No trades on EURUSDEURUSD continues holding around 1,0700 and no still no entry grounds.

US inflation data is coming on Wednesday and ECB interest rate on Thursday.

Upon continuation of the correction resistance levels will be 1,0780 and 1,0846.

We will be looking for new trades after the news upon good ratio.

Inflation

Lower High, and probably a Lower Low.The market is showing signs of weakening. After the previous high didn't take out the highest high it made on January 22, the momentum started to weaken. The volume is going through a bearish cycle and the VIX is starting to show signs of waking up. The interest rates haven't receded and there are signs of an economy slowdown with upticks in the unemployment and the reduction of the inflation.

The oil market went high, but along with oil production cuts, which means the oil cartels are trying to keep the prices high not by increasing demand, but by reducing supply. This means the economy is reaching the point where more oil is not needed, it's peaking its recovery cycle.

All these ingredients signal we're reaching a level where the overall economy has peaked. It must slow down to allow the inflation to go down, and the so called soft landing would mean the unemployment would not be harsh while the Fed reaches its economic goals. However that is not a guarantee, let's remember we went through a flood of cash after the pandemic, which was what triggered the worst inflation in decades.

Previous bubbles have been because of different reasons, too much debt to enter the raising market, too much interest in tulips, too much promissory e-commerce, the real estate bubble, ... and the story repeats itself, just with different actors. I would call this one the cash bubble, and it is far from over.

Let's remember the printed bills are endorsed by faith, by the believe that they are worth something and the fact that the only one who can legally print them is the government. But they're worthless by themselves. They are not Money, they are tokens that represent money, the money is produced after the productivity of the economy, how many people are in the workforce, how productive the companies are, how efficient the distribution networks are, and the fact that there are transactions going on in the economy, but if there are more tokens (printed bills) than economic activity their value is reduced, and prices are higher (inflation), until the economy catches up with the amount of currency in the market.

My forecast here is that if the Federal Reserve senses a slowdown in inflation, then they will start pivoting the interest rates, at which point they will keep them like that for a while to see how the overall economy reacts, trying to curve the inflation, while keeping the economy moving, until it reaches levels that show signs of stalling, like higher unemployment and reduction of GDP. A reduction of interest rates will start to make the institutional capitals to exit the market to bet on a big bearish market, and while the media will be ignoring these signs, the institutions will be dumping assets until it's so evident that the market panics.

Once the market has been slaughtered, while a lot of chickens run headless on the street, and there are signs of capitulation, it'll be when the big institution will start accumulating assets at a discount and with a lower interest rate, just like it has always happened before, and the cycle will repeat. This time, pretty much like the way it happened on 2009 and 2020, with a large amount of cash to be allocated in financial assets.

"Patterns repeat because human nature hasn't changed for thousands of years."

~ Jesse Livermore.

“The investor who says, 'This time is different,' when in fact it's virtually a repeat of an earlier situation, has uttered among the four most costly words in the annals of investing.”

~ John Templeton.

"Buy when there's blood in the streets, even if the blood is your own."

~Baron Rothschild.

Inflation to accelerate again or not?Today, we want to draw attention to the price differences now versus a year ago for multiple assets. While some commodities make a case for the reacceleration of inflation (presuming they continue higher), others do not. We would like to hear your opinion on the subject. Also, feel free to share any other assets we omitted.

Illustration 1.01

Illustration 1.01 shows the daily chart of USOIL (WTI oil), down approximately 2.7% compared to the price 365 days ago.

Illustration 1.02

Illustration 1.02 displays the daily chart of Copper CFD. Its price is up about 11% versus a year ago.

Illustration 1.03

The picture above portrays the daily chart of Aluminium futures, which are nearly flat compared to the price 365 days ago.

Illustration 1.04

Illustration 1.04 shows the daily chart of Platinum CFD. This commodity is up slightly more than 15% versus a year ago.

Illustration 1.05

Illustration 1.05 displays the daily chart of Corn. In the last 365 days, corn lost about 27% of its value.

Illustration 1.06

The illustration above shows the daily chart of Rice futures down approximately 5% versus a year ago.

Illustration 1.07

Illustration 1.07 exhibits the daily chart of Pork cutout futures. The price of this commodity is down more than 6% versus a year ago.

Illustration 1.08

Illustration 1.08 presents a daily chart of Soybean futures. Within the past 365, Soybean futures lost about 3% of their value.

Please feel free to express your ideas and thoughts in the comment section.

DISCLAIMER: This analysis is not intended to encourage any buying or selling of any particular securities. Furthermore, it should not be a basis for taking any trade action by an individual investor. Therefore, your own due diligence is highly advised before entering a trade.

$DXY plows higherTVC:DXY still going strong!

It's highly likely that the retests the recent highs.

We history in the making!

This is the 1st time the US #DOLLAR didn't break down @ major support! It has not withstood a monthly close after peaking.

Does it have enough steam to retest the 2022 highs?

#interestrates #GOLD #SILVER #BTC

EUR/USD falls to 2-month low on soft Services PMIsThe euro is back to its losing ways on Tuesday, after holding steady a day earlier. In the North American session, EUR/USD is trading at 1.0745, down 0.48%. The euro has faltered badly, losing about 2% since Wednesday and trading at its lowest level since July.

ECB Christine Lagarde has been talking about the importance of beating inflation but has shrugged when asked about interest rate policy. Lagarde spoke in Jackson Hole in late August and again on Monday in London, hammering home the messsage that inflation remains too high and the ECB will maintain high rates for as long as necessary in order to bring inflation back to the 2% target.

Lagarde's hawkish message in these speeches gave no hints as to whether the ECB would raise rates at its meeting on September 14th. Perhaps she is keeping the markets guessing, but another reason could be that the ECB hasn't yet decided whether to hike or hold, with doves and hawks at the ECB strongly divided on the next move. Inflation remains high at 5.3% but another hike increases the risk of tipping the weak eurozone economy into a recession.

