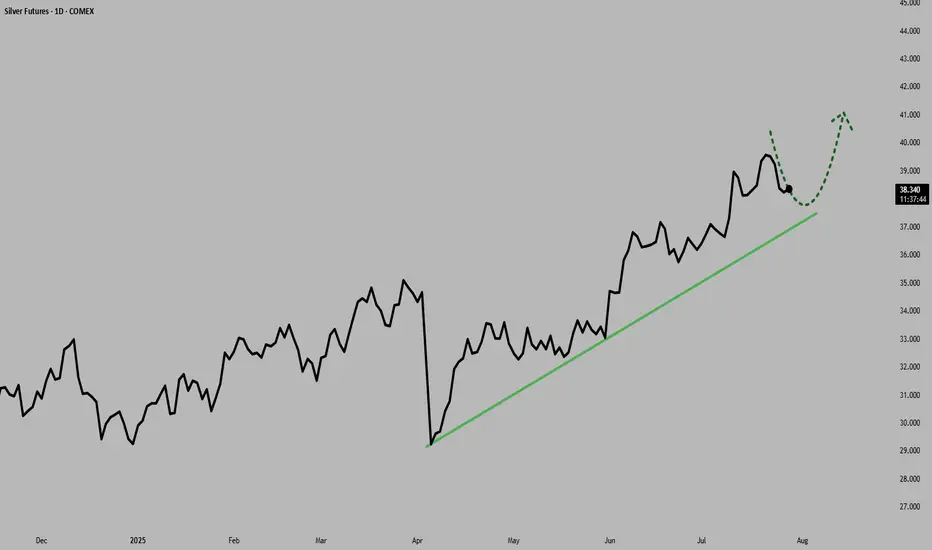

Silver Near $40: Deficits and Demand Fuel the RallySilver prices surged to multi-year highs in July 2025, driven by an extraordinary convergence of bullish factors, pushing prices above $39 per ounce, levels last seen in 2011.

Silver’s rally, supported by robust industrial demand and safe-haven inflows, aligns with traditional patterns as the U.S. dollar has weakened over 2.3% over the recent period.

Macroeconomic Drivers and the U.S. Dollar

Silver's rally is unfolding around shifting macro conditions. The Federal Reserve has kept interest rates at a restrictive 4.25-4.50% throughout 2025 due to persistently high inflation (2.7% YoY). However, expectations for more rate cuts are growing, with the CME FedWatch tool showing a 59.8% probability of a cut at the September meeting as of July 28.

Adding to the complexity, U.S. trade policies have triggered significant market volatility and raised concerns over a potential supply shock. The U.S. administration has imposed steep 30% tariffs on imports from Mexico, set to resume on August 1. This has heightened fears, as Mexico is the world’s largest silver producer and supplies over half of U.S. silver imports.

But macro drivers aren’t the full story. The real force behind silver’s rally lies in the physical market itself. A structural supply deficit, escalating industrial demand, and growing investor appetite from Asia and North America, are proving to be far more pivotal than shifting rates or a softer dollar.

Physical Market Dislocation and Industrial Demand

The year 2025 marks the fifth consecutive year of a structural deficit in the global silver market, and the imbalance between supply and demand shows no sign of easing.

With minimal new mining capacity expected to come online and lengthy lead times for project development, supply constraints are structural rather than temporary.

Since 2021, the cumulative shortfall has reached nearly 800 million ounces (25,000 tons), steadily drawing down available inventories and tightening the market.

Industrial demand remains the central pillar of silver’s bull market. Forecasts for 2025 project record consumption of roughly 700 million ounces, driven by rapid adoption in green technologies and digital infrastructure. The electrical and electronics sector, which includes solar photovoltaics (PV), consumer electronics, automotive electronics, power grids, and 5G networks, has increased its silver usage by 51% since 2016.

Solar PV alone consumed approximately 197.6 million ounces in 2024, a record largely driven by China’s 45% expansion in solar capacity. With global EV production expected to approach 20 million units in 2025, automotive silver demand alone could exceed 90 million ounces.

Together, persistent deficits, accelerating industrial consumption, and capital flowing into physically backed investment vehicles are creating a market where available silver is increasingly scarce, amplifying upside pressure on prices regardless of short-term macroeconomic shifts.

COMEX silver inventories peaked at 504.72 million ounces on May 11 but have since eased back to levels last seen on April 24, indicating a recovery in demand following the large accumulation in US inventories post-tariff shock.

Positioning and Ratios Favour Gains

With net inflows of 95 million ounces in the first half of 2025, silver ETP investment has already surpassed the total for all of last year. By June 30, global silver ETP holdings reached 1.13 billion ounces, just 7% below their highest level since the peak of 1.21 billion ounces in February 2021

Futures positioning has also surged , with long positions up 163% over six months. These factors have helped propel silver prices over 35% higher year-to-date, building on a 21% gain in 2024.

The iShares SLV ETF netted inflows of $1,467.5 million over the past 3 months.

