$SOFi soared 8 days straight, 15minOn Thursday, Oct 10 I purchased two NASDAQ:SOFI 15 NOV 24 9c @ $64 ($128 total).

ENTRY @ $8.72 (12:27pm, Thu, Oct 10) because I noticed NASDAQ:SOFI had been undergoing a temporary recovery to the upside.

EXITs @ $9.99 & $9.93

- 1 contract - Profit taking at 120% ($64 -> $141), Mon, Oct 14 @ 1:18pm

- 1 contract - 6% trailing stop triggered at 114% ($64 -> $137), Mon, Oct 14 @ 2:15pm

Total revenue: $278 || Profit: $150

This is a good point to grab profit because price is around the 0.214 fibonacci and there is a gap to fill to the bottom which increases the chances of the stop dropping below continuing its journey to the upside.

Loans

$CNINTR - Interest Rates Cut- The People’s Bank of China on Tuesday trimmed its one-year loan prime rate (LPR) by 10 basis points from 3.65% to 3.55%, and reduced the five-year rate by the same margin to 4.2%. The cuts follow reductions in other interest rates last week.

The LPR sets the interest that commercial banks charge their best clients, and serves as the benchmark for household and corporate lending. The one-year rate affects most new and outstanding loans, while the five-year rate influences the pricing of longer term loans, such as mortgages.

This is the first time the PBOC has cut both LPR rates since August 2022, when renewed Covid lockdowns and a deepening property downturn were pummeling the economy.

PRA Group: Bullish Shark at a Weekly Support Congestion ZonePRA Group is currently trading above a Support/Resistance Congestion Zone visible on the Weekly Timeframe, and at this zone it has formed a decently sized Bullish Shark pattern with a Bullish PPO Arrow as confirmation, and this all happens to align with the all-time 0.786 retrace. If this plays out, I think it could come back up to make around a 0.886 retrace, which would put it at around $60.

For further context, PRA Group is a Debt Buyer/ Collector, which is something that furthers my interests in the stock.

Consumer Credit: Harmonically Set Up to Return Down To TrendConsumer Credit has recently risen to over $1 Trillion and this rise happens to align with a 2.618 Fibonacci Extension and the PCZ of a Bearish ABCD. If we view this based on the expectations of Harmonics and Fibonacci, we would expect that this is indeed the top and that we will now begin a retrace back down to trend, which could likely land us between the 50% and 61.8% retrace down at $600–$500 Billion as those retraces line up with the trend line we have formed.

Is the delinquency rate too good to be true?The red indicator shows the level of delinquency for each quarter.

The blue index is the SPX.

We have an inverse correlation.

With the increase in interest rates around the world, the cost of money becomes more expensive.

The payment of loans becomes more expensive, so the percentage of defaulters tends to increase.

To pay off debts, positions in the equity market are liquidated.

I'm waiting for the Q3 result (quarter 3 - July to September).

Any bullish indication above the value of 1.24 (quarter 1) would already be a yellow signal.

A value above 1.43 (Q1 2019) would be a red flag for an earthquake.

That would trigger a further drop in the equity market...

UPSTUpstart has a 7price target from myself In the future. Maybe a good buying spot..

Look at names like FSLY to compare

How Will Increased Interest Rates in the USD Affect Crypto? Now that the Federal Reserve seems committed to raising interest rates in response to inflation (something that they denied was a problem during 2021) we're going to see a shift in the way money is talked about in the near future. What does this mean for crypto, and the greater economy, overall?

- The US growth and assets markets have been driven strongly by the availability of cheap loans since 2008, an era that is now coming to a close because the only way to avoid a hyper-inflationary economy in the USD right now is to raise interest rates.

- The historic rate at which the US Treasury printed money -- largely justified through COVID woes -- is extreme and it's TBD whether or not the proposed rates will be enough to offset its after-effects. (Was initially 2%, now proposed to ~3%.) The government is broke and has no other choice.

