Prepare for LIFTOFF $ADAThe Global Net Liquidity index is breaking out of its multiyear downtrend channel on the back of a weak TVC:DXY dollar. Altcoins like CRYPTO:ADAUSD and other risk assets historically wildly outperform during Global Net Liquidity uptrends and dollar debasement cycles. As the business cycle heats up with ISM Manufacturing PMI ECONOMICS:USBCOI rising above 50, expect altcoins to gain relative strength to CRYPTO:BTCUSD and a Bitcoin Dominance

CRYPTOCAP:BTC.D collapse into the 35-45% range.

This is your last chance.

ISM

ride the gold with premium trade backed with macro market data analysis to predict ism news and it's affect on dxy then correlation with gold also fundamentals approach on gold bearish and take advantaghe of entrys on technicals

eurusd oportunutybacked with ism to provide momentum and liquidity fundamentals to determine the bias or the direction tech to execute 'enter' 'exit'

ISM Indices vs. GDP YoY% - Leading Economic IndicatorsBoth ISM Manufacturing Index and Non-Manufacturing Index vs. GDP YoY% for the US economy.

ISM Manufacturing: Yellow

ISM Non-Manufacturing: Blue

GDP YoY%: Green/Red

ISM Manufacturing currently signaling contraction with a level below 50 and the momentum seems lower.

Non-Manufacturing Index is likely to follow the same path although currently signaling growth, but less than before.

GDP YoY% could potentially experience a slow-down within the next 6 Months to a Year.

The FED has being somewhat more Dovish on the latest speech, as they're seeing a negative outcome in keeping Interest Rates higher for much longer.

ISM Manufacturing New Order IndexMacro Monday (6)

United States ISM Manufacturing New Order Index - ECONOMICS:USMNO

This week I have honed in on the Institute of Supply Management Manufacturing New Orders Index (ISM New Orders Index) as it is the largest component of the headline Purchaser Managers Index(PMI) making up 30% of that index. I also make the case below for how it can act as leading indicator of demand by way of trend projection.

The ISM New Orders Index is an indicator of U.S. economic activity based on a survey of more than 300 purchasing managers at manufacturing firms advising if orders have increased, decreased or stayed the same. Survey responses reflect the change, if any, in the current month compared to the previous month.

A reading above 50 indicates the expansion in the manufacturing sector which is interpreted as a positive indicator of economic growth. A reading below 50 indicates a contraction in the manufacturing sector which suggests a slowing economy.

According to Investopedia "ISM data is considered to be a leading indicator of economic trends. Not only does the ISM Manufacturing Index report information on the prior two months, it outlines long-term trends that have been building over time based on prevailing economic conditions".

The ISM reports are released on the first business day of each month for the month that has previously closed. Thus, they are some of the earliest indicators of current economic activity that investors and business people get regularly.

ISM New orders provide an indication of current consumer demand. Utilizing a chart of New Orders readings we can attempt to understand the trend of consumer demand forward. ISM New Orders could be considered an additional gauge of consumer sentiment because if businesses are reporting increases in orders month over month, this demonstrates consumers have the consistently had the resources and the desire to spend. If this continues over months a trend can form and we can capture this direction on a chart.

To support the ISM predictive argument I include a chart that illustrates a correlation between the ISM Manufacturing New Orders Index and the University of Michigan Consumer Sentiment Index, the latter of which is considered one of thee leading indicators for predicting future consumer spending/demand. This will be posted in the comments.

According to the University of Michigan, the Consumer Sentiment Surveys "have proven to be an accurate indicator of the future course of the national economy."

Based on the above correlation I postulate that we can use the ISM New Orders Index as an additional leading/predictive indicator to establish what direction consumer demand is trending.

The ISM New Orders Chart

Focusing on the ISM Manufacturing New Orders Index Chart you can see that a breach below the sub 50 level can act as a leading or affirming indicator of a slowing economy, lowering consumer demand/sentiment and ultimately recession.

Orange Zone

Historically If we enter into the orange area and stay there for greater than 7 months it has resulted in a recession every time except for 1966 and 1995 (8 out of 10 times). Some analysts have recognised and compared the similarities of the current period to the 1995/96 period. The similarities are evident on this chart with two touches or bounces from the red zone which appears to be happening at present. The August and September ISM New Orders reading will ultimately tell us if this will play out similar to 1995/96 or not. We know what to expect if it doesn’t.

