IBM | Fundamental Analysis | Must Read...IBM shares fell nearly 10 percent to a seven-month low on Oct. 21 after the tech behemoth released a weak Q3 report.

IBM's revenues rose just 0.3 percent from a year earlier to $17.6 billion, $190 million less than forecasts. But excluding divestitures and foreign exchange rates, the company's revenues were down 0.2%.

Excluding the impending Kyndryl spin-off, IBM's revenue was up 2.5% in the period. Excluding divested businesses and foreign exchange rates, "excluding Kyndryl" earnings were up 1.9%.

IBM's GAAP earnings, which include Kyndryl spin-off expenses, fell 34% to $1.25 per share. Non-GAAP earnings, which exclude those expenses, still fell 2% to $2.52 per share, but beat forecasts by one penny.

IBM's performance was unimpressive, but it was in line with the outlook the company presented at an investor briefing in early October. Did investors exaggerate IBM's disappointing third-quarter report and create a new buying opportunity?

As in previous quarters, IBM reported third-quarter earnings in five main segments: cloud and cognitive software, global business services, global technology services, systems, and global finance.

IBM's cloud and cognitive software revenues grew thanks to double-digit growth in its cloud-related business, which offset low growth in its applications business and lower revenues in its transaction processing business.

The global business services segment profited from strong demand for cloud services, consulting, application management, and global technology services.

However, the Global Technology Services division weakened again, as weak growth in cloud services could not offset the continued decline in the Managed Infrastructure Services segment, which will be taken out by the Kyndryl spin-off.

The company's systems division struggled because of cyclically declining sales of IBM Z and Power systems, and financing revenues declined amid lower demand for financing services and slow sales of used equipment.

Once again, IBM's strengths failed to offset vulnerabilities, and investors were left attempting to find positives in lackluster reporting segments. However, this may all change as the "old" IBM ceases to exist.

After IBM spins off from Kyndryl next week, it will present four new reporting segments: consulting (29% of continuing operations revenue in 2020), software (42%), infrastructure (25%), and finance (2%).

IBM thinks these four segments will make it easier for investors to track the expansion of its faster-growing businesses.

IBM expects the software segment, which includes Red Hat and other hybrid cloud and artificial intelligence services, to be a major growth driver.

It also probably anticipates a streamlined consulting segment to better stand up to faster IT services and consulting companies, such as Accenture and Globant.

IBM's infrastructure business, which includes the legacy systems business as well as other hardware products and services, is likely to remain underperforming. However, IBM's earnings outlook suggests that the company will focus on streamlining its business and cutting costs to improve margins.

IBM believes that after the Kyndryl spin-off, it will deliver "sustained mid-single-digit revenue growth" from 2022 to 2024.

The company believes this growth to be driven by the expansion of hybrid cloud and AI services that can be integrated with public cloud platforms such as Amazon Web Services (AWS) and Microsoft Azure.

IBM probably realizes that it is too late to catch up with AWS and Azure in the public cloud market, but it can still use its large enterprise customer base and Red Hat's open-source software to develop services for the hybrid cloud, which sits between private clouds and public cloud services.

IBM investors will get Kyndryl stock next month. If they keep both shares, they will initially receive a combined dividend equivalent to IBM's current dividend, but then both companies may reduce their payouts.

It would seem that IBM investors should sell their Kyndryl stock immediately since the latter would likely have difficulty keeping up with companies like Accenture, but hold onto their shares of a "renewed" IBM to see if its plans to get out of the crisis work.

Nevertheless, today is not a good time to buy IBM stock. Right now, the stock may seem cheap at 12 times forward earnings, but the company still faces stiff competition from Amazon and Microsoft, which are expanding their public clouds in a hybrid market, and an unstable infrastructure business could derail growth in its software and consulting business.

Investors should wait for IBM to complete its spin-off and for results to improve for a few quarters before believing that the tipping point has arrived. Until then, they should buy other blue-chip stocks, not Big Blue.

