$US30 DOW JONES—STEADY AMID THE STORMDOW JONES—STEADY AMID THE STORM

(1/9)

Good morning, Tradingview! The Dow Jones is the cool-headed cousin—less wild than Nasdaq’s growth party 📈🔥. Blue-chip stability shines, even as inflation bites—let’s unpack it! 🚀

(2/9) – WHY SO CALM?

• Makeup: 30 big, steady names—Walmart, Goldman 💥

• Price-Weighted: High flyers lead, not tech zingers 📊

• Edge: Less sway from growth stock swings

Dow’s the tortoise—slow and steady wins?

(3/9) – RECENT VIBES

• Feb 22: 1.7% dip—support at 43,400 holds 🌍

• VIX: Stays chill—Nasdaq would’ve freaked 🚗

• CPI Hit: 400-point drop, 300 back—meh 🌟

Stability’s the Dow’s secret sauce!

(4/9) – SECTOR SNAP

• Vs. Nasdaq: Tech’s jittery—Dow’s diversified 📈

• Volatility: ~15-20% vs. Nasdaq’s 25-30%

• Champs: Blue-chips buffer the chaos

Steadier ship—less Nasdaq nuttiness! 🌍

(5/9) – INFLATION RIPPLES

• CPI Spike: 3% YoY—400-point jolt ⚠️

• Fed: No rush to cut—rates sting 🏛️

• X Buzz: Tariffs, inflation spook recovery 📉

Even the Dow feels the heat—but shrugs!

(6/9) – SWOT: STRENGTHS

• Stability: Blue-chip backbone holds firm 🌟

• Dividends: Cash flows steady the ship 🔍

• Mix: Less tech tantrums—broad base 🚦

Dow’s the rock in choppy waters!

(7/9) – SWOT: WEAKNESSES & OPPORTUNITIES

• Weaknesses: Inflation nicks costs—ouch 💸

• Opportunities: Safety shines if tech flops 🌍

Can Dow dodge the inflation blues?

(8/9) – Dow’s steady play—what’s your vibe?

1️⃣ Bullish—Stability’s golden.

2️⃣ Neutral—Holds, but inflation looms.

3️⃣ Bearish—Growth wins anyway.

Vote below! 🗳️👇

(9/9) – FINAL TAKEAWAY

Dow’s less jittery—blue-chips cushion the storm 🌍🪙. Inflation’s a nag, but stability rules. Rock or relic?

Inflation

Market Alert: Potential Downside Ahead! The S&P 500 (SPX) just closed with a strong bearish candle, dropping -104 points (-1.71%), signaling a possible shift in momentum. The index is now testing a key support level near 6,000, and if this level breaks, we could see a sharper pullback.

📉 What’s Happening in the Market?

1️⃣ Rising Interest Rate Concerns – The Federal Reserve remains cautious about inflation, and recent economic data suggests they may keep rates higher for longer. This puts pressure on equities, especially high-growth stocks.

2️⃣ Earnings Season Uncertainty – Many companies are reporting mixed earnings, with some missing expectations. Weak guidance from major corporations could fuel more downside.

3️⃣ Geopolitical Tensions & Market Volatility – Ongoing global uncertainties, such as geopolitical conflicts and supply chain disruptions, are adding risk-off sentiment to the market.

4️⃣ Technical Breakdown Risks – The SPX is currently sitting near critical support at 6,000. If this level fails, we could see further selling pressure toward 5,920 - 5,880 and possibly as low as 5,773.

🔥 What to Watch Next?

✅ Can the market hold 6,000 and bounce? Or will sellers push prices lower?

✅ Watch for reactions around 6,068 - 6,100—if the index struggles here, more downside is likely.

✅ Increased volatility means risk management is key—stay cautious, and don’t chase trades!

⚠️ Bottom Line: The market is at a turning point. If downside momentum continues, we could see a bigger correction. Stay alert and manage risk accordingly!

$JPIRYY -Japan's Inflation Rate (CPI)ECONOMICS:JPIRYY 4%

(January/2025)

source: Ministry of Internal Affairs & Communications

- The annual inflation rate in Japan climbed to 4.0% in January 2025 from 3.6% in the prior month, marking the highest reading since January 2023.

