JXY

Weekly Analysis JXYTrend: Down

Phase: corrective

Trade: SELL

NOTE:Truths

-Traders will do the same thing over and over again.

-In trading, no one to blame and no one to question what price did.

-Price can break any low/High because anything can happen.

If you fully allign your thinking in line with the truth about the market then you will win.

LQD: Follow the Fed? The key themes going into next week will be stimulus. The update from the federal reserve this week they showed they are purchasing high quality corporate ETF's (a new asset class for them) and amongst the ETF's being purchased was LQD . As you can see, it clearly benefited. For some that have been in the game for a while, front running the FED has never been our cup of tea, but the purchases of corporate bonds could be something that could be emulated successfully. The interest will be there, but I doubt that it's NOT already counted in.

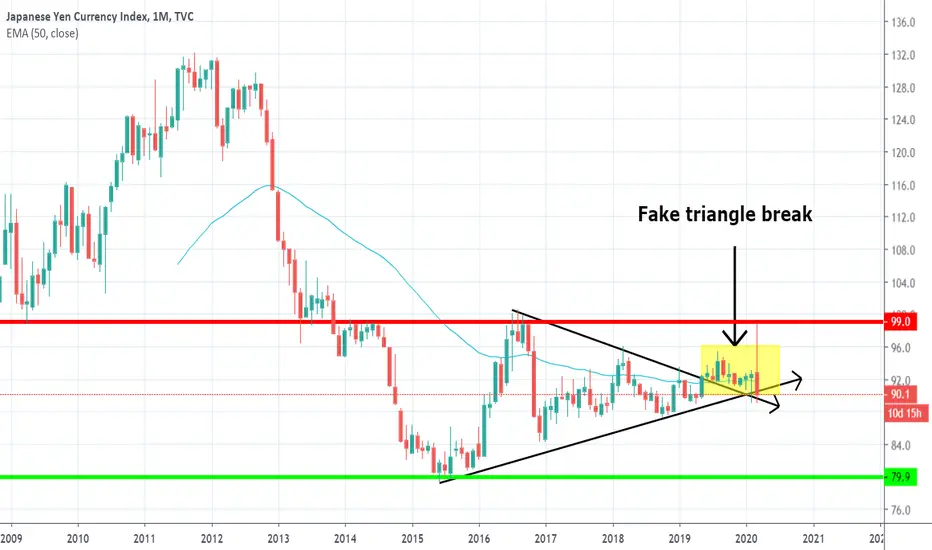

Jpy pairs- where nextIn 2019 we had what, at that point, seemed to be a break to the upside (Jpy pairs weakness) of a triangle. The beginning of March came with a big reversal from 100 zone resistance and Jpy index is trading now at 90 support zone. I expect this support to be broken and 2020 be dominated by Jpy weakness (JPY pairs uptrend)

Weekly Geopolitical Fundamental AnalysisGeo-Political Analysis

Headline risk out of Asia has been the Coronavirus. The Shanghai composite dropped along with iron ore, reaching their daily limit and risk aversion. Interesting enough this wasn’t spilled over to FX markets which I think stem from traders staying out of the market prior to the amount of event risk inhabiting traders to what could be volatility across assets. USD/CNY climbed to the highest point since December of last year spiking over 1%. This was the single greatest single day change going back to August 5th of 2019 as risk aversion from the Coronavirus grips Asian-Pacific markets.

Oil

Taking a lot at crude, we’re seeing price bounce after its low at 55.90; the same point from the August swing low. If this price is broken, the next area of support will be around 2- year lows so I think a bounce here combined with the technical from my other article will hold steady with former support possible turning into resistance. The $55.6 price will be an interesting price to watch. This is also earnings week which could move equity markets from companies like GM, Uber, Twitter, Disney, etc. Robust earnings could offset the risk-aversion that we’ve seen because of the coronavirus which is important to remember. Overall the Corona virus seeks to disrupt global supply chain networks powered base line to growth

Gold

Gold price could decline more from here. The State of the Union Address is given this week by President Trump and will likely cover topics on his achievement on trade, record high markets, unemployment rate, as well as other statistics. He may further touch on the tax cuts which he mentioned at the World Economic Forum. If he hints at more expansionary policy it could ease the against seen with the rise in FED funds rate expectations. The implied policy rate is rapidly declining, which a 50-basis point cut by the Jan 2021 meeting. This picked up significantly in the last week with the Coronavirus. Since the start of the China trade war, almost like the coronavirus we’ve seen the U.S. China trade war a political virus that’s spread throughout the world.

