Risk and Probability in Trading — Why Risk Assessment MattersRisk and Probability in Trading — Why Risk Assessment Matters More Than Chasing the “Holy Grail”

In trading, most participants and analysts are focused on finding the so-called “Holy Grail” — the perfect entry point where the price moves in the desired direction and yields profit. However, few actually assess the risks involved, as if success is possible without factoring them in. Market reviews are often filled with levels, forecasts, and price directions, but rarely include probability estimates or potential losses.

In my view, the real Holy Grail isn't a guaranteed profitable entry, but a scenario where the market offers a position with minimal risk relative to historical context. To identify such setups, we need a risk scale based on historical data — how favorable the current risk-to-reward ratio is compared to the past.

It’s also crucial to understand that no one can predict price direction with certainty. The key to opening a position is not hope, but evaluating all possible scenarios — upward, downward, or sideways — and knowing the outcome in each case. Risk management is more than just placing a stop-loss; it’s a structured approach that should be central to any trading strategy.

What Are Minimal Risks?

“Minimal risk” is a relative concept — it only makes sense when measured against a defined scale. Building such a scale requires historical statistics: what were the maximum and minimum losses and profits for similar positions in the past?

Profit-to-Loss Ratio

The idea behind the search for the “Holy Grail” is to find moments when the market offers the best possible profit-to-risk ratio. For example, if the current ratio is 10, and historically it has ranged from 0 (low risk) to 100 (high risk), then 10 may be a good entry point. If the ratio approaches 80–90, it signals that the position is extremely risky.

Why Are Probability and Risk Assessment Important?

Market reviews often talk about resistance levels, volatility, and price direction — but rarely address the risks of different scenarios. No expert can predict market movements with certainty — if they could, they’d be billionaires. Opening positions without accounting for risks and scenario probabilities is extremely dangerous.

How to Factor in Risks When Entering a Position

The key question is: what will the profit-to-loss ratio be after entering a position, depending on whether the price goes up, down, or stays flat? It’s important to understand the consequences of each case and make decisions based on risk assessment.

Risk Management Must Account for the Inability to React Instantly

Conventional tools like stop-losses and limit orders often fail to protect capital effectively during sudden price spikes. These tools are particularly vulnerable when market makers or high-frequency algorithms trigger stop levels en masse.

This highlights the need for more resilient risk management instruments — ones that can respond to volatility instantly and automatically. Options are one such tool, capable of limiting losses regardless of market dynamics.

Without robust risk management, long-term profitability becomes statistically unlikely. Sooner or later, the market will present a scenario that can wipe out your capital — unless you’re properly protected.

Important note: this is not an endorsement of options or any specific broker. It’s simply a conclusion based on the logic of building effective capital protection. If a broker only provides access to linear instruments (futures, spot, stocks) without the ability to hedge, it will inevitably lead to capital erosion — even for systematic traders.

And if this article gets more than 100 rockets, I’ll continue sharing specific examples of low-risk trading assessments.

Geopolitical-risk

Crude Oil Prices Rocketing amid geopolitical risks

NYMEX:CL1! NYMEX:MCL1! NYMEX:BZ1!

Macro:

Geopolitical tensions remain high and markets are now likely to price in our scenario discussing ongoing air and missile war, given one-off intervention from the US thus far. According to Reuters, the U.S. now assesses that Iranian retaliation could occur within the next two days.What happens next is anybody’s guess but as traders, it is important to navigate these uncertainties with scenario planning and/or reduce risk to account for increased volatility.

We also get Services and Manufacturing PMI data today and PCE Price Index on Friday. Chair Powell is set to testify on Tuesday 9am CT.

Key levels:

Jan 2025 High: 76.57

2025 High: 78.40

2025 CVAH(Composite Value Area High): 75.68

Key LIS zone: 73.50-73.15

We anticipate the following scenarios in crude oil:

Scenario 1:

Prices remain elevated as tensions remain high, despite limited retaliation, however, the situation overall now escalated beyond return to diplomacy.

Scenario 2:

Any push towards de-escalation, unlikely in our analysis, but given the headline risk, crude prices may remain volatile and come off the highs.

Given our key LIS (Line in Sand) zone above, we favor longs above this and shorts below this zone.

