products and the EU-US trade war could escalate in the coming weeks.

The euro has benefited so far from the escalating trade tensions, as hit 1.1476 last week, its highest level since February 2022. The US dollar has sustained sharp losses against the major currencies as investors look for safer shores in the midst of the turmoil in the financial markets.

The ECB statement said that the inflation continues to ease but expressed concern over worsening trade tensions which have muddied the economic outlook. ECB President Lagarde said in her follow-up press conference that "downside risks to economic growth have increased" which would likely impact on exports, investment and consumption.

The Federal Reserve is prepared to lower rates if necesary but the markets have priced in a hold at 90% the May 7 meeting according to CME Fedwatch. A cut in June is much more likely, with a 60% probability.

XAUUSD: Gold is making new highs!Gold is above the EMA200 and EMA50 on the 1-hour timeframe and is in its ascending channel. A downward correction of gold towards the demand ranges will provide us with the next buying opportunity with a good risk-reward ratio. We expect a fluctuation of $10-15 in each range.

• Revised Year-End Outlook: The bank attributes the bullish outlook to increased central bank purchases, inflows into gold ETFs, and continued geopolitical and macroeconomic uncertainty.

• Risk Scenario: Should the Fed shift course due to concerns over U.S. debt or weakening confidence in the dollar as a reserve currency, gold could climb to $4,500 per ounce.

One of the major forces behind this rally has been the weakening U.S. dollar under the Trump administration. Market participants are voicing three primary concerns fueling this sentiment: subpar U.S. economic growth, elevated inflation, and declining productivity. These fears stem from several core issues:

1. Tariffs: While intended to support domestic industry, tariffs are increasingly viewed as disruptive, raising fears of inflationary shocks and fragile supply chains—lessons painfully learned during the COVID era.

2. Economic Growth: Trump’s original growth agenda, centered on tax cuts and deregulation, has been overshadowed by other political developments. Many economists are uneasy about a government that seems willing to defy conventional economic principles—raising fears of repeating the failures of protectionist policies.

3. Budget Deficits: The U.S. is running a staggering 7% budget deficit relative to GDP despite low unemployment (~4%). This raises questions about how Trump’s proposed policies would be funded.

4. Erosion of International Norms: The U.S. dollar’s dominance relies on institutions like NATO, the WTO, and the United Nations, as well as global faith in the rule of law. These foundations are reportedly weakening. There are also emerging concerns from places like Beijing, pointing to American vulnerabilities—especially around intellectual property. In a world where IP rights are no longer respected, what value do American corporations really have?

5. Immigration: It remains unclear how much of Trump’s crackdown on illegal immigration is substantive versus symbolic. What is clear, however, is that undocumented migrants have played a crucial role in suppressing inflation in key sectors like agriculture and hospitality. Without a clear plan to replace this workforce, cost pressures could intensify.

April 17, 2025 - Powell, Japan & TrumpHello everyone, it’s April 17, 2025. Yesterday’s U.S. trading was pure market carnage. Semiconductors ( NASDAQ:NVDA , NASDAQ:AMD , NASDAQ:ASML ) were steamrolled as AI chip bans to China kicked in and Trump dropped another tariff bomb, hiking duties to 245%. That wiped $200 billion off Nvidia alone.

In Chicago, Powell stoked the flames, warning tariffs will fuel inflation and choke growth, and insisted he’s in no rush to cut rates. The CME_MINI:NQ1! tumbled 3%, the CME_MINI:SOX1! lost 4.1%, and bond futures plunged.

This morning, U.S. futures are up about 0.75% on headlines that Trump’s talks with Japanese negotiators are “going very well,” sparking rallies across Asia: Nikkei +1%, Hong Kong +2.7%, Shanghai +1%. It seems even a whiff of détente with Japan sends everyone scrambling back into risk assets.

On commodities, BLACKBULL:WTI jumps to $63.35 amid fresh U.S. sanctions on Iran and OPEC output cuts; OANDA:XAUUSD rockets to $3,352 /oz; INDEX:BTCUSD hovers near $83,500.

Today watch the ECB’s rate cut, Powell’s next speech, Philly Fed and jobless claims before the Good Friday shutdown. With Trump’s erratic tariff theatrics and Powell’s warning of higher inflation and slower growth, volatility is set to reign supreme. Buckle up.

USDCAD - Bank of Canada keeps interest rates unchanged!The USDCAD pair is below the EMA200 and EMA50 on the 4-hour timeframe and is in its descending channel. The continuation of the downward movement of this pair will provide us with a buying position with a good risk-reward ratio. If the correction continues, we can sell within the specified supply zone.