Physical silver investment demand remains robust, with significant buying from Asian markets. India, the world’s leading silver importer, saw record purchases of physical bullion and silver-backed ETFs during the first six months of 2025.

The gold-to-silver ratio, currently in the late 80s, remains historically elevated, suggesting silver remains significantly undervalued compared to gold. This indicates substantial upside potential for silver, especially given persistent market deficits, rising industrial and investment demand, and gold rising at the same time.

Hypothetical Trade Set-up

The silver market’s bullish fundamentals appear increasingly robust. Investors may consider accumulating silver positions, viewing short-term consolidations as attractive buying opportunities amid the compelling long-term outlook.

Options open interest for the September contract shows a bullish bias with a put/call ratio of 0.82 and high call interest at the far out-of-the-money call strike of $45 per ounce.

To express a bullish view on silver, investors can deploy a long position in CME Silver futures expiring in September. A hypothetical trade setup for this view is described below.

● Entry: $38.00 per ounce

● Target 1: $40.00 per ounce

● Target 2 (extension): $42.00 per ounce (if Fed easing in September coincides with physical tightness)

● Stop Loss: $36.70 per ounce

● Profit at Target 1: $10,000

● Profit at Target 2: $20,000

● Loss at Stop: $6,500

● Reward-to-risk ratio: 1.54 (Target 1) and 3.08 (Target 2)

Alternatively, investors can exercise the same view using CME Micro Silver futures, which offer smaller notional positions and more flexibility. Each Micro contract is priced in USD per ounce and represents 1,000 ounces of silver, compared to 5,000 ounces for the standard contract.

MARKET DATA

CME Real-time Market Data helps identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs tradingview.com/cme .

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed. Please read the FULL DISCLAIMER the link to which is provided in our profile description.

Industrialmetals

Nucor | NUE | Long at $120.17Nucor NYSE:NUE , a US manufacture of steel and steel products, will likely capitalize on reduced foreign competition as tariffs become reality. The CEO also recently stated that the steelmaker's order backlog is the largest in its history and is increasing prices. So, while there is a potential for short-term downside as tariff "unknowns" are negotiated, the longer-term upside may be there for those who are patient... but time will tell.

Basic Fundamentals:

Current P/E: 21x

Forward P/E: 15-16x

Earnings are forecast to grow 29.6% per year

Projected Revenue in 2025: $32.3 billion

[*} Projected Revenue in 2028: $39.4 billion

Debt-to-Equity: 0.4x (healthy)

Dividend Yield: 1.8%

Technical Analysis:

Riding below the historical simple moving average and there is risk the daily price gap near $109 will close before moving higher. If there is a "crash" in price, $70s is absolutely possible which will be a "steel" if fundamentals do not change.

Targets in 2027:

$142.00 (+18.2%)

$187.00 (+55.6%)

Copper (HG): Red Metal Rally or Rusty Bet?(1/9)

Good afternoon, everyone! ☀️ Copper (HG): Red Metal Rally or Rusty Bet?

With copper at $4.88 per pound, is this industrial darling a steal or a trap? Let’s dig into the dirt! 🔍

(2/9) – PRICE PERFORMANCE 📊

• Current Price: $ 4.88 per pound as of Mar 13, 2025 💰

• Recent Move: Up slightly this week (Mar 10-13), per data 📏

• Sector Trend: Industrial metals volatile, with tariff impacts 🌟

It’s a mixed bag—let’s see what’s driving the price! ⚙️

(3/9) – MARKET POSITION 📈

• Global Demand: Key in construction, electronics, renewable energy ⏰

• Supply Dynamics: Major producers in Chile, Peru, China; tariff risks loom 🎯

• Trend: Green energy demand up, but economic slowdowns could dampen growth 🚀

Firm in its industrial roots, but facing new challenges! 🏭

(4/9) – KEY DEVELOPMENTS 🔑

• Trade War Escalation: U.S.-China tensions on Mar 13, 2025, per data, could hit supply chains 🌍

• China’s Response: Uncertain, but likely to affect prices due to its role in copper 📋

• Market Reaction: Prices volatile but up slightly, indicating cautious optimism 💡

Navigating through geopolitical storms! 🛳️

(5/9) – RISKS IN FOCUS ⚡

• Economic Slowdown: Reduced industrial activity could lower demand 🔍

• Supply Disruptions: Tariffs or geopolitical issues could disrupt supply, per data 📉

• Substitution: Other materials or technologies could reduce copper’s importance ❄️

It’s a risky ride, but potential rewards are there! 🛑

(6/9) – SWOT: STRENGTHS 💪

• Increasing Demand from Green Energy: Solar panels, wind turbines, EVs require copper 🥇

• Industrial Staple: Essential in construction and electronics, ensuring steady demand 📊

• Price History: Historically, copper has been a good long-term investment, especially during expansions 🔧