S&P 500 Daily Chart Analysis For Week of June 20, 2025Technical Analysis and Outlook:

The S&P 500 Index has primarily exhibited downward trends during this week’s abbreviated trading session, narrowly failing to reach the targeted Mean Support level of 5940, as outlined in the previous Daily Chart Analysis. Currently, the index exhibits a bearish trend, suggesting a potential direction toward the Mean Support level of 5940, with an additional critical support level identified at 5888.

Contrariwise, there exists a substantial likelihood that following the accomplishment of hitting the Mean Support of 5940, the index may experience recovery and ascend toward the Mean Resistance level of 6046. This upward movement could facilitate a resilient rally, ultimately topping in the completion of the Outer Index Rally at 6073, thereby enabling the index to address the Key Resistance level situated at 6150.

EUR/USD Daily Chart Analysis For Week of June 20, 2025Technical Analysis and Outlook:

During this week's trading session, the Eurodollar has encountered a significant decline, dipping below the Mean Support level of 1.149; however, it exhibited a modest recovery on Friday. Recent analyses indicate that the Euro is likely to decrease further to the Mean Support level of 1.148, with the potential for extending its bearish trend to reach 1.140. Nevertheless, there remains a possibility that the current recovery will persist, which could result in price movements targeting the Key Resistance level at 1.158 and potentially leading to a retest of the Outer Currency Rally's 1.163 mark.

Bitcoin(BTC/USD) Daily Chart Analysis For Week of June 20, 2025Technical Analysis and Outlook:

In the recent trading session, Bitcoin exhibited an upward trend; however, it subsequently experienced a significant decline from the established Mean Resistance level at 110300. On Friday, Bitcoin exhibited notable price action, characterized by a pump-and-dump scenario. At this juncture, Bitcoin is retracing downwards as it seeks to approach the Mean Support level at 101500 and the ultimate Inner Coin Dip at 96500. It is essential to acknowledge the potential for an upward rally from the Mean Support levels of $101500 and/or the Inner Coin Dip at $96500. Such a rally could culminate in a retest of the Mean Resistance level at $107000.

Rising Geopolitical Tension (Iran Conflict) Signals Market RiskMoving Partially to Cash (VEA, QQQ, TQQQ, SPY, TECL, SOXL)

The global market is entering a high-risk environment. Geopolitical escalation, particularly the growing threat of direct US involvement in a military conflict with Iran, is pushing global uncertainty to new highs. Tensions in the Middle East, rising oil and gold volatility, and increased friction between major world powers all point toward a potential market breakdown. On the chart, VEA ETF is showing signs of topping out within a rising wedge pattern. Meanwhile, institutional funds are starting to reduce exposure to high-risk assets. I'm taking partial profits and shifting to cash across VEA, QQQ, TQQQ, SPY, SOXL, and TECL to preserve gains. Buy-back zones are set around 53.00, 48.00, and 44.00. In an environment of global escalation and rapid risk-off sentiment, active portfolio defense is more important than passive hope.

WTI on high time frame , price reach 60$?

"Hello friends, focusing on WTI, the price is currently in a bullish trend on the daily time frame. During the last NY session, the price swept liquidity in the $66 zone and faced a strong rejection. Considering both technical analysis and fundamental news, I believe the price is gearing up for a decline, with the initial target likely around $60."

If you need further clarification or have more details to discuss, feel free to share!

