Just a bounce off or a real trend reversal?DXY sits on a major support zone. Price often delivers a reflex bounce at strong levels before continuing the prevailing trend, so a quick pop isn’t proof of a new bull run. DXY is closely linked to US real yields (10y TIPS): if real yields roll over as the Fed eases, USD strength likely fades; if real yields stay firm, a durable reversal is more plausible.

This post is for informational/educational purposes only and is not investment advice or a solicitation to buy/sell any security. Past performance is not indicative of future results. I may hold positions related to the instruments mentioned.

FEDFUNDS

Behind the Curtain: Macro Indicators That Move the Yen1. Introduction

Japanese Yen Futures (6J), traded on the CME, offer traders a window into one of the world’s most strategically important currencies. The yen is not just Japan’s currency—it’s also a barometer for global risk appetite, a funding vehicle for the carry trade, and a defensive asset when markets turn volatile.

But what truly moves Yen Futures?

While many traders fixate on central bank statements and geopolitical news, machine learning tells us that economic indicators quietly—but consistently—steer price action. In this article, we apply a Random Forest Regressor to reveal the top macroeconomic indicators driving 6J Futures across daily, weekly, and monthly timeframes, helping traders of all styles align their strategies with the deeper economic current.

2. Understanding Yen Futures Contracts

Whether you’re trading institutional size or operating with a retail account, CME Group offers flexible exposure to the Japanese yen through two contracts:

o Standard Japanese Yen Futures (6J):

Contract Size: ¥12,500,000

Tick Size: 0.0000005 = $6.25 per tick

Use Case: Institutional hedging, macro speculation, rate differential trading

o Micro JPY/USD Futures (MJY):

Contract Size: ¥1,250,000

Tick Size: 0.000001 = $1.25 per tick

Use Case: Retail-sized access, position scaling, strategy testing

o Margin Requirements:

6J: Approx. $3,300 per contract

MJY: Approx. $330 per contract

Both products offer deep liquidity and near 24-hour access. Traders use them to express views on interest rate divergence, U.S.-Japan trade dynamics, and global macro shifts—all while adjusting risk through contract size.

3. Daily Timeframe: Top Macro Catalysts

Short-term movements in Yen Futures are heavily influenced by U.S. economic data and its impact on yield spreads and capital flow. Machine learning analysis ranks the following three as the most influential for daily returns:

10-Year Treasury Yield: The most sensitive indicator for the yen. Rising U.S. yields widen the U.S.-Japan rate gap, strengthening the dollar and weakening the yen. Drops in yields could create sharp yen rallies.

U.S. Trade Balance: A narrowing trade deficit can support the USD via improved capital flow outlook, pressuring the yen. A wider deficit may signal weakening demand for USD, providing potential support for yen futures.

Durable Goods Orders: A proxy for economic confidence and future investment. Strong orders suggest economic resilience, which tends to benefit the dollar. Weak numbers may point to a slowdown, prompting defensive yen buying.

4. Weekly Timeframe: Intermediate-Term Indicators

Swing traders and macro tacticians often ride trends formed by mid-cycle economic shifts. On a weekly basis, these indicators matter most:

Fed Funds Rate: As the foundation of U.S. interest rates, this policy tool steers the entire FX complex. Hawkish surprises can pressure yen futures; dovish turns could strengthen the yen as yield differentials narrow.

10-Year Treasury Yield (again): While impactful daily, the weekly trend gives traders a clearer view of long-term investor positioning and bond market sentiment. Sustained moves signal deeper macro shifts.

ISM Manufacturing Employment: This labor-market-linked metric reflects production demand. A drop often precedes softening economic growth, which may boost the yen as traders reduce exposure to riskier assets.

5. Monthly Timeframe: Structural Macro Forces

For position traders and macro investors, longer-term flows into the Japanese yen are shaped by broader inflationary trends, liquidity shifts, and housing demand. Machine learning surfaced the following as top monthly influences on Yen Futures:

PPI: Processed Foods and Feeds: A unique upstream inflation gauge. Rising producer prices—especially in essentials like food—can increase expectations for tightening, influencing global yield differentials. For the yen, which thrives when inflation is low, surging PPI may drive USD demand and weaken the yen.

