HTZ shifting gears? like a Bull!oh look at you HTZ if you keep this up I may just have to rent(buy) you for a little while. This one is warming up and getting ready for a nice ride maybe up to 22, could be, could be. I'll have to wait a bit longer to confirm the uptrend.

HTZ

HTZ bounce at support? a candle that opens below the bollinger bands lower band, then closes above it.

morning start reversal.

At Support

HTZ Bounce off support.a candle that opens below the bollinger bands lower band, then closes above it.

I can't take this trade, I am at my max capacity. Anyone else like this. If so why or why not. still trying to hone my charting skills and all input is welcome.

HTZ Buy Low Sell HighHTZ looks to have found support at the bottom of this channel, as well as with the 200 SMA underneath. Looking to go bullish with a breakout of today's 2/15 High-Wave candle. Best case scenario: we get an inside day candle tomorrow, and then break out on Tuesday 2/20. This would work great for a swing trade, or a possible intra-day play.

FOUR OPTIONS TRADE IDEAS FOR NEXT WEEK: HTZ, TLT, GLD, AND XOP... , one high implied volatility (HTZ), two low implied volatility (TLT, GLD), and one long-dated bullish assumption oil trade (XOP).

High Implied Volatility

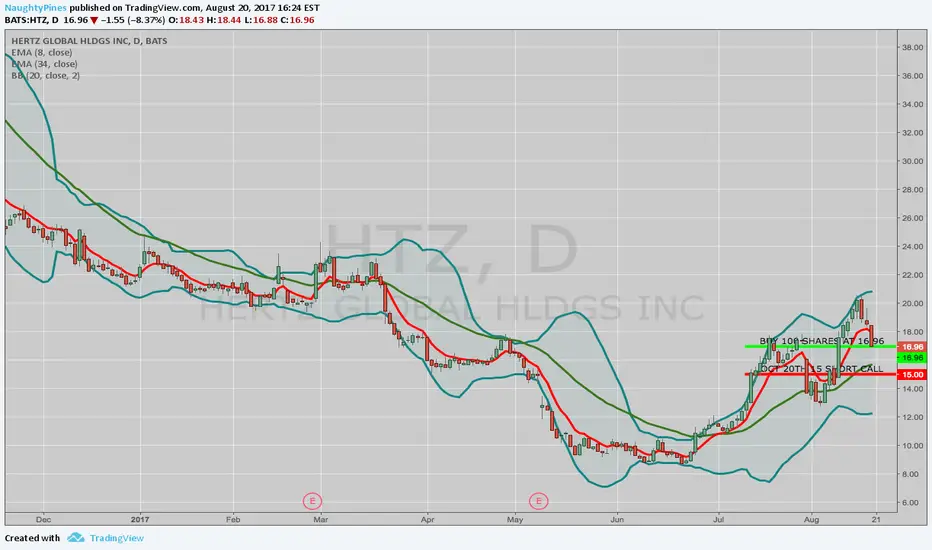

HTZ "Monied" Covered Call

Buy 100 Shares at 16.96

Sell Oct 20th 15 call

13.99 db (your cost basis in the shares)

1.01 max profit if called away at 15

Notes: Roll the short call out for additional cost basis reduction if it doesn't finish at 15 or you can't exit the trade before expiry around that mark. It's only got monthlies, so some patience may be required if you are unable to get your candy right away. An alternative approach would be to sell the 12.5 short put in the Oct 20th expiry (currently trading at .50) and then look to cover (monied or otherwise), if assigned.

Low Implied Volatility

Both TLT and GLD are in low volatility territory here, so look to deploy low volatility strategies on them ...

TLT Sept 15th/Dec 15th 125 put calendar

1.87 db

GLD Sept 15th/Dec 15th 121 put calendar

1.63 db

Notes: Roll the short put aspect out for duration "as is" on significant decrease in value, and look to exit the trade at 20% max of what you put it on for. Obviously, not "big money" plays, but also not big buying power pigs either ... .

Long-Dated Neutral to Bullish Assumption Oil Trade

XOP Oct 20th 31 short call/March 16th 21 long call Poor Man's Covered Call

8.06 db

Notes: Roll the short call aspect of this setup out for duration and credit to reduce cost basis in the setup and look to exit the trade for 10-20% max of what you put it on for. For a longer duration setup with the potential to reduce cost basis in the entire setup to zero over time, consider the Oct 20th 31 short call, Jan 18th '19 20 long call Poor Man's for a 9.54 db. An alternative instrument to consider which is also oil sensitive is XLE, although a similar setup comes with a heftier "entry fee" -- the Oct 20th 65 short call/Jan 18th '19 50 long call costs 12.29 to put on.

Long term trade on HTZ. BullAfter apple´s agreement with HTZ, the market have bought the tock and have increase 80% in 17 days. Even thought it seems enough, I am think we can reach the Daily 200MA after a gold cross between the 9MA and the 200 MA in a 4 hour TF.

Small term short position on HTZI am betting on a possible profit taking action before the closing bell, sending the price to the previous R2 on the pivot lines in the 4 hours chart.

THE WEEK AHEAD: PIVOT TO NON-HIGH VOLATILITY STRATEGIESWith this quarter's earnings season all but over and with VIX trundling along at sub-10 levels, there is a paucity of high implied volatility plays in the market for premium selling, so I'm looking at deploying something in either low volatility strategies (diagonals) or in directional plays that I've been eyeing.