Lagarde stressed on Monday that it was critical for the ECB to keep inflation expectations firmly anchored. I can only imagine her frustration today on reading the ECB monthly survey which indicated that inflation expectations for the next 12 months remained at 3.4% in July, and rose from 2.3% to 2.4% for three years ahead. Eurozone inflation has been moving in the right direction, but it appears that bringing it back down to target could take years.

Eurozone, German services PMI indicate contraction

The services sector has helped carry the eurozone economy at a time when manufacturing continues to decline. However, the expansion in services came to a crashing halt in August as indicated in today's PMIs for the eurozone and Germany. The 50.0 line separates contraction from expansion.

The eurozone Services PMI for August was revised to 47.9 from a preliminary 48.3 points. This marked the first contraction in services activity this year and was the weakest reading since February 2021. The news wasn't much better from Germany, the bloc's largest economy. The Services PMI was confirmed at 47.3, the first contraction in eight months and the lowest level since November 2022. The euro has fallen about 0.50% in response to the weak services data, another painful reminder of the fragility of the eurozone economy.

EUR/USD is testing support at 1.0716. Below, there is support at 1.0658

There is resistance at 1.0831 and 1.0889

USD/CHF rises as Swiss retail sales fall, Swiss CPI nextThe Swiss franc has lost ground on Thursday. In the North American session, USD/CHF is trading at 0.8835, up 0.59%.

Thursday's Swiss retail sales for July looked awful, falling 2.3% m/m. This follows a revised gain of 1.5% in June. Market attention has now shifted to Swiss inflation, which will be released on Friday. Swiss inflation dropped to 1.6% in July, the lowest level since July 2022. The downtrend is expected to continue in August with a consensus estimate of 1.5%.

Policy makers at the Swiss National Bank have to be pleased with the inflation rate. Switzerland boasts the lowest inflation rate in the developed world and both headline and core inflation are comfortably nestled in the central bank's inflation target range of 0%-2%. Still, the SNB remains wary about inflation, with concerns that increases in rents and electricity prices could push inflation back up to 2%. Food inflation remains high and rose from 5.1% to 5.3% in July.

Unlike other major central banks, the SNB meets quarterly, which magnifies the significance of each rate decision. At the June meeting, the central bank raised rates to 1.75% from 1.50% and hinted that further hikes were coming. The SNB has projected inflation will hit 2.2% in 2023 and 2024, above its target. That means the SNB expects to have to continue raising rates, although, as is the case with many other central banks, the peak rate appears to be close at hand.

In the US, unemployment claims dropped to 228,000 last week, down from a revised 232,000 and below the estimate of 236,000. All eyes will be on Friday's job report, with nonfarm payrolls expected to dip to 170,000, down from 187,000.

The Fed's favourite inflation gauge, the PCE Price Index, increased in July by 0.2% for a second straight month, lower than the estimate of 0.3%. On an annualized basis, the PCE Price Index climbed 3.3% in July, up from 3.0% in June. Service prices rose by 0.4% in July, up from 0.3% from the previous month. The numbers indicate that the Fed's battle with inflation is far from over, and the final phase of pushing inflation down to 2% may prove the most difficult.

USD/CHF is testing resistance at 0.8827. Above, there is resistance at 0.8895

0.8779 and 0.8711 are providing support

Higher for LongerUS inflation data in July 2023 provided mixed signals. While Consumer Price Index (CPI) is moving in the right direction, producer price inflation suggest pipeline pressures are picking up. Core CPI, which excludes often-volatile food and energy costs, rose only 0.2% for a second month in a row . However, US producer prices picked up in July, owing to increases in certain service categories. This likely buys more time for the Federal Reserve (Fed) to deliberate on the future path of monetary policy.

The flows into bond exchange traded funds (ETFs) have been volatile. Over the past year, investors were starting to embrace duration. Investors were positioned for recession, inflation crash, and Fed cuts - evident from $31.7bn inflows to Treasury bond ETFs on pace for a record year2. However, investors are starting to pull out of the biggest bond ETFs devoted to Treasuries. More than $1.8 billion came out of the $39 billion iShares 20+ Year Treasury Bond ETF last week, the most since March 20203. Sentiment toward long-dated Treasuries has soured over the past month amid growing conviction that the Fed will keep interest rates at elevated levels for an extended period. We expect rates to remain higher for longer and are unlikely to see the Fed cut rates until the Q1 of next year amidst a stronger US economy.

Don’t celebrate on disinflation just yet

Overall, the US economy continues to show extraordinary resilience despite monetary constraints and credit tightening. While inflation has shown encouraging signs of decline, we caution that the level remains high. Strong July retail sales raise the risk of a re-acceleration in inflation. The four biggest categories of the ex-auto’s component saw outsized gains: non-store retailers, restaurants & bars, groceries, and general merchandise. Amidst a tight US labour market, with unemployment at historic lows and wages continuing to rise, the downward pricing momentum in the service sector is likely to be at a slower rate. Commodity prices are also beginning to rebound from the weakness seen in Q2 2023. Energy prices have been rising on the back of Organisation of Petroleum Exporting Countries and its allies (OPEC+) production cuts. If commodity prices extend their recent momentum, it could pose upside risks to inflation.

Fed Officials remain divided

Messaging on a somewhat mixed inflation outlook from the Fed Officials remains a mixed bag. One faction remains of the view that rates hikes over the past year and a half has done its job while another group contends that pausing too soon could risk inflation re-accelerating. Fed governor’s Michelle Bowman and Christopher Waller remain in the hawkish camp, hinting at more rate increases being needed to get inflation on a path down to the 2% target.