- Higher interest rates are generally bad for "risk-takers" in the market, but good for people who like to save. The idea of the government and financial sectors actively encouraging people to save, however, has been missing from the mainstream narratives for a while. Whether or not the institutions can adapt fast enough to form a holistic plan in the midst of the turmoil is yet to be seen. The condition has been around long enough that this scenario will be new to even "experienced" financial experts out there.

- This presents a new economic landscape/opportunity for entrepreneurs and investors looking to capitalize on the change. But in this environment, the "slow growth" approach is likely to be more successful than the marketing-driven hype markets that has dominated the scene for the last 10-15 years. (Yes, even in crypto. ex. SHIB, NFT-hype.)

- Generally speaking, countries with higher inflation rates tend to have higher crypto adoption rates as well. Will the same happen to crypto, NFTs, and metaverse -based assets? Time will tell -- but now crypto at least has the title of an "alternative asset" with the potential for high growth, especially since it's not affected by supply chain issues that traditional assets are tied into right now.

- Since 2021 there have been a lot of crypto-based projects that have tied itself into the USD markets through traditional legal arrangements and contracts (as opposed to "pure" crypto investments that aren't concerned with what the traditional markets are doing right now) -- this money is more likely to run in parallel to the outcomes that fiat money will face as the interest rates start to ramp up in 2022.

Bank charter approved, go long $SOFISOFI has been successful in achieving a bank charter through the acquisition of California-based community lender Golden Pacific Bancorp.

It has been consolidating on the weekly chart for almost a whole year now. With the MACD curling up & histogram turning white heading towards green while the RSI is heading to test 50, I really like this set-up.

Some say it is priced in already. I highly doubt that. This stock could easily hit a $25 billion market cap (roughly the market cap of HBAN, which I say would be a reasonable comparison/achievable target since HBAN is a plain vanilla regional bank) with the combination of having a super app with the backbone of a bank charter. If it were to hit that market cap, SOFI would be trading at roughly $30.98. More than a double from here.

It seems to be the perfect time to go long. The combination of student loan management, IPO access, banking, crypto, stock trading, etc all in one app gives it a significant edge. If it can catch some momentum and pass $50, then it could be headed much higher.

An extremely bullish case would be SOFI reaching PYPL like numbers. SOFI's total assets increased from Sept 21 to Dec 21, while PYPL's decreased. On the day Dec 31st, 2021, PYPL had roughly 8.22x the assets of SOFI. Just throwing out a rough number, with net interest margins being added into the revenue basket for SOFI because of the bank charter and the potential to continue to increase its AUM and total assets then you could throw out a share price of $112.70 ($13.71 * 8.22).

Volume has been steadily increasing indicating increased interest and coverage. Oops. EBITDA somehow was from UCTT on the initial post and Tradingview won't let me edit it, no worries. Here is the chart with SOFI's EBITDA has shown some recent upward momentum.

This is just a theory, not financial advice, please do your own DD.

Affirm ~ AFRMCan see afrm possbily getting a push towards 88 R

above 84 , 88 follows . 95 - 104 resistance lvls follow above, likely these are just dead cat bounces and this will continue to fall.

A Success Tunnel for 360 DigiTech: Business TransformationChina's outstanding loan balance reached a fresh record of CNY 172.75 trillion in 2020 and keeps growing, spurred by the increasing digitalization and booming e-commerce market.

In China, 2020 was a milestone year for fintech. The year saw heightened regulatory scrutiny, intensified competition and business patterns were altered by the COVID-19 outbreak, both in the corporate and consumer sectors. The Matthew effect in the industry has been further exacerbated under such circumstances, where small-sized companies with less capital or poor risk resistance ability will be forced to quit the stage.

Although 360 DigiTech, Inc. (QFIN:NASDAQ) is a late starter, it is one of those niche players able to stand up to this fierce competition, mainly due to the reputation of its parent company – 360 Security Technology, Inc. (601360:SH) which brings significant brand visibility to the table.

