and finally reached it...For some time the price moved towards resistance and finally reached it. I expect a rebound from the level to the support area.

wait and see, maybe long?A triangle appeared. What does it mean? We have to wait and see, maybe long?

Elon Musk, what do you think?Tesla shares have been in a bearish trend for several days. Perhaps the reason is in Elon Musk, what do you think? Waiting for the bounce and fall

Maybe the bulls still have strength?A triangle appeared on the chart. Given the previous trend, where will the price go? Maybe the bulls still have strength?

Is this home?The third top has formed on the chart. The support line is the next target. Is this home?

rise above the maximum again?Tesla has dropped significantly over the past few weeks. Is it possible to rise above the maximum again? Or will we fall even lower?

Is that a short? Or ...We are still waiting for the breakout of resistance and further downward movement. Is that a short? Or ...

Is that short? What do you think?A double top has formed. There is a possibility of a fall below the neckline, possibly even to support. What do you think?

TESLA still bearishThe upside is still bearish, although there is a slight correction. I expect further drop to support.

short zoneApple is still in the short zone. I look forward to a fall after a slight correction. What do you think?

Will there be further growth?AMD has been in an upward trend for a long time. The price corrected to 140, as we expected. Will there be further growth?

up to ...BABA finished the second wave (correctional) and is now forming the third (impulse). I expect further take-off up to $ 120

long shadow upThere is a good signal - a long shadow up, which confirms our short attitude. What do you think?

Or is it too early for a short?it looks like the price has approached the resistance zone and the third wave will start forming soon. Or is it too early for a short?

good sign for a shortthe price has formed two tops. The second peak below the first is a good sign for a short. What do you think?

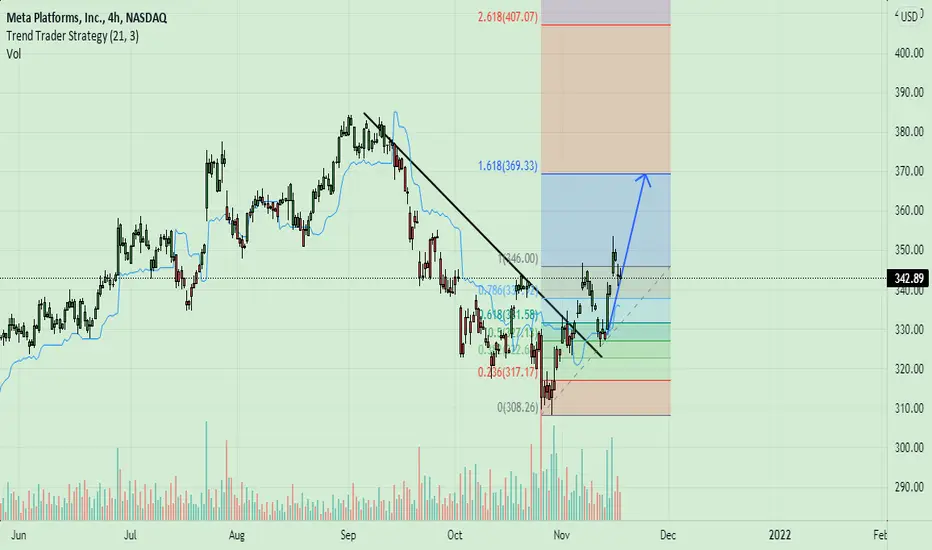

facebook started growingfacebook started growing. Exited the downtrend. a correction is being formed up to the support line.

The fall is near ...The price stopped at the resistance. A candlestick with a long upward shadow has formed - a signal that the bulls cannot gain a foothold higher. The fall is near ...

fall to 130?Perhaps this is the beginning of the fall to 130. The price cannot reach the previous high. What do you think will happen?

rise or fall soon?Amazon is closing the gap that was a few days ago. What will happen next? Continued rise or fall soon?

Is that short? Or....Apple entered a downtrend. at the moment there are reasons for short positions. there are several supports ahead that the price can go through. What do you think?

below the supportthe second (corrective) wave is forming on the chart, after which the third (impulsive) wave is expected. I expect an imminent fall below the support

fall to 138The downtrend continues, a correction to resistance is possible, after which I expect a fall to 138