Futures markets are assigning about a 11% chance of a 25-basis-point rate hike when the Fed next meets on 19 and 20 September4. Additionally, rate cuts have now been completely taken off the table until perhaps later in the Q1 2024. The latest Fed minutes reveal commentary from officials, including the hawks, such as Neel Kashkari, suggest a willingness to pause again in September, but to leave the door open for further hikes at the upcoming meetings5.

Opportunity for a yield seeking investor

It’s been an impressive turnaround since the pandemic when negative real yields became the norm. TINA- ‘There Is No Alternative’ to equities, is over now that evidence of the shift to a 5% world appears stronger than ever. Today investors have the opportunity to lock in one of the highest yields in decades, with US two-year yields paying close to 5% exceeding the yields at longer maturities without the volatility witnessed in the 10-year sector. A resilient US economy is likely to keep interest rates and bond yields higher for longer.

Sources

1 Bureau of Labour Statistics as of 10 July 2023

2 BofA ETF Research, Bloomberg as of 9 August 2022 - 9 August 2023

3 Bloomberg as of 14 August 2023

4 Bloomberg as of 17 August 2023

5 federalreserve.gov as of 16 August 2023

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

The downfall of Sunrun : What next !

Ladies and gentlemen, in today's financial analysis, we focus on Sunrun, examining recent price movements and conducting a comprhensive outlook.

First, we notice something significant: the stock has dropped by 16% from its previous trading zone. This is noteworthy, especially if the stock shows signs of going up again.

Now, let's discuss what happened at the Jackson Hole Symposium. The Federal Reserve Chair, Jerome Powell, talked about raising interest rates, which is different from what other officials said. For example, Patrick Harker from the Philadelphia Fed thought we should keep interest rates as they are. Austan Goolsbee, the Chicago Fed President, was also cautious. He mentioned challenges like high inflation, problems in the supply chain, and the possibility of a big strike in the auto industry. Despite these challenges, he remained hopeful that we can control inflation without causing a recession. He also stressed the importance of using data to make decisions, especially the real interest rate. The stock market liked what he said, and the SPDR S&P 500 ETF Trust went up by 0.8%.

Now, let's look ahead. I believe things might change for $NASDAQ:RUN. This belief comes from seeing other companies in the alternative power generation sector, like NYSE:NEP , NYSE:NOVA , and NASDAQ:RNW , starting to do better based on their recent performance. We've also heard that inflation might not keep going up, which is good news for RUN. In this situation, my plan is to keep a close eye on the market and stay updated on the latest news. I'll make sure to update this report with any new information.

Australian dollar edges up ahead of inflation reportThe Australian dollar is in positive territory on Tuesday. In the European session, AUD/USD is trading at 0.6437, up 0.12% on the day.

China's economic slowdown is bad news for the Australian economy, which counts China as its biggest export market. China's imports have been falling and as a result, commodity prices have dropped, hurting Australia's exports of iron ore and gold to China.

China continues to record weak economic numbers and this will likely be reflected in lower GDP releases, although economic growth is above 5%. The Australian dollar is sensitive to China's economic strength and has declined by around 3% in the third quarter.

The Reserve Bank of Australia meets on September 5th and is widely expected to hold rates at 4.10% for a second straight month. There are clear signs of the economy cooling, including inflation and wage growth easing and a slight rise in unemployment. The RBA would like to extend the pause in rate hikes, with an eye on lowering rates sometime in 2024.

All eyes will be on Australia's July inflation report which will be released on Wednesday. Inflation has been falling, albeit slowly. In June, inflation fell from 5.5% to 5.4% and the consensus estimate for July is 5.2%. If inflation drops to 5.2% or lower, it should cement a RBA pause in September. A higher rate than 5.2% won't necessarily mean a rate hike, but it would likely lower the odds of a pause, which are currently around 90%.

In the US, it is a busy Tuesday with consumer confidence and employment releases. The Conference Board Consumer Confidence index has been on the rise and soared to 117.0 in July, up from 110.1 in June. The estimate for August is 116.0 points. JOLTS Job Openings is projected to decelerate for a second straight month in July, from 9.58 million to 9.46 million.

AUD/USD tested support at 0.6424 earlier. Below, there is support at 0.6360

There is resistance at 0.6470 and 0.6531

Shanghai Stock Market (SSE Composite Index): A Closer LookThe Shanghai Stock Market is like a financial puzzle, and right now, it's showing us some interesting moves.

First, the rise in the 10-year yield from 3-year lows suggests that there might be changing expectations about economic growth, inflation, or monetary policy. This could be due to a variety of factors such as improved economic prospects, inflation concerns, or changes in the global interest rate environment. The central bank also did something important by closing a 5-billion yuan money deal. It's like they're keeping a watchful eye on how money is moving around. On top of that, they pumped a massive 385 billion yuan into the system, which can make things more exciting.

Now, let's talk about Ichimoku Cloud analysis. It's like a weather forecast for the stock market. Right now, it's showing that the market might be heading up, which is a positive sign. However, the cloud isn't very thick. This means we should be a bit cautious.

There's another important sign on this chart. Tenkan points up, suggesting the market might go up soon, even though it's under Kijun resistance line. It's a bit like seeing a green light at an intersection, even if the other light is still red.

So, as we decode these numbers and signals, it's clear that the Shanghai Stock Market is in a state of flux, with various factors at play. Investors will need to stay vigilant, considering both the data and the bigger economic picture to make informed decisions in the coming year.

Why the EURUSD might trade higherFollowing Powell's statement at the annual Jackson Hole symposium – “We are prepared to raise rates further if appropriate and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.” – markets seem more inclined towards expecting another rate hike in the US. This move, in our analysis, provides the Federal Reserve (the Fed) with added flexibility for future decisions. Meanwhile, the European Central Bank (ECB) echoes a similar sentiment, insisting on remaining stringent as the battle against inflation is ongoing.