Got solid fundamentals! 🏦

(7/9) – SWOT: WEAKNESSES & OPPORTUNITIES ⚖️

• Weaknesses: Price volatility due to economic cycles and supply disruptions 📉

• Opportunities: Expansion in emerging markets, new applications in tech and infrastructure 📈

Can copper shine through the challenges? 🤔

(8/9) – 📢Copper at $4.88 per pound—your take? 🗳️

• Bullish: $5+ soon, green energy boom drives prices up 🐂

• Neutral: Steady, risks and opportunities balance out ⚖️

• Bearish: $4 looms, economic slowdown hits demand 🐻

Chime in below! 👇

(9/9) – FINAL TAKEAWAY 🎯

Copper’s $4.88 price reflects a mix of optimism and caution 📈. With green energy demand rising but economic and geopolitical risks lingering, it’s a volatile market. DCA-on-dips could be a strategy to average in over time, banking on long-term growth. Gem or bust?

Will Copper Shine Brighter than Gold?Intricate dance between gold and copper prices is a tale beyond mere metals. It reflects global economic sentiments, industrial demand, geopolitical angst, and investment trends.

Gazing into the crystal ball to decipher the future of the gold to copper ratio, a fascinating narrative unfolds, particularly highlighting copper's brighter prospects.

Copper is displaying record futures premium unseen since 1994 fueled by supply side concerns. Beacon of positive economic data from China, is helping Copper shine brighter than Gold.

This paper delves into the forces propelling copper and illustrates how portfolio managers can use the gold-to-copper ratio to gain risk reduced exposure to copper’s ascent.

COPPER SUPPLY IS FACING PLENTLY OF HEADWINDS

Mined copper and Refined copper are facing potential supply disruptions.

Copper miners have benefited from the growth in supply over the past year. Australian mining giants reported higher annual copper production (BHP up 7% and Rio Tinto up 3%). Both benefited from a higher realized price.

Copper mining costs for Australian miners were higher due to outages. While copper operations have done well, other commodities have not. Iron Ore, Aluminum, Platinum Group Metals, and Nickel prices are performing poorly. This has negatively impacted performance of mining majors. BHP profit was flat while Rio Tinto was down 9%.

It is likely that miners will start scaling down production to boost profitability. Some have already started. For instance, Anglo American announced that it would lower its copper production guidance by 20% to 730k-790k tonnes.

Mine outages are another source of concern. Macquarie Bank highlighted that disruptions remain elevated resulting in supply deficit of 700k tonnes in 2024.

Copper shortage risks exacerbating the ongoing raw material shortage at refiners. Chinese copper smelters announced a rare joint production cut last month due to shortage of ore. Consequently, Chinese copper spot treatment charges (measure of refiner profits) plunged 75% in merely two months.

Recent guidance from BHP (+7%) and Rio Tinto (+11%) point to a sharp increase in copper production signaling strong demand. Rio Tinto’s own smelter projects are coming back online this year, and its guidance suggests refined copper production will surge 40%. This will exacerbate ongoing raw ore shortage.

COPPER FUTURES PREMIUM SURGES TO HIGHEST SINCE 1994

Potential supply disruptions are evident in the market. The contango for copper futures on CME Group is sharply steeper signaling even higher prices in the future.

Source: CME QuikStrike

Front-month futures are trading sharply higher than the spot price. According to Bloomberg, the gap between LME copper 3-month forward and cash market is at its highest since 1994. Copper prices are clearly sensitive to supply side shocks.

CHINA’S RECOVERING ECONOMY SUPPORTS COPPER DEMAND

Copper prices are shining bright. Supply constraint is not the only reason. Demand outlook is promising. Chinese economy has started to build up pace. Outlook however remains uncertain.

Copper is overwhelmingly impacted by industrial and manufacturing activity and growth. Caixin’s China manufacturing PMI surged from 50.9 to 51.1 in March. It marked the fifth consecutive month of manufacturing expansion which augurs well for copper demand. However, demand side headwinds remain. Besides manufacturing, housing is a key sector driving copper consumption. Housing construction consumes copper for wiring and piping. Persistent housing slowdown will drag down copper demand.

TECHNICAL SIGNALS POINT TO BULLISH COPPER

COPPER

GOLD

Both copper and gold exhibit strong bullishness. Technical signals for copper are marginally greater than those for gold. Copper shows stronger positive momentum according to RSI while Gold’s momentum is fading. Gold also faces resistance at its R1 pivot point while copper has found support at its R1 pivot point.

OPTIONS MARKET BODE WELL FOR COPPER RELATIVE TO GOLD

Positioning on CME options market signals that both copper and gold have a bullish outlook. However, copper’s put/call ratio is lower, indicating a more bullish sentiment. Unlike gold, copper has seen a buildup of bullish positioning over the past week too.

COPPER

CME copper options have a put call ratio of 0.44 as of 4/April.

Source: CME QuikStrike

Changes to open interest have been bullish with a larger growth in calls relative to puts over the past week.

GOLD

CME gold options have a put call ratio of 0.72 as of 4/April.

