Move index saw a140 level this is a Panic short term bottom ONLYThe spreads loved like a failure was near ! So the move index reached a short term bottom Only in the High yield market so now everyone things it is safe to jump back to RISK ON . This is what we see in BEAR MARKETS sharp strong up thrusts to be followed By longer declines .Best of trades WAVETIMER . NOT A NEW BULL MARKET TRADERS

HYG

Hyg and vixWell hard to argue this thing show oscylator kid behavior. I really do hope we gonna pierce dashed line. Otherwise we may have some serious discount on stocks.

IF you are Bearish SP 500 Your EARLY The chart posted is That of High yield Market ETF HYG we have just finished of the correct in this sector and should see Liquidity coming back into assets One Last Gasp This should raise mags qqq and spy toa new record high as most other indexes struggle to rally back to .618 best of trades WAVETIMER

MOVE INDEX BONDS SET TO HAVE CRISIS The chart of the move index aka BOND VIX is showing a high level of Complacency as the bonds are in sharp decline phases The worst is yet to come as the Panic in the debt markets has not been seen. Inflation and deep recession is in my model and forecast for the next 18 plus months .

MOVE INDEX A whole lot of FEAR today !!!The chart posted is that of the move index The Vix of the Bond market As you can see to the right of the chart Today Spike Outside of the bb bands . I am Long calls in TLT 90 strike 2026

$HYG will get a boost this summer when rates are cut due to BOJI see the BOJ dumping treasuries this summer, which'll force down the USDJPY pair, and increase inflation here at home. When rates go down, borrowing money is easier, especially for junk corporations avoiding default due to decades high interest rates.

Could AMEX:HYG fall back into the box one last time? Absolutely, if the dollar ticks higher after FED hawkishness. But then, AMEX:HYG will catapult.

When HYG is ready I'll give out some options plays to capitalize on the bullish trend.

High Yield Corporate Bonds as indicator for Risk AppetiteThis is not something I would use as a trading signal by itself, but it is a good indicator on the weekly chart of how bigger players are viewing risk appetite.

High yield corporate bonds, as seen reflected in ETFs like AMEX:HYG and AMEX:JNK , are an interest data point. High yield implies that these are riskier bonds with a higher chance of default on the debts. Just like as individuals, we have credit scores and when we apply for loans, the interest rate can vary depending on how the bank rates us risk-wise on perceived ability to pay back the debt, those who have a lower score might get a higher interest loan because they are considered higher risk of default. Same basic principle applies to corporate debt.

When liquidity is flowing and the economy overall looks good, large investors/investment banks will feel better about buying riskier high-yield bonds and other debts because we're in an economy paradigm where there's a better chance that not enough of those will default to cause significant harm to the debt holders.

But, when the economy is getting pinched for whatever reason and liquidity starts to dry up, high risk, high yield debts are much less desired due to perceived increased risk of default.

Sometimes the high yield debt moves pretty close in tandem with the market, see for example the dumping that happened during the 2020 COVID panic.

Before and after that, you can often see a bearish divergence in AMEX:HYG and AMEX:JNK many weeks before the S&P finally tops out and begins its decline. The above chart, you can see the decline become more obvious as we wind down 2017 and head into 2018, then also see it again pretty obviously in the second half of 2021 before the sell off for most of 2022 started.

Both AMEX:HYG and AMEX:JNK came online around 2007-8 timeframe, just before the GFC. You can see a pretty steady decline right from the beginning there, and a rapid rebound as things find bottom.

What is interesting is how far both AMEX:HYG and AMEX:JNK came down throughout 2022, and while equities have since had a nice recovery bounce for most of 2023, the high yield bonds have not had such a recovery. It's actually instead slowly condensing price action with slightly higher lows, but also lower highs. We seem to be nearing the end of that wedge and hopefully soon we get an answer on what the risk appetite really is of risky debt, because it will be a solid signal of where equities may be headed next.

Personally, I'm already seeing some indications that as we approach the end of the year, we may see a larger dip in equities. For how long and how large, that remains to be seen. For right now, we're having a recovery rally from selling off most of August and I'm not seeing any indication it's a good time to go against that trend, but that may change in the coming weeks.