A dive into headline & core inflation shows a decline in the former for both the EU and US. However, Europe's core inflation remains stubbornly high, without evident signs of decreasing. Further, Europe's robust PMI, in contrast to the sub-50 US print, paired with this sticky core inflation, indicates that the ECB might maintain its tight monetary stance to combat inflation.

The Futures and OIS market can give us some insights on market participants’ expectation of the forward rate path. Here we see similar expectations of an increase in rates before cuts are priced in.

Generally speaking, interest rate differential is inversely related to the EURUSD, hence in the chart above we see this relationship in play with the US-EU Interest Rate, roughly marking out the inverted EURUSD path. From 2019 to 2022, where we saw the rate differential held constant after a period of decrease, the EURUSD traded higher during that period. Hence whether the ECB tightens further or keep in line with market expectations, we see potential for the EURUSD to trade higher given historical precedence.

The US dollar is currently hovering near the upper threshold of a descending channel. The previous 3-times when RSI reached such levels marked the turnaround point for the dollar.

On a longer-term chart, we see the EURUSD trading right above the 1.08 level which has been a key support & resistance level going back to 1970s.

Zooming in, the EURUSD pair now trades on the lower band of an ascending channel with RSI pointing oversold. Again, the past 3 times when RSI were at this level marked the reversal point for the EURUSD.

Hence, whether the ECB reacts with more hikes as expected by market participants, or it stays the expected course, the EURUSD is likely to trade higher as we look back in history. Supported by technical, and the potential for a weaker dollar as it trades near resistance, we favour a long position in the EURUSD Futures at the current levels of 1.0827 with a stop loss at 1.05 and take profit at 1.130. Each 0.00005 increment per EUR in the EURUSD futures contract equals to 6.25$.

The charts above were generated using CME’s Real-Time data available on TradingView. Inspirante Trading Solutions is subscribed to both TradingView Premium and CME Real-time Market Data which allows us to identify trading set-ups in real-time and express our market opinions. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

Disclaimer:

The contents in this Idea are intended for information purpose only and do not constitute investment recommendation or advice. Nor are they used to promote any specific products or services. They serve as an integral part of a case study to demonstrate fundamental concepts in risk management under given market scenarios. A full version of the disclaimer is available in our profile description.

Reference:

www.cmegroup.com

www.cmegroup.com

USD/TRY is to jump in 2023?For the last months, the Turkish lira has been traded near the all-time lows against USD. I think that demand for the lira would shift soon, and it would trigger a breakout of resistance of 18.7 with the first psychological price target of TRY 20 for 1 USD with consolidation near 25 in the second half of the year.

In terms of technical analysis, I do not see any compelling things on the USD/TRY chart.

Therefore, I decided to look at an exotic currency pair with TRY on one side. I have taken Hungarian forint or HUF. Comparing HUF with USD or EUR , we can say, it is a weak currency that has constantly lost its value for the last 20 years. However, against the weakest TRY, HUF is a king. On the TRY/HUF chart, I see an opportunity to breakout of support of HUF 18.4 for TRY until the end of the year. The first target could be 14 with the chance to drop to 10. Keeping in mind that HUF is a weak currency that is now in a temporary good shape against the world currencies, such a possible forint strengthening against the lira could happen only if the latter drop to the majors.

If TRY/HUF is to be 14, and USDHUF is near its essential middle-term resistance of 380. It means USDTRY would be around 27,14. If TRY/HUF reaches 10, USDTRY would be 38. With a magical macroeconomic policy in Turkey, including jumping inflation , artificially low-interest rates in Turkey , and raising interest rates in USD, EUR, and Erdogan's elections in June (and budget spending increase), it doesn't seem impossible to me.

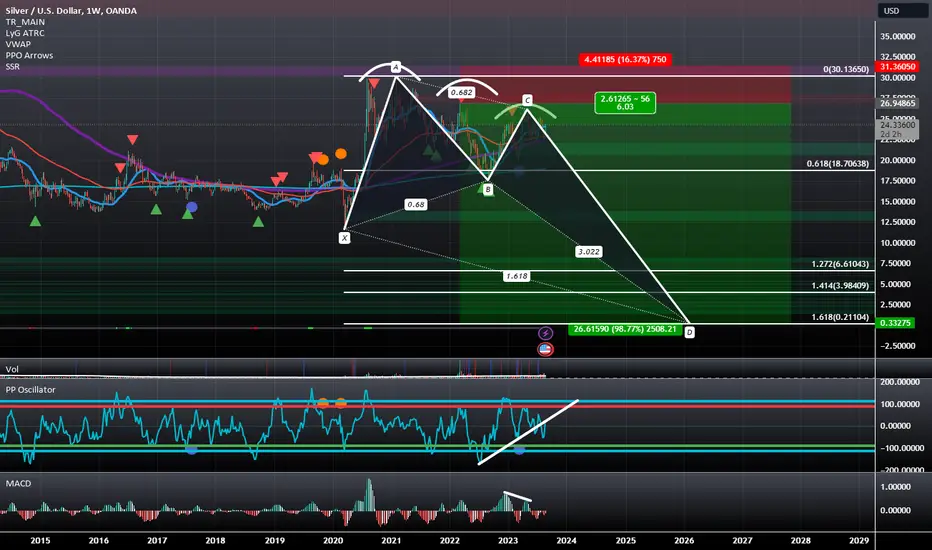

Silver is Setting Up to Drop Down to as Low as 21 Cents.Silver, after confirming Partial-Rise, has also formed 3 Falling Peaks and looks to be preparing to drop back below the bottom end of the range at 18 dollars. When it does this, it will enter a Butterfly BAMM Wave Structure that ends at the 1.272-1.618 Fibonacci Extensions. As a result of this new price action, I am lowering my price target to $6.61-$0.21 from my original $13 target.

Inflation Wears Out Its Welcome in JapanHas anybody ever told you to be careful what you wish for because you might get it? Well, the Bank of Japan appears to be in one of those situations today.