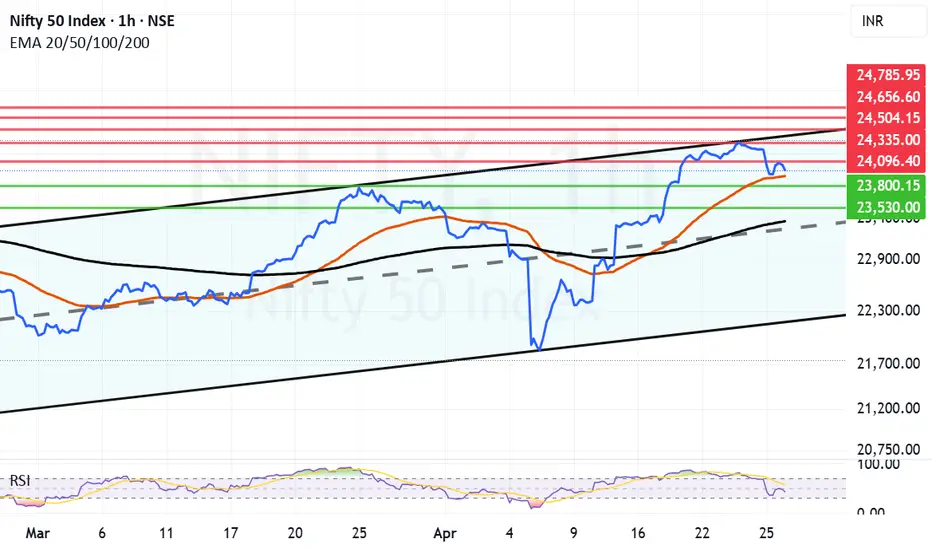

Despite Geo-Political tensions, Nifty closes above Mother line. It was quite remarkable for Nifty to close above the Mother line (50 Hours EMA) despite the Geo-Political tensions and brewing storm of escalations at border. This shows the character of not only Indian market but the resilience of India as a nation. In yesterday's post itself we had mentioned that strong technical resistance has been reached. Add the tension and intent of India to fight against terrorism so it was a perfect recipe for a major fall. Which may happen if things escalate further next week but recovering from 23847 and to close above 24K at 24039 shows that when things will be back to normal the indices will bounce back. Resistance for Nifty now remain at 24096, 24335 and 24504. Supports for Nifty remain at 23914 (Major Mother line support) of 50 Hours EMA, 23800, 23530 and finally 23363.

While Long term players, FII, HNI and DII look at such opportunities to invest for Retail trader it becomes very difficult to control their emotions in such an environment of Geo-political pressure and then we saw a huge fall in the market. The opportunity was seized by both DII and FII with both hands as both turned net buyers for Rs.6492+ Crores. So traders / investors should always avoid knee jerk reactions. Who knows what happens during the weekend the support and resistance levels to watch out for are already mentioned in the message.

Disclaimer: The above information is provided for educational purpose, analysis and paper trading only. Please don't treat this as a buy or sell recommendation for the stock or index. The Techno-Funda analysis is based on data that is more than 3 months old. Supports and Resistances are determined by historic past peaks and Valley in the chart. Many other indicators and patterns like EMA, RSI, MACD, Volumes, Fibonacci, parallel channel etc. use historic data which is 3 months or older cyclical points. There is no guarantee they will work in future as markets are highly volatile and swings in prices are also due to macro and micro factors based on actions taken by the company as well as region and global events. Equity investment is subject to risks. I or my clients or family members might have positions in the stocks that we mention in our educational posts. We will not be responsible for any Profit or loss that may occur due to any financial decision taken based on any data provided in this message. Do consult your investment advisor before taking any financial decisions. Stop losses should be an important part of any investment in equity.

XOM Analysis: Oil's Next Move & Policy ShiftsNYSE:XOM currently piques my interest, particularly with oil prices potentially stabilizing or rising further. Recent geopolitical developments and policy shifts under Trump’s administration—such as rolling back Biden-era energy regulations, reducing methane fees, and easing LNG export permits—could significantly influence the energy landscape.

My intuition suggests Trump’s "Mar-a-Lago Accord" might involve major global economies reducing holdings of US dollar assets, swapping short-term treasuries for century bonds. Such currency shifts and reduced drilling activity could lead to a tighter oil supply, benefiting prices. Additionally, a weakening US dollar could positively impact technology stocks, as investors rotate towards sectors less affected by traditional commodities.

Technical Analysis (Daily & Hourly Chart)

Current Price: Approximately $103.00

Key Resistance Levels:

Immediate resistance: $103.93 (L.Vol ST 1b)

Important resistance zone: $104.74 (118 AVWAP)

Critical resistance (Last week's high): ~$106.46

Key Support Levels:

Near-term support: $101.13 (Weeks Low Long)

Major support: $97.92 (Best Price Short)

Trading Scenarios

Bullish Scenario (Continued oil strength & supportive policy shifts):

Entry Trigger: Sustained breakout and close above immediate resistance at $103.93.