Food prices rose at the steepest pace in 15 months (7.8% vs 6.4% in December), with fresh vegetables and fresh food contributing the most to the upturn.

Further, electricity prices (18.0% vs 18.7%) and gas cost (6.8% vs 7.8%) remained elevated with the absence of energy subsidies since May 2024.

Additional upward pressure also came from housing (0.8% vs 0.8%), clothing (2.8% vs 2.9%), transport (2.0% vs 1.1%), furniture and household items (3.4% vs 3.0%), healthcare (1.8% vs 1.7%), recreation (2.6% vs 4.0%), and miscellaneous items (1.4% vs 1.1%).

In contrast, prices continued to fall for communication (-0.3% vs -2.1%) and education (-1.1% vs -1.0%).

The core inflation rate rose to a 19-month high of 3.2%, up from 3.0% in December and topping consensus of 3.1%.

Monthly, the CPI increased by 0.5%, after December's 14-month top of 0.6% rise.

Could One Event Propel Gold to $6,000?Gold has long been a refuge in times of crisis, but could it be on the brink of an unprecedented surge? Analysts now predict the precious metal could reach $6,000 per ounce, driven by a potent mix of geopolitical instability, macroeconomic shifts, and strategic accumulation by central banks. The prospect of a Chinese invasion of Taiwan, a major global flashpoint, could be the catalyst that reshapes the financial landscape, sending investors scrambling for safe-haven assets.

The looming threat of conflict in Taiwan presents an unparalleled risk to global supply chains, particularly in semiconductor production. A disruption in this critical sector could spark widespread economic turmoil, fueling inflationary pressures and eroding confidence in fiat currencies. As nations brace for potential upheaval, central banks and investors are increasingly turning to gold, reinforcing its role as a geopolitical hedge. Meanwhile, de-dollarization efforts by BRICS nations further elevate gold’s strategic importance, intensifying its upward trajectory.

Beyond geopolitical risks, macroeconomic forces add momentum to gold’s ascent. The U.S. Federal Reserve’s anticipated rate cuts, persistent inflation, and record national debt levels all contribute to a weakening dollar. This, in turn, makes gold more attractive to global buyers, accelerating demand. At the same time, the psychological factor—fear-driven safe-haven buying and speculative enthusiasm—creates a self-reinforcing cycle, pushing prices ever higher.

Despite counterforces such as potential Fed policy shifts or a temporary easing of geopolitical tensions, the weight of uncertainty appears overwhelming. The convergence of economic instability, shifting power dynamics, and investor sentiment suggest that gold’s march toward $6,000 is less a speculative fantasy and more an inevitable financial reality. As the world teeters on the edge of historic change, gold may well be the ultimate safeguard in an era of global upheaval.

Is History Repeating? XAUUSD on the Verge of a Breakout!📌 Description:

Gold's price action is aligning with a familiar historical pattern, hinting at a potential breakout. Let’s break it down:

1️⃣ Historical Precedent – Looking back, a similar market structure led to a significant bullish move. Recognizing these patterns can provide an edge in anticipating market behavior.

2️⃣ Recurring Structure – Once again, the chart is shaping up in a way that mirrors past price action. If history is any guide, this could be a pivotal moment.

3️⃣ Bullish Pennant Formation – The current price action suggests the formation of a bullish pennant, a classic continuation pattern. When combined with historical context, the probability of a breakout strengthens.

🔍 Fundamental Factors:

- Geopolitical Uncertainty: Rising tensions and macroeconomic instability continue to drive demand for gold as a safe-haven asset.

- Interest Rate Expectations: With potential shifts in central bank policies, any dovish signals could fuel further upside in XAUUSD.

- Inflation & USD Strength: Any weakness in the dollar or persistent inflation could further support gold’s bullish case.

⚡ Is this the next major move for gold? Let’s discuss! Drop your thoughts below! 👇

RBNZ lowers rates by 50 bps, NZ dollar gains groundThe New Zealand dollar has posted gains on Wednesday. NZD/USD is trading at 0.5721 in the European session, up 0.31% on the day.