Japan spent three decades oscillating into and out of deflation. As such, when inflation started to rise in 2022, the BOJ was initially thrilled. Finally deflation was coming to an end, and inflation was heading up to a target of 2.5%. The problem is that inflation didn’t stop heading higher at 2.5%. It’s now up to 4.2% excluding fresh food and energy. In a nation with a large elderly population where many people are on fixed incomes, having inflation too high is just as bad has having it too low.

But why should the rest of the world care what happens to Japan’s inflation rate? For starters, Japan has the world’s fourth largest economy, and what happens to the yen and to Japanese bond yields is of worldwide consequence.

Beginning in 2012, the BoJ launched a mega quantitative easing program – four times bigger than what the Federal Reserve did relative to the respective size of their economy. This QE program sent the yen plunging as the BoJ also capped 10-year Japanese government bond yields. But recently, they have softened the cap, sending not only Japanese bond yields higher but raising the cost of long-term borrowings all around the world, including in the United States and Europe.

If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

By Erik Norland, Executive Director and Senior Economist, CME Group

*Various CME Group affiliates are regulated entities with corresponding obligations and rights pursuant to financial services regulations in a number of jurisdictions. Further details of CME Group's regulatory status and full disclaimer of liability in accordance with applicable law are available below.

**All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the author and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

USD/JPY punches above 146, BoJ inflation nextThe Japanese yen has posted significant losses on Monday. USD/JPY is trading at 146.23 in the North American session, up 0.57% on the day. The US dollar has looked sharp and is within a whisker of pushing the yen below the 146 line, as was the case last week when the strong US dollar pushed the ailing yen to a nine-month low.

The Japanese economy was once synonymous with deflation, but that has changed in the era of high global inflation. Japan's inflation is slightly above 3%, a level that other major central banks would take in a heartbeat. Still, inflation is relatively high by Japanese standards and both headline and core inflation have persistently been above the Bank of Japan's 2% target.

Japan's inflation reports are carefully monitored as higher inflation has raised speculation that the BoJ will have to tighten its loose policy. The central bank has insisted that high inflation is transient, but the BoJ wouldn't be the first bank to make that claim and then backtrack with its tail between its legs. Remember the Fed and the ECB?

Last week, July's CPI remained unchanged at 3.3% y/y. Core CPI dropped to 3.1% y/y, down from 3.3%. On Tuesday, Japan releases BoJ Core CPI, the central bank's preferred inflation gauge, which is expected to dip to 2.7% in July, down from 3.0% in June.

China's economic troubles have sent the Chinese yuan sharply lower, with the Chinese currency falling about 5% this year against the US dollar. A weak yuan makes Chinese exports more attractive, but this is at the expense of other exporters including Japan. As a result, there is pressure in Japan to lower the value of the yen in order to compete with Chinese exports.

USD/JPY pushed above resistance at 145.54 earlier today. The next resistance line is 146.41

There is support at 144.51 and 143.64

XAUUSD TRADE RUNNING 260 PIPSDear Ziilllaatraders,

It is with a sense of urgency that we address the current state of the gold market, signaling a marked shift into a bearish territory. The convergence of inflation concerns and impending rate hikes has cast a shadow over the once-gleaming prospects of gold, prompting us to discern this transformation.

Inflation Fears' Impact on Gold:

The recent surge in inflation apprehensions has proven to be a formidable adversary for gold's traditional safe-haven appeal. Historically, gold has served as a hedge against eroding purchasing power caused by inflation. However, the current scenario has witnessed a departure from this historical norm. As inflationary pressures intensify, investors are presented with a broader array of options to preserve and grow their wealth. This has diminished gold's allure, leading to a tangible decline in demand and subsequently exerting downward pressure on prices.

Rate Hike Anticipation and its Ramifications:

Adding to the complexity, the anticipation of central banks implementing rate hikes further compounds gold's plight. Rate hikes are a manifestation of efforts to rein in inflation and tighten monetary policy. In this environment, interest-bearing assets gain attractiveness due to their potential for yielding returns, diverting capital flows away from non-interest-bearing assets like gold. The prospect of higher yields in alternative investments acts as a gravitational force, drawing investors away from gold and contributing to the market's bearish undertones.

Collective Impact on Gold's Bear Market:

When examined together, the dual influences of mounting inflation concerns and the impending rate hikes converge to sculpt a bearish narrative for the gold market. The allure of gold as a store of value and wealth preservation tool has waned amidst the burgeoning options available to investors in the face of inflation. The prospect of higher yields from alternative investments, driven by impending rate hikes, exacerbates gold's descent into the bearish realm.

It is incumbent upon us to acknowledge this transformative juncture with clarity. The prevailing market dynamics underscore the need for a reassessment of gold's role within portfolios and investment strategies. As inflation and interest rate landscapes continue to evolve, our decisions should be informed by a comprehensive understanding of the prevailing economic forces at play.

In conclusion, the confluence of inflation fears and rate hike expectations has orchestrated an unmistakable shift in the gold market's trajectory. The bear market that has emerged serves as an imperative reminder that the interplay between economic factors and market sentiment is pivotal in shaping investment landscapes.

Greetings,

Ziilllaatrades

USD/JPY - yen gains ground as core inflation slowsThe Japanese yen has extended its gains on Friday. In the North American session, USD/JPY is trading at 145.29, down 0.38%.

The month of August has been kind to the US dollar, which has posted strong gains against all of the major currencies. USD/JPY has risen 2.34% in that period and on Thursday, the yen fell as low as 146.56, a nine-month low against the US dollar.

The yen has been the worst performer among the majors over the past month, and the currency's sharp depreciation has raised speculation that Tokyo could respond by intervening in the currency markets. Japan's Ministry of Finance (MOF) shocked the markets in September 2022 when it intervened and bought billions of dollars with yen, which propped up the Japanese currency. At that time, the yen was also trading around the 146 level, and that has many investors on edge that the MOF may be planning another intervention.

