World Liberty Financial STABLECOIN | Everything YOU Need to KnowWorld Liberty Financial (WLFI), a DeFi lending protocol launched in 2024 and notably associated with the Trump family, is currently executing a key operational test for its new stablecoin, USD1.

This U.S. dollar-pegged stablecoin was introduced in March 2025 and backed by Treasuries and cash equivalents. It has already seen rapid adoption, surpassing $2.1 billion in circulation.

To validate their on-chain distribution systems ahead of a wider rollout, WLFI is conducting a test airdrop, proposing to send a small and fixed amount of USD1 to all existing $WLFI token holders on the Ethereum Mainnet. A governance vote on this proposal, set to conclude this Wednesday, May 14th shows overwhelming community support, with over 99.9% approval which is signalling confidence in the initiative's technical goals and community reward aspect.

Investors should note that while the vote seems assured, critical details like the exact USD1 amount per wallet and the precise airdrop date are yet to be announced, pending the vote's finalization. Also, WLFI retains discretion to modify or cancel this test distribution. This operational step occurs against a backdrop of significant scrutiny surrounding WLFI, stemming from its high-profile political connections, reported investigations, and potential conflicts of interest highlighted in various media outlet.

this test airdrop represents a practical infrastructure check and a community engagement tactic for WLFI as it builds out the ecosystem for its rapidly growing USD1 stablecoin. For current $WLFI holders, it presents a small token distribution contingent on final details announced after May 14th. For prospective investors, it's an operational milestone to observe, weighing the technical progress and market adoption of USD1 against the unique regulatory and political risks associated with the World Liberty Financial project.

____________

BYBIT:WLFUSDT

Growth

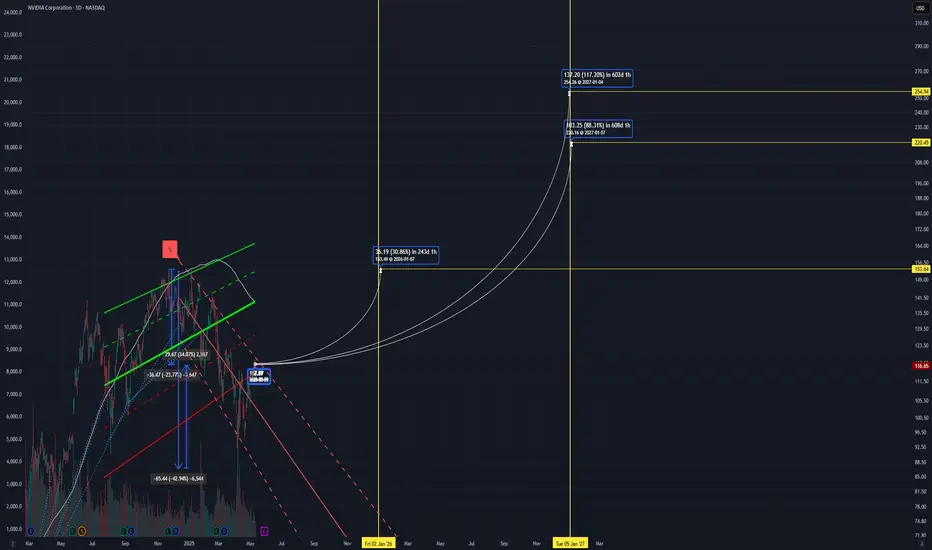

"God of AI" How does Nvidia make money?"God of AI" How does Nvidia make money?

NVIDIA is really at the center of the AI and data center boom right now. With these industries growing so quickly, it looks like NVIDIA’s sales and profits will keep going up for quite some time. Some experts even predict that by 2029, the company could be making over $300 billion just from its data center business.

What’s also impressive is how NVIDIA keeps rolling out new and better AI chips, staying ahead of the competition when it comes to technology. And they’re not just sticking to AI-they’re also moving into exciting areas like self-driving cars, the cloud, robotics, and even the metaverse. This kind of diversification gives them even mo NASDAQ:NVDA re ways to grow.