Red Zone

Anytime we have entered into the red zone we have confirmed a recession. Its key to realise that recessions are typically assigned 8 months after they have started and this could mean we are already in one... Interestingly we have toe dipped into the red zone twice, in Feb and May 2023 however I do not see this as a definitive move into the red zone, I see these as bounces from this level as noted above.

Moment of Truth for ISM New Orders

What is clear from looking at the chart is that we are at a critical juncture as we have been 13 months in the orange zone which is a historic first. The coming months readings for August (released Sept) and September (released Oct) will be vitally important for providing an indication of the direction of the economy.

A drop down into the red zone and you know what to expect. A rise out of the orange area and above the 50 level would be positive however we have been rejected from areas above 50 in the past (see red lines on chart). I have included some rough fractals from periods in the past (arrows in grey) where we were previously rejected from the 52 and 54 level only to be dumped back into the red and into recession. It’s great that we are aware of these potential false flags so that we don’t get ahead of ourselves. It’s important to note that these fractal examples from 1980, 1990 & 1967 are not projections, just observations from past readings on what may be possible. It only highlights that we need to be cautious, even if we rise above the 50 level, we can be rejected into recession from the 52 and the 54 level. This is why we need help from other charts and indicators to help gauge the likelihood of a continuation higher or rejection lower.

Here on Macro Mondays we have been and will continue to build a portfolio of leading market charts/indicators that you can check for free on my Trading View and see how they are all progressing. These charts will include trigger events and will be updated as matters progress. The charts can help inform you of the direction of the economy, the market and help you anticipate or time any potential looming recession.

Some prior charts and their indications to date (all linked under this article);

Concerning Charts:

o Macro Monday 2 – The 2/10 year Treasury Spread FRED:T10Y2Y : The current yield curve inversion on the 2/10 year Treasury Spread historically provided an advance warning of recession/capitulation in 2000, 2007 & 2020 however it provided us a wide 6 - 22 month window of time from the time the yield curve made its first definitive turn back up to the 0% level. September will be month 6 of that 6 – 22 month window and thus we are clearly entering dangerous territory.

o Macro Monday 6 – ISM Manufacturing New Orders Index ECONOMICS:USMNO : Its clear from our chart shared today that the ISM New Orders Index is also entering into dangerous territory having been below the sub 50 level and in the orange zone for 13 months. This has never happened before without a recession, bar a lessor 12 month timeframe in the orange zone in 1995/96. The ISM Manufacturing New Orders readings for August and September will be vital indicators for the direction of the economy.

o Macro Monday 4 – Global Net Liquidity Vs S&P 500 NYSE:GNL : We shared this chart on the 3rd July as an advance warning of an imminent and expected pull back in the $SPX500. A negative divergence was evident on the chart as Global Net liquidity was decreasing for 6 months from Jan – July 2023 and the S&P 500 increased over the same period. Please review the chart press play and see how accurate this call has been. GNL is currently signalling at minimum a continued correction over the months of Aug and Sept.

Side Note: I am very aware of the Halloween effect in which markets rally into the months of October – December thus a pull back in Aug/Sept could end up being short term with a surge in the markets in October. The ISM reading for August (released in Sept) and September (released October) should help us gauge what outcome is more likely. Any increase/decrease in GNL will also offer insight over those months. Aside from this we should be aware of any Fiscal Stimulus that is announced as this would likely have a significant impact. I hope to cover Fiscal Stimulus in coming Macro Mondays, it’s a work in progress.

Charts Demonstrating Strength:

o Macro Monday 1 - Dow Jones Transportation Index ( DJ:DJT ): The transportation sector acts as a leading indicator as it is further up the value chain ahead of the final products being sold by companies in Dow Jones Industrial Average $DJI. It is similar to ISM Manufacturing New orders in this regard, ahead of or at point of sale execution. When the Dow Jones Industrial Average TVC:DJI is climbing higher while the DJT is falling (Negative Divergence), it can be a signal of economic weakness ahead, this occurred prior to March 2020 capitulation, making this a very valuable tool to have in our arsenal.