Japan's inflation has been hovering above 3% for a prolonged period, higher than the Bank of Japan's target of 2%. The BoJ has insisted that it will not loosen its ultra-accommodative monetary policy until it sees evidence that inflation is sustainable, such as higher wage growth. The markets are not taking the BoJ at its word, as the BoJ keeps its cards very close to the chest in order to surprise the market when it shifts policy. Clearly, transparency is not high on the BoJ's list, in contrast to the Federal Reserve and other major central banks.

Since inflation data could well lead to a shift in policy, every inflation report out of Japan attracts significant attention. The July CPI report, released today, was no exception. Core CPI, which excludes fresh food, eased to 3.1% y/y, matching the consensus estimate and down from 3.3% in June. The indicator is closely watched by the BoJ and the decline supports expectations that the BoJ will maintain its current policy. This, despite the fact that Core CPI has now exceeded the BoJ's 2% inflation target for 16 consecutive months.

The BoJ is not expected to make any major shifts to policy in the near-term, but that doesn't necessarily mean that the central bank will stay completely on the sidelines. At the July meeting, the BoJ surprised the markets with a tweak to its policy which provided more flexibility to the 10-year bond yield cap. Governor Ueda insisted that this was not a move towards normalization, but investors have learned the hard way that the BoJ is not hesitant to make policy moves that have blindsided the markets.

.

USD/JPY Technical

USD/JPY is testing support at 145.71. Below, there is support at 144.07

There is resistance at 1.4640 and 147.31

Nasdaq is ready to drop or surprise us!Next CPI number will be important for SKILLING:NASDAQ , which has been rising like there will be no tomorrow. If we see a hot CPI number, we may see a strong drop towards 14500 area. If core cpi number shows a sign that the sticky part of the inflation is also cooling down, we may see some initial the first steps of the move towards ATH. Let's see if the market will respect the up trend or finally break it down.

Disclaimer – WhaleGambit. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis , like all indicators, strategies, columns, articles and other features accessible on/though this site is for informational purposes only and should not be construed as investment advice by you. Your use of the technical analysis , as would also your use of all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

📈MY TAKE ON THE FED, INFLATION AND CREDIT📊

TLDR: I think the price increase we are seeing is not inflation, the economy is going from bad to worse and the FED's actions don't make any sense.

At the peak of the great inflation of the 70s in USA while both long and short term interest rates were going up together with inflation, so was the aggregate credit.

In fact loans to businesses were growing faster than inflation.

Whereas now, while the short term rates are going up the aggregate credit is going down. Businesses aren’t borrowing and the banks aren’t lending.

And as it was established by Milton Friedman, inflation is exclusively a MONETARY phenomenon.

Therefore price increase followed by unchanged or decreased aggregate credit in not inflation. Which is exactly what we are seeing right now.

It might be attributed to the ongoing effects of the Covid era supply shock which created long lasting bottlenecks, the war in Ukraine or some other fundamental systemic economic problem but it’s not conventional inflation which means that raising interest rates will do nothing but further damage the already weak economy (which is reflected in the unprecedented drop in demand for credit)

So, the further rate hikes that were hinted yesterday by the FED don’t make any sense and we should be expecting a fast race to the zero with more QE when the economic sh*t hits the political fan.

But, let’s wait and see.

As Deflation Hits the Economy The Price of TIPs Should FallEarlier in 2022 I got some Bullish Exposure to Deflation by positioning Bearishly against TIPs (Treasury Inflation-Protected Securities) as can be seen here:

Fast-forward to today and we can now see the CPI declining and the TIPs declining even faster, This ETF Tracks the price of these TIPs and we can see that it is breaking through support even though the CPI has only retraced half way. If the CPI continues on this path and the Bond Market continues to price in Long Term Deflation, we should then see the pricing of this TIPs based ETF come down crashing in a big way. If that does happen, I would target at least the 1.618 Fibonacci Extension.

SPX to 4200 againSPX 500 going to 4200 again, bears are short in heavy this time, fear is back in the markets, maybe 2024 will be a better year...

TSLA Approaches Major Resistance and May Stall into July 21Primary Chart: TSLA on Weekly Time Frame with a Downtrend Line from the All-Time High and Fibonacci and Measured-Move Levels

Preliminary Comments

TSLA is poised to stall soon, perhaps into July 21. By definition, a stall does not necessitate a crash or major trend reversal (at the primary degree of trend). A major reversal downward (crash) is always possible especially once shorts have been decimated—major downward reversals seem to always wait for clearing out of hedging and shorts, right?

Although a major trend reversal could occur here given major resistance levels just overhead on higher time frames, no one has a crystal ball. Finding the time and price components of such a major reversal can be exceedingly difficult (note the conclusion section of this article about probabilities).

And no one who were to have a crystal ball that worked properly would share it. And a securities regulator would be sniffing around for insider trading for sure with too many trades lining up too perfectly especially before major news catalysts. Humor aside, trying to be too clever by calling the exact top is a misplaced endeavor. But it can be prudent to analyze the charts and consider the idea of vulnerability for a trend’s continuation in the short-to-intermediate term, i.e., whether the move might encounter major resistance that could at a minimum cause a mean reversion or retracement of the recent rally .

Trend Analysis

The charts don’t lie. TSLA’s intermediate-term trend since January 6, 2023 remains upward. Similarly, short-term (2-6 weeks) and intraday trends remain upward. But the primary trend is still arguably sideways when considered over a 2-3 year period, while the secular trend since 2010 arguably still remains firmly upward.