Profit Targets:

Target 1: $104.74 (AVWAP resistance)

Target 2: $106.46 (recent swing high)

Stop Loss: Below recent pivot around $101.00, limiting risk effectively.

Bearish Scenario (Oil price weakness or production surge):

Entry Trigger: Failure to sustain the above resistance at $103.93 or a breakdown below near-term support at $101.13.

Profit Targets:

Target 1: $99.00 (psychological & short-term support)

Target 2: $97.92 (strong support, ideal short target)

Stop Loss: Above $104.75 to control risk in case of a reversal.

Thought Process & Final Thoughts

Given the current geopolitical and regulatory environment, XOM appears poised for potential upside if oil prices remain strong and policy shifts materialize. However, caution is warranted, as oil companies seem hesitant to increase production due to profitability concerns. Clearly defined technical levels will help navigate trade entries and exits effectively around these evolving macroeconomic conditions.

Earnings Date: May 2nd—Keep positions nimble as earnings can significantly impact short-term volatility.

Is Erdogan’s Gambit Destabilizing Turkey’s Future?Erdogan’s administration continues to engage in high-stakes geopolitical maneuvers by maintaining direct and indirect ties with groups designated as terrorist organizations. His government’s strategic alliances, notably with Hayat Tahrir al-Sham (HTS), serve immediate military and political goals in Syria, despite significant international controversy and longstanding terrorist designations by the U.S. and other global actors.

This risky strategy has had a pronounced impact on the Turkish economy. Investors have increasingly shifted their capital from the Turkish Lira to the U.S. dollar, leading to a notable rise in the USD/TRY rate. Fears of further economic isolation and the looming threat of sanctions—which could cut off Turkey from critical European banking and trade services—have only intensified market instability.

The growing strains within NATO and shifting regional alliances are compounding these economic challenges. Erdogan’s pragmatic yet contentious foreign policy raises serious questions about Turkey’s future role within the alliance, as Western partners deliberate potential sanctions and other measures. Meanwhile, evolving dynamics with regional powers such as Russia and Iran add further uncertainty to Turkey’s strategic position and economic prospects.

Is Apple's Empire Built on Sand?Apple Inc., a tech titan valued at over $2 trillion, has built its empire on innovation and ruthless efficiency. Yet, beneath this dominance lies a startling vulnerability: an overreliance on Taiwan Semiconductor Manufacturing Company (TSMC) for its cutting-edge chips. This dependence on a single supplier in a geopolitically sensitive region exposes Apple to profound risks. While Apple’s strategy has fueled its meteoric rise, it has also concentrated its fate in one precarious basket—Taiwan. As the world watches, the question looms: what happens if that basket breaks?

Taiwan’s uncertain future under China’s shadow amplifies these risks. If China moves to annex Taiwan, TSMC’s operations could halt overnight, crippling Apple’s ability to produce its devices. Apple’s failure to diversify its supplier base left its trillion-dollar empire on a fragile foundation. Meanwhile, TSMC’s attempts to hedge by opening U.S. factories introduce new complications. If Taiwan falls, the U.S. could seize these assets, potentially handing them to competitors like Intel. This raises unsettling questions: Who truly controls the future of these factories? And what becomes of TSMC’s investments if they fuel a rival’s ascent?

Apple’s predicament is a microcosm of a global tech industry tethered to concentrated semiconductor production. Efforts to shift manufacturing to India or Vietnam pale against China’s scale, while U.S. regulatory scrutiny—like the Department of Justice’s probe into Apple’s market dominance—adds further pressure. The U.S. CHIPS Act seeks to revive domestic manufacturing, but Apple’s grip on TSMC muddies the path forward. The stakes are clear: resilience must now trump efficiency, or the entire ecosystem risks collapse.

As Apple stands at this crossroads, the question echoes: Can it forge a more adaptable future, or will its empire crumble under the weight of its design? The answer may not only redefine Apple but also reshape the global balance of tech and power. What would it mean for us all if the chips—both literal and figurative—stopped falling into place?