As for the stock price, most analysts seem to agree that there’s still a lot of potential for it to climb higher, even though there are some risks to watch out for-like increased competition, supply chain hiccups, or short-term market swings.

NASDAQ:NVDA

Base Case Costco 810. Total company revenues were up 6% compared to a year ago. The Profit Margin of 2.9% was better than the longer-term average of 2.5%. A 90x multiple applied to a Sales Growth Rate of 9% would imply a share price 810. Costco's narrative revolves around execution. Considering the company continues to execute and deliver top-line growth, the stock will be rewarded in some form.

WEX Inc | WEX | Long at $180.00NYSE:WEX Inc has a 40.8M float and recently initiated a $300 million share buyback. The stock has been in consolidation mode for some time and is playing "nicely" along my selected historical simple moving average (SMA). Recently, it may have double-bottomed off this SMA and, given the buyback, may move progressively up toward the $230's where there is a large price gap on the daily chart. It is currently in a personal buy zone at $180.00.

Target #1 = $209.00

Target #2 = $231.00

Wow, Id be dumping my life savings into this.First target is $25 and the $30 once we start to see price move closer to its volume profile gap down at my pink lines.

The key price level I see for support is 12.62$ but honestly, this looks like it could rip any day now.

Im longing until we break below $12

STOCKS | MARKET WATCH | Why Long-Term Investing Still Wins🤯 The start of 2025 was a bit of a rollercoaster for stocks.

Global markets got seriously rattled in the first few months by some sudden jitters. When President Trump announced those aggressive tariffs, it caused significant concern among investors, sending stock markets tumbling and prompting a flight to safety. Like Reuters said, April was "epic" for crazy market swings – the VIX fear index shot up to levels we hadn't seen since 2020 and 2008, and then just as quickly dropped back down. Markets went wild.

But then, by late April, the panic kind of ... disappeared. Once President Trump paused the implementation of the most severe tariffs, stocks bounced back pretty sharply. The S&P 500 recovered most of what it lost. After that nasty drop, it ended April only about 5% lower than it started the year. The Nasdaq, with all its tech stocks, pretty much ended the month where it began. So, after all that drama, major US stock markets weren't far from their all-time highs, showing how fast that "fear" can vanish.

📊 How key indexes did

S&P 500 (USA): 📉 Dipped in early April but bounced back late. Ended April around -5% for the year, after almost hitting a bear market.

Nasdaq Composite (USA): 📉 Similar story. Tanked on the tariff scare, then rallied when things calmed down, ending April pretty much flat for the year.

MSCI World (Global developed markets): 🤷♂️ Had its ups and downs along with the US markets. By the end of April, it was pretty much flat for the year – no big moves for the overall world index.

MSCI Emerging Markets: 📉 Didn't do as well as developed markets. Asian stocks, especially, took a hit early April because of trade war worries, so this index lagged, even though it recovered a bit by the end of the month.

FTSE/JSE All-Share (South Africa): 🇿🇦 The odd one out! The JSE jumped about +5% in the first three months of 2025, mainly thanks to mining stocks. It even hit a record high in March. The April craziness shook it up too, but because it did so well earlier, it was still slightly up for the year by late April.

Takeaway? Global stocks were jumpy, but they mostly recovered. By late April, most major indexes were close to where they started the year. South Africa's market was the exception, having a good first quarter that helped it weather the April storm.

⏳ Staying invested beats trying to be a stock Wizard

All this back and forth can make investors nervous. You start thinking, "Should I just sell now before it drops even more?" But history usually says that's the wrong move. Just sticking with it usually works out better than trying to guess the market's next move. BlackRock's iShares recently pointed out that "waiting for the 'right time' to invest might mean missing out on the best days," while staying invested lets you benefit from that "compounding" thing and get through the short-term bumps. Simply put, if you sit on the sidelines during big swings, you often miss the big rebound days. One study even showed that if you missed just the five best market days over 20 years, you'd end up with way less money than someone who just stayed in the market.