Source: CME QuikStrike

Puts open interest has been on the rise, especially in near-term contracts over the past week.

COMMITMENT OF TRADERS ALSO FAVOR COPPER OVER GOLD

COPPER

Asset managers have switched from net short to net long positioning over the past month in CME copper derivatives. However, the most recent report shows short positioning being built up sharply.

GOLD

Asset managers built up a large net long position beginning March in COMEX Gold. Since then, positioning has since remained unchanged at net long. Asset managers have also been consistently scaling back short positions over the last month.

HYPOTHETICAL TRADE SETUP

Copper is faced with the potential of worsening supply disruptions. Supply of raw ore for refiners is already disrupted, forcing them to become unprofitable.

This situation is likely to worsen as Rio Tinto’s smelting plants come online through the year consuming even more raw ore. Supply of ore is also being cut by miners as they face unprofitable conditions.

Supply of ore is also rising. Australian miners stated that production is expected to rise this year. Supply may become resilient if refiner’s scale back production.

Demand favors copper with consistent economic recovery in Chinese manufacturing. Housing remains a headwind creating downside risk to demand. Copper prices are high and so is uncertainty on the path ahead. Prices are up 10% YTD as of 4/April.

As such, a straightforward long position is risky. Demand at present is not higher, as suggested by the spot discount. In case the disruptions do not materialize, prices could pull back sharply.

Alternative to an outright position in copper is the Gold-Copper ratio which exhibits strong mean reversion.

The ratio is also elevated right now, owing to the massive rally in gold prices through 2024. Gold is trading near its all-time high, which is limiting demand and further price appreciation. Contrastingly, copper is still far from its highs of 2022.

Expecting copper outperformance, a short position in the gold-copper spread can be used to gain exposure to copper’s tailwinds with lower risk.

The following hypothetical trade setup comprises of a long position in CME Micro Copper Futures and a short position in CME Micro Gold futures. The position requires two contracts of Micro Copper for each contract of Micro Gold to balance the notional values. Each Micro gold contract provides exposure to 10 troy ounces of gold (representing a notional value of ~USD 23k. Each Micro copper contract provides exposure to 2500 pounds of copper (representing a notional value of ~USD 10.6k).

• Entry: 558

• Target: 531

• Stop Loss: 567

• Profit at Target: USD 1,402

• Loss at Stop: USD 333

• Reward-Risk: 4.2x

MARKET DATA

CME Real-time Market Data helps identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed. Please read the FULL DISCLAIMER the link to which is provided in our profile description.

$CLF metals get a bounce as market steady & value catch-upCleveland-Cliffs the steel producer looks cheap here. CEO has been working to reduce the blast furnace emissions which gets them a lot of praise. Cleanest steel produces in the world. CLF is vertically integrated and the fact it produces its own ore is huge. May acquire US Steel before year ends which would give this company a lot of power when it comes to the steel market. Looking for at least 18 in the short-term.

$CENX A Cyclical Industrial Metal Stock for the Cold HeartsAluminum is a highly cyclical sector just like other industrial metals. If you think the cycle continues, this is the sport to buy at trough levels. It could get cut in half if things get ugly. If things go okay and demand rises and the sector tightens, this stock can travel to $25-30 quick like it has several times before. Small investment. AA Alcoa Corp is a less risky big cap aluminum stock.

TSXV primed for a BULL RUN, which means SO ARE MINING STOCKSFor those into junior mining stocks, one of the best indicators of a bull run is the TSX Venture Exhange. Typically, when this chart bounces off oversold territory, it has led to strong bounces for most miners on this exchange and the overall mining sector.

A positive divergence is forming on the monthly. No guarantee it will hold up, but something to keep an eye on for sure.

Copper - has a history of crashing violently.As a industrial metal

When the economy slows

the price of copper nosedives

as we saw last summer when that neckline was breached

Can we see the same again? sure

But electric cars???

What of Tesla . Rivian, BYD

makes you wonder, hey?

Nickle Finds long term supportNickle Commodity Index DJ:DJCIIK

Monthly Chart

- Long Term Support Line (holding)

- DSS Bressert Cross ideal (TBC)

- On DSS cross confirmation you could enter a

trade or enter at current price & place a tight

stop under the Long Term Support line to protect

your position.

Industrial metals continue to face headwinds as Chinese data disIndustrial metals were the worst performing commodity sector last month and were down 2.7%1. Over the last six months, the sector is down 15.2% and has created the biggest drag on the overall performance of commodities.

China's real estate sector, once the engine of its economy, is now teetering on the edge of crisis because of excessive borrowing, overbuilding, and a housing slowdown. The government's crackdown on risky practices and sudden intervention in 2020 to prevent a housing bubble have led to over 50 Chinese developers defaulting or failing to make debt payments in the last three years. The consequences include reduced consumer spending due to falling housing prices, disappearing jobs tied to housing, and decreased business confidence. While policymakers have taken modest steps to address the situation, the real estate turmoil has spread to financial institutions and the broader economy, prompting concerns of a larger crisis. A build-up in industrial metal inventories over the last 3 months is consistent with market expectations of ample supply of the metals for the rest of the year, given relatively modest demand. Zinc inventory is up 96% while lead inventory is up 85% compared to 3 months ago.

