Is Intel about to broke his strong supports???After checked only in 1d and 1w timeframes I was able to see a knowing bearish price-action pattern which indicates that we are almost about to SELL, as per supports in 1d and 1w I just add an arrow which indicates the most possible FIRTS target, need to go deep into analysis in order to check if stonks will stay there or they carry on with bearish trend.

Intel

INTEL presenting a SELL ENTRYINTEL is presenting an opportune level to sell with the least risk and the most potential reward.

All Requests Suggestions and Remarks are Welcome .

Fervently brought to you by ManhattanStocks

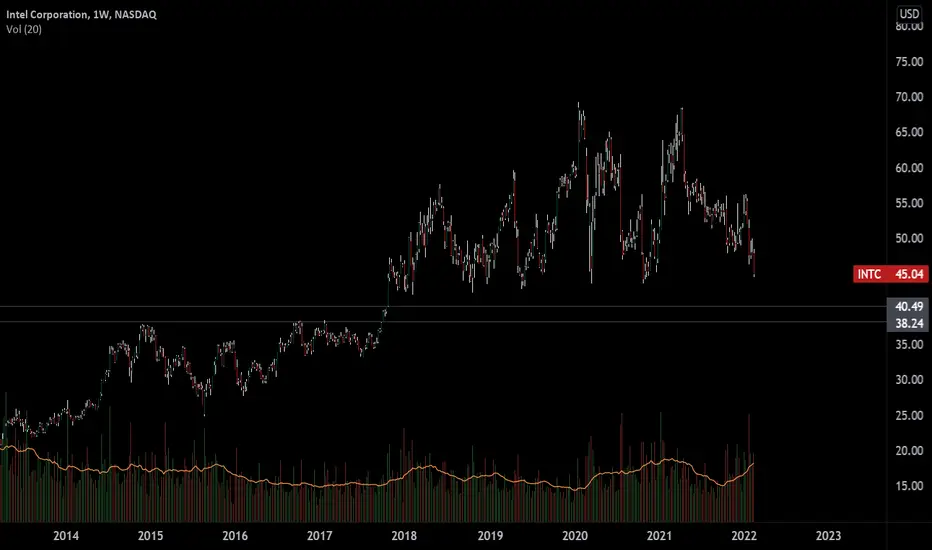

⏩ INTEL. 1 WEEK CHART ACCUMULATION?Hello! Lets look at Intels 1w chart.

1. Mark-up finished with climactic action (buying climax = resistance line) in 2018. Then we saw change of behaviour reaction from bears, we stopped at 42$ level (support line)

2. Then price started to move between resistance and support lines in a horizontal range. In December 2019, January 2020 bulls rally breaked the resitance line but covid incident have declined this try. Bears immidietaly seized the initiative and price tested support line (demand zone). Just look at this BIG SUPPLY BAR (july 2020) with the one of the biggest spreads and volume! But whats the result? Looks bearish, but acts neutral.

3. After that, Bulls tryed to rally and they overcame that bar but have been declined at 68$ as in January 2020 - Lower High.

4. Finally, bears started their reaction - downward channel. Supply and demand lines of the channel work properly.

5. Now we are still in this structure. To tell the truth, this sellers move does not consist great momentum, spread of the bars are not as big as in 2020 reaction so thats more bullish. Recent low on 22 february is LH compare to previous one. Look at rally that began - good spreads, there is no climactic volumes too, just consistent demand, But resistance line have declined that move.

6. Last week closed in a body of big bullish bar, we expect local stopping action (1d. 4 hour) at 45-46 level. This is a nice Point of entry. Targets:

1st - 51$, 2nd 53-54$

7. Overall, in our opinion, we havent seen phase C yet (shakeout, spring) , final move to shake out all weak hands. Only after that we will see higher prices!

Massive cause, isnt it? Write your thoughts down in comment section below.

INTC Double BottomIf you haven`t bought the $44 strong support:

Then you should know that Nvidia and Intel might join forces to end Chip Shortage!

I expect INTC will go to $56.

Looking forward to read your opinion about it.

Intel Shooting Star at Resitance? Intel Corporation - Short Term - We look to Sell at 48.40 (stop at 50.05)

A shooting star has been posted as prices reject the higher levels. Previous resistance located at 49.00. We look for losses to be extended today. Price action remained broadly negative yesterday with the early highs being rejected after bullish momentum stalled.

Our profit targets will be 44.11 and 41.20

Resistance: 49.00 / 55.00 / 68.00

Support: 44.00 / 40.00 / 35.00

Disclaimer – Saxo Bank Group. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis, like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis, as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.

INTC exposure to China The U.S. warning China it could face devastating sanctions if it defies the ban on doing business with Russia!

This is a move that could have huge impact on American companies.

27% of AVGO Broadcom revenue comes from China.

My one year price target for INTC is $48, but after it moves lower, to $43.60 or $42.40

Looking forward to read your opinion about this.

Intel Color TheoryI like drawing trendlines on charts. In this video I examine all the trends INTC has experienced and show what I think is currently happening and where we are headed in the future.