The legendary investor Charlie Munger put it simply: "The first rule of compounding: never interrupt it unnecessarily." Trying to jump in and out of the market around all the volatility is super tough – the biggest up days often follow right after the biggest down days. On the other hand, patient investors who just ride out the noise tend to grab more of those long-term gains. After all, with compounding, those small gains build on each other over time.

💰 The awesome power of compounding over time

Compounding basically means the sooner you invest and the longer you stay invested, the more your returns build on each other like a snowball rolling downhill. For example, the total return JSE All-Share index was up almost 23% over the last year. That kind of gain shows how just staying invested during good times can really grow your wealth. If you'd panicked and pulled out, you would have missed most of that growth. Over longer periods, like 5 to 10 years, the JSE has almost always gone up. The big lesson is that it's about "time in the market," not trying to "time the market," that really makes your returns grow and smooths out those bumps along the way.

🌍 What's driving the markets and the economy

There were a few big things happening that explain why the markets moved the way they did.

🇺🇸 US GDP Slowdown: The US economy actually shrank a bit in the first quarter of 2025. A lot of people blamed this on a big surge in imports as businesses bought stuff ahead of those potential President Trump tariffs. Even though this news spooked the stock market briefly in late April, underlying consumer spending was still looking pretty decent.

📈 US Company Profits: On the bright side, US companies reported some pretty strong profits. Analysts were expecting good growth in earnings for the S&P 500 in the first quarter, even with the economic slowdown. And it turned out even better – a lot of companies beat expectations, and overall earnings were up quite a bit from last year. This helped keep stock prices from falling too much during the pullbacks.

🇪🇺 European Spending Boost: In Europe, governments are starting to spend more. Germany, for example, proposed a huge fund for infrastructure and energy. The EU is also loosening its spending rules and increasing defense budgets. Some experts think this could actually boost Europe's economic growth a bit each year, which would mean better profits for European companies. Some even think European companies might see faster profit growth than US companies in the next few years because of this spending.

🇨🇳 Asia and Trade Wars: Asia was the weak spot. China's economy showed some signs of trouble, with a survey suggesting its manufacturing activity might have shrunk in April after a couple of months of growth. This seemed to be a direct result of the US tariffs. Asian stock markets took a hit on the tariff news, which dragged down the overall emerging markets index. Basically, tariffs and trade tensions hurt growth in Asia and its markets, which then affected returns in emerging markets globally.

✅ The bottom line

Early 2025 reminded us that markets can freak out quickly – but they can often bounce back just as fast. The swings felt scary, but history tells us that just sticking with your investments usually pays off. Major stock markets are pretty much where they were a few months ago, while economies and company earnings are still moving forward. For long-term investors, that wild week in April just reinforced an old lesson: stay invested and let compounding do its thing. As some experts say, "get invested and stay invested" because the most volatile times often have the biggest market gains. By sticking to your plan, you avoid missing those big up days when the "fear" fades and markets recover.

_________________________

SP:SPX

Sources: Recent market reports and data including the April SATRIX 2025 market newsletter “Once Again, Volatility Blinked and Fear Lost., nasdaq.com, reuters.com, ishares.com, insight.factset.com, reuters.com, iol.co.za

About to go nuclear pt 2Seems consolidation is coming to an end. 4 hr is set up for bulls to take the move before earnings on the 15th. Easy beat for them with likely more good news to be announced. Also kulr has been buying btc which is currently breaking out I'm sure they will ride with the hype. Looking to move through 1.50 and flip $2 with some decent volume for continuation. Possible it just continues sideways of course with strong support for buying at $1

UNH....OVERSOLD......REVERSAL SOON?UNH testing third support touch at ~$394, with RSI near 30 on the weekly, signaling potential oversold conditions. Despite a tough Q1 with 4% EPS growth and rising medical costs, UNH boasts 10% revenue growth, a 2.08% dividend yield, and a massive 51M member base. Is this a dip to buy?

NATRIUM | Investing | Why BILL GATES is Betting on NATRIUMBill Gates is betting big on Natrium - should you be, too?