HYG and why it matters

High yield corporate bonds show a significant correlation with the risk-on/risk-off sentiment for the S&P 500 (SPX). As we can observe, the current market structure resembles a wedge, which can technically serve as both support and resistance.

To add complexity, we're currently at a channel resistance level, which also happens to be a historic trendline. This trendline has consistently been respected and traded in markets experiencing changing sentiment.

It's becoming apparent that several factors are aligning for the upcoming months when you consider these various charts. This confluence of technical indicators and historical patterns suggests that careful monitoring of these charts is essential as they could provide valuable insights into market movements in the near future.

$PEPEUSDT key support and resistance levels + weekly forecastOKX:PEPEUSDT continues its weakness relative to CRYPTOCAP:BTC and broader "risk on" signal markets such as $NQ!

This latest dip was driven by an extremely negative news event - Grifter Gensler and his band of goons at the SEC are employing some bank-collapse-contagion-red-herring tactics by suing Binance. This news allowed the bears to take control and we see the temporary decoupling from the usual tight correlation with the Nasdaq break:

In such events, traders with massive positions such as wallet 0x4614 move to protect their capital and sold huge positions to cut short term losses, as the market readjusts to lower key levels.

If this was a catastrophic sell off event, we would not have seen a bounce off key support at 0.00000095, and the last remaining support for OKX:PEPEUSDT 0.0000005 would have fallen.

The 0.0000005 level is revealed by my TA as the "last stand" support level for $PEPEUSDT. Breakdown BELOW this level would be a pivotal bearish moment and we would need a week or so to establish relatively "strong" support levels, not just daily price ranges, at lower price levels.

However, this is not what happened during Bitcoin's multi thousand dollar move down which means that short term volatility can continue.

Using a three-way outcome/decision matrix - down-neutral-up - we can prepare for three scenarios and deploy capital accordingly.

The first outcome which is down, is a breakdown below the 095 handle and a cascade towards 056 handle (red box range in title image). As OKX:PEPEUSDT is tightly correlated with CRYPTOCAP:BTC and AMEX:HYG (BBB bonds), this would likely mean those two broader markets would have continued lower. If we look at CRYPTOCAP:BTC key levels, again we're not in catastrophe scenarios at all, a nice bounce off the $25.5k level and bulls will target $25.9k as next resistance:

And AMEX:HYG levels also looking healthy, above 74.3 support with 75.3 as overhead resistance.

Secondly in the neutral outcome we find a new range in OKX:PEPEUSDT bouncing between 0.000000950 and 0.00000108. A perfectly acceptable outcome for active traders as this offers a nice 10% intra day range.

Thirdly in the OKX:PEPEUSDT bull case we need to see a breakthrough in CRYPTOCAP:BTC above $25.9k level and a move towards its next major resistance level now at $27k.

just an observation. $SPY vs $IEF / $HYGAppears we are running out of risk appetite. Put also looks like we have built a very nice base for a significant move higher. Hopefully, that's a risk on move, not a risk-off move.

Personally, I believe we have already corrected in each individual sector, it just didn't happen all at once like it normally does.

According to this, risk aversion and sentiment have been flat in a range for the past few months according to IEF/HYG.

HYG daily bullish hammer above 100 day moving averageHYG daily bullish hammer above 100 day moving average if we break above we can run into 200

$HYG setting up for a H&S breakdown? Corporate bond blowup?$HYG looks like it's about to fall.

There's a H&S pattern forming on the 4Hr timeframe and price just rejected the 200DMA.

Should price break support at $73.05, I think we'll see a quick move down to the $69 region, maybe even lower.

I've taken some puts just incase this plays out.