On Wednesday, oil prices climbed by approximately 1%, driven by renewed optimism in the markets regarding potential trade talks between the United States and China. However, lingering concerns about the trade war’s negative effects on global energy demand limited further gains in oil prices.Initially, oil prices declined, but market sentiment shifted after Bloomberg reported—citing an anonymous source—that China was seeking greater respect from the Trump administration before agreeing to new negotiations. The same source also stated that China had requested a new outreach from the U.S. to initiate the discussions.

Giovanni Staunovo, an analyst at UBS, commented that easing trade tensions between the two nations could help reduce constraints on economic growth and energy demand, potentially exerting downward pressure on oil prices.

Meanwhile, the International Energy Agency (IEA) reported that global oil demand is expected to rise by just 730,000 barrels per day this year—well below both its previous projections and those of OPEC.

In a new report, the Fitch rating agency warned that the intensifying global trade war has significantly weakened the outlook for economic growth. According to the report, China’s economic growth will fall below 4% in both this year and the next, while the eurozone is projected to grow by less than 1%.

Fitch further estimates that global economic growth in 2025 will fall below 2%, marking the weakest performance since 2009 (excluding the COVID-19 pandemic period).

Despite the sharp decline in the U.S. growth outlook, Fitch expects the Federal Reserve to delay any interest rate cuts until Q4 of 2025. Conversely, deeper rate cuts are anticipated for the European Central Bank and emerging market economies.

In the energy sector, Fitch lowered its short-term oil price forecast due to risks stemming from weaker demand and trade disruptions but left its natural gas price forecast unchanged.

Additionally, the Bank of Canada maintained its policy rate at 2.75%. Highlights from the Bank’s monetary statement include:

• Tariffs and logistical challenges are driving price increases.

• New U.S. trade policies have heightened uncertainty, slowed growth, and sparked inflation fears.

• The Bank supports economic growth with inflation control but urges caution due to elevated domestic risks.

• Both upside risks (higher costs) and downside risks (weaker growth) to inflation are under close watch.

• Beginning in April, the removal of carbon taxes and cheaper oil are expected to temporarily lower inflation for about a year.

• The recent rise in inflation reflects renewed commodity price growth and the end of temporary sales tax relief.

• Due to high uncertainty related to U.S. trade tariffs, the Bank is refraining from issuing an economic forecast.

• The output gap in Q1 2025 was estimated between 0% and -1%.

• Annualized GDP growth for the same quarter was 1.8%, down from the January forecast of 2%.

• Two scenarios are under consideration: one involving tariff reduction via agreement, and another involving a prolonged global trade war.

• In the first scenario, Canadian and global growth temporarily decline, inflation drops to 1.5%, and later returns to the 2% target.

• In the second, the global economy slows sharply, inflation surges, and Canada enters a severe recession. Inflation surpasses 3% by mid-2026 before returning to the 2% target.

• In both scenarios, the neutral interest rate is estimated to be around the midpoint of the 2.25%–3.25% range.

GBP/CAD at a crossroads: this key level could trigger the drop!My visual analysis highlights a strong multi-timeframe resistance zone (weekly and monthly) between 1.8662 and 1.8779, where price has reacted sharply multiple times. This area, marked in dark burgundy, signals a significant supply zone.

Currently, price is trading back in the 1.8350–1.8400 region. Based on my note on the chart ("Looking for a short opportunity on H1"), I’m anticipating a potential short entry from lower timeframes—likely triggered by a structural break or bearish candlestick confirmation.

🔻 Bearish Scenario:

If I get a short confirmation around the current area, I’ll be targeting the 1.7900–1.7677 demand zone (highlighted in deep blue), which has previously shown strong bullish reactions.

The RSI is also showing signs of potential divergence or overextension, adding weight to the bearish thesis.

🟢 Alternative Scenario:

If price decisively breaks above the 1.8780 monthly resistance, we could see an extended bullish move towards levels not currently visible on this chart.

📌 Operational Note:

I’ll be looking for entry confirmations on lower timeframes (like H1), with valid reversal patterns or price action triggers, and will manage the position dynamically depending on how price behaves around the 1.79 zone.