Natrium is this next-generation nuclear reactor design that's attracting a lot of attention from people like Bill Gates and other major investors. What's particularly interesting about it is that it combines a fast reactor with a built-in molten salt "battery." Essentially, it can generate a steady output of power and then provide an extra boost during peak demand by drawing on its stored heat. This design aims for greater flexibility in meeting fluctuating electricity needs.

The technology is a joint development by TerraPower, the company co-founded by Bill Gates, and GE Hitachi. They're presenting it as a zero-carbon power source capable of reliably backing up intermittent renewables like wind and solar, ensuring a consistent supply of clean energy.

The excitement from investors like Bill Gates appears to be driven by the need to address climate change and secure reliable energy supplies. They view Natrium as a way to deliver large-scale, carbon-free power while potentially overcoming some of the limitations of older nuclear reactor designs. Gates has emphasized the enhanced safety features and potential for lower operating costs. Furthermore, Natrium's specific design to complement the intermittency of solar and wind, through its energy storage, is a significant draw for investors looking at future energy solutions. The substantial public and private investment, including government funding and bipartisan legislative support, also signals strong confidence in this technology.

The description of TerraPower as a "Bill Gates-backed" firm developing this multi-billion dollar demonstration plant highlights the high-profile nature of the project. The fact that corporate partners, such as the data center company exploring Natrium for their power needs, are also getting involved indicates a broader recognition of its potential beyond just government initiatives.

Compared to traditional nuclear reactors, Natrium offers some potential advantages. Its sodium coolant operates at near-atmospheric pressure, simplifying safety compared to the high-pressure water systems in older designs. This allows for natural heat dissipation in case of issues, reducing the risk of large steam explosions. Another key aspect is Natrium's potential for more efficient fuel utilization and reduced long-lived waste generation. The design aims for better fuel efficiency and a smaller volume of long-term radioactive waste compared to current light-water reactors.

Natrium's primary advantage over wind and solar is its dispatchability. Unlike the intermittent nature of renewables, Natrium can provide power consistently, 24/7. The integrated energy storage allows it to complement renewables by absorbing excess energy or releasing power during periods of low renewable output. This firm grid support is a significant benefit for utilities concerned about grid stability and the variability of renewable sources.

For utilities transitioning away from coal, Natrium offers a carbon-free, relatively direct replacement in terms of power output. It also has a smaller land footprint compared to large-scale wind or solar installations.

There are inherent challenges with a first-of-a-kind system like Natrium. The prototype is still under construction, lacking a proven operational track record. Construction and licensing processes could face delays and cost overruns. Critics also raise valid points about the actual safety and cost-effectiveness compared to projections. The use of sodium coolant, while offering safety advantages, also presents risks due to its reactivity with air and water, requiring robust containment systems. Regulatory scrutiny will undoubtedly be extensive.

And fuel supply is a critical uncertainty. Natrium requires high-assay, low-enriched uranium (HALEU), which is not currently widely available. Disruptions in the supply chain and limited existing production capacity pose a significant risk to the timely and cost-effective operation of Natrium plants.

Looking ahead, Natrium is being considered for deployment in regions needing reliable power to complement renewables and to power energy-intensive industries. The long-term vision involves integrating Natrium with renewable energy sources to create a more stable and decarbonized grid.

The speculative outlook for Natrium in the next 5-10 years is heavily dependent on the successful completion of the Wyoming demonstration plant. If it meets its targets, it could pave the way for wider adoption. However, the timeline is ambitious, and challenges related to fuel supply and regulatory approvals remain. A successful demonstration could trigger significant investment and adoption in the coming decades, positioning Natrium as a key player in the energy transition.

If you're interested in investing in companies involved with TerraPower's Natrium reactor, several publicly traded firms are integral to its development and supply chain:

🔧 Engineering & Construction

KBR Inc. | (NYSE: KBR)

KBR has formed a strategic alliance with TerraPower to commercialize and deploy Natrium reactors globally. The collaboration focuses on creating a replicable contracting framework to reduce financial risk and ensure cost transparency in deploying Natrium technology.

terrapower.com

⚛️ Nuclear Fuel & Components

BWX Technologies Inc. | (NYSE: BWXT)

BWXT has been awarded a contract by TerraPower to design the Intermediate Heat Exchanger for the Natrium demonstration project. This component is critical for transferring heat within the reactor system.