This is clearly weighing on sentiment towards industrial metals. Copper (COMEX) was down 2.8%1, and aluminium down 2.8%1. The only bright spot in the basket was lead, which was up 3.7% last month. Speculative positioning in COMEX copper has been oscillating between positive and negative territories in recent months and entered negative territory again last month after briefly becoming positive2. COMEX copper inventory is up around 46% compared to 3 months ago. And although copper held in COMEX is one of the smaller stores of the metal, when combining London Metal Exchange, Shanghai Futures Exchange and COMEX, copper inventory is still 27% above where it was 3 months ago.

Nickel was down 5.7% last month1. Although nickel is widely known for its use in electric vehicle batteries, a growing market, it still draws around two-thirds of its overall demand from the production of stainless steel. China's steel market has been facing pressure in August due to continued high steel production despite sluggish end-user demand. Blast furnace utilization rates have risen, but some local mills in key steelmaking provinces like Hebei and Jiangsu have not received official communication about output reductions. Uncertainty surrounds the extent of China's steel output cuts for the rest of the year, with expectations of smaller scale cuts targeting environmentally sensitive regions. Rising steel inventories are attributed to robust production and weak demand. Despite potential production cuts, market sentiment remains cautious due to these challenges, and steel prices have declined. This, in turn, is weighing on nickel.

Source:

1 Bloomberg as of 21 July 2023 to 21 August 2023

2 Commodity Futures Trading Commission (CFTC) as of 15 August 2023

3 change in inventory over the past 3 months by United States Department of Agriculture

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Silver ~ Snapshot TA / Bullish ConsolidationTVC:SILVER rallying to the upside & revealing its Bullish inclinations ahead of key Global Economic events.

Fibonacci Extension doing a great job identifying key Demand/Supply zones to watch for smaller-timeframe trend rejection/continuations.

Dashed horizontal lines (~25.26/~22.21) highlight key Make or Break levels for longer duration Swing Trades.

Golden Pocket/Gap Fill confluence presents interesting Stink Bid opportunity if Silver price action turns to disaster.

Boost/Follow appreciated, cheers :)

OANDA:XAGUSD COMEX:SI1! COMEX:SI2!

$PAAS: Weekly trend confirms on close, daily bullishI like the setup in $PAAS here to get some #Silver exposure now that silver's trend is bullish in the daily and weekly can fire a spectacular signal in it soon.

Best of luck!

Cheers,

Ivan Labrie.

Industrial Metals: Copper the king of green metals!I have a long-term positive outlook on the industrial metal sector given the increase in demand towards the electrification of the world.

I expect a dampening in shorter-term prospect however a renewed surge to fresh record high's in the new year by miners around the world, most notably from Central and South America as well as Africa.

This will lead to copper gaining momentum due to electrification of the world (Less dependency on Russia). Massive amounts of new copper is needed in the years ahead for the power grids to cope, we are already seeing producers like Chile, the world’s biggest supplier of copper, struggling to meet production targets. China’s slowdown is viewed as temporary and the economic boost through stimulus measures is likely to focus on infrastructure and electrification—both areas that will require industrial metals.

I have chosen Freeport-McMoRan Inc. as my trade idea, often called Freeport. Freeport is an American mining company based in the Freeport-McMoRan Center, in Phoenix, Arizona. The company is the world's largest producer of molybdenum, is a major copper producer and operates the world's largest gold mine, the Grasberg mine in Papua, Indonesia. FCX is looking strong with a strong financial situation and growing Inventories at good levels. Copper demand is increasing, electrification around the world will continue into the future.

Industrial metal cyclicality is only skin-deepIndustrial metals prices are traditionally cyclical

Industrial metals have historically been cyclical. In this current downturn, we are finding that metal prices are suffering, as they have done in the past.

However, the importance of base metals in delivering the energy transition has never been greater. We are currently living in an energy crisis exacerbated by the war in Ukraine. Europe wants to accelerate the energy transition to reduce reliance on Russian energy sources. That will place a higher onus on renewable energy sources coupled with battery storage to meet our energy needs. In short, that will require a lot more metals. However, the production of many base metals is declining. That’s partly due to falling prices, making it more difficult to justify the capital expenditure. Also, high energy prices are making the smelting of metals uneconomical1.

We believe there is a risk of supply destruction of base metals due to the energy crisis being greater than the demand destruction coming from a decelerating economy. So, while sentiment may be weighing on metal prices right now, the fundamentals may be tighter than the market assumes. That could pave the way for a substantial rebound in metal prices when the market refocuses on supply imbalance and sentiment turns.

Inventories are low

It is clear from the table below that industrial metal inventory is especially low. We do not believe the year-to-date price performance reflects that degree of tightness. And there is ample room for an upward correction.

