GBPCHF looking up 🦐GBPCHF on the 4h chart is testing 4h resistance near to the 1.23 level.

The price after the attempt to break below the support area took the liquidity and now is pushing for a break.

According to Plancton's strategy if the market will break above and satisfy the ACADEMY rules we will set a nice long order.

--––

Follow the Shrimp 🦐

Keep in mind.

🟣 Purple structure -> Monthly structure.

🔴 Red structure -> Weekly structure.

🔵 Blue structure -> Daily structure.

🟡 Yellow structure -> 4h structure.

⚫️ Black structure -> <4h structure.

Here is the Plancton0618 technical analysis , please comment below if you have any question.

The ENTRY in the market will be taken only if the condition of the Plancton0618 strategy will trigger.

GBP-CHF

GBPCHF is on bearish momentum! | 10 Dec 2021Prices are on bearish momentum. We see potential for a drop from our sell entry at 1.23586 which is an area of Fibonacci confluences towards our Take Profit at 1.22024 in line with 61.8% Fibonacci retracement. Technical indicators are showing bearish momentum.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

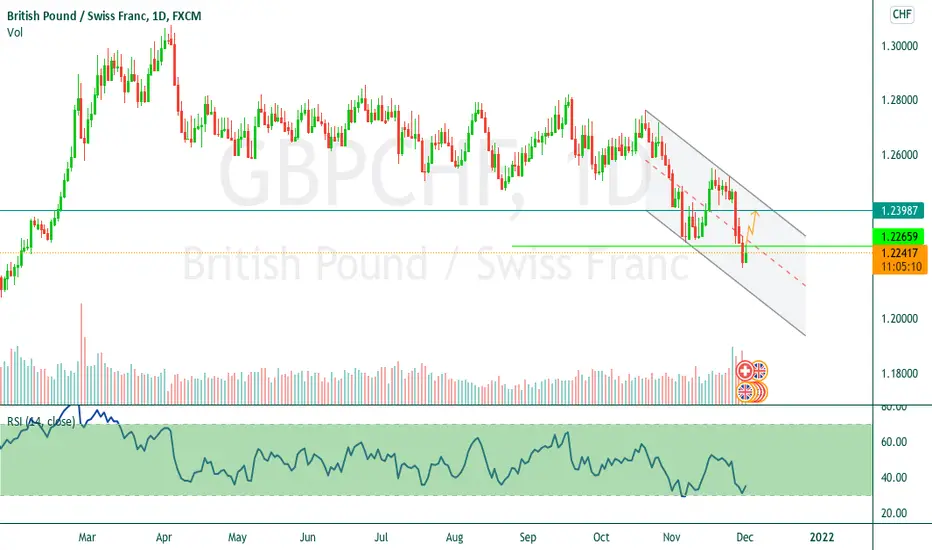

GBPCHF bearish momentum! | 9th Dec 2021Prices are consolidating in a diminishing triangle. We see potential for a dip from our Sell Entry at 1.22065 in line with 50% and 23.6% Fibonacci retracement towards our Take Profit at 1.20194 in line with 61.8% Fibonacci extension and 161.8% Fibonacci Projection. Technical indicators are showing bearish momentum.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

GBPCHF,H4 | short-term bullish bouncePrice is abiding to the descending trendline resistance, signifying overall bearish momentum. However, we can expect a short-term bullish bounce from the pivot level in line with 61.8% Fibonacci projection towards 1st Resistance in line with 78.6% Fibonacci projection. Our bullish bias is further supported by the RSI indicator where it is abiding to the ascending trendline support.

ny opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

DOA Trading Strategy - GBPCHF#GBPCHF - Green DOA fired in 30 mins, green DOA meter have been holding as well, we just broke above the DOA S/R.

GBPCHF a bounce at the 0.618 🦐GBPCHF on the daily chart reached the 0.618 Fibonacci level.

The price perfectly bounced over it in a confluence zone with dynamic and static support.

According to Plancton's strategy if the price will satisfy the ACADEMY rules we will set a nice long order.

--––

Follow the Shrimp 🦐

Keep in mind.

🟣 Purple structure -> Monthly structure.

🔴 Red structure -> Weekly structure.

🔵 Blue structure -> Daily structure.

🟡 Yellow structure -> 4h structure.

⚫️ Black structure -> <4h structure.

Here is the Plancton0618 technical analysis , please comment below if you have any question.

The ENTRY in the market will be taken only if the condition of the Plancton0618 strategy will trigger.