Centrus Energy Corp. | (NYSE American: LEU)

Centrus Energy is collaborating with TerraPower to establish domestic production capabilities for high-assay, low-enriched uranium (HALEU), which is essential for fueling the Natrium reactor.

⚙️ Manufacturing & Industrial Partners

Doosan Enerbility Co., Ltd. | 034020.KQ (KOSDAQ)

Doosan Enerbility is supplying critical components for the Natrium reactor, including the core barrel and internal supports.

HD Hyundai | 329180.KQ

HD Hyundai is manufacturing the reactor vessel for the Natrium project.

🌍 International Collaborators

SK Inc. | 034730.KQ

SK Inc., a South Korean conglomerate, has invested $250 million in TerraPower to support the demonstration and commercialization of the Natrium reactor.

Korea Hydro & Nuclear Power (KHNP) | 15760.KS (KOSPI)

KHNP has entered into a strategic collaboration with TerraPower to support the Natrium project, leveraging its expertise in nuclear power development.

OTHERS:

1. Mirion Technologies (NYSE: MIR)

Mirion is supplying the Radiation Monitoring System (RMS) and Nuclear Instrumentation System (XIS) for the Natrium Reactor Demonstration Project in Wyoming.

2. GE Vernova (NYSE: GEV)

Through its subsidiary, Global Nuclear Fuel–Americas (GNF-A), GE Vernova is partnering with TerraPower to establish the Natrium Fuel Facility in Wilmington, North Carolina. This facility aims to produce high-assay, low-enriched uranium (HALEU) fuel essential for the Natrium reactor.

3. NuScale Power Corporation (NYSE: SMR)

While not directly involved with the Natrium project, NuScale is a prominent developer of small modular reactors (SMRs), a category that includes Natrium. The company's advancements in SMR technology contribute to the broader nuclear energy landscape.

4. Southern Company (NYSE: SO)

Southern Company is collaborating with TerraPower on the development of a molten chloride fast reactor (MCFR), a separate advanced nuclear project. Their involvement in advanced nuclear technologies aligns with the innovations seen in the Natrium project.

________________________________

Sources: Recent industry reports and news articles and TerraPower press releases provide the data above. Also put together with the help of AI.

world-nuclear-news.org, ans.org, gatesnotes.com, scientificamerican.com, terrapower.com, reuters.com

Arm - Positive outlook ahead of earnings - Value to collect?Hi guys we would be looking into our analysis for ARM Holdings before their earnings call!

ARM Holdings (ARM) – Positive Outlook Ahead of Earnings

ARM Holdings plc, a leading provider of semiconductor intellectual property, is poised to deliver a strong earnings report, driven by robust demand for its advanced chip architectures, continued growth in AI and data center markets, and deepening strategic partnerships across the tech ecosystem. As we approach the upcoming earnings announcement, several key factors support a bullish thesis on ARM's stock.

1. Strong Market Position and Licensing Growth

ARM continues to dominate the RISC-based processor architecture market, with its designs powering over 99% of smartphones and making significant inroads into the computing and server space. The company's royalty and licensing model provides a resilient revenue base, which has historically performed well even during industry slowdowns. Recent licensing agreements with leading tech companies, including NVIDIA, Apple, and Amazon, signal continued reliance on ARM's technology.

In Q1 2025, analysts expect double-digit year-over-year growth in licensing revenue, reflecting heightened demand for ARMv9 architecture, which powers next-generation AI and machine learning workloads. This growth is being further fueled by increased adoption in automotive and IoT sectors.