1. Secular trend (since 2010): uptrend

2. Primary trend (since 2020/2021): sideways trend (range)

3. Intermediate / secondary trend (since early 2023): uptrend

4. short-term trend: uptrend near crucial resistance

5. intraday trends: uptrend near crucial resistance

Supplementary Chart A: Primary Trend

Supplementary Chart B: Secular Trend

The intermediate term trend has run fast and furious for 1H 2023 (since the Jan. 6, 2023 low). That alone is not enough to expect a reversal. Shorting something merely because it seems to have risen too far is a well-known trading mistake comparable to catching a falling knife in a downtrend. Shorting powerful uptrends is not an easy way to make a living.

But several charts suggest vulnerability for TSLA’s rally at this level. This comes right as earning will be reported this week along with a major monthly options expiration on July 21. Earnings reports like TSLA's upcoming one present a binary risk event that could stretch prices significantly in either direction, or it could a whipsaw price in both directions before settling on a final directional move (see the section below titled “Trend vs. Fundamentals.”)

Supplementary Chart C shows that TSLA’s price is nearing a crucial Fibonacci level on a linear chart. This is the 61.8% Fibonacci retracement ($299.05) of its entire decline from its all-time high into the early January 2023 low. Coincidentally, this level shows confluence with other important resistance levels shown on the chart such as the down trendline from the all-time high. (Some prefer Fibonacci levels adjusted for a logarithmic chart, which is not shown. The next relevant upside Fibonacci level on a log chart, however, is the .786 of the entire decline at $306, which is not far from the .618 level at 295.05.

Supplementary Chart C

If the .618 Fibonacci retracement is overcome and held (not just a false breakout), this suggests prices may run higher to at least $314.67 or the next higher Fibonacci level at $347. But these are upside levels conditioned solely on the .618 retracement being overcome and held.

Next, consider the down trendline from TSLA's all-time high. This is being approached at around $300, right were significant call OI exists. Trendlines can be somewhat rigid measures of trend, but they can provide some value especially when other support / resistance levels coincide with the trendline. The down trendline from TSLA's all-time high runs right into the measured-move zone, shown by the blue circle on Supplementary Chart D.1.

Supplementary Chart D.1

Some traders prefer to look only at logarithmic charts, though here it doesn't add much to the technical picture since the trendline is quite close to where it lies on the linear chart.

Supplementary Chart D.2

Finally, some bearish divergences in momentum and price/volume indicators suggest that price has become quite stretched right at a time when TSLA has reached some major resistance levels. Supplementary Chart E shows the Elder Force Index (EFI), a useful indicator that displays a combination of volume and price, weighing the extent of each price change along with the extent of volume. It tends to pick up divergences in the "force" or commitment behind a move with more sensitivity than RSI or other common momentum indicators, but with increased sensitivity often comes more noise (more false signals) which can be helped to some extent through indicator adjustment. Nevertheless, here is what that indicator shows for TSLA on the daily timeframe:

Supplementary Chart E

As TSLA has made higher highs, it has done so with less force and commitment for each high, creating a divergence between higher price highs and lower EFI highs. TSLA may make a new YTD high this week, and if so, it will be important to see where the EFI high prints for that new high. Given how low EFI is currently, it would take a lot of volume and price change to move the high to exceed the prior EFIs (erasing the divergence). In SquishTrade's view, EFI is unlikely to erase both the June EFI high and the January EFI high even if TSLA runs to $300-$320 post earnings.

Supplementary Chart F shows RSI and ROC, two common momentum indicators which most readers understand well. ROC shows a series of three highs that each make a successively lower high while price made higher highs at the same time: January 2023, June 2023, and July 2023. RSI only shows a series of two highs where price made a higher high and RSI made a lower high.

Supplementary Chart F

Downside Targets

TSLA's price seems poised to pullback / retrace at a minimum. But referring to downside targets may seem a bit premature as price hasn't confirmed even a short-term reversal or the start of a retracement / consolidation within the intermediate trend yet. The technical conditions for a retracement are present, so if confirmation lower does occur in the next week or so, price can fall to trend support, however one decides to measure that within one's trading system.

Based on persistently and deeply inverted yield curves, many astute market players may be looking for more than just a retracement or consolidation within the intermediate uptrend. They want more than mean reversion, and that is understandable. Should TSLA followers expect that now? Today, July 15, 2023, confidence cannot exist about an impending trend reversal on higher time frames. Why? A major reversal where price retests / breaks January 2023 lows will likely coincide with recessionary economic data (e.g., rising UE rates), drastically changing EPS estimates based on disappointing earnings reports, and/or unexpectedly high interest rates across the curve because of sticky inflation won't budge further downward (the recent CPI print came in at 3% for headline but 4.8% for core for June 2023). Note: Fundamentals are discussed in greater depth in the next section below. But economic data has continued to come in better than expected. Recent real GDP print for Q1 2023 was recently raised to 2% and labor markets remain persistently tight as the Fed even has noted in its recent pressers. Inflation has cooled for June but this may result from basing effects.

Most importantly, trend structure on the weekly and daily time frames (intermediate and short-term) has not been broken. Until the intermediate trend structure is decisively broken, forecasting a major top / trend reversal is rash and unfounded from a technical viewpoint. This intermediate-term trend structure is the up trendline from January 2023 lows or some other more dynamic or flexible measures of trend.

So with the idea that price can run a bit higher before any retracement—since we haven't yet seen a confirmation lower yet—these downside targets remain conditioned on a short-term trend reversal. For now, the targets also must be considered corrective retracements / mean-reversion targets within the context of the current trend until the evidence proves otherwise.

Conservative Target: $245-$250

Moderate Target: $232-$238

Aggressive Target: $199-$218

Trends vs. Fundamentals

A purely technical analyst or technically oriented trend trader tends to consider only the trend and technical evidence supporting that objective. At critical junctures after retracements / corrective moves, this means favoring trend continuation rather than a reversal until the evidence says otherwise. And pure trend following means seeing the odds as favoring mean reversion when a trend gets too extended or stretched rather than reversal.