Will Russia’s New Dawn Reshape Global Finance?As the Russo-Ukrainian War edges toward a hypothetical resolution, Russia stands poised for an economic renaissance that could redefine its place in the global arena. Retaining control over resource-laden regions like Crimea and Donbas, Russia secures access to coal, natural gas, and vital maritime routes—assets that promise a surge in national wealth. The potential lifting of U.S. sanctions further amplifies this prospect, reconnecting Russian enterprises to international markets and unleashing energy exports. Yet, this resurgence is shadowed by complexity: Russian oligarchs, architects of influence, are primed to extend their reach into these territories, striking resource deals with the U.S. at mutually beneficial rates. This presents a tantalizing yet treacherous frontier for investors—where opportunity dances with ethical and geopolitical uncertainties.

The implications ripple outward, poised to recalibrate global economic currents. Lower commodity prices could ease inflationary pressures in the West, offering relief to consumers while challenging energy titans like Saudi Arabia and Canada to adapt. Foreign investors might find allure in Russia’s undervalued assets and a strengthening ruble, but caution is paramount. The oligarchs’ deft maneuvering—exploiting political leverage to secure advantageous contracts—casts an enigmatic shadow over this revival. Their pragmatic pivot toward U.S. partnerships hints at a new economic pragmatism, yet it prompts a deeper question: Can such arrangements endure, and at what cost to global stability? The stakes are high, and the outcomes remain tantalizingly uncertain.

This unfolding scenario challenges us to ponder the broader horizon. How will investors weigh the promise of profit against the moral quandaries of engaging with a resurgent Russia? What might the global financial order become if Russia’s economic ascent gains momentum? The answers elude easy resolution, but the potential is undeniable—Russia’s trajectory could anchor or upend markets, depending on the world’s response. Herein lies the inspiration and the test: to navigate this landscape demands not just foresight, but a bold reckoning with the interplay of economics, ethics, and power.

Could One Event Propel Gold to $6,000?Gold has long been a refuge in times of crisis, but could it be on the brink of an unprecedented surge? Analysts now predict the precious metal could reach $6,000 per ounce, driven by a potent mix of geopolitical instability, macroeconomic shifts, and strategic accumulation by central banks. The prospect of a Chinese invasion of Taiwan, a major global flashpoint, could be the catalyst that reshapes the financial landscape, sending investors scrambling for safe-haven assets.

The looming threat of conflict in Taiwan presents an unparalleled risk to global supply chains, particularly in semiconductor production. A disruption in this critical sector could spark widespread economic turmoil, fueling inflationary pressures and eroding confidence in fiat currencies. As nations brace for potential upheaval, central banks and investors are increasingly turning to gold, reinforcing its role as a geopolitical hedge. Meanwhile, de-dollarization efforts by BRICS nations further elevate gold’s strategic importance, intensifying its upward trajectory.

Beyond geopolitical risks, macroeconomic forces add momentum to gold’s ascent. The U.S. Federal Reserve’s anticipated rate cuts, persistent inflation, and record national debt levels all contribute to a weakening dollar. This, in turn, makes gold more attractive to global buyers, accelerating demand. At the same time, the psychological factor—fear-driven safe-haven buying and speculative enthusiasm—creates a self-reinforcing cycle, pushing prices ever higher.

Despite counterforces such as potential Fed policy shifts or a temporary easing of geopolitical tensions, the weight of uncertainty appears overwhelming. The convergence of economic instability, shifting power dynamics, and investor sentiment suggest that gold’s march toward $6,000 is less a speculative fantasy and more an inevitable financial reality. As the world teeters on the edge of historic change, gold may well be the ultimate safeguard in an era of global upheaval.

Could Silver's Price Soar to New Heights?In the realm of precious metals, silver has long captivated investors with its volatility and dual role as both an industrial staple and a safe-haven asset. Recent analyses suggest that the price of silver might skyrocket to unprecedented levels, potentially reaching $100 per ounce. This speculation isn't just idle talk; it's fueled by a complex interplay of market forces, geopolitical tensions, and industrial demand that could reshape the silver market landscape.

The historical performance of silver provides a backdrop for these predictions. After a notable surge in 2020 and a peak in May 2024, silver's price has been influenced by investor sentiment and fundamental market shifts. Keith Neumeyer of First Majestic Silver has been an outspoken advocate for silver's potential, citing historical cycles and current supply-demand dynamics as indicators of future price increases. His foresight, discussed across various platforms, underscores the metal's potential to break through traditional price ceilings.