M2 Money Supply: Reflects monetary liquidity. A sharp increase in M2 may spark inflation fears, sending interest rates—and the dollar—higher, pressuring the yen. Conversely, slower M2 growth can support the yen as global liquidity tightens.

Housing Starts: Serves as a growth thermometer. Robust housing data suggests strong domestic demand in the U.S., favoring the dollar over the yen. Weakness in this sector may support yen strength as traders rotate defensively.

6. Trade Style Alignment with Macro Data

Each indicator resonates differently depending on the trading style and timeframe:

Day Traders: React to real-time changes in 10-Year Yields, Durable Goods Orders, and Trade Balance. These traders seek to capitalize on intraday volatility around economic releases that impact yield spreads and risk appetite.

Swing Traders: Position around Fed Funds Rate changes, weekly shifts in Treasury yields, or deteriorating labor signals such as ISM Employment. Weekly data can establish trends that last multiple sessions, making it ideal for this style.

Position Traders: Monitor PPI, M2, and Housing Starts for broader macro shifts. These traders align their exposure with long-term shifts in capital flow and inflation expectations, often holding positions for weeks or more.

Whatever the style, syncing your trading plan with the data release calendar and macro backdrop can improve timing and conviction.

7. Risk Management

The Japanese yen is a globally respected safe-haven currency, and its volatility often spikes during geopolitical stress or liquidity events. Risk must be managed proactively, especially in leveraged futures products.

8. Conclusion

Japanese Yen Futures are a favorite among global macro traders because they reflect interest rate divergence, risk sentiment, and global liquidity flows. While headlines grab attention, data tells the real story.

Stay tuned for the next installment of the "Behind the Curtain" series, where we continue uncovering what really moves the futures markets.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

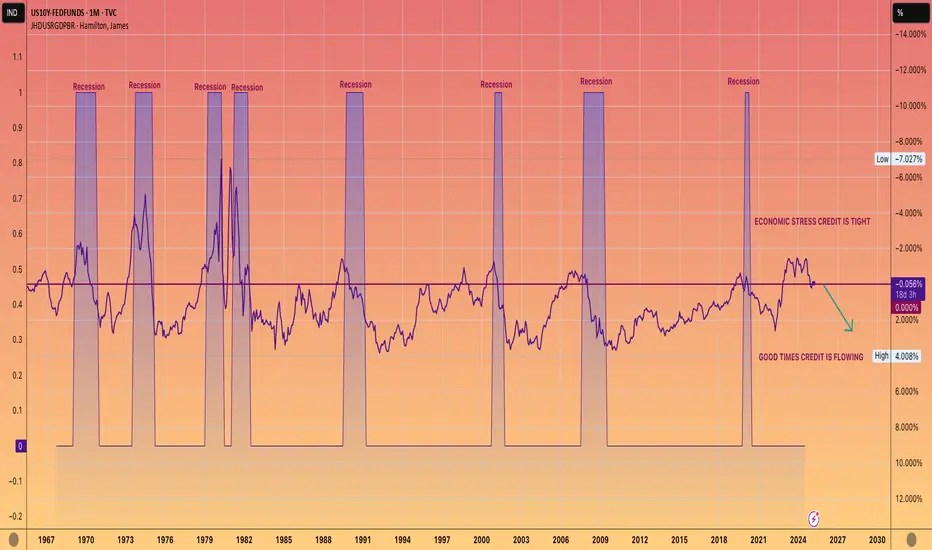

WE ARE COMING OUT OF A RECESSION. NOT GOING INTO ONE.This chart shows 10-year yield, which is closely tied to mortgage rates, minus the Federal funds rate.

When this figure is negative, it typically indicates that we are experiencing a recession or economic downturn.

Conversely, a positive number usually aligns with economic growth, often referred to as the good times.

While it's up to you to determine the reasons behind a official recession not being declared during the Biden administration, the undeniable data reflects a prolonged period of economic strain.

However, the current trend seems to be shifting towards a positive reading, which should lead to more accessible lending and economic growth.

AKA The good times are coming.

Fed Funds with 2yr, 10yr and 30yr TreasuriesChart recessions on a graph of Fed Funds with several Treasury issuances and charts of JPY, EUR, Gold DXY etc.

Enjoy.

What is the future of interest rates?Only time will tell. My guess is that they'll be coming down, but first we get a major melt up from equities and then the recession can start when government spending gets the Elon AXE.