GBPCHF bearish continuation | 1st Dec 2021Price is abiding to the descending trendline resistance, signifying bearish momentum. We can expect price to drop from pivot level in line with 50% Fibonacci retracement and 100% Fibonacci projection towards 1st Support in line with 78.6% Fibonacci extension . Our bearish bias is further supported by the price holding below the Ichimoku Cloud indicator.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

GBPCHF - DAY TRADE VIEWGBPCHF - Momentum is in favour of buyers & as per the trend analysis, technical indicators it's a good buy.

My approach will be a buy only above 1.22650

Maintain stop loss around 1.22000

Potential upside 1.23400 - 1.23900

Trade as per your risk appetite, I will be glad to see your likes & comment.

AUDNZD is on bearish momentum! | 1st Dec 2021Price are on bearish momentum and abiding to our bearish trendline. We see potential for a dip from our sell entry at 1.04559 in line with 50% Fibonacci retracement and 61.8% Fibonacci extension towards our Take Profit at 1.03874 which is an area of Fibonacci confluences. Technical indicators are showing bearish momentum.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

GBPCHF bearish continuation | 1st Dec 2021 Price is abiding to the descending trendline resistance, signifying bearish momentum. We can expect price to drop from pivot level in line with 50% Fibonacci retracement and 100% Fibonacci projection towards 1st Support in line with 78.6% Fibonacci extension. Our bearish bias is further supported by the price holding below the Ichimoku Cloud indicator.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

GBPCHF shortHey Traders, today we are monitoring GBPCHF for the short term selling opportunity around 1,233 zone. once we will receive any bearish confirmation the trade will be executed.

Trade Safe, Joe.

GBPCHF end of a long retracement 🦐GBPCHF on the daily chart reached the 0.618 Fibonacci level and turned to the weekly resistance.

The price is in a long retracement and according to Plancton's strategy if the market will break above and satisfy the ACADEMY conditions we will set a nice long order.

--––

Follow the Shrimp 🦐

Keep in mind.

🟣 Purple structure -> Monthly structure.

🔴 Red structure -> Weekly structure.

🔵 Blue structure -> Daily structure.

🟡 Yellow structure -> 4h structure.

⚫️ Black structure -> <4h structure.

Here is the Plancton0618 technical analysis , please comment below if you have any question.

The ENTRY in the market will be taken only if the condition of the Plancton0618 strategy will trigger.

GBPCHF is on a bullish momentum! 23 Nov 2021Price is consolidating in a triangle. We see potential for a break upwards from our buy entry at 1.24981 in line with 50% and 61.8% Fibonacci retracement towards our Take Profit at 1.25809 which is an area of Fibonacci confluences. Technical indicators are showing bullish momentum.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

FOREX ANALYSIS : GBPCHFFX:GBPCHF

The blue and red lines mean: I think prices can return in these areas.

Green lines mean: I think the price can reach these areas. They are therefore known as transaction targets.

If you want to use this deal, please risk only one percent of your account balance.

GBPCHF I'm in a sell position 👍POW EDGE trend strategy in use for this USDCHF trade.

Entry details are shown on the chart.

Trade has been live since 23:00 UK time.

Working the H1 time frame here and we're only looking for TP3.

Previous trades can also be seen on chart.

A successful long and a short that hit SL.

As always the report box at foot of the idea shows the stats for this strategy.

In that box every trade is logged and can be viewed by clicking the tabs in the report box.

You as the viewer of this idea can also do that so go ahead and have a play.

------------------------------------------

I try and share as many ideas as I can as and when I have time. My trades are automated so I am not sat in front of a screen daily.

Jumping on random trade ideas 'willy-nilly' on Trading View trying to find that one trade that you can retire from is not a sustainable way to trade. You might get lucky, but it will always end one way.

------------------------------------------

Please hit the 👍 LIKE button if you like my ideas🙏

Also follow my profile, then you will receive a notification whenever I post a trading idea - so you don't miss them. 🙌

No one likes missing out, do they?

Also, see my 'related ideas' below to see more just like this.

The stats for this pair are shown below too.

Thank you.

Darren.

GBPCHF is on a bearish momentum! | 18 Nov 2021Prices are abiding to a bearish trendline . We spot a potential sell entry at 1.25201 which is an area of Fibonacci confluences towards our Take Profit at 79.763 in line with 50% Fibonacci retracement . RSI is at a level where dips previously happened. Alternatively, out stop loss will be placed at 1.25667 which is an area of Fibonacci confluences,

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

GBPCHF is on a bearish momentum! | 18 Nov 2021Prices are abiding to a bearish trendline. We spot a potential sell entry at 1.25201 which is an area of Fibonacci confluences towards our Take Profit at 79.763 in line with 50% Fibonacci retracement. RSI is at a level where dips previously happened. Alternatively, out stop loss will be placed at 1.25667 which is an area of Fibonacci confluences,

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and represent their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

GBP/CHF Possible RetracementHello Traders

In last 2 weeks, GBP/CHF suffered a big drop.