Geopolitical risks add another layer of complexity to silver's valuation. The potential for an embargo due to escalating tensions between China and Taiwan could disrupt global supply chains, particularly in industries heavily reliant on silver like technology and manufacturing. Such disruptions might not only increase the price due to supply constraints but also elevate silver's status as a safe-haven investment during times of economic uncertainty. Moreover, the ongoing demand from sectors like renewable energy, electronics, and health applications continues to press against the available supply, setting the stage for a significant price rally if these trends intensify.

However, while the scenario of silver reaching $100 per ounce is enticing, it hinges on numerous variables aligning perfectly. Investors must consider not only the positive drivers but also factors like market manipulation, economic policies, and historical resistance levels that have previously capped silver's price growth. Thus, while the future of silver holds immense promise, it also demands a strategic approach from those looking to capitalize on its potential. This situation challenges investors to think critically about market dynamics, urging a blend of optimism with strategic caution.

Is Gold the Ultimate Safe Haven in 2025?In the labyrinthine world of finance, gold has once again captured the spotlight, breaking records as speculative buying and geopolitical tensions weave a complex narrative around its valuation. The precious metal's price surge is not merely a reaction to market trends but a profound statement on the global economic landscape. Investors are increasingly viewing gold as a beacon of stability amidst an ocean of uncertainty, driven by the Middle East's ongoing unrest and the strategic maneuvers of central banks. This phenomenon challenges us to reconsider the traditional roles of investment assets in safeguarding wealth against international volatility.

The inauguration of Donald Trump as President has injected further intrigue into the gold market. His administration's initial steps, notably the delay in imposing aggressive tariffs, have led to a nuanced dance between inflation expectations and U.S. dollar strength. Analysts from major financial institutions like Goldman Sachs and Morgan Stanley are now dissecting how Trump's policies might steer inflation, influence Federal Reserve actions, and ultimately, dictate gold's trajectory. This intersection of policy and market dynamics invites investors to think critically about how political decisions can reshape economic landscapes.

China's burgeoning appetite for gold, exemplified by the frenzied trading of gold-related ETFs, underscores a broader shift towards commodities as traditional investment avenues like real estate falter. The Chinese central bank's consistent gold acquisitions reflect a strategic move towards diversifying reserves away from the U.S. dollar, particularly in light of global economic sanctions. This strategic pivot in one of the world's largest economies poses a compelling question: are we witnessing a fundamental realignment in global financial power structures, with gold at its core?

As we navigate through 2025, gold's role transcends simple investment; it becomes a narrative of economic resilience and geopolitical foresight. The interplay between inflation, monetary policy, and international relations not only affects gold's price but also challenges investors to adapt their strategies in an ever-evolving market. Can gold maintain its luster as the ultimate Safe Haven, or will new economic paradigms shift its golden allure? This enigma invites us to delve deeper into the metal's historical significance and its future in a world where certainty is a luxury few can afford.

Can the Yuan Dance to a New Tune?In the intricate ballet of global finance, the Chinese yuan performs a delicate maneuver. As Donald Trump's presidency introduces new variables with potential tariff hikes, the yuan faces depreciation pressures against a strengthening U.S. dollar. This dynamic challenges Beijing's economic strategists, who must balance the benefits of a weaker currency for exports against the risks of domestic economic instability and inflation.

The People's Bank of China (PBOC) is navigating this complex scenario with a focus on maintaining currency stability rather than aggressively stimulating growth through monetary policy easing. This cautious approach reflects a broader strategy to manage expectations and market reactions in an era where geopolitical shifts could dictate economic outcomes. The PBOC's recent moves, like suspending bond purchases and issuing warnings against speculative trades, illustrate a proactive stance in controlling the yuan's descent, aiming for an orderly adjustment rather than a chaotic fall.

This situation provokes thought on the resilience and adaptability of China's economic framework. How will Beijing reconcile its growth ambitions with the currency's stability, especially under the looming shadow of U.S. trade policies? The interplay between these two economic giants will shape their bilateral relations and influence global trade patterns, investment flows, and perhaps even the future of monetary policy worldwide. As we watch this economic dance unfold, one must ponder the implications for international markets and the strategic responses from other global players.

