Bullish Iron Condor with 64% PoP for 41% profit at eventMax profit: $291

Probability of Profit: 64%

Profit Target relative to my Buying Power: 41%

Max loss with my risk management: ~$200

Req. Buy Power: $709 (max loss without management at expiry, no way to let this happen!)

Tasty IVR: 53 (high)

Expiry: 43 days

Buy 1 SQ Jun18' 190 Put

Sell 1 SQ Jun18' 200 Put

Sell 1 SQ Jun18' 290 Call

Buy 1 SQ Jun18' 300 Call

Bullish Iron Condor for 2.91cr with +4.82 delta

Stop/my risk management : Closing immediately if daily candle is closing outside the box, max loss in my calculations in this case could be 200$. Probability of loss in this way: ~20% .

Take profit strategy: 65% of max.profit in this case with auto sell order at 1.02db. Probability of profit this way: ~80%.

Of course I'll not wait until expiry in any case!

If you liked this article, check my other ideas.

Anyway: HIT THE LIKE BUTTON BELOW , and for fresh option ideas FOLLOW ME( @mrAnonymCrypto ) on tradingview !

Ironcondor

SAGE 62% PoP Bearish Iron Condor after event

My favorite bearish neutral trade for today.

Losing only upside, I like the extreme high IVR values to play.

Reasons to play this:

1/ After event, big selloff, high implied volatility.

2/ Extreme High Implied Volatility, good for credit strategies

3/ I can boost my original bearish vertical spread with 2 bottom legs at fib 0.786 to boosting my reward almost zero risk to the downside (max loss below strike 35 is $17 ...)

4/ Secure zones are 88$ and the 40$

So the winner is the negative delta Iron Condor Strategy.

Max profit: $483

Probability of Profit: %62

Profit Target relative to my Buying Power: 42%

Max loss with my risk management: ~$250

Req. Buy Power: $1050 (max loss without management at expiry, no way to let this happen!)

Tasty IVR: 92 (ultra high)

Expiry: 45 days

Buy 1 SAGE Jun18' 35 Put

Sell 1 SAGE Jun18' 40 Put

Sell 1 SAGE Jun18' 90 Call

Buy 1 SAGE Jun18' 105 Call

IRON CONDOR for 4.83cr with negative -8.3 delta, because IVR is very high and I'm bearish.

Stop/my risk management : Closing immediately if daily candle is closing ABOVE $90, max loss in my calculations in this case could be 250$. Probability of loss in this way: ~20% .

Take profit strategy: 60% of max.profit in this case with auto sell order at 1.69db. Probability of profit this way: ~80%.

Of course I'll not wait until expiry in any case!

If you liked this article, check my other ideas.

Anyway: HIT THE LIKE BUTTON BELOW , and for fresh option ideas FOLLOW ME( @mrAnonymCrypto ) on tradingview !

IRON TARIHi guys!

This iron condor is 4weeks 10% strike.

Odd pretty nice, the premium is not that much, but sice we can cut the loss the RR is on our side!

Enjoy your wallet!

Tari.

IRON TARIHi guys!

This iron condor is 4 weeks, 10% strikes, 87% probability to get max profit.

The premium is nice, with 5$ spread per strike we have:

Max profit 90$

Max losso 410$

Very nice for an 87% proability to get the maximun credit!

Enjoy your wallet!

Tari.

IRON TARIHi guys,

this week I found this awesome iron condor, 3 weeks, 12% strikes.

We have 89% chance to earn the max profit, and looking at the moneyness we see that the market pays the double.

We should expect 0.05 Delta per leg, but we are at 0.30 for the Iron Condor.

Let' go!!

Enjoy your wallet!

Tari

Watch this BEFORE taking Iron Condors! (IV Rank & Percentile)Iron Condors have been the buzz lately on my social media. People have discovered or re-discovered them because they are WORKING now! But should traders keep using them without knowing WHY they are working? If you are getting into Iron Condors you MUST watch this to understand the key metrics professional options sellers look at when placing their trades.

Tradingview cut me off at 20 minutes but I got the info in!

RUSSEL ETF 20% profit play during correction with Iron Condor

One of the most highest probability of trades are: neutral Iron Condors with high Implied Volatility on large indices. (SPX, DJI, RUT)

The more an indice is overbougth, than better this strategy works, as the correction also results more movement into downside.

Unlike other overvalued stocks, however: the indices are not collapsing. (except for 1-2 extreme cases where immediate intervention is required, eg March 2020)

I'm always trading the alternative ETFs of these indices:

SPY = S&P500 = ES mini futures IWM = Russel 2000 = RT mini futures DIA = DJI = YM mini futures .etc...