The Reserve Bank of New Zealand slashed the cash rate by 50 basis points, bringing the cash rate to 3.75%. The markets had priced in the cut at 90% so there was no surprise at the jumbo cut. This lowered the cash rate to its lowest level since Nov. 2022. The RBNZ demonstrated again that it can be aggressive, as it has cut rates by 175 basis points since the easing cycle started last August.

The New Zealand dollar is stronger on Wednesday, which is somewhat surprising, given the jumbo rate cut and the RBNZ's signal that further rate cuts are on the way in the coming months.

The rate statement noted that the members were confident lowering rates as CPI remained near the midpoint of the 1%-3% target band. At the same time, members expressed concern that economic activity in New Zealand and abroad were "subdued" which posed a risk to economic growth.

The statement also made a brief mention of "trade restrictions" which could dampen economic growth. No mention was made of US President Trump's tariff threats but policymakers are clearly concerned that US tariffs, even if not aimed directly at New Zealand, could chill the global economy and hurt the country's key export sector.

In a follow-up press conference, Governor Adrian Orr said that the Bank expected to lower the cash rate to 3% by the end of the year. This forecast was lower than the November projection of 3.2% by year's end. The central bank is expected to deliver smaller rate cuts of 25-bps in the coming months.

NZD/USD is testing resistance at 0.5713. Above, there is resistance at 0.5731

0.5686 and 0.5668 and the next support levels

XAUUSD - Consolidation, what’s next?Here is our in-depth detailed view on XAUUSD . Potential opportunities and what to look out for. This is a detailed overview on the pair sharing possible entries and important Key Levels.

Alright first, taking a look at XAUUSD from a lower time-frame . For this we will be looking at the m15 time-frame .

As of right now, we are consolidating on OANDA:XAUUSD The best “signal” for now is to sit on our hands and wait for a clear break. Right now we are in a range from around 2905.6 and 2896 . Until we get a clear break , we can’t know the direction of the pair just yet. So, breaking down everything and understanding the importance of Key Levels we have several outcomes possibly in play.

Scenario 1: BUYS at the break to the upside (from the consolidation area)

- We broke above our consolidation area.

With the break to the upside, we can expect to see 2915 or a deeper revisit of 2920. At this point we would have to see if we make any pullbacks, possibly revisiting the top of the consolidation area (now becoming our support).

Scenario 2: SELLS at the break to the downside (from the consolidation area)

- We broke below our consolidation area.

With the break to the downside, we can expect to see lower levels such as 2880. At this point we would have to see if we make any pullbacks and continue chugging away to the downside. With the breaks of current lows we have on gold, we can expect drops even down to 2840.

KEY NOTES

- XAUUSD is consolidating.

- Breaks to the upside would confirm buys.

- Breaks to the downside would confirm sells.

- Possible deeper digs to the upside from 2915.

Happy trading!

FxPocket

U.S. Michigan 5 Year Inflation Expectations ComparisonThe U.S. Michigan 5 Year Inflation Expectation Comparison in the image attached shows the difference of the past 3 presidential administrations. I'm not trying to make this a political issue, but merely just looking at a comparison of what the masses of people have expected the future inflation rates to be in the past in order to have an idea of what to expect in the future.

When looking at this comparison, it shows the difference between economic policies (different administrations) and their effects on inflation expectations. Granted, with some policy implementations having a lag effect, there is likely some overlap between administrations and their effect on the inflation expectations. The dashed orange lines show the limits of the majority of data points that fall within those dashed lines. Anything that plots outside the dashed orange lines are outliers / not normal (for the last 30+ years).

COVID obviously had an outsized impact on inflation expectations since the U.S. government printed massive amounts of new money (Quantitative Easing (QE) by the Federal Reserve) to offset the closing of the economy / lockdowns due to COVID. That is marked on the chart to show approximately when that would have started. Thankfully, when COVID hit, we were at historically the lowest inflation expectations in U.S. history (as far back as the data goes on this chart).