- In our chart recently shared a positive weekly MACD cross gave us a heads up that price might break through strong resistance levels, which it in fact did. If we can make the prior resistance level support and bounce off the support, price could stretch to all-time highs at which point we can reassess.

o Macro Monday 3 – SPDR Homebuilder Index AMEX:XHB : The Chart can be used as a leading indicator for the US housing market as the stocks in the XHB comprise of companies that provide the materials and products to build new houses and renovate homes. These products are higher up the supply chain and sold before construction commences or during. In the past the XHB chart provided a significant advance 12 month+ warning of the 2007 Great Financial Crisis which is illustrated in red on that chart.

- Since sharing the chart price appears to be on course to testing its all time high and has a bullish MACD Cross on the monthly. This could also be a double top however historic positive MACD Cross performance suggests we have higher to go. Its looking positive.

o Macro Monday 5 – Arca Major Markets Index (XMI): The XMI has proven itself as a leading indicator as it provided an advanced 9 month warning of the follow up recession/capitulation price action that initiated in Sept 2000 on the S&P 500.

- Since we shared this chart it has broken above its all time highs and is currently resting on support. A bounce higher here would be confirmation of the uptrend, however this could be a false breakout which would be confirmed if we lost the support. This chart will be important to watch for the August – September period also, again highlighting just how important these 2 months are.

Conclusion

Its clear from all of the above charts that the price and readings for the months of August and September 2023 will be critical to determining the potentiality of a recession / market capitulation or for letting us know will there be continuation of climbing the wall of worry. Its clear that we are at an inflection point over the next 60 days. Based solely on the charts shared to date the fact that the DJT, XMI and XHB are still leaning bullish, I remain long term long until these charts break down or the GNL and ISM Manufacturing Index confirms to the downside. That does not mean that we can’t get a 10% ,15% or 20% pullback in the S&P over the next 60 days, this would not surprise me, however based on some of the charts I have shared previously I think it is probably that this will be a temporary pull back. This leans me towards thinking that if there is a hard landing, it will come later in 2024 or even 2025. If that view changes and the above positive charts pull back, ill be the first to let you know.

Stay Nimble folks, August and September are decision time.

PUKA

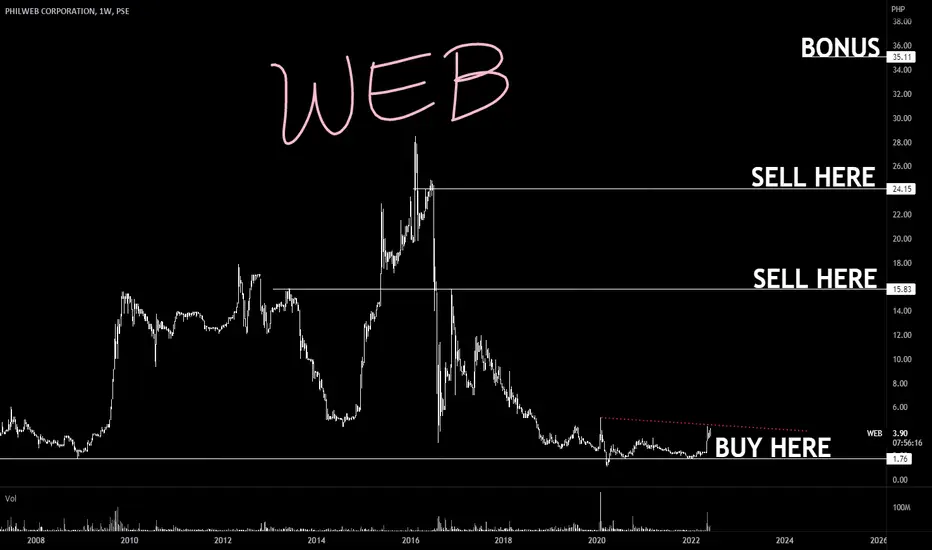

WEB: ₱P3.90 | a Future Unicorn in the Gaming Scene 20x++same handler of iSM a telco backdoored issue acquired by DAU (Dennis Ang Uy) ₱1.0 --> ₱20.0

WEB a favorite bread and butter of Balesin folks (owner of iSM Balesin) turned over to Araneta Group

for a 100 day recovery to fresh highs

entry: spot +- 25%

exit: when youre happy

XLI could be on the verge of breaking down. A close above the neckline negates the bearish pattern.