On Friday I've opened an IWM Iron Condor, so here are my reasons:

(1) RTY1! Futures Analysis

The Russel mini futures at local top hit the 3 year trendline, bluffy upside trendline permanently broke.

(2) Divergence with breakdown

Hard daily divergence in the last few months, my smooth RSI trendline breeaks.

(3) Relative high IVR

Relative Implied Volatility Rank (IVR) increases.

This value, if high enough (e.g., above 45), favors neutral credit strategies like Iron Condor.

In the case of indices, this is particularly rare, occurring every few months. At these times you can safely open neutral strategies (wide wings), for example: Iron Condor, Strangle.

(4) My Iron Condor hunter script signal

My Iron Condor Hunter indicator give me an automatic signal with safe ranges.

As you see: in the past almost every time indicated the safe range successfully. (I'm not counting the 2020 Marc, every regular strategy failed in that crash).

(5) Safe levels are well defined in my range

I'm always defining safe price levels (based on the nearest short term high/low points).

In my case these levels are well defined inside the Iron Condor Hunter range:

CONCLUSION: I've opened an Iron Condor on IWM (Russel ETF)

Profit target: 20% Max profit: 68$ Max loss: 332$ Tasty IVR: 13 POP: 69% Expiry: 42 days

Strategy: Neutral IC

Buy 1 IWM April16' 185 Put Sell 1 IWM April16' 189 Put Sell 1 IWM April16' 244 Call Buy 1 IWM April16' 248 Call

Stop: Closing immediately if daily candle is closing below put strikes or above call strikes. Safe levels (190,205,229) are defending my borders.

Take profit strategy: I'm taking at the 55% of max.profit in this case. Inside the curve I'm usually in profit.

If you liked this article, check my other ideas.

Anyway: HIT THE LIKE BUTTON BELOW, and follow my fresh ideas ( @mrAnonymCrypto on tradingview ).

Old Nuggets: Defined Risk Skew AccommodationSkew. It can be a pain in the butt if you want to trade both delta neutral and probability neutral.

In QQQ, a delta neutral setup at the moment would be: selling a spread on the put side with the short put leg at the 275 (17 delta) and on the call side with the short call leg at the 344 (17 delta). However, this results in a short put strike 38 strikes away from current price and a short call strike 31 strikes away. It's delta neutral, but the probability of profit on the put side is 83% and on the call side 78%, so it isn't both delta neutral and probability neutral. Ugh.

Fortunately, there is a solution to obtain both a delta neutral and a probability neutral setup, and it's with a variation on the iron condor: a "double double" -- double the contracts on the call side, with the put side being double the width of the call side spread. Because the risk associated with the put side spread -- that attributable to a five wide -- is greater than the risk associated with the call side (2 x 2 or the equivalent of a four wide), the maximum risk of the setup is that of a five wide -- the widest wing of the setup. In other words, doubling up the number of contracts on the call side doesn't increase buying power effect, because it's attributable to the widest wing (i.e., 5 > 2 x 2, so buying power effect is that attributable to the five wide).

Here, you can't quite go exactly double due to strike availability at the moment on the put side (there's only five wides there), but you can go five wide on the put side, and 2 times a two wide on the call (the functional equivalent of a four wide) to get both a net delta and probability neutral setup:

Put Side Short Put Leg: 17 delta

Put Side Probability of Profit: 83%

Call Side Short Call Leg: 2 x 12 delta

Call Side Probability of Profit: 82%

Resulting Setup Delta: .07

Naturally, skew isn't always to the put side; it's sometimes on the call side, where we'd do the opposite to accommodate skew: double up the number of contracts on the put side (but at half the spread width of the call).

BIDU IRON CONDOR with high Probality of ProfitHi everybody!

After a very big break - MrAnonymCrypto back on board!

The past year I'm spent for learning and developing my new trading system and indicator pack and full trading strategy system for option trading of the us stock market. I'm tired to waiting for any bitcoin daytrades and unregulated price moves: those instruments eated my life and time.