With our current administration trying to cut costs of the federal government and trying to increase external sources of tax revenue to offset decreases to internal tax revenue sources, I suspect that will decrease the federal spending (net effect). A large portion of our inflation in the U.S. economy comes from government spending and printing of new money (QE). Granted the Federal Reserve has been in a Quantitative Tightening (QT) mode lately to help cool recent elevated inflation. However, I bet the Fed will be going to a net zero (not QT or QE) stance soon before they begin QE again in the future.

This will, hopefully in the short term, help inflation expectations come down, but tariffs will pressure inflation to increase if tariffs aren't offset enough by the administration lowering the taxes on U.S. citizens and businesses to have a net zero effect (which is possible). If the Federal Reserve starts QE sooner than later (highly unlikely unless our economy goes into a recession), then that will certainly put a lot of pressure on inflation to go up. This is a mistake the Fed has done before in the past back in the 1970's / 1980's until past Fed Chairman Paul Volcker raised rates to the highest they've ever been to break the insane inflation rates back then. Time will tell if history rhymes again or not. I certainly hope inflation is tamed and not allowed to go crazy again. Please feel free to leave a comment / your thoughts below. I welcome all feedback on anywhere my analysis may have been wrong. Good luck trading / investing out there.

The Future Looks Bright-Platinum No BrainerWhy platinum is in the top 3 most undervalued assets. It won't be like this for long in my opinion, and I explain why platinum is a no brainer long

News TradingLet’s talk about news trading in Forex . While news trading is extremely lucrative it’s one of the most risky things a trader can do and experience. News and data cause extreme volatility in the market and as we always say “volatility can be your friend or your enemy” . Let’s take a deeper dive into news trading, which news and data affect the TVC:DXY precious metals such as OANDA:XAUUSD and other dollar related currency pairs. We will also cover having the right mindset for trading the news.

1. Understanding News Trading in Forex

News trading is based on the idea that significant economic data releases and geopolitical events can cause sharp price fluctuations in forex markets. We as traders, aim to profit from these sudden price movements by positioning ourselves before or immediately after the news hits the market. However, due to market unpredictability, it requires a strategic plan, risk management, and quick decision making.

2. What to Do in News Trading

1. Know the Key Economic Events – Monitor economic calendars to stay updated on high-impact news releases.

The most influential events include:

Non-Farm Payrolls (NFP) – A report on U.S. job growth that heavily influences the U.S. dollar.

Consumer Price Index (CPI) – Measures inflation, impacting interest rate decisions and currency valuation.

Federal Open Market Committee (FOMC) Meetings – Determines U.S. monetary policy and interest rates, affecting global markets.

Gross Domestic Product (GDP) – A key indicator of economic growth, influencing currency strength.

Central Bank Statements – Speeches by Fed Chair or ECB President can create large market moves.

2. Use an Economic Calendar – Websites like Forex Factory, Investing.com, or DailyFX provide real-time updates on economic events.

3. Understand Market Expectations vs. Reality – Markets often price in expectations before the news is released. If actual data deviates significantly from forecasts, a strong price movement may occur.

4. Trade with a Plan – Whether you are trading pre-news or post-news, have clear entry and exit strategies, stop-loss levels, and a defined risk-to-reward ratio.

5. Monitor Market Sentiment – Pay attention to how traders are reacting. Sentiment can drive price action more than the actual data.

6. Focus on Major Currency Pairs – News trading is most effective with liquid pairs like FX:EURUSD , FX:GBPUSD , FX:USDJPY , and OANDA:USDCAD because they have tighter spreads and high volatility.

3. What NOT to Do in News Trading

1. Don’t Trade Without a Stop-Loss – Extreme volatility can cause sudden reversals. A stop-loss helps prevent catastrophic losses.

2. Avoid Overleveraging – Leverage magnifies profits but also increases risk. Many traders blow accounts due to excessive leverage.

3. Don’t Chase the Market – Prices may spike and reverse within seconds. Jumping in late can lead to losses.

4. Avoid Trading Without Understanding News Impact – Not all economic releases cause the same level of volatility. Study past reactions before trading.