Most base metals are in backwardation

With the exception of aluminium and nickel, all base metals are in backwardation. Backwardation is when spot or front-month futures contracts are priced higher than the price of contracts for delivery in later months. The fact that someone is willing to pay for immediate delivery rather than entering a contract for delivery in a few months’ time indicates that they need the material urgently. Thus, the backwardation structure of futures markets is another indication of market tightness.

Production is hampered

Surprisingly, aluminium and nickel are not in backwardation like the other base metals. The inventory table seems to indicate that metal availability is the worst for these two metals. Looking at European aluminium production data this year (to July 2022, the latest data point available) relative to production in 2021 over the same period, production is down 11%. A surge in China’s summer temperatures in August 2022 has led to a power crisis, resulting in curtailed power supply to the industrial sector in Sichuan province. Aluminium is very energy-intense to produce.

Inflation Reduction Act and European policy on energy transition

European policymakers are currently debating the path to secure energy independence from Russia. In her State of the Union speech on 14th September 2022, Ursula von der Leyen, President of the European Commission, emphasised investing further in renewable energy and hydrogen in particular. These investments will be metal demand positive.

In the US, the Inflation Reduction Act, which was signed into law in mid-August, sets out several initiatives to reduce inflation. The US also recognises that energy reform is part of the puzzle. The bill includes circa $390Bn of spending/credits over the next ten years related to energy and climate change, with the goal of putting the US on the path towards 40% emissions reductions by 2030.

The bill takes steps to enhance energy security and provides credits to help tackle climate change. There are incentives for cleaner fuels (e.g. hydrogen), for consumers to electrify appliances/upgrade home energy efficiency, and tax credits for buying electric vehicles. We expect the bill will be metal demand positive.

Conclusions

We believe supply destruction is occurring at an equal or faster pace than demand destruction in the base metals space. However, metal prices are currently falling, mirroring historical cyclical patterns for industrial metals. When markets refocus on the fundamentals, we may find prices correct to the upside. Our long-term projections for industrial metal demand – underpinned by an infrastructure rebound and energy transition – remain firm.

Sources

1 See Zinc and aluminium supply tightening amid energy price shock

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Zinc and aluminium supply tightening amid energy price shockMore and more metal smelters are falling victim to the European energy crisis. Last week, Nyrstar, a large European zinc smelter, announced it would shutter production at its Dutch Budel facility from 1 September 2022 and Norsk Hydro, a significant aluminium producer in Norway, said it will close its Slovakian smelter around the same time.

Aluminium is one of the most energy intense metals to produce, leaving the metal very sensitive to soaring energy prices. Drought in parts of China is also reducing the availability of hydropower. Energy rationing in China resulting from this is likely to see a decline in aluminium production from the largest producing country.

In July, the European Union agreed that it would ration natural gas by 15% until spring 2023. That will mean the Union will have to depend on other forms of energy or cut back on economic production.

The production halts are likely to deepen recession risks in Europe. However, if demand for these metals does not fall as quickly as the supply is contracting, we may find base metals markets significantly tighten.

Inventory in decline

Supply of both zinc and aluminium is already looking tight. London Metal Exchange (LME) inventory of zinc has pared back to pre-covid levels and sits at only 6% of the level seen at the peak in 2012. You would have to go back to the 1990s to see LME inventory of aluminium as low as it is today.

Underappreciated story

While zinc prices popped higher on the day Nyrstar announced its closure, the metal's tightness appears to be an underappreciated story. Net speculative positioning in zinc futures is at the lowest it has been since 2018 and more than 1.5 standard deviations below the 4-year average. Positioning in aluminium is also below average but not as extreme.

Energy transition to boost demand for both metals

Both metals are essential for the energy transition that is required to meet global climate goals. Aluminium is needed to lighten vehicles to reduce their energy needs and is a key element in electrical infrastructure, solar panels and wind turbines. Zinc coatings protect solar panels and wind turbines and prevent rust. A 10MWh offshore wind turbine requires 4 tonnes of zinc, while a 100MWh solar panel park—enough to supply 110,000 homes—requires 240 tonnes of zinc1.

The EU is focused on energy security today as it tries to wean off Russian energy dependency. It will be pushing the energy transition harder as a result.

Zinc backwardation underscores tightness

Zinc is also one of the most backwardated base metals2. Backwardation is when front-month delivery futures prices are higher than the second or third-month delivery prices. That is also an indication of market tightness, i.e. that people are willing to pay more for immediate delivery rather than wait a couple of months, indicating they need the metal soon and it is in high demand. Investors in rolling futures strategies tend to benefit from markets in backwardation: as the futures approach spot prices as time passes, the price should rise (assuming the curve shape remains the same).

Conclusion

The energy crisis in Europe and elsewhere is driving supply challenges in the base metals market. There have been notable smelters shuttered in zinc and aluminium. Zinc stands out as a metal with low speculative length, indicating an underappreciated story.