TLT/TLT5 Indicates TLT BBOTThe current value of the ratio of TLT to its leveraged product is equal to the monthly closes of the last two blast off points, resulting in 16% and 20% rallies within 2-5 months.

NFP & Port Strikes: Why Jobs Matter This Week Nonfarm Payrolls (NFP) are projected to rise by 140,000 in September, matching August's pace and pushing the three-month average job gains to the weakest level since mid-2019. The NFP data is due this Friday.

At the same time, a major labor disruption is underway. Dockworkers at 14 key ports, handling roughly half of U.S. trade, have launched an indefinite strike. The walkout could disrupt trade and strain the economy ahead of the presidential election and the crucial holiday shopping season.

Chicago Fed President Austan Goolsbee expressed concern that a prolonged strike could worsen supply chain bottlenecks, exacerbate inflation, and alter expectations for the Federal Reserve's next move on interest rates.

How to break the marketsIn a fortunate turn of events, inflation has calmed.

For equity bulls, more good news. Yield rates have probably peaked.

To stop inflation, you must cool down a HOT economy. Overconsumption tends to increase prices. In an unfortunate (?) turn of events however, the markets haven't calmed down. Some charts suggest that the markets haven't felt at all the decisive rate-hike schedule.

A question arises: Are markets so strong not to feel current yield rates? Or is there some kind of lag we must take into account? When will equities suffer, and how much? These are important questions right now that need serious answers.

A custom indicator was invented to calculate the average-rate-of-return of equities against yield rates. It attempts to answer the following question:

How much better do equities perform YoY against the "safe" US 10-year bond investment?

Some interesting charts come up from this analysis:

In 1951 yield rates broke out of their long-term bear market. At the same time, the equity market exploded in even higher strength. Note that at that period, equities managed to perform better than the ever-increasing yield rates. It was after yield rates ~tripled that problems arised.

Moving to today, we only recently witnessed a breakout in the equity and the yield-rate-schedule. Judging from the '60s, we could even witness a decade of yield rates trying to catch up to the equity market.

A simultaneous breakout can make sense. A massive amount of money has flown out of the bond market and had to enter the equity market.

Equities may be forced to grow, for now. An incoming drop in yield rates from a pause in the rate-hike-schedule will almost certainly create an outflow from equities and back into bonds.

Be prepared. The weakness in the equity market hasn't showed up yet. At any point, the steep upward trend can collapse. A crash will certainly come. But at a time when nobody expects it to. Remember, rates of ~7% managed to break irreversibly the equity market back in the '60s.

Ask yourself and wonder. How tight of an economy can opportunistic equities handle?

At what point will stability become more important for us than growth?

Tread lightly, for this is hallowed ground.

-Father Grigori

FOMC FORWARD GUIDANCE SINCE 2018 w/FED SPEAKERS w/SPX The chart provided visually represents the forward guidance issued by the Federal Open Market Committee (FOMC) alongside the performance of various key economic indicators and market indices. The FOMC forward guidance serves as a crucial tool for signaling the Federal Reserve's monetary policy stance and future intentions, thereby influencing market expectations and economic behavior.

By examining the interplay between FOMC forward guidance and these key economic indicators, investors, policymakers, and analysts can gain insights into the likely direction of monetary policy and its potential impact on financial markets and the broader economy.

I have also included comments from various FOMC speakers to better form a picture of the past.

FOMC FORWARD GUIDANCE SINCE 2018 w/SPXThe chart provided visually represents the forward guidance issued by the Federal Open Market Committee (FOMC) alongside the performance of various key economic indicators and market indices. The FOMC forward guidance serves as a crucial tool for signaling the Federal Reserve's monetary policy stance and future intentions, thereby influencing market expectations and economic behavior.

By examining the interplay between FOMC forward guidance and these key economic indicators, investors, policymakers, and analysts can gain insights into the likely direction of monetary policy and its potential impact on financial markets and the broader economy.

Gold forecast: Crazy to expect rate cut tomorrow? Gold forecast: Crazy to expect rate cut tomorrow?

Mostly yes. Market consensus leans towards the U.S. central bank maintaining current interest rates following the conclusion of its two-day meeting tomorrow. However, the potential impact on the U.S. dollar and gold is likely to hinge on statements from Fed Chair Jerome Powell regarding expectations for a rate cut.