5. Don’t Rely Solely on News Trading – Long-term success requires a balanced strategy incorporating technical analysis and risk management.

4. The Unpredictability of News Trading

News trading is highly unpredictable. Even when a report meets expectations, market reactions can be erratic due to:

Market Sentiment Shifts – Traders might focus on different aspects of a report than expected.

Pre-Pricing Effects – If a news event was anticipated, the market might have already moved, causing a ‘buy the rumor, sell the news’ reaction.

Liquidity Issues – Spreads widen during major news events, increasing trading costs and slippage.

Unexpected Statements or Revisions – Central banks or government agencies can make last-minute statements that shake the market.

5. How News Affects Forex, Gold, and the U.S. Dollar

1. U.S. Dollar (USD) – The USD reacts strongly to NFP, CPI, FOMC statements, and GDP reports. Strong economic data strengthens the dollar, while weak data weakens it.

2. Gold (XAU/USD) – Gold is an inflation hedge and a safe-haven asset. It often moves inversely to the USD and rises during economic uncertainty.

3. Stock Market & Risk Sentiment – Positive economic news can boost stocks, while negative reports may trigger risk aversion, benefiting safe-haven currencies like JPY and CHF.

6. The Right Mindset for News Trading

1. Accept That Volatility is a Double-Edged Sword – Big moves can mean big profits, but also big losses.

2. Control Emotions – Fear and greed can lead to impulsive decisions. Stick to your strategy.

3. Risk Management is Key – Never risk more than a small percentage of your capital on a single trade.

4. Adaptability – Be prepared to change your approach if market conditions shift unexpectedly.

5. Patience and Experience Matter – The best traders wait for the right setups rather than forcing trades.

Thank you for your support!

FxPocket

Hot Inflation & What to Watch Next - 14/02/2514th of February 2025

•XRP and BNB leading, as Bitcoin trades flat in the last seven days.

•Headline inflation metrics in the US land above expectations.

•Impactful data point to watch heading into the end of February.

---

A big week of headlines and events, particularly out of the US, have netted very little change in Bitcoin’s price.

Bitcoin is down 0.1% at the time of writing in the last seven-days, while altcoins such as XRP and BNB are showing double-digit gains.

Bitcoin has struggled to make new year-to-date highs in the current state of global conditions. In contrast, global indices in the UK (FTSE100) and China (CSI300) have continued to make new year-to-date highs

Mixed Messages & Above Expected Results

Fed Chair Jerome Powell mentioned earlier this week at a senate banking enquiry that the current state of monetary policy does not require easing conditions, as the economy remains strong and the 2% target for inflation is key.

However, he has referenced that unexpected moves in the labour market or a significant cooling of inflation could change the committee’s mind.

“If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, we can ease policy accordingly.”

On this point, headline metrics for inflation land above expectations this week.

On Tuesday, Consumer Price Index (CPI) landed above expectations at 3.0%, rising 0.1% from the previous month.

Overnight the Producers Price Index (PPI) landed above expectations at 3.5% year-on-year. This figure remains unchanged from the previous month and represents the inflation burden on producers in the US.

Key data to come

On the last day of February the US Personal Consumption Expenditures (PCE) data will provide further clarity towards the state of monetary policy heading into next month.

PCE is the leading indicator used by the policy committee to measure inflation.

Fear and greed currently reads 40 – neutral.

Bitcoin Analysis

The price of Bitcoin is currently trading within the January high and low range, and on the Bollinger band we are entering a period where the upper and bottom channel is compressing.

Bullish Scenario

In the coming days, price may see a sharp move higher as the Bollinger Bands tighten. If bulls regain control and reclaim the monthly open, they could push toward last month’s high.

Bearish Scenario

We could also with this compression in the Bollinger Bands, see volatility moving price to the downside. This may result in prices heading towards the January low.

DISCLAIMER: The information is for general information purposes only. It is not intended as legal, financial or investment advice and should not be construed or relied on as such. Before making any commitment of a legal or financial nature you should seek advice from a qualified and registered legal practitioner or financial or investment adviser. No material contained within this website should be construed or relied upon as providing recommendations in relation to any legal or financial product.