Internationalbusinessmachines

IBM:FULL DETAILS FUNDAMENTAL+PRICE ACTION ANALYSIS|SHORT SETUP🔔IBM just posted its best quarter in years. This tech giant demonstrated very modest overall revenue growth in the second quarter of 2021, but an expansion in its cloud computing business, driven by its flagship Red Hat, which the company acquired in 2019. For income-seeking investors, IBM is a great dividend stock right now, and the hope is that growth will be even stronger after the Kyndryl spin-off is completed by the end of this year.

Here are several reasons why IBM is one of the best variants to buy right now.

- IBM's cloud solution sales are too undervalued

In the second quarter, IBM's total revenue rose just 3% year over year to $18.7 billion, and in the first half of the year, sales rose 2% to $36.5 billion. No big deal given the fast-paced digital age we live in, but not too bad for IBM given that it has been stuck in a steady decline for years.

Hidden beneath the surface and helping IBM regain positive momentum, however, is its huge cloud computing segment, which is still noteworthy. Total cloud computing sales were up 13 percent from a year ago to $7 billion, led by cloud provider Red Hat, which reportedly grew 20 percent. In fact, Red Hat has accelerated from the pace it set last year.

In fact, this strong performance of the cloud segment is the main reason IBM is spinning off its managed infrastructure segment (which we now know will be called Kyndryl). While technical infrastructure hardware is still an important segment of IT, it is not a growth area. It also offers lower profit margins than cloud software. Thus, the new IBM will focus more on its cloud business, which should help it achieve higher growth and earnings potential once the spin-off is complete by the end of this year.

- A high level of free cash flow generation

Of course, in the period leading up to the new cloud-focused IBM, it's primarily a dividend stock. And when it comes to dividend payments, it's all about free cash flow generation. IBM is doing well in that regard. In the first six months of this year, free cash flow was $2.56 billion, which pretty much covers the $1.47 billion paid out as dividends to shareholders.

Of course, $2.56 billion is a bit less than the $3.65 billion in free cash flow generated in the first half of 2020. So what's the bottom line? First, IBM spent $1.22 billion in 2021 on one-time expenses related to setting up the Kyndryl division. Setting that amount aside, free cash flow would have increased by 4%. IBM also spent $2.87 billion on cash acquisitions this year.

Since January, it has acquired nine smaller software and consulting companies to bolster its presence in cloud computing. Setting aside these acquisition-related costs, IBM would report an impressive 81% year-over-year increase in free cash flow in the first half of 2021.

In other words, IBM's current dividend yield of 4.7% is a good bet right now.

- Improving the balance sheet

When it comes to tech giants, industry leaders (like FAANG stock) have net cash. But not so at IBM. The more than century-old company has far more debt than cash. At the end of the second quarter, the company had $7.35 billion in cash and cash equivalents and another $600 million in marketable securities, but still had $55.2 billion in debt.

It's far from the nicest-looking balance sheet, but progress is evident. IBM had $61.5 billion in debt at the start of 2021, so the old tech company has reduced its obligations to bondholders by about $6.3 billion this year -- and has reduced debt by $17.9 billion since buying Red Hat in 2019. Although there's still work to be done, IBM has an investment-grade credit rating due to its strong free cash flow generation, and it can handle both dividend payments and gradual debt repayments.

The sale of Kyndryl promises to be a major event for IBM later this year, but for now, it is the best dividend company for investors looking for additional income. At the time of writing, the company's stock price is up 12% this year.

IBM 1M The history of the corporation is worthy of respectInternational Business Machines Corporation is an American electronic corporation, one of the world's largest manufacturers of all types of computers and software, one of the largest providers of global information networks.

IBM owns more patents than any other technology company.

The story begins in the 19th century.

If you have been following us for a long time, you should notice that we decided to make a portfolio of ideas from assets in the stock market for the long term.

And of course, it would have been blasphemy if we hadn't written a review of such a powerful company as IBM.

The corporation has been actively developing for more than a century, making our life easier and better by introducing new technologies into it.

Looking at the chart, you can name one dark period in their history - this is the beginning of the 90s, when the price of IBM shares fell to a critical $10.

In the early 1990s, the mainframe market crisis began, which peaked in 1993. And you guessed it - the main developer of mainframes was the IBM corporation. In 1993 Many analysts talking about the complete extinction of mainframes just now, and about the transition from centralized information processing to distributed (although the last mainframe was turned off in 2013).