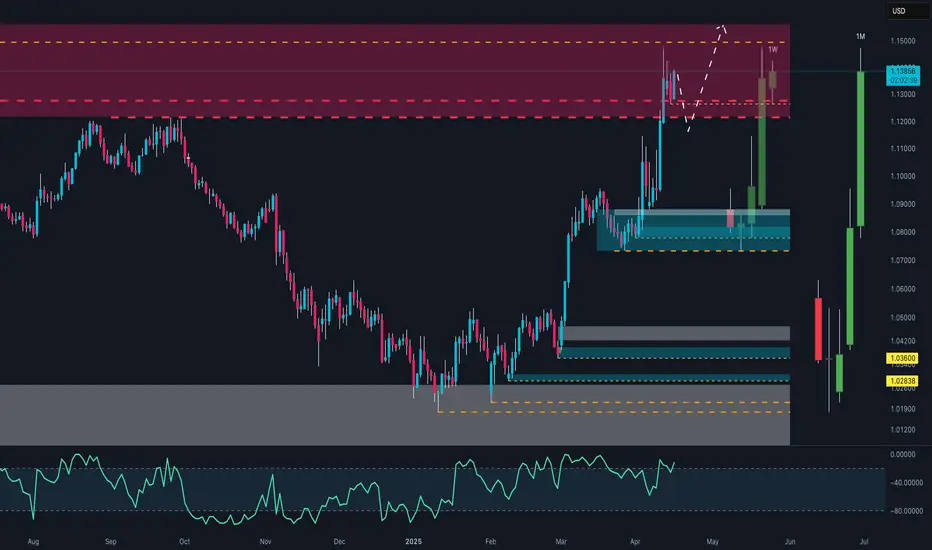

EUR/USD at Key Decision Zone – Breakout or Smart Money Trap?🟢 Current Context

Price: 1.13820 USD

Trend: Strong bullish structure, with impulsive moves especially in April.

Main timeframe: Appears to be daily or weekly, with multi-timeframe zones (1W, 1M marked).

🧱 Key Zones

🔴 Supply Zone (1.13000–1.15000)

Well-defined area of historic selling pressure. Price reacted with a temporary drop but bounced right back into it.

🟦 Demand Zone (1.08500–1.10000)

Major order block where the current rally was initiated. Price used this as a base to launch higher.

⚫ Lower Supports

1.03600: Weekly support

1.02838: Monthly support

Broad accumulation zone (grey box) from which this trend began.

📈 Price Structure

Strong breakout above 1.10–1.11 resistance.

Currently pulling back inside the supply zone – the dashed arrows hint at potential liquidity sweeps before a continuation to 1.15+.

🔍 Momentum Indicator (likely RSI/CCI)

Currently elevated, but not yet in extreme overbought. No clear divergence. Momentum favors bulls.

📊 Scenarios

✅ Bullish:

Clean break above 1.14500–1.15000 opens the door to 1.1600 and 1.1800. Wait for a structural retest for safer long entries.

⚠️ Bearish (corrective):

Strong rejection from the supply zone → potential pullback to 1.10–1.0850 (blue zone).

Only below 1.0850 would a deeper bearish structure toward 1.03600 be confirmed.

🧠 Strategic Note

This is a zone of clear smart money activity: liquidity grabs on both ends.

Watch how this weekly candle closes – we’re either validating above 1.13 or setting up a trap for late longs.

SILVER at a CROSSROADS: Bounce or CRASH to $28?🔹 General Context

Silver has shown a strong bullish reaction from the lows around $28, later reaching a key monthly supply area between $34 and $35. However, this zone has once again been firmly rejected, leaving room for a potential deep retracement.

🟥 Key Zones

🔴 Monthly Supply Zone (34.00 - 35.00 USD): Strong resistance already tested multiple times. Candlesticks show strong rejections and long upper wicks.

🟥 Weekly Supply Zone (33.00 - 34.00 USD): Breaker block or mitigation area that triggered a strong bearish move.

⬛ Current Weekly Support Zone (32.00 - 31.90 USD): Price is currently testing this area. A new impulse could arise here — or we may witness a breakdown.

🟦 Monthly Demand Zone (28.20 - 29.20 USD): The last area defended by buyers in the mid-term. A realistic target in case of breakdown.

📊 Price Structure

The short- to medium-term trend remains bearish, with lower highs and strong rejection candles.

Current price action shows indecision, with lower wicks on recent weekly candles but smaller bullish bodies — a sign of potential accumulation... or just a pullback?

📉 RSI (Relative Strength Index)

RSI is in the neutral-high zone, not yet overbought, but in a downward phase → more room for downside if buyers don’t step in soon.

No clear divergences visible, but watch for signals on the daily timeframe.