If Weak ISM data continues you could see more weakness in this sector.

A pair trade I'm watching is Long GE / Short XLI

ISM New Orders vs Consumer SentimentISM New Orders Vs Michigan Consumer Sentiment index

ISM New orders provide an indication of current consumer demand. Utilising a chart of New Orders readings we can attempt to understand the trend of consumer demand forward. ISM New Orders could be considered an additional gauge of consumer sentiment because if businesses are reporting increases in orders month over month, this demonstrates consumers have the consistently had the resources and the desire to spend. If this continues over months a trend can form and we can capture this direction on a chart. To support the ISM predictive argument I include a chart that illustrates a correlation between the ISM Manufacturing New Orders Index and the University of Michigan Consumer Sentiment Index, the latter of which is considered one of thee leading indicators for predicting future consumer spending/demand. This will be posted in the comments.

According to Investopedia "ISM data is considered to be a leading indicator of economic trends. Not only does the ISM Manufacturing Index report information on the prior two months, it outlines long-term trends that have been building over time based on prevailing economic conditions".

According to the University of Michigan, the Consumer Sentiment Surveys "have proven to be an accurate indicator of the future course of the national economy."

Based on the above correlation I postulate that we can use the ISM New Orders Index as an additional leading/predictive indicator to establish what direction consumer demand is trending. Something we can keep an eye on and something that will factor in this weeks MACRO MONDAY Edition which i will post immediately after this

PUKA

PMI Data & How it Effects DXYJust to summarise quickly what the ‘Purchasing Manager Index’ is, it’s a monthly data release by the ISM. PMI data is based on 5 survey areas: new orders, inventory levels, production, supplier delivery & employment.

PMI data ranges from 0-100. A PMI reading ABOVE 50 represents expansion in the economy. Whereas, a reading BELOW 50 represents contraction.

Below is the PMI data for March 2023, which came in at 47.7 which shows the economy is contracting. Now to show the importance of this, let me show you the last few times the PMI dropped below 50👇🏻

2008 - The Financial Market Crash🩸

Early 1980’s - Sky High Inflation🩸

Mid 1980’s - Recession which left unemployment at 7.5%. The recession was caused by tight monetary policy from the government , in an ‘effort’ to fight high inflation🩸

ISM PMI Long Term Chart - 04/08/23The ISM currently stands at 46.3%, signaling a contraction.

Business activity is implying that rising interest rates and growing recession fears are starting to weigh on businesses. The reading pointed to a fifth straight month of contraction in factory activity, as companies continue to slow outputs to better match demand for the first half of 2023 and prepare for growth in the late summer/early fall period.

Frequentist's will tell you that the market tends to bottom six months after the ISM drops below 50.00.

In the chart, I've drawn a channel with fib standard deviations.

This will be a good one to save and track

$JPY - What can we do? $JPY - What can we do?

As mentioned in previous posts, data ISM will impact the market today. However, I am looking at key levels as long as we dont break the lows in the yen - this could be a little bit of a pull back trade we as traders could take advantage of.

Don't forget to trade your own plan.

Trade Journal

$DXY - Pull back?$DXY - Pull back?

We have ISM this later afternoon but technically looks like a pull back occurring!

Trade Journal

Dollar index continues to decline The dollar index continues to decline and tests an important psychological support at 110

Pressure from the ISM manufacturing index and negative expectations for the service index today

The dollar is likely to face a wave of weak demand until the end of the week and the emergence of employment data

to watch

110.00

108.90

Daytrading EURUSD the day after ISM Non-Manufacturing PMII made a backtest EURUSD and U.S. ISM Non-Manufacturing Purchasing Managers Index (PMI) finding a good opportunity going long the day after if Actual PMI is greater than Previous PMI.

This is not a standalone strategy but a good piece of a puzzle before deciding to open my trade. This trade has closed this evening with 100 pips profit.

my puzzle had today a lot of intersting pieces:

1. Advantage from the last ISM release matching with my backtest

2. USDOLLAR reached the fibonacci's extension

3. Chart 6E1!/DX1! close to a support

3. 30min chart. I setted my entry price after rebouncing twice from a double strong support (red lines = weekly and montly highs/lows)

4. Good bullish wedge pattern on EURUSD (1Day chart)

5. Expectation for rising interest rate tomorrow by ECB.

I like trading with a so lot of opportunities

How to make quick 40 pips in USDJPYSince the FED last week went from an ultra hawkish stance to a more data dependant one it is clear that US data will now become even more important and volatile for USD pairs and also for the whole market.