Sources

1 Word Economic Forum

2 See Commodity Monthly Monitor, July 2022

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Not a silver lining.Silver is special as it is both an industrial and precious metal. So, let’s look at Silver from both points of view to identify what seems to be dimming the shine on this metal.

As a precious metal, we can compare silver with the dollar and yield as both affect the demand for precious metals. Dollar and silver are generally negatively correlated, with a stronger dollar leading to weaker silver. In the chart below, we see this relationship at play until the start of February 2022, when it started to weaken. It seems the effect of a rapidly strengthening dollar has not been reflected in the prices of silver and we expect this gap to close, resulting in lower silver prices.

The 10-year yield also provides us with a reference to understand where silver might trade at. A high yield environment is often considered headwind for precious metals as investors prefer holding yield-generating assets in such periods. In the chart below, we see can observe the roughly negative relationship between yields and silver, with periods of lower rates showing higher silver prices and vice versa.

With the Federal Reserve indicating that they are still not done with the rate hikes to combat inflation, silver might take a dent in upcoming rate hikes.

Secondly, we can look at business and consumer confidence to gauge the potential demand for silver as an industrial metal. Generally, higher business and consumer confidence indicate expansionary periods, which translate to higher demand for industrial metals. With the University of Michigan consumer confidence index at a low and United States Business Confidence Index turning lower, such negative outlook will slow demand for silver as a form of industrial metal, potentially adding resistance to prices.

On the technical front, silver is sitting right on the 19-dollar level, which has acted as a key support & resistance level over the past 10 years. An attempt to breach this level a few weeks ago was rejected and prices are now back to retest this support. On a shorter timeframe, we also see silver in a descending channel pattern indicating a downwards continuation pattern.

With the dollar strengthening, higher yields, and downbeat business and consumer confidence, the macro backdrop for silver does not look rosy. Overlaying that with the bearish technical price action, we think Silver is likely to struggle.

Entry at 18.960, stops at 20.160. Targets at 16.620.

The charts above were generated using CME’s Real-Time data available on TradingView. Inspirante Trading Solutions is subscribed to both TradingView Premium and CME Real-time Market Data which allows us to identify trading set-ups in real-time and express our market opinions. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

Disclaimer:

The contents in this Idea are intended for information purpose only and do not constitute investment recommendation or advice. Nor are they used to promote any specific products or services. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios.

What’s hot: Which party will industrial metals attend?While the Federal Reserve, European Central Bank and other developed world central banks are removing the punch bowl from the party, the People’s Bank of China (PBOC) is serving the Baijiu . Industrial metal prices could lift as they move to the afterparty.

Developed world central banks removing the punchbowl

Increasing fears of an economic recession are weighing on commodity prices as many developed nations’ central banks rev up their fight against inflation. As hawkish central bank headlines dominate the press, commodity prices are increasingly ignoring the underlying tightness in supply of many commodities. The US June 2022 Consumer Price Index inflation print from last week, which surprised once again to the upside, has increased the market’s conviction that the US Federal Reserve will raise Fed fund rates by anywhere between 75 and 100 basis points when the Federal Open Market Committee convenes on July 27th. The European Central Bank is likely to exit negative interest rates by September and commence its first increase in the Refi rate since 2011.

PBOC serving the Baiju

But while many investor’s eyes are focused on these developed market central banks, the People’s Bank of China has been loosening its monetary policy setting for several months. China has been grappling with slower economic growth for most of this year due to the country’s zero COVID policy. Q2 2022 grew only by 0.4% y-o-y, missing the 1.2% expectations and 4.8% from the prior quarter. Hence the central bank has been easing policy for some time. That effort is starting to show in aggregate financing to the real economy (Figure 1) . Not only was the reading higher in June 2022 than the average since 2017, but it is also close to the reading from March 2020 when extraordinary efforts were made to help avert the Chinese economy falling off a cliff when COVID-19 became a global pandemic.

Metal demand to rise

Historically, a boost in aggregate financing to the real economy in China has been accompanied by a boost in demand for metals. Figure 2 illustrates the case for China’s copper demand. Given that China accounts for more than 50% of demand for copper, nickel, zinc and aluminium , this is meaningful for the supply-demand balance of all metals used in infrastructure.

China’s government encouraging more infrastructure spending

In addition to central bank policy loosening, the government has been also providing stimulus. In April 2022, President Xi called for an “all-out” effort to construct infrastructure. Proposed projects ranged from waterways and railways to facilities for cloud computing. Back in April however, words felt cheap. Today, we are seeing evidence of government financing support. In July 2022 media reports claimed China’s Ministry of Finance is considering allowing local governments to sell 1.5 trillion yuan ($220 billion) of special bonds in the second half of this year. These special bonds are traditionally used to raise money for infrastructure spending. In aggregate, according to Bloomberg calculations, China is making 7.2 trillion yuan (US$1.1 trillion) available for infrastructure spending. That represents a decisive move away from the focus on debt control from last year.