Strong performance with low valuation

This USD 6.57 billion company is currently outperforming what the market expects. On May 27, 360 DigiTech released its unaudited financial results for the first quarter of 2021. The total net revenue increased by 13.1% to CNY 3.6 billion (USD 0.55 billion) from CNY 3.2 billion in the same period of 2020, while the non-GAAP net income reached CNY 1.41 billion (USD 0.2 billion) with an astonishing increase of 452.8%. The operating income along with the account under the non-GAAP measure achieved a growth of 745.7% and 533.0%, respectively.

However, given this relatively strong financial performance, 360 DigiTech's P/E ratio appears to have been lower than that of its peers for a long time, although it is currently ranked the highest among the top four. Lexin (LX:NASDAQ), a leading online consumption and consumer finance platform, is also using technologies to encompass risk management and loan facilitation systems, just as QFIN does, but its P/E ratio is far higher than that of QFIN. For example, in the third quarter of 2020, Lexin's P/E ratio was more than 5 times that of 360 DigiTech; by Q2 2021, Lexin was lower than 360 DigiTech for the first time, at the level of 8.1. Along with the progressively upward stock price, the necessity of re-assessing 360 DigiTech is becoming more obvious.

How the asset-light business model works

360 DigiTech is one of the earliest platforms in the industry to proactively initiate the transformation of reducing the proportion of self-operated loans and improving loan facilitation. This turned out to be an informed decision.

In the third quarter of 2019, 360 DigiTech first proposed its new strategic target for adopting the 'capital-light,' or more commonly as 'asset-light' business model. More colloquially, this refers to the company directly navigating the borrower to their cooperative financial institution, while collecting service fees from credit evaluation, credit management, or other technical-related services.

According to the published unaudited financial results of 360 DigiTech for the first quarter of 2021, the total loans originated by financial institutions were CNY 74.15 billion, of which CNY 37.25 billion (50.2%) was under an asset-light model and other technology solutions, achieving an astonishing increase of 211.9% over the same period in 2020.

Haisheng Wu, CEO of 360 DigiTech, stated that "...over 50% of the loans were facilitated under the capital-light model and other technology solutions..." and it is a "fundamental change to the nature of our business, from being capital-driven to technology-driven."

The highlight of this model is that as a loan facilitator, the company is not required to inject any margin for each loan. In other words, the credit risk of the asset-light business is borne by the capital; the loan facilitator is thus riskless. Besides, it can better respond to regulatory requirements and resist the impacts of uncertainty on business stability.

Moving further towards 'tech'

In policy terms, the tightening regulatory rules pose a little impact to loan facilitators like 360 DigiTech – even as fintech giants like Ant Group and JD Digits may suffer – as its targets are excess leverage and systematic risks. It creates opportunities for 360 DigiTech to jump a queue. The asset-light model is hence the core strategy of reducing the regulatory and credit risk. Besides, QFIN is trying to use less capital and more technology-powered services to open up more opportunities, both in terms of client acquisition and risk management.

The improved portfolio quality, as indicated by the relatively low delinquency ratio, was one of the contributors for its shining performance even in the special 2020, although it showed an upward-trending slope for the period during the epidemic. However, it seems reasonable: due to the lag of loan repayment as well as its timeliness of statistics, the negative effects of China's -6.8% GDP in 2020Q1 only started to appear in the second quarter of 2020, causing a history of high non-payment ratio of 2.82%. Up to date, the company's delinquency ratio has nearly risen back to the level before COVID-19, and we will keep an eye on its future performance.

Moreover, with a few innovations and technologies, for example, Argus RM Model, Intelligence Credit Engine (ICE), Cloud Bank System, Cosmic Cube System, Apollo Platform and AI Robots, 360 DigiTech is working hard towards the 'tech side' of the fintech business as well as being technology partners with banks. The strategic collaboration with Kincheng Bank (KCB) is a good example.

The bottom line

360 DigiTech's asset-light model works well, and it has the potential to pay off from the long-term perspective, which brings further expectation for its growth prospects. The company's business expansion plans are proceeding with KCB as the first step. These strategies will further improve the company's flexibility in this competition for market share.