And thats great news! It means we can now extract pips from the market every time there are important US news like for example the ISM manufacturing data today.

If you want to participate you can enter to my group trough the link in my bio.

For the ISM report yesterday it was really easy to get 30-40 pips out of USDJPY:

1. The ISM came better than expected with 52.7 vs. 52.1 consensus.

-> go long USDJPY immediately

2. Algos drove USDJPY higher for 40 pips

3. Take profit immediately when the first impulse of the move weakens.

4. Market participants realize that the most important subcomponent of the ISM, -> prices paid <- , came much lower than expected (60.0 vs 75.0 consensus)

5. USDJPY falls all the way back again

I made easy peasy 40 pips and so can you next time.

ISM New OrdersPersonal notes on the indicator.

Heading lower.

Last major read was fallout of 08.

Incurs a negative bias on the wider economy.

XAUUSD 12H TA : 05.02.22 (Update)If this current strong price support is lost, we can expect a drop to the $ 1845 range . but its not , (PLEASE SEE THE PREVIOUS ANALYSIS)

Follow us for more analysis & Feel free to ask any questions you have, we are here to help.

⚠️ This Analysis will be updated ...

👤 Arman Shaban : @ArmanShabanTrading

📅 05.02.2022

⚠️(DYOR)

❤️ If you apperciate my work , Please like and comment , It Keeps me motivated to do better ❤️

Macro study of U.S. economy - Market warning signals?They do not scream "SELL" just yet, but these indicators offer strong caution of further market correction. Please take some time to study the charts so you understand the story they tell. I am not an economist; I am a trader who has been learning more about bonds and macro indicators.

(I have ignored the pandemic drop because it was extraneous to normal economic factors that move markets.)

ISM Manufacturing

> A leading indicator - below 50 indicates contraction

> Peak expansion in 2021 seems to have ended, yet wages have risen - this will pinch corporate profits

> If next month is lower, it indicates further slowdown (slowing expansion)

> Texas manufacturing for Jan'22 showed concerning declines

> Note the readings below 50 from Aug-Dec 2019 indicated a problem. Covid-19 did not cause markets to drop; it exaggerated the move.

HYG high yield bond ETF

> Includes many junk bonds - indicative of economy's credit situation (corporate, municipal, consumer)

> Yellow lines show the beginning of a significant drop that indicated worsening credit conditions

> Note the "valleys" below 85 match with SPY corrections

> Will this keep dropping to 81-80?

CCI - Consumer Confidence Index

> A leading indication of people's optimism about economy

> Red rectangles show significant drops that corresponded with SPY correction

> Does most recent CCI drop reflect more SPY correction?

Long XLU short IWMIt is time to go defensive again. ISM PMI declining from expansion, historical high percentiles of distribution. US10Y going down together with ISM. Long Utilities as defensive sector, short IWM small-caps high-beta assets.

Best,

Home Depot should be in your WatchListThere is a macro narrative underway that is wildly bullish for Home Depot.

The fuse being lit here under a MASSIVE bull run evident within the latest WSJ article. Get ready for a flood of improvements and investments in homes. Keep in mind how cash flush consumers are, and how pent up they have been in their homes. The WSJ certainly made the case when they said:

"The estimate represents a 52% rise in the nation’s home shortage compared with 2018, the first time Freddie Mac quantified the shortfall."

“We should have almost four million more housing units if we had kept up with demand the last few years,” Mr. Khater said. “This is what you get when you underbuild for 10 years.”

Housing my friends is about to get red red hot.

www.wsj.com

Let's also take a peek at flatbed capacity folks. Flatbeds provide capacity for the construction sector and massive commodities within the logistics sector. New truck sales are up ...gulp 424% in march!

www.ttnews.com

Demand is wild, but who are going to drive all of these trucks with a driver shortage underway at exactly the same time?