Gold and Silver Out of Sync-Extreme Sentiment and Runaway Movesgold and silver futures chart analysis and why gold may no longer predictably be used to time the silver moves at this period in time; though there are several ways for silver to reach 37-43 and ultimately 50, as gold is likely set to overshoot 3000.

GBP/USD dips on hot US inflation reportThe British pound is lower on Wednesday. GBP/USD is trading at 1.2400, down 0.37% on the day.

The January inflation report was hotter than expected, giving the US dollar a boost against the major currencies today. Headline CPI rose 3% y/y, above the December gain of 2.9% which was also the market estimate. Monthly, CPI rose 0.5%, up from 0.4% in December and above the market estimate of 0.3%. It was the highest monthly inflation rate since August 2023.

The core rate, which excludes food and energy, rose 3.3% from 3.2%, above the market estimate of 3.2%. Monthly core CPI accelerated to 0.4% from 0.2%, above the market estimate of 0.3%.

The inflation report didn't change expectations about the March meeting, with the Fed virtually certain to hold rates. However, expectations for a cut in May have dropped to just 9%, compared to 21% a day ago. The economy is performing well and the Fed will be reluctant to lower rates again until it sees inflation moving lower.

Fed Chair Powell repeated a familiar message in testimony before a Senate Banking committee on Tuesday, saying that the Fed "does not need to be in a hurry" to adjust policy. Powell said that rate policy remains restrictive but the Fed would be careful not to lower rates too quickly or too slowly. Powell deflected a question about Trump's tariffs and US trade policy but acknowledged that tariffs could lift inflation and complicate the Fed's ability to lower rates.

The UK releases GDP on Thursday, with little change expected from the sputtering UK economy. Annually, GDP is projected to remain unchanged at 1%, while the GDP 3-month average to December is expected to decline by 0.1%, compared to a flat reading in the previous release. The economy contracted in the third quarter and may show a small gain in Q4 thanks to increased government spending.

GBP/USD tested support at 1.2411 earlier. Below, there is support at 1.2368

1.2491 and 1.2534 are the next resistance lines

Skyrocket Inflation at 3%!Previous U.S. Inflation Rate: 2.9%

New U.S. Inflation Rate: 3%

U.S inflation rate has rocketed up once again, which comes as no surprise. An excuse they’ll use to keep interest rates high, which effects the everyday person. Part of the game they’re playing📈

$QQQ - Where are we going now?NASDAQ:QQQ

A drop to $517 looks in the cards here and would be a good spot to bounce to keep the Symmetrical Pattern alive.

Further weakness would take us down to previous support at $510-$515.

Not financial advice

My CPI/ Inflation PredictionECONOMICS:USCIR NASDAQ:QQQ AMEX:SPY AMEX:IWM

We are just 15 minutes away from some very important inflation data coming out.

Here is my prediction: 3.1 YoY CPI or Lower

- Double top to drop continues

- Had a small lower high form and deflect off the 9ema

- Curling over and pointed down again

- Bearish WCB is still thriving

- The trend is your friend and the trend says we are going to continue to fall lower