While there is an anticipation of a somewhat dovish shift from Fed officials in the market, the robust January data and the positive JOLTS job report this morning present a case for the possibility of a sustained hawkish stance,

The JOLTS report revealed that U.S. job openings in December surged to 9.026 million, surpassing the expected 8.750 million and marking the highest figure in three months.

XAU/USD was trading in the green for a second consecutive day before the JOLTS report. Gold is currently above a mildly bearish 20 Simple Moving Average for the first time in over two weeks, with longer moving averages situated significantly below the current level.

Still, gold has breached its minor downtrend line originating from the early January high raises the possibility of a bullish target towards $2055, presumably reliant on the possibility of a Fed rate cut (or not).

déjà vuCircle is the most perfect of shapes. It optimizes its area perfectly. An architectural marvel with no point of failure. And it is unique. All circles are similar to each other. Some small, other large. In the end identical.

Cycle is the Hellenic word of Circle.

I purposefully call it "Hellenic" instead of "Greek"

Market cycles are just that, cycles/circles. All of them are identical clones of the original.

Price is after all, nothing more than perfect fractals, the equation of which is, and will forever be, unknown to us.

FED is the all-powerful entity that gives birth and death to bull markets. Its only weapon is yield rates. Don't go against the FED.

Yield rates up = Bull Equity Market

Yield rates down = Bear Equity Market

Many think this is the other way around, that yield rates kill equity markets.

Why do rate hikes help equities though? Because Bonds. Bonds suffer during periods of rate hikes. And they soar when yield rates remain constant or fall.

The usual investment strategy of equities+bonds is creating a rapid shift in flow as we speak.

For a year, massive amounts of wealth was withdrawn from bonds, and invested into equities.

This trend is about to shift rapidly.

And the speed of such a shift is extreme.

While short-term rates are very fast moving, long-term yields represent a heavy market, and thus are more important in our analysis. I will ignore the FEDFUNDS rate because it represents a fraction of the weight of US10Y.

Long-term yields didn't change much in 2007, but the crash was devastating.

In 2018 the same happened, but faster in US10Y. The slope was much higher than in 2007. This resulted in a literal black swan event. The consequences of the 2020 crash are still unknown.

Moving to today, we witness an unparalleled change in yield rates. This has resulted in massive bond crashes as we have shown before, and will most certainly lead to incalculable effects in the equity market.

History has shown that the stronger the rate change, the harder the crash. This makes sense. The higher yield rates go, the greater the incentive to invest in bonds.

Be aware, the market is waiting for the FED to trigger the crash.

Make sure to pick the correct side when the cycle ends again.

Tread lightly, for this is hallowed ground.

-Father Grigori

The Great SufferingWe all remember The Great Depression. That is a lie.

Very few who live today lived when this monumental event occured.

After the Roaring '20s, a decade of parabolic stock market growth and explosive demand for stocks , the cash-out came. In the Depression, people were giving out stocks for free, burning the titles. Truly a desperate action by many. Demand for stocks has gone to zero.

Then, WWII came around, and demand for money was vital for survival.

In finance, supply and demand dictate everything.

Prices increase when demand increases, and they fall when demand diminishes.

Equities and Currencies are opposite powers, both vital to sustain the eternal cycle of markets.

The aftermath of the Great Depression is full of lessons.

Demand for stocks has never been so high as it was in the Roaring '20s.

This may have two explanations. Most of worlds' debt is denominated in Dollar. The function of the dollar changed substantially after the first QE experiment: Abandoning the Gold Standard.

A modern analogue of the mania that existed in 1920s is Bitcoin.

With that in mind, we may conclude the following for the relationship between Gold and Dollar.

Now, demand for Dollars is at an all-time high level.

Fiat currency is a proof of debt. To make some sense of the scale of demand for dollars, we can calculate the total debt. The World Economic Forum has posted the following article regarding world debt.

www.weforum.org

In short, Global Debt has surpassed 300 Trillion in 2023.

Much of that debt is dollar-denominated. US Debt alone has reached 33T at the time of writing.

The (im)possible serviceability of that scale of debt deserves a conversation on its own.

Many questions arise, more than the conclusions.