Load postings (loads shippers need transported) are up +129.9% Y/Y

Truck postings (trucks available to haul loads) -6.9% Y/Y

-Stats provided by DAT

Let's drill in a bit further folks! This upcoming ratio is a bit like saying... the average temperature in North America is 70.7 degrees Fahrenheit, or 21.5 degrees Celsius for our friends across the pond. Not very helpful if you are trying to zero in to the Florida market vs the Alaska market. But regardless this data is stunning as the current load-to-truck ratio for flatbed is over 80 loads per trucks. In some very hot markets it is well over 120 loads per truck. Think about what that means! The average driver has over 80 loads to select from before hauling his freight. This enables him to bid himself much higher. Obviously this cost to manufacturers and distributors or even those providing raw goods in lowlier verticals all can not just shoulder this costs - it must get passed on to consumers. Clearly this will result in further inflation pressure. It is stunning if you think of it that Dr Michael Burry predicted that the inflation pressures would be observed initially within supply chains...and yes he nailed it.

Citation of chart displaying Load-to-truck ratio:

www.facebook.com

There are many ways to monetize the current situation. And I recommend a plethora of strategies to diversify risk. And this includes exposure to transportation equity products, building materials, commodities, construction starts, and yes Home Depot.

The final comment I have - and please keep in mind I do not subscribe to political tribalism, I play it monk like focused on how we can be opportunistic in any environment-if Biden passes the infrastructure package again this would lead to a massive supply crunch in many of the areas outlined above. Especially flatbed capacity. Keep in mind flatbed seasonality typically does not kick up until May-June when housing and construction starts are heating up.

As always dear traders if you found this content helpful please be sure to like, share, and perhaps tell me what I may be missing in my content here.

Final content share that is a MUST READ. Manufacturing PMI is at 64.7% ... So for those unfamiliar with what that means if the PMI index is under 50 we are in a state of contraction, growth mode is evident with numbers above 50. A reading of 64.7% is frankly remarkable.

www.ismworld.org

Pivot Points

Bollingers/EMA/Volume

Can you see the trend friends?

Home Depot is great as well because keep in mind on days equities sold off in the broader market, they continued to march higher as well.

Let the roaring 20's commence! And please be sure to follow me on TradingView as I will let you know any helpful content I can find as we navigate through the rest of this decade.

Good fortunes to you dear traders!

The myth of hyperinflation series #7- Supply & productionLet's keep it simple.

Increase in raw material & production cost-> Decrease in aggregate supply (Suppliers drop out as profit deteriorates)-> Decrease in total production->. If demand remains the same (most likely going to be the case unless there is another stimulus check coming in), then remaining producers/suppliers who now have more pricing power can and have to pass down the cost to consumers-> Potential supply-induced inflation happens as the same number of buyers chase after the shrinking pool of goods.

However, the chart shows no such risk. As the consumption picks up, supplier/producer starts to hire more people (Manufacturing employment) and ramp up the production lvl (Manufacturing production). The increasing demand is matched by the increasing production (manufacturing production keeps up with the demand of the new order) and declining inventory (Manufacturing inventory). In other words, even though oil price and raw material cost rose (still below the historical standard), we didn't see any decrease in aggregate supply . Of course, I have simplified the matte and left out many details, but I think the only issue we have to worry about that can cause the imbalance between aggregate supply and demand is the potential supplier delivery difficulties being mentioned in the ISM report.

In general, supply is elastic, meaning that the producer/supplier usually rush to increase the production/capacity as the price of good and demand go up because capital has been abundant ever since China joined WTO and the interest rate has been suppressed to such a low lvl ever since sub-prime mortgage crisis. The whole world is on the disinflationary trend as we live in a world of excess savings and insufficient demand because developing countries constantly export their savings to developed countries and because the disposable income doesn't keep up with the inflation.

Such over-capacity/overproduction & over-abundance of capital and good will keep the price lvl low & affordable and the inflation lvl manageable, especially in the disinflationary environment in which there is a moderate amount of consumer demand.

Next, I will talk about some of the external factors and circumstances that could influence the possibility of hyperinflation.

ISM vs SPX yoy divergence signals more downside comingBig ISM decline with SPX divergence is signaling more SPX downside is likely in coming months

fast scalping for XAU/USD Go Long 5mins before the ISM revealedthere are some rumors that ISM Manufacturing PMI will be negative

so for the fast scalping

I recommended buying GBP/USD and XAU/USD

for at least 15pips Movement 5 Minutes before the news published in Forexfactory

instagram : Simonezed