Intel DCF Model - Intrinsic ValueIntel DCF Assumptions:

Tax Rate = 12.0%

Discount Rate = 7.4%

Perpetual Growth Rate = 2.0%

EV/EBITDA Multiple = 9.0x

Transaction Date = 28/02/2022

Fiscal Year-End = 25/12/2022

Current Price = $47.71

Shares Outstanding (m) = 4,072

Debt (m) = $38,101

Cash (m) = $28,413

Capex (m) = $20,329

Base Case Scenario

In addition to the above assumptions, the below DCF model is based on our base case scenario, which assumes a revenue growth over the next five years of -4%, 4%, 5%, 8%, 10%. These assumptions are slightly lower than analysts’ forecasts.

DCF (5Y) EBITDA EXIT MODEL:

Terminal Value

Final Forecast EBITDA (m) = $44,337

EV/EBITDA Multiple = 9.0x

TERMINAL VALUE (m) = $339,031

Intrinsic Value

Final Forecast EBITDA (m) =$44,337

EV/EBITDA Multiple = 9.0x

TERMINAL VALUE (m) = $339,031

DCF (5Y) PERPETUAL GROWTH RATE MODEL

Terminal Value

Enterprise Value (m) = $324,750

Plus: Cash (m) = $28,413

Less: Debt (m) = $38,101

Equity Value (m) = $315,062

EQUITY VALUE / SHARE = $77.37

Intrinsic Value

Enterprise Value (m) = $262,768

Plus: Cash (m) = $28,413

Less: Debt (m) = $38,101

Equity Value (m) = $253,080

EQUITY VALUE / SHARE = $62.15

DISCLAIMER:

All information is the author’s views, opinions, and assumptions at the time of writing, and Bull Headed Bear makes no guarantees of the information’s reliability and accuracy. The information is to be used for entertainment and informative purposes only. Bull Headed Bear and its authors reserve the right to change their views, opinions and assumptions due to many influencing factors.

Any actions taken based on the information on the website is strictly at your own risk. All investments carry a risk of loss, and you could lose all your money. Consider seeking professional advice from a financial advisor. Bull Headed Bear and its authors will not be liable for any losses or damages from the information on this site.

DISCLOSURE:

I/we have open long positions in Intel. We may increase this position depending on market movements over the coming weeks.

Buying at 38-40 rangeLooks like this is heading towards 38-40 range. It will be a good trading opportunity. Expecting a bounce then for a week or so.

INTC Intel will be free cash flow negative this yearIntel, which plans large investments in chip technologies in the next four years, warns that it will be free cash flow negative this year.

INTC predicts 10% to 12% annual revenue growth by 2026.

As a speculative buy, you can take into consideration the 44-45 usd area of support for a bounce.

Technical Analysis Of 10 Mentioned Stocks!Hi,

Long time no see! ;)

Actually, quite a busy time but still, have some old depths again and here they are - the stocks you mentioned in the comment section. Probably you don't even remember them :)

Sadly this series is not popular amongst crypto followers but still got enough data to sort out some stocks which may indicate that technically we get short-term bounces from shown areas.

To be said, it is the only technical side, fundamental analysis is your homework to do. These aren't my picks, these are your mentioned stocks.

Remember - fundamental analysis showing what to buy, technical analysis showing when to buy. So, do your homework and select what to buy ;)

1. Adobe

2. Alibaba

3. NVIDIA

4. Ball Corporation

5. Block

6. JD.com

7. Ford

8. CRISPR Therapeutics

9. Intel

10. PayPal

If you were interested in anything, go and do your homework! ;)

Regards,

Vaido

INTEL CORP (INTC) RSI+MACD+STOCH FIB RETRACEMENT TA TRADING 💡📉I developed a personal trading strategy on NASDAQ:INTC to setup a trading buy scenario.

What are the different indicators Showing?

MACD:

EMA's crossed, no sign early retracement bounce

!!! market uptrend could have turned into a downtrend, but we need more confirmation

RSI:

Market is globally in an uptrend but RSI looks like its crossing the 50 line towards a downtrend, so there may be no retracement bounce

INTC is accordingly to the RSI not overbought nor underbought, confirmation to come

STOCH:

STOCH looks like it's going towards its underbought level, I would wait till both lines cross the underbought level

What is FIB/Graph saying

Previous retracements reversed at around 50% to 61.8% fib level

I expect this retracement (if last retracement wasn't a trend reversal) to reverse around the same levels.

Intel Corp. as long term: 📈📈

Intel will definitely hit a 100$ in the future, with a lot of new big upcoming projects

For example: a crypto mining dedicated CPU

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

If you enjoyed this post and agree with me, a like and a sub would be very nice : )

If you have any other ideas or simply disagree, manifest yourself in the comments ⬇️⬇️⬇️

Stay updated for more content

Have a nice Day : ) Bye!

-----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Intel Analysis 16.01.2022Hello Traders,

welcome to this free and educational analysis.

I am going to explain where I think this asset is going to go over the next few days and weeks and where I would look for trading opportunities.

If you have any questions or suggestions which asset I should analyse tomorrow, please leave a comment below.

I will personally reply to every single comment!