Will History Repeat as Major Currencies Dance Toward Parity?In a dramatic shift that has captured the attention of global financial markets, the euro-dollar relationship stands at a historic crossroads, with leading institutions forecasting potential parity by 2025. This seismic development, triggered by Donald Trump's November election victory and amplified by mounting geopolitical tensions, signals more than just a currency fluctuation—it represents a fundamental realignment of global financial power dynamics.

The confluence of diverging monetary policies between the U.S. and Europe and persistent economic challenges in Germany's industrial heartland has created a perfect storm in currency markets. European policymakers face the delicate task of maintaining supportive measures. At the same time, their American counterparts adopt a more cautious stance, setting the stage for what could become a defining moment in modern financial history.

This potential currency convergence carries implications far beyond trading desks. It challenges traditional assumptions about economic power structures and reevaluates global investment strategies. As geopolitical tensions escalate and economic indicators paint an increasingly complex picture, market participants must navigate a landscape where historical precedents offer limited guidance. The journey toward potential parity serves as a compelling reminder that in today's interconnected financial world, currency movements reflect not just economic fundamentals but the broader forces reshaping our global order.

Conclusion

The current landscape presents unprecedented challenges for the EUR/USD pair, driven by economic fundamentals and geopolitical tensions. One significant concern is the potential release of sensitive footage from Israel (by the Israeli National Security Agency (NSA) from Hamas body cameras, containing graphic atrocities from the October 7th incident.), which could threaten European stability. These developments go beyond simple market dynamics and have the potential to reshape the social and political fabric of Europe.

Market professionals emphasize the importance of adaptable strategies and the vigilant monitoring of key indicators. Investors must prepare for increased volatility while maintaining strong risk management frameworks. The pressure on the euro-dollar relationship is likely to persist, making strategic positioning and careful market analysis more crucial than ever in navigating these turbulent waters.

Will Europe's Gas Gambit Reshape the Global Energy Landscape?In a bold move reverberating across global energy markets, Ukraine's decision to halt Russian gas transit on New Year's Day 2025 has ushered in a new era of energy geopolitics. This watershed moment not only challenges decades-old supply patterns but also tests Europe's resilience and strategic foresight in securing its energy future. The immediate market response, with gas prices surging to levels unseen since late 2023, underscores the significance of this pivotal shift.

Against this backdrop of uncertainty, Norway's Troll field has emerged as a beacon of hope, setting unprecedented production records and demonstrating Europe's capacity for strategic adaptation. With production reaching 42.5 billion standard cubic meters in 2024, this achievement showcases how technological innovation and operational excellence can help reshape traditional energy dependencies. Meanwhile, BMI's forecast of a 40% price increase for 2025 signals the complex interplay between supply disruptions, growing demand, and market expectations.

The transformation of Europe's energy landscape extends beyond mere supply chain reorganization. While countries like Slovakia, Austria, and Moldova face immediate challenges in securing alternative gas sources, the broader European response highlights a remarkable shift in energy security strategy. With storage facilities maintaining robust levels and infrastructure upgrades underway, Europe's energy transition demonstrates how geopolitical challenges can catalyze innovation and strategic resilience in the global energy sector.

Will Iran's Nuclear Ambitions Redefine Global Energy Markets?In a world where geopolitical tensions and energy markets dance an intricate waltz, the latest developments surrounding Iran's nuclear program have emerged as a pivotal factor in global oil dynamics. The Biden administration's deliberation of military options against Iranian atomic facilities has introduced a new variable into the complex equation of international energy markets, forcing investors and analysts to reassess their traditional market models.

The strategic significance of the Middle East's oil infrastructure, particularly the Strait of Hormuz, hangs in delicate balance as diplomatic chess moves unfold. With approximately one-fifth of the world's oil supply flowing through this crucial chokepoint, the stakes extend far beyond regional politics, touching every corner of the global economy. Market participants have begun incorporating these heightened risks into their pricing models, reflecting a new reality where geopolitical considerations carry as much weight as traditional supply and demand metrics.