Conclusion

While China faces several challenges ranging from falling property sales to private market reluctance to invest in infrastructure during uncertain times, we believe the strong lift in aggregate financing to the real economy and government support for financing infrastructure bode well for an infrastructure rebound. Along with that will be a boost for metal demand. China’s outsized presence in metal demand will be felt in prices once the initial shock of developed market central bank hawkishness abates.

Sources

1 Baijiu, a traditional alcoholic drink from China is the most-consumed distilled spirit in the world (Source: londonspiritscompetition.com)

2 Total social financing (TSF) refers to the aggregate volume of funds provided by China’s domestic financial system to the private sector of the real economy within a given timeframe. It includes financing from the following 10 sources: RMB loans; Foreign currency loans; Entrusted loans; Trust loans; Undiscounted bank bills of acceptance; Corporate bonds; Non-financial corporate domestic equity financing; Insurance company repayments; Investment property; Financing via other financial instruments.

3 Source: IMF Special Focus Report 2018: Changing of the Guard - Shifts in Industrial Commodity Demand

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Remember Copper? Time to buy (not advice)Hello. I talked about Copper back in March, and then in May, ideas linked below.

It has been 6 months, and after patiently waiting well here we are.

From a "George Soros investment tips" article:

"Short term investing, it must be stressed, is not like day trading. Day trading is really kind of a myth. You can’t just sit at home, follow stock trends and expect to turn a profit from one day to the next. Short term means waiting for months to expect any return on your investment."

Well I did wait 6 months. George Soros waits to buy for months, then he buys, waits for weeks, and then his gains happen over a few days. This is more what I'd expect. Seems like it always works this way.

Don't have much to add about the price going up, now is just the time to buy for me, not much has changed.

Wyckoff spring? Upthrust? Something something. Doesn't matter.

In the short term there was some FUD about China demand which helped create the down movement (typical).

In the medium term USD goes down, commodities go up, maybe energy makes it worse, green transition demands lots of material...

There is a lot we can read about copper, well a bit, not a lot compared to Oil or Bitcoin but still, enough. They talk much about the risk, it could not go up and so on. Great, noob retail gamblers, hedge fund managers, industrials and other hedgers are being careful, wait and see. Best to wait and see, because of the risk. But me? I want the risk, someone has to take it. Yes please give me the risk that's my job. Not for hedgers or gamblers. I'm as close as it gets to being stopped or winning without a greedy entry that would cause me to always miss out. Top inflexion point. Here if it goes to ~$5 I think I'll be making 10 times what I'd lose if stopped. I'm here to enter at the maximum risk, maximum "we don't know let's wait and see", I'm here to take hits.

Once there is certainty we'll probably be close to the top, and there might be a big violent correction with the gamblers snatching profits, also of course the miners want to sell, then the hedge funds that want certainty will be looking to get in on that correction. Not sure what I will do, probably weak hands once I'm at a high multiple of my risk. Probably just take another hit though.

Bullish pump in Rhodium?If the 200 period MA supports the price, it seems like a good buying opportunity with a stop-loss order below the local low at 1750 USD. Price quotations over 1900 USD are a good sign for continuing the bullish trend. At least targeting the ATH at 2600 USD.

Industrial metals are set to witness an upcoming rally

Industrial metals are set to witness an upcoming rally after Joe Biden's $6T budget proposal, The spending plans would fund investments roads, water pipes, broadband internet, electric vehicle charging stations and advanced manufacturing research.

CENX is an industrial metal stock that's being traded within a descending channel on the 4hr time frame since March 12.

Momentum and strength indicators are supporting that the stock would move upward to hit $14.65 and $16.25 levels consequitvely on the short term.

Century Aluminum shares CENX rose 7.62% in yesterday's trading in a strong session for metals.

Potential routes for Silver price in the upcoming PM bull runFirst route is based on 2008 bull market in silver.

Second route is based on the bull market in late 70s.

I think a bullish phase similar to late 1970s makes the most sense. You can check out my analysis on Gold to see why.

Copper close to complete the measured move!Copper has a healthy stair-step trend, with mid-term consolidations after big rally's, as drawn in chart.

We are about to make the measured move which I projected in my last chart on this ETF, at this point I expect we could enter a period of consolidation.

Risk Management

I will tight my exits to the 5-day moving average once we complete the measured move. That way I can still be in it if it continues to rally, but will secure my gains which I set in my initial plan.

To see the initial plan and breakout setup, click on related ideas "Copper breaking out"

Infrastructure Bill helping SteelTechnical Analysis

We are breaking out to a 52-week high, with heavy volume (100%+ stronger volume intraday vs its 10-day average volume)

First measured move target is at $32, which is coincidental with a Fibonnaci 61.8% level.

OBV is supportive of the overall uptrend.

~~~

Take a look at USCR (US Concrete) which is rallying in my opinion based on the same infrastructure scenario.

If you would like a chart analysis on this symbol, please let me know.