If you enjoyed this analysis, I would definitely appreciate it, if you smash that like button and maybe consider following my channel.

Thank you for watching and I will see you tomorrow!

$INTC Intel Corp to Drop In PriceWith the recent blow to the companies reputation I would assume we see a good dip!

BUT lets take a look at the technical analysis.

We have been rejected at the current price 4 times now on the hour chart.

The daily chart appears to be seeing a bearish divergence as well.

money flow is not looking good.

I would assume this would play out as a sharp dip to 48.00 range or a slow decline through late Feb.

Let me know what you think!

Intel Corporation seems to be undervalued, Long it 20/02/2021 as you can see this ticker has broken its trend line and is rallying

total of 3 TPs,

1 TP is very easy to achieve

if 2 TP triggers, then we can easily expect the 3 TP to be achieved too

Micron cerca de romper record del 2000. Lo lograra? Micron sigue subiendo después de su reporte trimestral, y al los analistas arrancar el 2022 subiendo sus estimados con respecto a la accion. Les contamos como la salud técnica y fundamental están en la accion de cara hasta 2022

INTEL - Little more wait for entry before starts reversal. Wait for some more time before entry. Start entry from ~$48 - $42 range. Probably should bottom out by end of Jan. Will be interesting to see if this bottom out before earnings or after.

After that ride until 70+. That's ~60% or ~$25 potential upside.

Enjoy....

IntelI like historical pattern of this company. This an opinion based on an article I've just read but it seems as if the semiconductor issue is simmering down a bit relative to how unsure this issue was late last year. We also see a bunch of car companies having increased deliveries as well. Although Intel isn't the end all, be all within this sector, I can see at least a retracement of about 45% of the previous high seeing how price has reached this point up to 5 times since 2018's May. Let's see what happens! They also have enough cashflow to compensate for a hike in interest rates.

INTC idea #1Another breakout and retest of range formed 2nd half of November.

Now consolidating above and if it holds, could trade back to $52-55 range prior to big gap down of end October.

Intel joins Nasdaq recovery RallyIntel stock rose an impressive 2.8% on Tuesday taking its price to $52.44, and its overall growth in 2021 to 5.3%.

Any pullback and close of the gap from the good news Tuesday will be perfect entries for a stock that can rally with the Nasdaq now Omicron fears are subsiding.

The rise was fueled by the news that Intel was filing an IPO for Mobileye a producer and developer of advanced automotive safety systems, that pioneered camera arrays on cars that allow features such lane assistance and adaptive cruise control. This technology is expected to lead into autonomous cars in the near future.

The Israeli company founded in 1999 by Prof. Amnon Shashua was public on the NYSE between 2014-2017 until it was acquired by Intel for approximately $15 billion. The tech company is currently valued at staggering $50+ billion.

Any pullback and close of the gap to $51 from the good news Tuesday will be perfect entries for a stock that can rally with the Nasdaq now Omicron fears are subsiding. Targets are recent highs at $56.

Is Intel Headed for a Bull Market ? (TL;DR @ end)For the past 5 years, NASDAQ:INTC has been through quite the 'ride' of market price. For a good portion of their existence - they ran the multi-core CPU world almost entirely unchallenged. As of about 3 years ago, Advanced Micro Devices ( NASDAQ:AMD ) suddenly emerged from the mist with cheaper, greater performing chips that were idolised by the gaming and high-performance workstation community. While this was happening, Intel was far more interested in the large scale server industry, supplying various high capacity servers to various institutions such as universities and state owned research facilities. The public eye began to look down on Intel. AMD had come up neck and neck with Intel in performance and price yet Intel didn't exactly make their 'best efforts' to get ahead. Inevitably AMD surpassed them and Intel's market price fell.

Although, recently, new developments have come out of Intel (possibly consequent to the COVID pandemic). Last week, they announced the IPO of their daughter company, Mobileye. The IPO is planned for the middle of next year but this drove the stock price up slightly. Furthermore, their biggest rival, AMD has been falling behind both in the graphics card and CPU markets. The release of the 12th generation Alder Lake chips from Intel and the (stated) high performance (supposedly far better than available AMD chips) have also driven the price further up.

Intel also recently stated that they have adjusted their budget for development in desktop and laptop chips which should in theory result in the further production of even better products, even sooner.

So with an optimistic outlook on the company, the value should begin to increase and soon. If you're lucky enough to put money in now and results turn out as expected, COVID restrictions may just settle (due to Omicron not being as much of a threat) and the shortage of hardware across the industry may very well give the price that added 'leg-up'.

For investors and traders, all I would suggest is keeping your eyes peeled and thinking about the possibilities of this market dominated by only 2 companies. As usual, other opinions, facts and news are definitely welcome, so comment away!

TL;DR: Intel has been potentially pulling themselves up through these 3rd and 4th quarters. The release of 12th gen chips and the announcement of the IPO for Mobileye could all lead up to a hefty price climb. Conveniently AMD (biggest competitor) is also having a tough time and to add to this 'stroke of good luck', if COVID restrictions are eased due to the lack of intensity of the omicron, the price could climb higher.