It seems we already have reached bottom because price is showing us 2 morning star patterns in Daily TF.

Also price has broken it downward trendline and formed a Bearish Bat Pattern.

RSI is moving up and everything looks fine for retracement.

-We will be happy to see your Comments!

Thanks for Reading

Team Fortuna

-RC

GBPCHF is on a bearish momentum! | 12 Nov 2021Price is abiding by our bearish trendline . We see the potential for a dip from our sell entry at 1.23477 in line with 78.6% Fibonacci retracement and 61.8% Fibonacci extension towards our Take Profit at 1.22959 in line with 61.8% Fibonacci extension and 78.6% Fibonacci retracement . Technical indicators are showing bearish momentum.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and representing their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

GBPCHF is on a bearish momentum! | 12 Nov 2021Price is abiding by our bearish trendline. We see the potential for a dip from our sell entry at 1.23477 in line with 78.6% Fibonacci retracement and 61.8% Fibonacci extension towards our Take Profit at 1.22959 in line with 61.8% Fibonacci extension and 78.6% Fibonacci retracement. Technical indicators are showing bearish momentum.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, as general market commentary, and do not constitute investment advice. The market commentary has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and it is therefore not subject to any prohibition on dealing ahead of dissemination. Although this commentary is not produced by an independent source, FXCM takes all sufficient steps to eliminate or prevent any conflicts of interest arising out of the production and dissemination of this communication. The employees of FXCM commit to acting in the clients' best interests and representing their views without misleading, deceiving, or otherwise impairing the clients' ability to make informed investment decisions. For more information about the FXCM's internal organizational and administrative arrangements for the prevention of conflicts, please refer to the Firms' Managing Conflicts Policy. Please ensure that you read and understand our Full Disclaimer and Liability provision concerning the foregoing Information, which can be accessed on the website.

GBPCHF short moving⤵️👍We are using our trend following EDGE strategy for this GBPCHF trade.

Entry details are shown on the chart.

Trade has been live since 17:00 UK time.

Working the H1 time frame here and we're only looking for TP3.

As always the report box at foot of the idea shows the stats for this strategy.

In that box every trade is logged and can be viewed by clicking the tabs in the report box.

You as the viewer of this idea can also do that so go ahead and have a play.

Last trade was also covered in an idea yeasterday.

Great scalping strategy this one.

------------------------------------------

I try and share as many ideas as I can as and when I have time. My trades are automated so I am not sat in front of a screen daily.

Jumping on random trade ideas 'willy-nilly' on Trading View trying to find that one trade that you can retire from is not a sustainable way to trade. You might get lucky, but it will always end one way.

------------------------------------------

Please hit the 👍 LIKE button if you like my ideas🙏

Also follow my profile, then you will receive a notification whenever I post a trading idea - so you don't miss them. 🙌

No one likes missing out, do they?

Also, see my 'related ideas' below to see more just like this.

The stats for this pair are shown below too.

Thank you.

Darren.

GBPCHF short valid 👇✅It's clearly CHF day as this is my third idea on a CHF pair!

Using the POW reversal script for this strategy.

Trade details for current trade are shown on the chart.

Trade has been live since 11:45 UK time and we are using our POW reversal script.

We are working the 15M time frame on this strategy.

We're looking for the green line which is take profit target.

Little red short arrow is entry point and purple line is stop loss.

Been a good run over the last few days on this strategy as you will see from the previous trades on the chart.

Lets see if it can end the week on a high.

As always trade history can be seen at the foot of this trade idea too for full transparency.

------------------------------------------

I try and share as many ideas as I can as and when I have time. My trades are automated so I am not sat in front of a screen daily.

Jumping on random trade ideas 'willy-nilly' on Trading View trying to find that one trade that you can retire from is not a sustainable way to trade. You might get lucky, but it will always end one way.

------------------------------------------

Please hit the 👍 LIKE button if you like my ideas🙏

Also follow my profile, then you will receive a notification whenever I post a trading idea - so you don't miss them. 🙌

No one likes missing out, do they?

Also, see my 'related ideas' below to see more just like this.

The stats for this pair are shown below too.

Thank you.

Darren

gbpchf seems ready to down in 1hOANDA:GBPCHF

Hi everybody , so now I'm waiting for a trigger to enter a short position on GBPCHF

as we can see in chart , it looks good if we get entry confirmation for short .

what do you think guys ??