Iowa Caucus

The first caucus in the dem nomination takes place in Iowa this week. Victory in this particular state can give a candidate (theoretical) enough votes to win the DNC. In the fast 5 DNC’s the winner has gone onto be the party’s nominee. I will go over some candidates and their fundamental impact on the market in another article. As we’ve seen under Trump, global growth has fallen below the benchmark set by the IMF and leading institutions, we’ve seen the U/. S. China trade war create disruptions in manufacturing and supply chain networks and manufacturing and overall lowered the projected baseline for growth. This was a big reason for the demand for dollar, and the surge to 100 that I think is in the near future with the amount of geopolitical uncertainty currently in the marketplaces.

As candidates progress towards election day, here’s a refresher of the candidates’ stances and the market moving potential:

Regardless of the political spectrum; the only question that markets care about is do they bring more or less certainty to the global economy? Generally speaking, markets don’t care about political categorization. Markets are more concerned the economic policies intended (and truly intended) by the leader of the free world. The only factors that investors look at is the degree of severity in their policy.

Biden/ Buttigieg:

Market sentiment would be risk-on (relatively moderate in policy compared to trump or warren or sanders). We could see them calm market worries because it removes uncertainty.

AUD/USD, NZD/USD higher, JPY and CHF lower (risk-off)

Biden/ Pete

These would be seen as figures of certainty. Risk-on; “relief rally”. I say relief rally because of the amount of turmoil that Trumps administration has caused through its protectionist inclined policy has falling below the baseline compared to the IMF and other reputable institutions and is in need of an improvement. This would be seen as a suppressant for VIX.

Biden: His policy on trade is more moderate based off of what he’s said. He’ll be likely to deescalate the Iran deal and reinstate 2015 ‘nuclear agreement’. This would be bad for BRENT, good for equities, and bad for risk-oriented assets. As we saw crude in 2019 in large point were manipulated by disruptions in supply chain, this would further crush an already over-demanded commodity.

Bloomberg: Just like Biden and Buttigieg, he’s also moderate and would be positive to risk sentiment (risk-on). More “market friendly”. As the candidates narrow down, we haven’t seen the poles have an impact on markets. That’s because the field of the democratic candidates are too broad; now we should see more and more impactful market moving volatility. In the eyes of the markets, do they bring uncertainty or certainty? It boils down to that.

International Trade Conference

The uncertainty during this time by the public debt reached a record high of 17$ trillion (negative yielding debt) and gold followed suit. If there’s a return to necessary to a return to multilaterals and away from protectionism at the next meeting and it could ease this and offer relief to the Aussie dollar the NZD/USD. This comes as the IMF just put out the world economic last week in Davos and said that while growth is anticipated to slow, their seeing “moderate “signs of stabilization. However, the coronavirus could derail this.

Corona Virus:

Considering the frontier and emerging market economies are much more vulnerable to economic systematic risk such as the coronavirus, countries such as Vietnam, Malaysia, Philippines, India, Hong Kong, and China could have a significant negative cascade data from emerging markets inflation (PMI). This can be used to gauge the health of emerging markets when we are seeing global equities stabilize. If we see weak data out of the emerging markets, we could see outflow from the economies. While we may expect these numbers to be higher, what we’re seeing is that paranoia about the coronavirus gave purchasing managers caution that may have been productive rather than the true intention.

Yields

Looking at yields from France, Germany, Canada, and the U.S, yields have broadly declined back to short minus longer term bond yield inversion. . It could be that the virus resumed the downward resumption as investors seek safer assets such as equities. Interestingly enough, declining bond yields (US sovereign debt) it has its own risk. As the leveraged loan market and debt in the market in general is rising to new highs, it should be brought to our attention with the FED quoting it “elevated” and the concern about the stability of the actual economic machine lays in question. A leveraged is a loan to a highly in debt company with a poor credit history. It allows barrows to magnify projected earnings. This leads to a distortion in the ratings attached to each loan, which has various degrees of risk rated with something who’s risk is not properly reflected in the rating. This, called collateralized loan obligation, is similar they aren’t the same as a mortgage back obligation (MBO). My point is, is that an implosion of this leveraged market could drive investors who want to purchase bonds from a comparably higher rate secured, we could see the AUD/USD, NZD/USD, and emerging markets fall thus further.

Taylor Norboge