In 1993, IBM posted a $8bn loss - the largest in American corporate history at the time - and it was time for drastic action.

New gene. director Luis Gerstner decides to cut 20% of its employees, which is 60,000 people. It was the largest cut in American history, but helped the IBM corporation survive from 1993-1994. From 1993 to 2002, when Gerstner left the Big Blue, the company's market capitalization rose from $29 billion to $168 billion . This man is considered the savior of IBM.

The next interesting period is the beginning of 2013 , then a protracted correction in the value of IBM shares began, with which the price is now trying to start going up.

An interesting coincidence is that the price of Gold went into its 6-year correction also at the beginning of 2013.

Such a correlation might suggest that long-term investors have so much faith in IBM that they can view their stock as a defensive asset on par with Gold?)

By the way, below is our global thought in relation to Gold.

So, now let's talk about the prospects that we assume looking at the chart.

The maximum correction that we are now admitting is a fall to $110.50-112.50 , from which we expect a solid rise in the value of IBM shares.

We consider the critical level - $180

Fixing the price above this level will open the way for a long-term growth perspective to $500-530

If the market will be negative, and the price cannot break through above $180, then unfortunately, then it will already be necessary to look towards $70 per IBM share

What do you say, about such material, comes in?

Share your thoughts and expectations in the comments on IBM stock

IBM Linear regressionIBM Linear regression analysis, short entry should be made accordingly. Only bullish sign is a cup and handle.

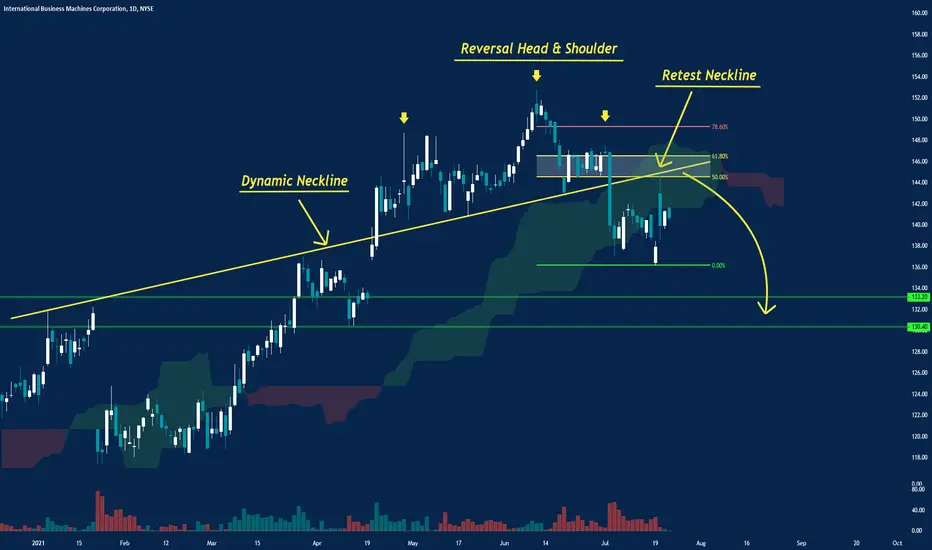

IBM: Bearish Wave Is Coming!

hey traders,

IBM gives us a perfect shorting opportunity.

we have a lot of clues:

bearish trend on a daily,

touch of the major trendline,

rsi divegence,

horizontal structure on the left,

fib.confluence

based on that I believe that soon we will see a strong bearish wave.

the initial target will be 130.0

the second target will be 120.0

IBM Earnings Create Velocity RunIBM blasted through previous resistance levels after its earnings report, then broke out to a new yearly level. Despite heavy profit taking by Professional Traders, the stock price held above that resistance level.

IBM Bump and Run!First bump and run pattern analysis, as you can see the price 'bumped' up from the upward trend leading to a round over then decline through the observed trendline. This is a bump and run reversal top, which often lead to a short term bearish correction. Feedback encouraged!

IBM Hitting Lower ResistanceIBM has been trending sideways, and recently filled the gap up from 4th-quarter earnings in 2018. IBM has formed an intralevel short-term bottom, which is at a short-term completion level.