2. AI and Data Center Tailwinds

The surge in AI demand is transforming the semiconductor landscape. ARM's energy-efficient designs are increasingly being integrated into AI accelerators, edge devices, and cloud data centers. The company's Neoverse platform has been gaining traction, especially as hyperscalers seek alternatives to x86 architectures for power- and cost-efficiency. Amazon Web Services’ Graviton processors, based on ARM, are a prominent example of this trend.

As AI infrastructure spending accelerates globally, ARM stands to benefit significantly. Positive forward guidance around AI-related royalties and design wins would further validate this tailwind in the upcoming earnings report.

3. Financial Strength and Margin Expansion

Analysts anticipate revenue growth of 20-25% YoY in the upcoming report, accompanied by improved gross and operating margins. ARM’s high-margin royalty revenue stream contributes significantly to profitability, and recent cost controls have enhanced operational efficiency.

The IPO in 2023 provided a strong capital base, enabling increased R&D investment while maintaining financial flexibility. Shareholder sentiment has been buoyed by ARM's prudent capital allocation and expanding free cash flow profile.

4. Ecosystem Momentum and Strategic Partnerships

ARM’s ecosystem-first approach—collaborating with chipmakers, software developers, and system integrators—has become a key competitive advantage. The company's recent partnerships in the automotive and industrial sectors highlight growing non-smartphone revenue streams. Additionally, ARM is collaborating closely with AI chip startups and hyperscalers, reinforcing its central role in the evolving semiconductor landscape.

Investors should also watch for updates on ARM’s role in emerging verticals such as AR/VR, smart cities, and secure edge computing, all of which could significantly boost its long-term growth narrative.

5. Technical and Sentiment Indicators

From a technical standpoint, ARM stock has shown resilience, trading above key moving averages and gaining momentum in recent weeks. Options activity suggests bullish sentiment, with increased call buying ahead of earnings. If the company delivers a beat-and-raise quarter, it could catalyze a breakout to new highs.

📌 Trade Plan

📈 Entry: 121

✅ Target: 144 Below the strong resistance

❌ SL: 95 - Above the strong support

MELI at Risk from Momentum Shift and High ValuationMELI has gained over 35% since the April dip, but momentum has been fading since September. The slowdown has become increasingly visible, and last week's high may remain the top for some time unless Wednesday’s earnings report surprises the market on the upside.

The consensus estimate for MELI’s revenue is $5,497.05 million, representing a 26.86% year-over-year increase but a 9.27% decline quarter-over-quarter. MELI is currently trading at a forward P/E of 41.9x, which is significantly higher than the 19.8x average of comparable companies. Its geographic advantage over U.S.-based peers gave MELI an edge in April, but without strong earnings to support the high valuation, the stock could become vulnerable.

Over the past five years, MELI averaged 56.2% annual sales growth. That figure is expected to fall to an average of 22.1% over the next three years, which remains solid but signals a clear deceleration.

MELI could move more than 7% on earnings day, depending on the report. If the stock falls below 2,000, it may present a buying opportunity. However, the loss of momentum is usually a negative signal for sustaining trends, so the risk of buying the dip is higher than before.

Microsoft - Positive earnings expectation , value to collect?Hi guys we would be looking forward to our next stock analysis for Microsoft!

Microsoft Corporation continues to demonstrate robust financial performance, underpinned by its strategic investments in artificial intelligence (AI) and cloud computing. The company's strong earnings and forward-looking initiatives position it favorably for sustained growth.

In Q4 FY2024, Microsoft reported revenue of $64.7 billion, marking a 15% increase year-over-year. Net income rose to $22.0 billion, with diluted earnings per share (EPS) of $2.95, surpassing analysts' expectations of $2.90 . For the full fiscal year, revenue reached $245.1 billion, reflecting a 16% increase, while net income grew by 22% to $88.1 billion.

Microsoft's Intelligent Cloud segment, which includes Azure, generated $28.5 billion in revenue for Q4 FY2024, a 19% increase year-over-year. Azure's revenue alone grew by 29%, driven by strong demand for cloud services and AI integration . The company's AI initiatives, such as the integration of Copilot across Microsoft 365 applications, have been pivotal in enhancing productivity and driving adoption.