The energy sector stands at a crossroads where strategic petroleum reserves, investment strategies, and risk management protocols face unprecedented challenges. Portfolio managers and energy traders must navigate this complex landscape while balancing short-term volatility against long-term strategic positioning. As the situation continues to evolve, the global oil market serves as a mirror reflecting the broader implications of international security dynamics, challenging conventional wisdom about energy market fundamentals and forcing a reevaluation of traditional risk assessment models.

Fundamental Analysis of EURUSDEURUSD is trading in the support area which has been respected by the price action since December of 2022. Similarly, there is an area of resistance.

There are two scenarios based on the current geopolitical tension and the policy of the new administration in the US.

Scenario#1: Risk OFF or USD depreciates against EUR and other currency pairs

The new US administration will take charge in Jan 2025, and by that time if the Scenario#2 has not happened then the EUR should appreciate significantly against USD. The new administration is expected to be business friendly. The US economy should get an ultra-boost because of lower taxes and less regulations.

There are many other promises made by the winning party like the increase in import tariffs on all the countries, deportation etc., maybe those promises were to attract voters. We don't know how it will play out, so we go with the simple approach that republican party means less regulation, hence business friendly.

Scenario#2: Risk ON or USD appreciates against EUR and other currency pairs

This scenario could play out even before the new administration takes charge!!! We don't know if it is a bluff from Russia or a real threat, but the fear of nuclear war can be frightening. Whenever there are major escalations in the world, the USD appreciates and that is as simple as 1 + 1 = 2, right?

Could South Korea's Currency Crisis Signal a New Economic ParadiIn a dramatic turn of events that echoes the turbulence of 2009, the South Korean won has plummeted to historic lows, breaching the critical KRW1,450 threshold against the US dollar. This seismic shift in currency markets isn't merely a numerical milestone—it represents a complex interplay of global monetary policy shifts and domestic political dynamics that could reshape our understanding of emerging market vulnerabilities in an interconnected world.

The Federal Reserve's recent "hawkish cut" has created a fascinating paradox: while lowering rates, it simultaneously signaled a more conservative approach to future reductions than markets anticipated. This nuanced stance, combined with South Korea's domestic political turbulence following President Yoon Suk Yeol's brief martial law declaration, has created a perfect storm that challenges conventional wisdom about currency stability in advanced emerging economies. The won's position as this year's worst-performing emerging Asian currency raises profound questions about the resilience of regional economic frameworks in the face of complex global pressures.

What makes this situation particularly intriguing is the response from South Korean authorities, who have deployed sophisticated market stabilization measures, including an expanded foreign exchange swap line of $65 billion with the National Pension Service. This adaptive response showcases how modern economic management requires increasingly creative solutions to maintain stability in an era where traditional monetary policy tools may no longer suffice. As markets digest these developments, the situation is a compelling case study of how developed economies navigate the delicate balance between market forces and regulatory intervention in an increasingly unpredictable global financial landscape.

Bearish on CrudeOilA very short post 😁

I just wanted to let you know, based on my technical analysis I see $62 to $63.5 an area that Crude Oil probably see in the near future. Then it has the potential to go towards $57.

That's it 😉

Cheers 🍻

Can Political Tremors Rewrite Global Financial Markets?In the intricate dance of global finance, South Korea's recent political upheaval serves as a compelling microcosm of how geopolitical dynamics can instantaneously transform economic landscapes. The Kospi Index's dramatic 2% plunge following President Yoon Suk-yeol's fleeting martial law declaration reveals a profound truth: financial markets are not merely numerical abstractions, but living, breathing ecosystems acutely sensitive to political breath.

Beyond the immediate market turbulence lies a deeper narrative of institutional resilience and adaptive governance. The swift parliamentary intervention, coupled with the Bank of Korea's strategic liquidity injections, demonstrates a remarkable capacity to pivot and stabilize in moments of potential systemic risk. This episode transcends South Korea's borders, offering global investors a masterclass in crisis management and the delicate art of maintaining economic equilibrium amid political uncertainty.

The broader implications are both provocative and instructive. As heavyweight corporations like Samsung Electronics and Hyundai Motors experienced significant share price fluctuations, the event underscores an increasingly interconnected global financial system where local political tremors can rapidly cascade into international market movements. For forward-thinking investors and policymakers, this moment represents more than a crisis—it's an invitation to reimagine risk, resilience, and the complex interdependencies that define our modern economic reality.