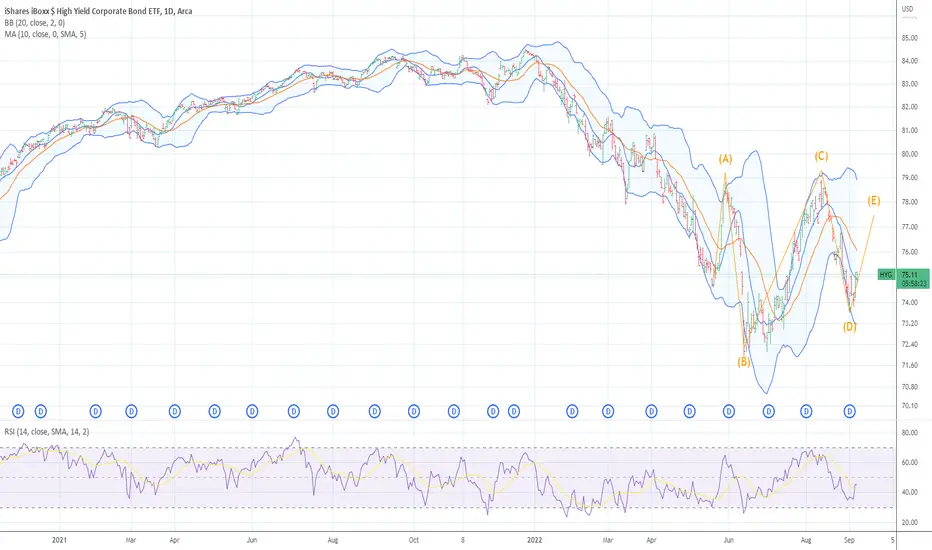

HYG TRIANGLE. Wave D low is NOW rally in wave E of B HYG hourly chart TIME is running OUT for the rally in SPY QQQ I have now moved back to 100 % cash sold the 75 % net long at 4144

HYG TRIANGLE. Wave D low is NOW rally in wave E of BThe chart is what I have felt is the most important chart to watch for sometime . We rallied and stopped right at the trend line . I have watching this as to it will become an issue for the sp 500 going forward . best of trades WAVETIMER

SPY QQQ HYG Divergence again I’m not sure if SPX/HYG divergence is reliable moving forward, but this indicator has proven pretty effective last year. We are currently diverging again, last 3 major divergences created pull backs of -17%,-13%, -21%

Any thoughts from my fellow analysts?

Any other divergence indicators you can share with high probability?

Good luck to all

The Sh!t is going to hit the FAN still ahead if we break .618The chart posted is that of debt in corp market lqd We bounced off the .618 in what looked to be a large ABC DECLINE .But it can also be counted now as wave 5 of 3 down which would mean we would see another leg down to 89. 8 soon

Rolling (IRA): HYG November 18th 69 to December 16th 69... for a .35/contract credit.

Comments: With the November 18th 69 converging on .10, rolling it out for a credit about equal to the monthly dividend. Total credits collected of .42 (See Post Below) plus the .35 here for .77 ($77) per contract.

Credit Conditions and the Fed: Part 2In part 2 I take a quick look at high yield corporates and describe a common mistake made in using ETF ratios to monitor changes in credit risk. Part one and an earlier piece that described how to use the TradingView platform to monitor secondary market credit spreads are linked below.

If there is any one thing that will produce a Fed policy a pivot, it is credit distress. Credit is far more vital to economic functionality than equity. If companies are unable to secure funding, they may face liquidity issues, and if liquidity problems become widespread, they have the potential to become systemic. In 2008 and again in 2020 credit markets were frozen. Particularly in 2008, many companies ran into barriers that inhibited their conducting their ongoing daily business lines. There were plenty of offers but, as I so painfully remember, in many cases zero bids…. None…at any price. It was this credit distress that convinced the Fed to move.

In part 1 we looked at the weekly chart of the option adjusted spread (OAS) of the broad ICE BofA Corporate Index and concluded that the there is no evidence of the kind of credit distress that would galvanize the Fed, and that, at least on this basis, that there was no compelling value (rich/cheap) argument to be made.

What of high yield? Does high yield OAS suggest a meaningful deterioration in credit markets? Again, I plot a regression mean and one and two standard deviation bands above and below. Just as in the IG market, high yield OAS has widened, but only to its long term mean, and this following a lengthy period of being nearly a standard deviation rich. In short, while spreads have widened somewhat, there is no compelling rich/cheap argument and certainly nothing that would suggest to the Fed that credit conditions are meaningfully impaired.