Ever since I’ve only been dealing with the stock market for up to an hour a day: my life has changed - in a positive direction.<3

Today I'm releasing the first live tradig publication of my indicator: the Iron Condor Hunter . // If you are new in the option's world I'm recommending to learn options first via tastytrade youtube videos //

More about my Iron Condor Hunter script in advance:

This script is for neutral credit strategy trades. This script indicates the secure Iron Condor setups automatically on any liquid+volatile instrument, based and calculated with auto Murrey Math level script and current price actions, and IVR. (MurreyMath is my other script, telling more later) If the script indicates new potential setup: you can see a blue background with the levels of the Iron Condor wings, automatically! You can check the success rate of the script for the past with same setup I've designed this indicator for 45-60 days expirations, (because you can exit automatically at 50% profit in 30 days, if the instrument stays inside your original range!)

And now, let's look an today live example: BIDU

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

REASONS

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

(1) Backtesting the indicator

17 Iron Condor detected in the past 10 years, with 100% succes rate, with exact range detection at the beginning.

Today I'm catched another signal, so I'm grabbing the opportunity!

(2) The trading range & IVR

Today Iron Condor Hunter script detected the 372-221 range for safe-play this setup.

Because the most volatile expriation is the April 16th in the 45-60day range: I'm playing this for credit.

The (tastytrade) IVR is high (above 80) - this is very high Implied Volatility Rank - safe for credit play, the instument is liquid.

Good Defined Strikes:

Sell 1 BIDU Apr16' 220 put Buy 1 BIDU Apr16' 210 put

Sell 1 BIDU Apr16' 370 call Buy1 BIDU Apr16' 380 put

(3) Divergence on my oscillator

As you can see: the very obvious divergence is detected at the overbought levels.

This and the formation meaning for me: some correction started.

No kind of event ( divident ) coming in the next 60 days, so I'm not expecting more significant price movement.

(4) Define safe zones

At Iron condor setups I'm always define some "safe-zone" : for upside and downside too.

Safe zones meaning for me: I can sleep peacefully until the price is moving between these edges.

BUT! If the safe zone beaks: my eyes on the final strikes.

Another seat beld is the 0.618 fib-retrace level, because if the price is falling straight down: at this level we are expecting some resistance. But in current case: the fib 0.618 level is inside our range.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

SUMMARY - MY TRADE SETUP

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Max profit: $288 Max loss: $712 IVR: 87 Probability of Profit: 68% Expiry: 50 days Strategy: 67.7% wide delta neutral Iron Condor for credit Risk management : I'm closing the trade immediately - if the daily bar closing outside my strikes - and I'm cutting my loss. (no matter what I'm believing)- usually I'm losing mutch less than my max profit in this case.

Profit management: I'm sending an order at the 50% of max profit, immediately after my position successfully opened

Welcome any comments:

* whether about the options, my indicators in the future.

* in private, I will be happy to help you with any questions about the option for free.

* are you interesting in options, or only "when bitcoin moon"?

BIDU - neutral possibility BIDU is a ticker that has recently been beat down. Looking at the four hour we can see that its in a falling wedge, a bullish pattern. we have a cross on on the MACD and a TTM that shows an increase. short term still seems a little bearish and an inverse cup and handle can be seen however it seems that tech is making a strong come back and hopefully that continues.

Im thinking we might see some sideways action for a little bit, bouncing up and down.

IRON TARIHi guys!

New Iron Condor, check my last trades, and get my script for free!

But I went in trading a strangle, RR is better, because I get out from the losing leg for a lower loss

Enjoy your wallet!

Tari.

IRON TARIHi guys,

this is a new trade for this week.

Since the low IVrank I trade this with diagonals, to benefit of an IV rise.

Subscribe for free to my strategy and

Enjoy your wallet!

Tari.