📈 Positive Overall Outlook

Analysts maintain a bullish outlook on Microsoft's stock, with expectations of continued growth in earnings and revenue. For fiscal year 2025, analysts forecast an EPS of $13.04, up 10.5% from the previous year . The company's strategic focus on AI and cloud computing, coupled with its strong financial results, support this positive sentiment.

Microsoft's commitment to expanding its AI capabilities is evident in its planned $80 billion investment to enhance its global network of computing centers . This investment aims to support the growing demand for AI services and solidify Microsoft's position as a leader in the AI and cloud computing markets.

To summarize, Microsoft's strong financial performance, driven by its cloud and AI initiatives, positions the company for continued success in the evolving technology landscape.

📌 Trade Plan

📈 Entry: 390 -

✅ Target: 430 - Just below the ATH / around the strong resistance

❌ SL: 365 - Just around the current rejected support zone

Bitcoin - consolidation will lead to continuation (up)

Very basic chart.. only needs one markup !

- Institutional buyers are scared the price will drop

- Retail buyers are worried it drops (like so many are predicting)

But nobody knows where it will go next.

Common sense - After consolidation comes continuation... it wont go sideways much longer, its lightly to go up at least to the 100+ range.

That's my short summary for the next few weeks.

-14% 95 incomingBack down to retest the lows snagged 100 95 90 5/23 P before the close today then SMCI drops it 2% with a BILLION dollar miss not the news I was anticipating but I'll take it very fragile stock not holding up well GDP tm could accelerate loss.

Expect ENPH breakout by EOY 2025. Buy <$60Trends:

- LT parallel channel shown marks some key trendlines for the company since IPO

- LT falling wedge intersects the bottom of this channel H2 2025 --> a buying opportunity above $50. If that breaks, falling wedge ends around $35, a 30% downside (or 40% vs today's price).

- The early 2023 peak aligned with peak in revenue and net income (decline matched stock decline). We're now seeing revenue and net income growth again (growth can bring back stock growth)

My Bias:

I'm a long-term believer in solar. ENPH plays mostly in the residential solar space (and is expanding into small commercial). They are often lauded for their high levels of customer service.

Investment Thesis:

We're back to financial growth but the stock is down. We're in a few months window before LT trends converge mid / H2 2025. If we break bullish from falling wedge and hit LOWEST point of parallel channel by EOY 2026, we'd be at $70/share (16% upside from $60; 40% upside from $50). This is my expected worst case scenario, meaning anything under $60/share is now a buying opportunity.

Clean set up Bouncing of the lower trend line yet again, CleanSpark plans to sell mined Bitcoin each month and has secured a $200M credit line from Coinbase Prime as it shifts toward self-funding operations.

I'm a fan of more cash on hand giving the room to scale.

Under 400$ is a steal Strong move off 150 support. They had a 180 sell downgrade announced from some clowns today they'll be revising there targets shortly. COIN will be used be everyone and there grandma soon enough. Consumer/government dollars pouring in is insane this company is not going anywhere they also just realsed plans for BTC Yield Fund, offering 4-8% APY to non-US institutional investors through a limited leverage cash-and-carry trade strategy.

I don't think we'll be falling below 178 would be a great entry if your lucky enough.

StoneCo | STNE | Long at $8.76StoneCo NASDAQ:STNE revenue rise is staggering.

Position started at $8.76. Chart looks ready for a move up, but nothing is guaranteed.

Price Targets into 2027:

$10.00

$12.00

$14.00

$16.00

$30.00 (long-term view)

PAPL - Good epxectation for earnings, collect potential?Hi guys we would be looking into Paypal Today

Analysts maintain a "Moderate Buy" consensus on PYPL, with 17 buy, 17 hold, and 2 sell ratings. The average 12-month price target is $84.69, suggesting a potential upside of about 29.6% from the current price. Price targets range from $49 to $125.

Earnings Performance

In the most recent quarter, PayPal reported adjusted earnings per share (EPS) of $1.20, a 22% year-over-year increase, surpassing expectations. However, revenue grew by 6% to $7.85 billion, slightly below forecasts. Notably, PayPal has exceeded EPS estimates in each of the last four quarters.