Not financial advice

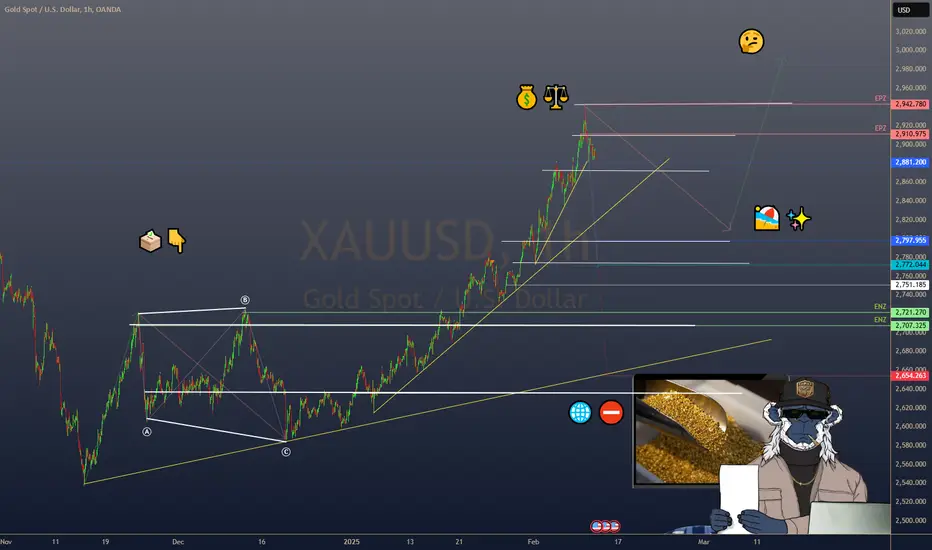

$GOLD EASES FROM RECORD HIGHS AHEAD OF U.S. INFLATION DATAGOLD EASES FROM RECORD HIGHS AHEAD OF U.S. INFLATION DATA

1/7

Gold hit a record high of $2,942.70/oz on Feb 11, fueled by safe-haven demand amid fresh U.S. tariffs. Today, it’s dipped 0.2% to $2,892.50 as investors take profits and watch U.S. inflation data. Let’s dig in! 💰⚖️

2/7 – RECENT PRICE ACTION

• All-time high at $2,942.70/oz—sparked by President Trump’s 25% tariffs on steel & aluminum

• Spot gold now at $2,892.50 (↓0.2%), with futures at $2,931.40 (↓0.1%)

• The rally’s paused—are we in for a short breather or a bigger correction? 🤔

3/7 – TARIFF TENSIONS

• 25% tariffs raise global trade war fears, boosting gold’s safe-haven appeal

• Markets worried about inflation, as import costs could climb

• Gold remains a hedge against economic uncertainty and currency devaluation 🌐⛔️

4/7 – MACROECONOMIC DRIVERS

• Fed Chair Powell’s hawkish comments on rate policy sent gold lower—higher rates often weigh on non-yielding assets

• U.S. inflation data (due soon) could shape the Fed’s next move—any upside surprise might strengthen the dollar, pressuring gold further

5/7 – INVESTOR SENTIMENT

• Profit-taking: After a massive run-up, traders might lock in gains

• Safe Haven: Still an underlying bullish sentiment if tariffs escalate

• The $2,900–$2,950 range is in focus—will gold consolidate or stage another breakout?

6/7 Where’s gold heading next?

1️⃣ Above $3,000—safe haven demand remains strong ✨

2️⃣ Sideways around $2,900—pausing for data 🏖️

3️⃣ Back under $2,850—hawkish Fed sinks gold ⬇️

Vote below! 🗳️👇

7/7 – STRATEGY WATCH

• Short-Term: Watch U.S. inflation data & dollar moves—gold typically moves opposite the greenback

• Long-Term: If tariffs stoke inflationary pressure, gold may shine even brighter. Keep an eye on geopolitical developments! 🌎

EURUSD Ahead of Inflation DataYesterday, EURUSD continued its upward movement, reaching 1,0381.

Later today, U.S. inflation data will be released.

This news has a significant impact and will determine the next move for the USD.

If the pair continues to rise, the target will be to break previous highs and reach 1,0568.

Be cautious of misleading price movements and avoid emotional trading!

$CNIRYY -China Inflation Rate Hits 5-Month PeakECONOMICS:CNIRYY 0.5%

(January/2025)

source: National Bureau of Statistics of China

- China’s annual inflation rate surged to 0.5% in January 2025 from 0.1% in the prior month, above consensus of 0.4%.

This was the highest figure since August 2024, driven by seasonal effects from the Lunar New Year.

Meantime, producer prices fell by 2.3% yoy, keeping the same pace as in December while declining for the 28th month.

VIX & SXP There is some W on actual lows in VIX , so if it will play out ...It will be next higher low on VIX. It could lead in to higher high. Time will show how markets react on today employment data .I think it was little bit pro inflation with can lead in to stronger DXY situation ...