Ambiguity as to trend on varying time frames often confounds the discussion of trends. This is why it's important to remain precise and focused on time frames. For example, a long term secular trend in a given index can be upward while a primary trend can be downward or sideways (retracing / consolidating within the secular uptrend) while an intermediate trend can be upward (retracing or consolidating the primary downtrend)—and intraday traders levered up on calls and riding the short-term rip may be so hyperfocused on a rip in the short term that they dismiss a long-term analyst’s accurate characterization of corrective rally within a primary downtrend. This is just a hypothetical example of how vagueness around terminology and time frames doesn’t can obfuscate the proper technical approach to a given security.

As discussed, TSLA’s trend right now is upward on the intermediate trend and minor (short-term) trends. But the primary trend is still arguably sideways when considered from 2-3 years ago. And the secular trend since 2010 arguably still remains upward.

But may a trend trader peek outside the trend? That is a complicated question without a definite answer. For those wanting to explore whether it’s prudent to look at non-technical evidence outside the scope of the trend (e.g., considering the fundamentals and the broader macro), the following post offers some cost-benefit analysis and suggestions:

For those who wish to avoid being influenced by fundamental information, please skip this paragraph and read on to the next one. Andrew Dickson, the founder of Albert Bridge Capital and CIO of Alpha Europe Funds recently noted the following incongruities (downtrends) in EPS-estimate trends vs. price trends:

1. In late 2022, TSLA’s sell-side analysts expected $6.34 EPS in 2023 (about 9 months ago estimates).

2. After TSLA reported delivery numbers in early July, Dickson noted that “despite today's apparent 4% rev beat (implied from delivery-numbers) for Q2, 2023 EPS expectations have plummeted to $3.50. So earnings expectations for TSLA are now down -55% in 9 months and yet the stock is up +15%.”

3. He concluded that "the 2023 P/E multiple has expanded from 38x to 79x, or by 107%."

Dickson’s comments show that price is often not driven by fundamentals. Exactly what was priced in when the stock plummeted to $100 in January? And what is different now has nearly doubled off the lows? Or maybe the question is whether the data that gets priced in has different (and ever changing) weightings depending on the type of data. For example, maybe the data that affects price is most heavily weighted toward liquidity, capital flows, sentiment, seasonality, rather than fundamentals. But David Lundgren, a combined technical and fundamental analyst for whom SquishTrade has utmost respect, highly regards technical analysis, and especially favors technicals in the short / intermediate term, but says that fundamentals always matter in the long run. Here is a quotation from Lundgren from notes I've taken on his commentary in interviews and articles: "In the long-term, actual fundamentals will simply overwhelm any short-term technicals, emotions, sentiments driving a security or market price action."

Concluding Comments

Traders think in terms of probabilities, not certainties. Further, traders' time frames, risk management, and position sizes vary dramatically, which is why it seems imprudent to blindly follow another person’s signal service (whether paid or free). One very knowledgeable TV follower of mine has shorted TSLA with a position size that gives him a sizable margin of error. In other words, he can wait and allow significant fluctuations in price before getting shaken out of the position. My inference from our conversations is that his short thesis is based on deeply and persistently inverted yield curves, volatility being at major lows, deteriorating fundamentals at TSLA and other broader macro problems.

But macro and fundamentals can take a great deal of time to unfold, i.e., they do not play out immediately, and if they did, the big short should have been weeks or months ago. This year everyone thought a recession would be here by now, including experts with long-term experience managing or advising multi-billion dollar funds. This does not mean my fellow trader must be wrong. His thesis might yet succeed with time and patience, or it may yet experience more pressure or even be stopped out. This is why position size, risk management, and time frames matter. Before entering a trade or investment, one must consider time frame, position size, risk tolerance, risk management, technical or fundamental evidence, and an invalidation or stop level (which defines risk and relates integrally to position size). Shorter-term traders with leveraged, derivative, or supersized short positions would have already gotten crushed trying to short TSLA or other mega cap leaders the last few weeks or months.

GBP/USD pushes higher as inflation drops to 6.8%The British pound has posted considerable gains on Wednesday. In the North session, GBP/USD is trading at 1.2754, up 0.39%.

The UK released the July inflation report today and the readings were a mixed bag. Headline CPI dropped to 6.8% y/y, a sharp drop from the 7.9% gain in June and matching the consensus estimate. The decline was certainly welcome news but the driver of the downswing was a sharp drop in fuel prices. Core CPI, which excludes energy and food, remained unchanged in July at 6.9% and above the estimate of 6.8%. The core rate rose 0.3% m/m in July, up slightly from the July reading of 0.2%, which was also the estimate.

There was some good news in the inflation report as headline CPI declined by 0.4% m/m in July, compared to +0.1% in June and very close to the consensus estimate of -0.5%. Still, the fact that core CPI remains elevated and sticky provides support for the hawks at the Bank of England who believe that rates must rise further in order to curb inflation.

The inflation report comes on the heels of a soft UK employment report on Tuesday. The data revealed that the tight labour market is finally cooling, which would ordinarily be positive news for the Bank of England. The one glaring exception to the soft numbers was wage growth, which jumped to a record 7.8%, up from 7.5% and above the consensus estimate of 7.3%. The increase in wage growth is indicative of a wage-price spiral which will hamper the BoE's efforts to curb inflation.

The US released a robust retail sales report on Tuesday, giving a boost to the US dollar as speculation rises that the Fed may not be done with the current rate-tightening cycle. Headline retail sales rose 0.7% m/m in July, but core retail sales stole the show with a massive 1% gain up from an upwardly revised 0.4% in June. Consumer spending is picking up, which could complicate the Fed's plan to ease up on rates and guide the economy to a soft landing.

GBP/USD is testing resistance at 1.2726. The next resistance line is 1.2787

1.2634 and 1.2573 are providing support