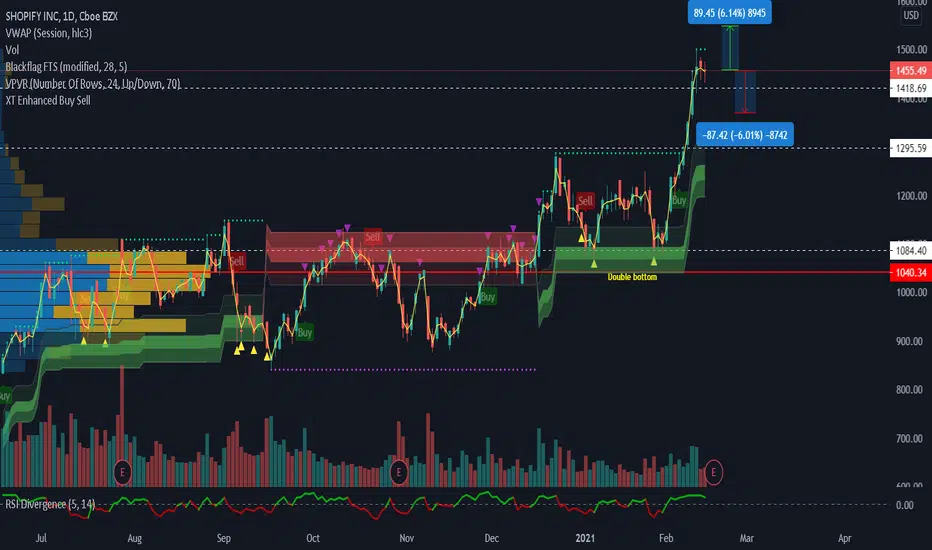

Evening star pattern, up 25% just in February prior to earningsSHOP has been a beast for along time! It has runup 25% just in February, so be careful for earnings on Feb 17th. The past 3 days show a bearish evening star pattern (not 100% perfect). I calculated the implied move to be 6% or $90 dollars. Options - 1068 in $1500 weekly calls, over 1600 in $1200 weekly puts. If you know how to play iron condor, I think that is best earnings trade o capture premium. They beat last earnings and raised expectations , its going to be hard to repeat, imo. Have a great long wknd!

IRON TARIHi guys!

New Iron condor, check my last trades, and get my script for free!

Enjoy your wallet!

Tari.

IRON TARIHi guys!

New Iron condor, check my last trades, and get my script for free!

Enjoy your wallet!

Tari.

IRON TARIHi guys!

New Iron condor, check my last trades, and get my script for free!

Enjoy your wallet!

Tari.

IRON TARIHi guys!

New Iron condor, check my last trades, and get my script for free!

Enjoy your wallet!

Tari.

IRON TARIHi guys!

New Iron condor, check my last trades, and get my script for free!

Enjoy your wallet!

Tari.

IRON TARIHi guys!

New Iron condor, check my last trades, and get my script for free!

Enjoy your wallet!

Tari.

IRON TARIHi guys!

New Iron condor, check my last trades, and get my script for free!

Enjoy your wallet!

Tari.

IRON TARIHi guys!

New Iron condor, check my last trades, and get my script for free!

Enjoy your wallet!

Tari.

INTC -- iron condor over againI like doing iron condors on Intel all the time and consistently just keep rolling them out. Never a huge risk play with Intel in my opinion with smaller spreads but always adds a little daily theta to my portfolio.

I don't do a lot, really none at all, Elliot wave counts with Intel. Recently, I just draw supply and demand zones and trade the range.

My play: will look to enter an iron condor tomorrow, looking to sell the $57.50 strike call to upside (buy 60) and sell the 47.5 strike put to downside (buy the 45). Simply approach play and not throwing a lot at it. Something to balance out portfolio a bit and grab some daily theta. Earnings are approaching, however, but will still look to enter this play.

Options strategy Iron CondorIron Condor - a spread with limited risk and limited profit, using four different striking prices but the same expiration date. The position is a combination of puts and calls all of which are Out of the money. The maximum profit is realized between the two inner strikes, and the maximum loss is realized outside of the higher and lower strikes.

This strategy is preferable for beginner traders because there is no unlimited risk theoretically, unlike selling straddle/strangle. When selling an Iron Condor (or Iron Butterfly), the trader is neutral.

Because all the options are Out of the money, the trader receives credit for it.

The inner options are being sold, those options worth more than the outer options that being bought, inner options are closer to the stock price, which means their strike is closer to At the money strike (to more expensive options).

If the stock price closes between the two inner strikes at expiration, all the options will expire worthless. The trader will receive all the credit.

Chart example:

Inputs:

Credit recived-> 13.45, Stock price-> 484,

Top Upper strike (Bought) ->560 Call

Top Lower strike (Sold) ->530 Call

Bottom Upper strike (Sold) ->450 Put

Bottom Lower strike (Bought) ->450 Put

Days to expire -> 46

Implied Volatility -> 46.7% (0.467)

Date - > 02/11/2020

Maximum Profit = The credit recived = $1345

Maximum Loss = Difference in Upper (or Lower) Strike – the credit

= 560 - 530 – 13.45 = 16.55

= 450 - 420 – 13.45 =16.55

Maximum Loss = $1655

If the Iron Condor is not balanced (the differences between strikes are not equal like in this example), the calculations are different.

Like selling Straddle / Strangle, the same conclusions about increase or decrease in Implied volatility are true here.

In these conditions, it will take 10 days for the position to enter the profit zone and 35 days to receive 50% of the credit.

This post relates to previous posts.