SPX500 programmed to have a correction.My analysis is straightforward. On the weekly timeframe, there is a significant bearish divergence on the RSI, indicating that the market is moving in the wrong direction relative to fundamentals. This divergence has been present for six months, so one might assume there’s no reason for a change.

The market is in a bubble, but it needs a catalyst to wake up. While I appreciate some of Trump's policies, certain aspects of his approach could crash the market.

- Imposing tariffs on most imports might seem like a good idea. Trump aims to make the U.S. a producer of goods rather than an importer. However, the U.S. has lost much of its manufacturing base, engineering expertise, and know-how. China now dominates these areas, making this policy difficult to implement within the short span of a four-year term.

Instead, tariffs on all imports would raise prices, worsening inflation. The market's prolonged rise has been largely driven by the Fed's efforts to control inflation. Higher inflation would force the Fed to raise interest rates, spooking the market. Another risk is a potential disagreement between the government and the Fed over policies, which would create uncertainty.

I believe that increased inflation, higher prices, and tariffs will ultimately undermine trust in U.S. monetary policies, leading to the opposite of the intended effect. The USD could weaken, and more countries may move away from dollarization (regardless of tariffs, as Trump cannot dictate other nations' monetary policies).

The market would likely react negatively, and the bearish divergence would play out, potentially causing a crash lasting at least a year, similar to what happened in January 2022.

I hope I’m wrong, but this scenario has a high probability of occurring.

EUR/USD slides on tariff turmoil, euro CPI risesThe euro has weakened at the start of the new week. EUR/USD slumped over the weekend and dropped as low as 1.0141, its lowest level since Nov. 2022. The euro has recovered somewhat on Monday and is trading at 1.0277 in the North American session. Still, the euro has dropped 0.76% since Friday's close.

US President Trump hasn't wasted any time and imposed 25% tariffs on Mexico and Canada over the weekend, effective February 4. Mexico and Canada have both announced retaliatory tariffs in response. Earlier today, just one day before the tariffs were to take effect, the US announced that the tariffs against Mexico would be delayed for a month. The breather is good news, but the US could still find itself embroiled in a trade war with its two neighbors, in what is the world's largest trade zone.

Trump hasn't slapped the European Union with any tariffs yet, but said on Friday that he would "absolutely" go after imports from the EU. Global markets have been hit by fears of a global trade war resulting from the US tariffs and the US dollar is up sharply against most of the major currencies, including the euro.

Inflation in the eurozone ticked upwards to 2.5% y/y in January from 2.4% in December, above the market estimate of 2.4%. This was the highest CPI level since July 2024, driven mainly by a sharp jump in energy prices. Core CPI, which excludes food and energy prices, remained unchanged at 2.7% y/y for a fifth straight month, just above the market estimate of 2.6%. This is above the European Central Bank's 2% target but is the lowest level since January 2022. Services inflation, which is closely watched by the ECB, eased to 3.9% in January, down from 4% in December.

Today's inflation report affirms that inflationary risks remain and could complicate the ECB's plans to reduce interest rates and kick-start the weak eurozone economy. The ECB meets next on March 6.

EUR/USD has pushed above resistance at 1.0244 and is testing resistance at 1.0297

There is support at 1.0203 and 1.0175

www.tradingview.com

Inflation vs gold correlation 60's to 80's Pattern.Gold seems to like inflation. Or, is inflation food for gold? These are chars that no one is showing you.

According to this chart, Gold has a seven year bull run ahead of it that should top at some point in 2032.

This a chart of the US Inflation rate on the 2 month (Blue line) right from the horses mouth, Bureau of labour statistics. On the top in gold or yellow is the gold chart. As you can clearly see, in the seventies gold was very heavily correlated with inflation. This is not my opinion this is a fact, and it will be again.

THIS IS A 2 FOR ONE GUYS. INFLATION AND GOLD FORCAST ALL IN ONE!!

Let me know what you think down below.

Kind regards,

WeAreSat0shi