If BRICS is to create an alternative reserve currency to dollar, what effect will that have in the strength of the dollar? Some may believe that dollar strength will vanish if an alternative is born. After all, demand for it will surely decrease.

Well, there is a catch to all of that.

Dollar has been artificially weak so as weaker economies can afford to borrow it.

As we talked about, world debt has largely depended on dollars.

Some charts (even slightly wrong ones like the following one) may suggest that a Dollar Milkshake scenario is indeed probable. A simplistic PnF analysis of accumulation gives us the following targets for DXY. Don't forget that DXY is nowhere near its all-time high value. So there is the remote probability that this chart is true.

Until now, the focus of the FED was keeping dollar cheap to promote its' borrowing.

Now their stance has changed dramatically.

Yield rates are decisively high, and money supply is actually being burned.

Money supply is vanishing rapidly. This has given birth to a war, between demand for dollars and demand for other currencies. The FED is doing what it can to stop the mania for equities and crypto.

A pivot has been reached. For decades the benefit of the many (cheap debt) resulted in dollar taking the hit (dixie). With the US indirectly involved in war, it is time for The States to look at their survival....

...keeping the nation, the currency and the economy strong. Now that, is something the FED is unwilling to pivot upon. All charts suggest that the FED is performing actions that will strengthen the US. Inflation is being fought, unemployment avoided and equities being kept in stable levels.

Extra Chart:

If the role of the dollar changes once again, and global demand for it decreases substantially, what effect will that have for the relative demand for equities?

Thought Experiment:

Imagine if you will, a scenario where corporate investment utilizes Bitcoin ETFs.

What effect will that have in the performance of their equities as a result of improved investment strategies?

Tread lightly, for this is hallowed ground.

-Father Grigori

Galloping SPYThis chart is frightening. It suggests that SPY can become a modern-day example of Galloping Gertie, the famous Tacoma Narrows Bridge which collapsed from nothing more than wind.

I have said it before, 2022 was the year when an Equity Crash didn't actually happen, while we were all talking about it.

It is but a scratch. But with a bleeding chopped-off arm, how long can you last in war?

Instead of an equities being killed, a Bond Crash came, and nobody has talked about its ramifications.

This is the European Bond, one of the most stable, until 2021. Imagine what has happened in corporate bonds. We can never know for sure the sheer extent of the destruction...

In stock market, higher is not necessarily better. Higher is riskier.

SPY is considered to be diamonds. JUNK Bonds are, well, junk.

Imagine the balance shift when this trend breaks. And it very much it will.

It is statistics after all. The more times you get heads repeatedly, the rarer the event.

Think, for how long has SPY been diamond, and JNK junk?

With yield rates peaking problems may arise. The bond market will suddenly revive again.

As a byproduct, dollar will get a massive hit. Some charts suggests that its days are numbered.

This chart calculates dollar strength based on the value of its total supply. If a currency manages to get printed a lot and sustain high strength, then it must be good. Especially if it pays out good yield rates. Rate cuts in US isn't good news for Dixie...

Tread lightly, for you are dead. You just don't know it yet.

-Father Grigori

Final thought:

Rate cuts can be a double-edged sword.

If FED announces rate cuts, this gives two messages.

-- Financial strength has weakened and rate cuts must come to keep the economy afloat. Bad news can trigger Black Swans. The 2008 crisis followed after rate cuts, not rate hikes.

-- Rate cuts will trigger a massive flow of money into bonds, emptying the equity market.

Careful what you wish for, and what you prepare for.

Parabolic Volatility in the Bond MarketYield Rates represent a percentage. How much would an investor get if they invested in a US Treasury Bond.

A stable economy needs three things, at least according to the FED.

- Low Inflation

- Low Unemployment

- Strong Economy

Yield Rates are the ultimate weapon of the FED. By manipulating rates they stabilize the economy accordingly. They stimulate when they should, and they calm as needed.

A strong economy is a stable economy. Volatility in markets is bad juju.

Stability in yield rates is a matter of survival.

But it seems that we have failed in that.

The average rate-of-change in yield rates has gone parabolic over the decades.

And we are talking about 100 years. The bond market is currently in a whipsaw.

The rate / percentage yields oscillate is beyond comprehension.

Who knows what effects this will have in the years to come.