EQZ | Flash Loans | Green DildØI'd say, wait n profit.

With some token release yesterday, now we're back to business.

Not a financial advice.

SC Santander Consumer [SHORT]SC Santander Consumer . RSI & CCI reversing at double top. Price at multi-year hi w/decreasing vol.

Catalyst: $66 billion, or 5% of outstanding #autoloans are over 90 days delinquent (up $57B prev yr, & $35B prev decade).

EQZ | Flash Loans | Strategic ReleaseWell, as some nice investors PM me, there's an idea.

I'll keep the investment strategy as Long (some guys told me that i only post LONG xD).

Targets to LONG:

4.5 - 5 w/ max 31 million marketcap;

8 - more w/ max 60m marketcap.

Stop:

As graph.

DYOR please.

Not a financial advice.

If you want to talk about (more), pm me.

EQZ | Flash Loans | Huge x7 possibilityEqualizer did a consecutive breakout and for most users gave them x3/4, but I believe that can give even more, something like x6/7 this month.

Reasons:

No more token release for more than 1 month;

Uniswap getting lower and lower amount available;

Announcements to be released this week, as said on Telegram (BIG);

Not listed on Binance yet;

Marketcap less than 20m (5m x ~3).

DYOR please.

I strongly recommend HOLD than trade on coins that are on begging, like this.

Not a financial advice.

$RKT IPO Winner?We've been long this name since $19 dollars, we continue to believe this company will be worth 5-10x IPO value in the coming years! LONG TERM HOLD

Just a ThoughtIt looks like the third wave has been extended.I think we Usd/zar will make higher highs

Baby Buy Buy BuyXLMUSD broke twice in the past 24 hours. Looks to me like the start of the short bull run.

medium.com

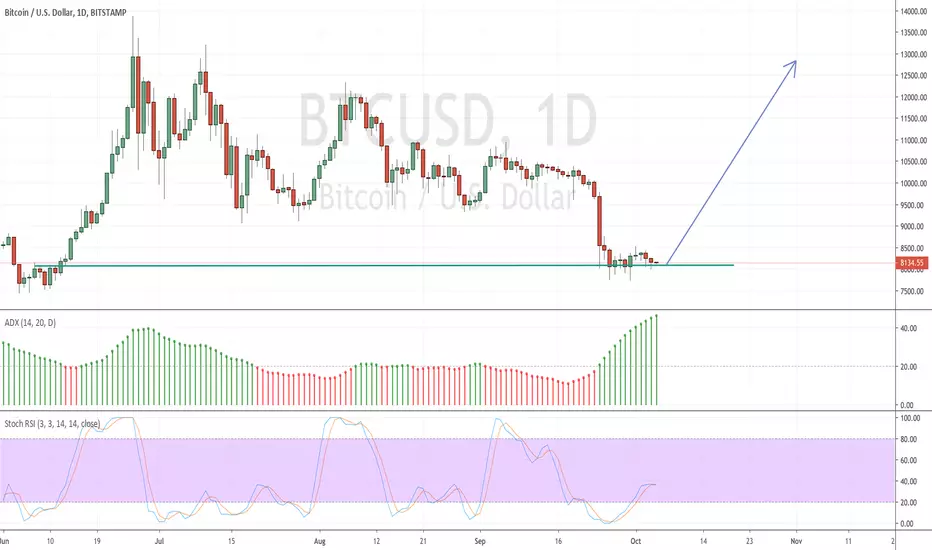

Time to Get More BTCBTCUSD is flat and that's a potential bull run in the next few days and weeks. Time to bag more by leveraging your existing BTC as collateral for a crypto loan and stock up on BTC before it goes up.

medium.com

BTCJPY pretty clean daily chartBTCJPY more sell off to come as it breached the previous support zone.

#WellsFargo | NYSE: $WFC is experiencing a HUGE #ABCCorrection!#WellsFargo | NYSE: $WFC is experiencing a HUGE #ABCCorrection!