Growth Initiatives and Strategic Outlook

Branded Checkout Enhancements: Efforts to improve user experience and competitiveness against rivals like Apple Pay

Venmo Monetization and Debit Card Expansion: Initiatives to increase revenue through Venmo and broader payment options.

Fastlane Guest Checkout: A new feature aimed at streamlining the checkout process, with significant monetization expected in 2025.

Valuation and Future Prospects

PayPal's current valuation at 14 times forward 2025 earnings is below its five-year average P/E of 50.5, indicating potential for multiple expansion. Forecasts suggest revenue could reach $35.1 billion in 2025, with EPS around $4.93.

Our Conclusion

Given its strategic initiatives, consistent earnings performance, and favorable valuation, PayPal appears poised for growth. While challenges like competition in digital payments persist, the company's focus on innovation and user experience may drive its stock price upward in the coming years.

📌 Trade Plan

📈 Entry: 65.50

✅ Target: 75.50 - Targeting the weak resistance

❌ SL: 55.50 - protecting the trade above the bottom zone

Solana | BULLISH ON SOL | SOL Dominates Blockchain RevenueEven with a dip in activity particularly around memecoins, Solana has managed to hold its ground impressively when it comes to generating revenue.

While you might think fewer transactions would automatically mean less money coming in, Solana's performance shows otherwise. This ability points to the solid value being created by the different applications and uses on the network right now.

A big reason for this financial resilience is the continued strength of dApps on Solana. These apps have been really effective at bringing in fees and adding value to the network. It seems that while the hype around certain speculative tokens has died down significantly, the core utility and economic activity within Solana's dApps are still going strong. This shift towards more fundamental uses for generating revenue is a really positive sign for how the network can keep growing in the long run.

Looking ahead the future for SOL is bright imo as more projects are linking Artificial Intelligence with Solana, taking advantage of its speed and low costs to build new things. Plus, the introduction of Solana ETFs in Canada is a big step.

Other Solana-based alts including Official Trump (TRUMP), Jupiter (JUP), Raydium (RAY), and Bonk (BONK), have followed SOL with good price increases.

It seems like the focus is shifting towards building more lasting and useful applications. With ongoing support for developers and increasing interest from the traditional financial world, Solana seems well-positioned to handle market ups and downs and keep finding new ways to create value in the future. I'll definitely be watching to accumulate for the long-term.

______________________________

BINANCE:SOLUSDT

$3.9 Billion At Support?Long term buy structure forming now.

Large volume sweeps and blocks are being made here. Very large trade at this level happened last week and I think this is going to explode in the coming weeks/months.

Target #1 - $35

Target #2 - $40

ETH/USDT LONG IDEAPosition opening range 1798~1803 USDT in batches

Total Position Recommendation Within 5% of total funds (or 1~2% of total account loss)

Stop Loss 1784 USDT, liquidate the position when triggered.

Take Profit First Target 1844, Second Target 1872

Cooling-off rule: 24 hours cooling-off after stop loss

Prohibition Prohibition of chasing high, prohibit the increase of positions, prohibit continuous trading

FTM Delisting | OFICIALLY Becoming SONIC (S)Although a name change for FTM was announced in Aug 2024 already, many exchanges still list FTM, and this will soon change.

It is expected the Fantom will officially be delisted and become SONIC within the next two months.

In August 2024, Sonic Labs announced that they would be replacing Fantom with a new token called Sonic (S). Sonic Labs have confirmed that all existing FTM holders would be able to convert to S at a fixed rate of 1 FTM : 1 S. However, many exchanges will only transfer now, as they will finally be delisting FTM for good and converting all FTM S. This will be done at a conversion rate of 1:1.

_________________________

Make sure you don't miss the latest ETH update, since BTC is likely heading towards a new ATH and ETH stands much more to gain.

_________________

CRYPTO:SONIUSD

POLONIEX:FTMUSDT