A similar picture prints in FEDs mind right now.

In absolute yield-rate terms, the average-true-range of rates has formed a bull flag.

Once again this confirms the beginning of the 1960s stagflation.

Tread lightly, for this is volatile ground.

The Golden Elephant-- Prologue --

Crises don't come when everybody expects them to.

I have said this over and over again, for the last year I've been in this platform.

I don't take it back.

Finding out the kind of crisis that will come, the time and the severity, is hard.

Trading, investing, living, is hard...

Some have called me schizophrenic. This is funny. When you say what they want to hear, you are a genius.

When science presents something we aren't used to, we take it as impossible.

In my last few ideas, I received the "kindest" comments of all.

How is it possible... when a chart shows weakness on equities and strength on commodities, it is loved.

How is it possible... when a chart shows weakness on gold and strength on dollar, it is hated.

In my bio I warned you. You will have to deal with my presence for much, much longer.

So here I am again. In front of your face.

-- Analysis --

Price discounts everything. The magic of the fractal nature of the stock market satisfies me every time.

Chart patterns like flags, wedges, channels, triangles, rectangles, rounded tops, appear everywhere.

Some of them have greater strength than others. But each one of them has it's meaning and importance.

To get the elephant out of the room, let's look at the historical Gold chart.

Do note that this chart measures: How much one ounce of Gold is worth in dollars?

In a sense, how precious is a piece of colorful paper compared to a piece of yellow metal?

After decades of QE, Gold has trapped itself inside a MASSIVE wedge, that engulfs it's entire lifespan (inside stock market).

What is the outcome of such a trap? Usually down.

Fractals at their best!!!

If one believes in the Dollar Milkshake, they must not believe that Gold/USD will explode.

And with Bull-Flagging dynamics in the scarcity of Dollar, what will the outcome be?

-- Thought Experiment --

IF a food crisis comes, and you have invested in gold, what would you do?

- Find a food market that accepts gold, and purchase food with gold.

- Find a gold market and sell gold for dollars, and purchase food everywhere with dollars.

Even if you buy stuff with gold coins, the receiver of the coin will go out and exchange it for dollars to pay out their business responsibilities. In both scenarios, gold is taken out of the picture, exchanged for dollars.

Either we like it or not, by default we give more value to money because we use it as money. We don't use gold as money.

-- Conclusion --

There are two ways price increases. Scarcity and demand.

Gold is scarce but who demands it and for what?

Dollar is plentiful and everyone uses it. And now, it gets less and less plentiful.

Tread lightly, for this is hallowed ground.

-Father Grigori

-- Extra Charts --

Commodities like oil could very well overperform equities. I don't advice for or against any investment. I am not an investor. Trade at your own risk.

If one believes in the Dollar Milkshake, then they should invest either in dollars, or in dollar-denominated investments.

Question is: What could these investments be, and how will they perform?

For more information, I have linked below my two hated ideas.

Top of the world... again.The scale of what is happening cannot be understated.

Massive amounts of money have been printed, then burned immediately.

It is as if the FED is trolling us... Or we are being trolled by our own minds.

Equities reflect the mental state of investors, big and small alike.

The dilemma is causing headaches, it has reached a paradoxical state.

No human, not even ChatGPT can solve paradoxes, it is not suicidal.

This chart is one attempt into clearing the picture.

This exotic chart attempts to calculate the price of equities based on the current state of yield curve inversion. It can help calculate the "absolute" strength of indices like IXIC. Similar calculations can be made using the DXY*IXIC/100 formula. It has reached with incredible accuracy the 1.272 retracement, as shown in the main chart.

In short, the higher this chart goes, the better the QE Machine performs.

The Yield Curve is now showing a clear warning signal.

I have been watching closely the price action, now it is more certain than ever that the yield curve may correct sooner than later. A correction of the yield curve has usually led to severe recessions.

After all of this analysis, still no conclusion about equities...

Occam's razor could be the solution. Clear and simple analysis gives the best results.

---

1. Simple Price Patterns.

Sometimes, the simplest answer is the correct one.

---

2. Classic Dow Theory.

It dictates that the weakness of the few may lead to the weakness of the many. DJI is the first to show signs of weakness. Will wider indices like SPX weaken?