I frequently see commentaries that use price changes in the high yield ETF (HYG) and the investment grade ETF (LQD) as a measure of investor risk preference. Since the January high, LQD is down 26.15% versus 19.65% for high yield. At first glance it appears as if investors prefer the lower quality HYG. But the price changes do not account for the differences in fund duration. Put simply, LQD at 8.36 years duration has roughly twice the interest sensitivity of HYG at 4.06 years. In other words, a 100 bps change in rate, will change LQD 8.36% and HYG 4.06%.

LQD in Ratio with HYG and Ten Year Futures in Ratio to Five Year Futures: I also see analysis that uses the ratio between LQD and HYG to ascertain risk preference. But the direction of the ratio is almost completely due to the difference in duration. You can see this by compare LQD/HYG to the ratio between ten year and five year note futures. LQD/HYG ratio is almost entirely correlated with changes between five and ten year treasuries. When rates are volatile and directional the total return of many rate products generally a reflection of rates than it is investor quality preference.

And finally, many of the topics and techniques discussed in this post are part of the CMT Associations Chartered Market Technician’s curriculum.

Good Trading:

Stewart Taylor, CMT

Chartered Market Technician

Taylor Financial Communications

Shared content and posted charts are intended to be used for informational and educational purposes only. The CMT Association does not offer, and this information shall not be understood or construed as, financial advice or investment recommendations. The information provided is not a substitute for advice from an investment professional. The CMT Association does not accept liability for any financial loss or damage our audience may incur.

Opening (IRA): HYG November 18th 69 Short Put... for a .42/contract credit.

Comments: Targeting the strike paying around what the distribution would be were I to actually be holding shares. The last distribution was .351 per share; 5.19% annualized.

BTC, SPX, RUT wide gap from HYG. We're up for a rude awakening dear fellows,

it came to our attention the monthly chart of HYG, BTCUSDT, SPX, RUT. they all belong to the same class of speculative assets.

of them, HYG is likely to have the greatest demand for liquidity as it lives out of refinancing its cash flow, let alone its debt.

notice how

1. they are synchronized in what concerns the bottoms

2. HYG renewed the lows at each new bottom, never the highs at each top.

3. the others did the opposite

this mismatch opened up a wide gap in the logarithmic scale of the y axis.

the logarithmic scale shows how much percentually current level still can fall.

thus, BTC, SPX and RUT still can fall more than they did already until they catch up with HYG.

that is precisely the case of FED keeping current policy "until something brakes".

that would be a rude, late, awakening for anyone not knowing where to look at for market health check.

best regards.

BULLISH Signal flash with 2008 failure exampleThere is some discussion taking place regarding the divergence of SPY and HYG during the last few days and this divergence is a signal for marking the market bottom.

I would like to point out while this generally is a true indication of a potential reversal/bottom (under normal circumstances).

We are not dealing with normal circumstances.

The same signal existed in 2008 (also not normal circumstances) between 2 Jun 08 - 19 Jun 08. The "rally" in SPY was very, very lite before failure. SPY only "rallied" 2.7% before

cycling back down another 10%, holding in range for 2 months then waterfalling down another 38%.

Use extreme caution IF trading this signal.

I would consider this signal as being "Set-up", the "Follow-Thru" would be price moving above 373.04

2008 required a follow-thru above 141.17, "rally" price high was 137.12 which obviously failed to reach the follow-thru requirement and prices failed through the support. Down ~48% within 5 months.

This is not a prediction/forecast, this is pointing out potential of failure while others are discussing potential of success.

U.S. INTEREST RATES IN THE 2 YR 5 YR 10 YR HAVE TOPPEDTOP WAVE STRUCTURE the chart posted a week ago is very clear we have peaked in ALL interest rates and A major I..T. top in U.S. $ Iam 75 % net short the DXY at 109 I stated the alt target was 110.25 the original projection was 114/116 DO NOT BE LONG THE US $ THIS SHOULD BE A STRONG POSITIVE FOR BONDS STOCKS and ALL Metals move to a net long Silver copper gold platinum NOW rally to start or has begun .best of trades WAVETIMER

JUNK BONDS HYG WAVE D .887 The chart posted is that of hyg the junk bond market . so far we all three waves within the structure . if we hold here at a .887 golden ration we would then see the last rally this market will see for years to come we would then see wave E UP THIS WOULD BE WAVE B TOP