Screening for underlyings with greater than 70% implied volatility rank over the past 52 weeks, greater than 50% background implied volatility, and relatively high options liquidity yields a few names -- P, HTZ, and NBR, but it'll be tough to squeeze good premium out of these because they're all <$10 underlyings. I would be willing to get into exchange-traded funds if only there was one with >70% implied volatility rank and >35% implied volatility; there currently isn't.

With the individual underlyings, a P 9 short straddle in the July 21st expiry yields 1.84 at the mid with BE's at 7.16 and 10.84 (put side, below expected move; call side, at expected move); a HTZ July 21st 10 short straddle yields 2.03 with BE's at 7.97 and 12.03 (both sides clear of the expected move); and the NBR July 21st 9 short straddle, 1.54, with BE's at the expected move on the put side and above it on the call (7.46/10.54).

Alternatively, NBR is a petro play,* so I can see taking a bullish assumption on the underlying and short putting it, even though it won't pay all that much (the July 21st 8 put brings in .40 with a BE of 7.60).

Directionally, I've got my eye on two sector exchange-traded funds: XLE and XRT. Out of all the sectors, energy and retail have been the most downtrodden, so this may be an opportunity to go long with comparatively "cheap" setups that have oodles of time to work out -- Poor Man's Covered Calls -- with long-dated back months several cycles out. I'll post setups on those separately; however, each time I look to pull the trigger on a bullish XLE setup, oil seems to trundle lower and XLE with it ... .

* -- NBR is deepwater; if they're not in trouble now with oil sub-$50/bbl., they will be in trouble in short order if prices hang around here for long. Generally, BE for deepwater oil exploration and production is well above this year's $55/bbl. high, so I'm hesitant to take a bullish assumption on deep water anything. Frankly, I'd rather put my buying power to work on something like XOP, where I'm not exposed to single name risk in this area, given the fact that there are so many troubled companies in this sector.

HRI - Flat Double Zig-ZagFlat double zig-zag looking to launch this back into 50+ share territory. Look to go long at break of 50 using the Elliot structure as your guide you.

THE WEEK AHEAD: EARNINGS AND A PERSISTENTLY LOW VIXIf you're going to play anything next week premium selling wise, it's going to be in earnings, because that's all that's really out there volatility-wise. The VIX remains persistently low here, and running a screen for exchange-traded funds with >70% implied volatility rank, and >35% implied volatility yields absolutely nothing.

Here's what showed up on my radar -- some sketchy ADR action (WUBA), a little bit of frisky biopharm (BCRX), and some beaten-down brick-and-mortar retail (M, SHLD, JCP):

WUBA (99/56) (Online Retail): It's scheduled to announce earnings on Thursday (2/23) (Short strangle/iron condor).

BCRX (98/287) (Biopharm): Earnings Monday (2/27) Before Market Open. (Short puts, short straddle). This is biopharm, which -- in itself -- should serve as a warning. You may want to do a bit more due diligence on this one than you would ordinarily, since they can explode, but also implode.

DKS (98/48) (Sporting Goods/Retail): Earnings are three weeks out, but I thought I'd put it out there since it's nearly ripe for play implied volatility rank/implied volatility wise. (Short strangle, iron condor).

M (96/49) (Department Store Retail): Earnings Tuesday (2/21) Before Market Open. Because we have a long holiday weekend here, with the markets being closed on Monday, I've probably missed an opp to play this one unless there is high vol afterglow post earnings. (Short strangle, iron condor).

SHLD (93/127) (Department Store Retail): I don't see that this has earnings up, but it's in the process of imploding. (Short puts, short straddle).

BBY (93/47) (Retail): Earnings 3/1 Before Market Open. We're still a ways out from earnings, so like DKS, nearly ripe ... . (Short strangle, iron condor).

HTZ (92/73) (Car Rental): Earnings 2/27 (Monday) After Market Close. Another one that's ripe right now. (Short strangle, iron condor).

JCP (88/65) (Department Store/Retail): Earnings Friday (2/24) Before Market Open. Another beaten down brick and mortar retail issue. (Short puts, short straddle).

OCN (85/70) (Financial): Earnings on 2/22 (Wednesday) After Market Close. (Short puts,short straddle).

HTZ In Wave 3 on Hourly ChartBullish Kicker on daily chart trading close to 52 week low on high volume with Connors RSI(2) overbought at 94. Also was some big buys and an insider buy. I got in at 25.92

ADX is >30, TSI cross and above zero, and it closed above the 60sma.

Also a case can be made for the formation of an intermediate impulse wave - starting wave three which will mean a move close 27, which happens to coincide with the nearest short term resistance level.

If the count is correct, we will only have a retracement to 27.14 which is the end of wave 1, and Elliot says wave 4 cannot overlap into the territroy of wave 4.

I''m still ,long and will look to take profits around 27, setting a buy limit in the area of 26.30.

SOLD HTZ SEPT 16TH 40/57.5 SHORT STRANGLEThis one popped up earlier today as a high implied volatility play ... .

Filled for a 1.83 ($183)/contract credit ... . I'll look to take it off at 50% max ... .

HTZ possible bear call spreadSpread is above strong resistance and the 100 SMA. The covered call is if you are in shares...