With bear flags clearly appearing, and an apparent HnS pattern forming, things couldn't get worse. The post-GFC bull market may fail any time now.

---

3. The Basis of Stock Market

There is this rule that everybody knows and most forget. Price is split between two areas, above and below average. When price is above average, sellers dictate price. Similarly, when price is below average, buyers dictate prices.

Price is higher than average for a long-long time. It is one of the longest-standing equity bull markets. For many years, equity prices are facing increasing selling pressure and decreasing buying pressure. Why? Because investors progressively cash-out of equities.

There may be too little interest for serious investors to buy into equities. Equities are too expensive and too risky for them to be a viable investment decision. You can find more about investment risk in @SPY_Master 's idea linked below.

Tread lightly, for this is hallowed ground.

-Father Grigori

P.S. There is much information I may have left out of this idea. I don't want to be repetitive and I try to keep ideas short and clear. You can find more info about the QE Machine in the following idea.

You against inflationMoney printing has been a double-edged sword. One one hand ample liquidity helped the exponential productivity of the economy, on the other hand inflation hit hard.

In periods of stagflation like the 1970s, immense inflation created an impenetrable ceiling for equities.

In periods of extreme deflation (2010s), equities bubbled. It is interesting that in this period, inflation figures were are all-time lows, with immense money printing.

With this chart we attempt to measure when and how much equities managed to overperform the weight of inflation.

There are two methods of calculating inflation, one is total money printed, and the other is the "cumulative inflation".

If we analyze SPX compared to money printed, this would be the outcome:

This is not very helpful, since SPX is too closely related to total money printed.

To measure "cumulative inflation" I attempted modifying this chart by @SPY_Master

DBC*GOLD is a good estimate of inflation. Since we don't have enough historical data for the DBC index, we analyze one of it's cousins, the PPIACO index. DBC is an energy-focused mutual fund, while PPIACO measures the production cost. We assume that PPIACO*GOLD is a suitable replacement for DBC*GOLD.

We end up with the cover chart, which I will briefly analyze, since it speaks on it's own.

For almost 10 years we were attempting at penetrating the ribbon, to no avail...

These fib-retracements are very beautiful...

SPX:

NDQ:

They all prove that there is massive weight on top of us.

After almost 10 years of trying to get back inside the high-energy-level above, can we do it now?

Tread lightly, for this is hallowed ground.

-Father Grigori

FRED Are Done Raising Rates -- Raise Rates? Japan Collapses.

Japanese Currency Strength is back to 1987 levels

Japan is the main source of YCC for the USA buying down bond Yields

If USA raises rates any more Japan will be in free fall collapse (hyperinflation)

They need to pause at worst start reducing rates.

My guess?

Money printer is coming back and will come back fast to save the Yen, this is not just a "Asian currency" this is the single weak point for the entire US bond system if the Yen goes the US bond yields go ^^^^^^^^^^^^^^^^^^^^^

Japan cannot tap out and raise rates, Japan cannot ditch the Yen and adopt the US Dollar, Japan is in some serious trouble here.

All Japan can do is continue to issue "Stimulus Packs" that is making the M3 go parabolic that leads to serious inflation. Now what happens when a country issues unlimited Stimulus Packs and cannot raise interest rates?

Oil, S&P, FED Funds & CPIPurple droplets indicate where CPI peaks (pink line) and green arrows point to the corresponding oil peak.

Blue dotted lines measure where oil peaks to allow a reference point to S&P chart. Light blue is FED Funds rate.

FEDFUNDS | Too TightThe point of TradingView (and being a human/trader in general) is to learn from your mistakes. I did make some mistakes. Perhaps this idea by itself is another mistake. But I cannot do any different. I must speak out about what I see.

For the past year I tried to understand the pressures that are pushing prices higher, equities lower.

It is important in analysis to avoid the mass, the "common truth".

We all have expected a future of uncontrollable inflation, extreme prices and The Great Reset. The place where everything is too expensive to buy, and we will have to live with coupons.

While some of these may come, it is important to analyze what isn't coming.

Oil prices have been paired with the dollar (with the petrodollar).

Many expect oil prices to explode even further, while "dollar is losing value" and "hyperinflation is imminent".

Some charts however show a different picture...

WIth the 2M chart warning of downward swing, and with the 3M chart showing divergence, the future of oil may not be as explosive as we may believe.