🧭 Possible Scenarios

✅ BULLISH Scenario:

Condition: Support holds between 32.50 and 31.90 USD with a clear reversal candle.

Target: Move back toward the supply zone at 33.80 – 34.90 USD.

Confirmation: Break above 33.00 USD with increasing volume.

❌ BEARISH Scenario:

Condition: Weekly close below 31.90 USD → sign of weakness.

Target: Zone between 29.20 – 28.20 USD, a potential new institutional buy area.

Confirmation: Strong bearish break with follow-through and lack of buying reaction.

🧠 Operational Conclusion

Silver is at a critical decision point: bearish pressure from the monthly zones is evident, but as long as the 31.90/32.00 zone holds, buyers may still defend. A clean breakdown would open the door for a drop below $30.

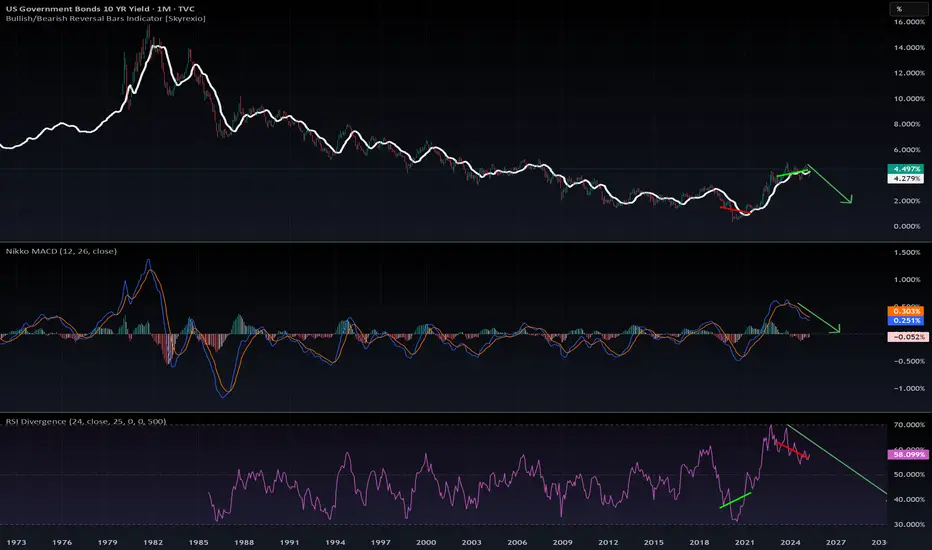

10YR Bond Yields: Panic on LTF, Calm on HTF📉 10YR Bond Yields: Panic on LTF, Calm on HTF

Yes, the recent spike in the 10-Year Yield is causing some short-term panic. But if you zoom out to the monthly timeframe, the bigger picture looks far more constructive.

🔍 Here’s what the chart says:

The MACD and RSI on the monthly are both pointing down.

Yields touched 4.5%, historically a key recession threshold.

We’re now seeing a MACD bearish crossover and a clear bearish divergence—classic signs of a trend reversal.

💡 What does this mean?

If no new fear or shock hits the market, yields are likely headed down, potentially toward the 2% range in the coming months. This would naturally ease pressure on equities and crypto.

📉 Conclusion:

This recent spike in yields seems to be transitional, not structural.

The chart suggests that the top is in, and the market is correcting from an overextended zone.

The Fed might not even need to intervene—the bond market is likely to correct on its own.

Stay calm. Stay rational. Always zoom out.

#10YearYield #BondMarket #MacroAnalysis #InterestRates #RecessionWatch #MarketPanic #MACD #TechnicalAnalysis #FederalReserve #CryptoMarkets #StockMarketInsights #StayCalmZoomOut #DYOR

BITCOIN 2025 - A MODERATE SCENARIOBitcoin’s price trajectory hinges on critical technical levels. Should Bitcoin fall below the key support zones—referred to here as the 'red lines' and t he bold black line —it risks entering a bear market, potentially signaling the end of the current bull cycle. These levels are pivotal for sustaining the parabolic bull market’s final leg. Following an initial decline from current levels, Bitcoin is projected to drop to approximately $70K, where it may consolidate for a couple of months. For the best-case scenario to unfold, Bitcoin must hold above the critical $70-77K threshold and execute a sharp V-shaped recovery. From there, a robust rally could propel it beyond $100K around August, culminating in the cycle’s peak in September at its highest point. While this outcome appears unlikely in the short term, it remains the most favorable projection, contingent on Bitcoin maintaining strength above the $70K line. Failure to do so could prematurely terminate the bull cycle.