But that is in relative terms. The strength of money seems fated to increase a lot more. Which in relative terms will constitute oil cost to be viable.

In the main chart, it appears that oil is moving into what appears to be a Wyckoff Distribution.

And oil is not the only one who will have trouble with the high-yield environment.

Until now, the usual equity-bond investment scheme has performed tremendously.

This trend is now changing. With a significant trend violation that occurred last year, it seems that we are entering a new period of investment strategies.

From bonds as a hedge against equity weakness, investors should seek alternatives.

The old way of doing things is broken. Commodities will be playing a significant role in the future of investments.

It is in our power to find the new way of doing things.

Tread lightly, for this is hallowed ground.

-Father Grigori

P.S. A link to the indicator I am using.

SPX | Waiting For The Miracle To ComeThis year has been very boring... Lot's of horizontal movement, not many interesting news.

Well, except of course that "a couple" of banks went bust.

But if I didn't tell you that, you couldn't tell where in this chart this occurred...

SPX, and the market in general, has been too stubborn despite the importance of the events occurring.

On the one hand, this makes sense. This kind of crisis (banking) has come before, so the markets are calm. A crisis comes when nobody expects it to. And by design, a crisis is an unknowing event of unknowing consequences. A bank going bust is not frightening anymore. The market expects the FED to step-in and bail everyone out.

But the FED cannot possibly bail anyone out. They cannot print any more money (we might have reached a debt ceiling), and even if they could, they could be unwilling to print more money. Inflation will get worse.

So no more money.

Dollar has served as the worldwide reserve currency, until now. China amongst other powerful nations, collaborate into creating an alternative reserve currency. One that will be controlled by them, not by a panicking (?) FED.

The FED might not be panicking, even if we believe that they are trapped. I believe that they have very good knowledge of what they do, and of the repercussions. Absurdly high interest rates can be a mechanism to increase the dollar purchasing strength. And you need purchasing power when you have enemies (Russia, China etc.)

Since 2015, this has worked out tremendously well. The Dollar is making higher highs.

Of course, there are many fundamentals (like the Dollar Milkshake) that push the dollar value to new highs. But interest rates are interest-ing (hahaha) to the Dollar.

And the Dollar is winning battles against many countries of the world.

And with lower money supply, it's value is fated to increase even further.

(I like real reality, not augmented reality, that's why I used M2REAL instead of M2SL)

The money supply is vacuumed back into the printer which created it. And the power of the vacuum is not big, it is exponential.

The Dollar Milkshake Black Hole is now open.

But how much can the FED possibly hike?

The discrepancy between the FED's rate and the Market's rate is at it's highest level. The FED may not be able to hike any higher against the market's expectance. Who knows what will happen if the FED overcomes this limit... (is it even fundamentally possible?)

Inflation is high and it is fated to increase even more. I have posted about it extensively.

The preview of this chart idea is broken, oops...

Now, oil is looking substantial signs of strength.

Oil, the main inflation influencer, is showing significant signs of bottoming. Furthermore, it has retested a trendline that followed us since 2008. Long-term, the only way for Crude is up!

And the only way for equities is down! Just to reach the mean, the OIL/SPX ratio has to increase by 75%. So there is much room upwards for commodities...

Have you realized what SPX has shaped into?

Could this be the anatomy of a bubble? And has it already broken?

It seems that the recession is only now just beginning.

During normal times for the US economy, equities could grow even as yields were increasing. Now we are entering a period of weakness for the economy. Something has to give, either the equities go bust, or the yield rates. (Equities have much more room to drop than Yields do)

A crisis is definitely inching towards us...

A final chart for today:

Equities used to grow as money was created. Now this chart has immense dynamics to move downwards. In a sense, equities have MUCH room downwards, even if money gets created. This comes to prove that equities cannot absorb any more money supply. Money printing from the FED cannot possibly help equities, no matter what they do, they are trapped inside the bearish wedge. Only way for equities is down!

And similarly for SPX

Tread lightly, for this is hallowed ground.

-Father Grigori

PS. What could these charts mean? Are they of any meaning after all?

A crisis is definitely itching towards us...

I HAVE to test. All the time. Or I get this... this ITCH. It must be hardwired into the system or something.

-Wheatley, Portal 2