Nightly $SPY / $SPX Scenarios for July 3, 2025🔮 Nightly AMEX:SPY / SP:SPX Scenarios for July 3, 2025 🔮

🌍 Market-Moving News 🌍

📉 U.S. Private Payrolls Surround Weakness

The ADP report showed a drop of 33,000 private-sector jobs in June, the first decline in over two years, reflecting businesses holding back hiring amid trade uncertainty. However, layoffs remain low, signaling no acute stress yet

📊 Markets Braced for NFP Caution

Markets are wary ahead of this morning’s Non‑Farm Payroll (NFP) release—currently projected at +115,000 jobs and 4.3% unemployment—based on indications of labor-market cooling from weak ADP numbers

💵 Canadian Dollar Strengthens

The loonie jumped 0.4% as investors adjust expectations for broader central-bank dovishness, driven by the weak U.S. jobs signals and optimism over a revived U.S.–Canada trade dialogue

📊 Key Data Releases 📊

📅 Thursday, July 3:

8:30 AM ET – Non‑Farm Payrolls (June):

Forecast: +115,000; Previous: +139,000 (May). Watching for signs of sustained job-growth slowdown.

8:30 AM ET – Unemployment Rate:

Forecast: 4.3%, up from 4.2% in May. A rise may increase odds of rate cuts.

8:30 AM ET – Average Hourly Earnings (MoM):

Forecast: +0.3%; prior: +0.4%. Cooling wages would ease inflation pressures.

8:30 AM ET – Initial & Continuing Jobless Claims:

Track week-to-week stability or worsening of labor-market conditions.

9:45 AM ET – Services PMI (June, flash):

Monitor for signs of slowing in U.S. service-sector activity.

10:00 AM ET – ISM Non-Manufacturing PMI (June, flash):

Forecast: 50.8. A reading below 50 suggests contraction in services.

⚠️ Disclaimer:

For informational and educational purposes only. It does not constitute financial advice. Consult a licensed financial advisor before making investment decisions.

📌 #trading #stockmarket #economy #jobs #Fed #labor #technicalanalysis

Market

Is Japan's Economic Future at a Tariff Crossroads?The Nikkei 225, Japan's benchmark stock index, stands at a critical juncture, facing significant pressure from potential US tariffs of up to 35% on Japanese imports. This assertive stance by US President Donald Trump has already triggered a notable decline in Japanese equities, with the Nikkei 225 experiencing a 1.1% drop and the broader Topix Index falling 0.6% on Wednesday, marking consecutive days of losses. This immediate market reaction, characterized by a broad-based selloff across all sectors, underscores profound investor concern and a pre-emptive pricing-in of negative outcomes, particularly for the highly vulnerable automotive and agricultural sectors.

The looming July 9 deadline for a trade agreement is pivotal, with President Trump explicitly stating his intention not to extend the current tariff pause. These proposed tariffs would far exceed previous rates, adding substantial financial burdens to industries already facing existing levies. Japan's economy, already struggling with a recent contraction in GDP and persistent declines in real wages, is particularly susceptible to such external shocks. This pre-existing economic fragility implies that the tariffs could amplify existing weaknesses, pushing the nation closer to recession and intensifying domestic discontent.

Beyond immediate trade concerns, Washington appears to be leveraging the tariff threat to compel allies like Japan to increase military spending, aiming for 5% of GDP amidst rising geopolitical tensions. This demand strains the "ironclad" US-Japan military alliance, as evidenced by diplomatic setbacks and Japan's internal political challenges in meeting such ambitious defense targets. The unpredictable nature of US trade policy, coupled with these geopolitical undercurrents, creates a complex environment where Japan's economic stability and strategic autonomy are simultaneously challenged, necessitating significant strategic adjustments in its international relationships.

Nightly $SPY / $SPX Scenarios for July 2, 2025🔮 Nightly AMEX:SPY / SP:SPX Scenarios for July 2, 2025 🔮

🌍 Market-Moving News 🌍

🏭 U.S. Manufacturing Remains Under Pressure

The ISM Manufacturing PMI for June rose slightly to 49.0 from 48.5 in May—still in contraction territory. Tariff-induced uncertainty and rising input costs continue to weigh on factory activity, with new orders still weak and employment contracting

📈 Global Factory Rebound Led by India & Europe

While U.S. factories struggle, India hit a 14-month high in its manufacturing PMI at 58.4, and euro‑zone factory orders stabilized at 49.5—the first sign of recovery in over three years. Asia-Europe divergence may shift global capital flows .

🏦 Powell Says Tariffs Are Delaying Rate Cuts

Fed Chair Powell warned at the ECB forum in Sintra that elevated inflation—driven in part by Trump-era tariffs—has postponed the timeline for U.S. rate cuts. The Fed’s dot-plot now indicates only two cuts for 2025, with markets adjusting accordingly

💵 Dollar Nears 3½-Year Lows

The U.S. dollar weakened further, trading near a three-and-a-half-year low amid soft PMI data, a dovish Fed tilt, and renewed optimism over U.S.–Canada trade talks

📊 Key Data Releases & Events 📊

📅 Wednesday, July 2:

(No major scheduled U.S. economic data)

Market focus shifts to upcoming Nonfarm Payrolls on July 3, Powell's remarks, and trade-talk headlines.

⚠️ Disclaimer:

This information is for educational and informational purposes only and should not be construed as financial advice. Always consult a licensed financial advisor before making investment decisions.

📌 #trading #stockmarket #economy #manufacturing #Fed #inflation #charting #technicalanalysis

S&P 500 Outlook. Best Quarter Since 2023… But What Next?The S&P 500 just logged its best quarterly performance since Q4 2023 , surging on optimism around global trade negotiations and growing expectations that the Fed may begin cutting rates as early as September. US futures are green this morning, thanks to developments like Canada backing off digital taxes, ongoing dialogues with China ahead of the July 9 deadline, and risk-on sentiment is pushing yields and the dollar lower.

But as traders, we need to ask:

Are we witnessing a genuine economic inflection point? Or is this just a liquidity-driven rally that’s pricing in a best-case scenario?

Technical View

Support Zone: 6,150 was just broken through. And 6000, the round number level, coinciding with the 20-day EMA and previous swing level.

Resistance Levels: 6,235 is the next critical ceiling, a clean breakout could see price reach the extension level of 6,415.

Momentum Indicators: RSI remains elevated and is creeping toward the overbought. While momentum is strong, watch out for the possible development of a divergence.

Possible Scenarios

The 'Soft Landing’ Is Now the Base Case

Markets are trading as if the Fed has successfully engineered a soft landing. But that’s now fully priced in, and historically, the most dangerous trades are the ones everyone agrees on. If trade talks stall, inflation re-accelerates, or earnings disappoint, the reversal could be brutal and fast.

Risk-on Sentiment Without Volume Is a Yellow Flag

Despite the price strength, volume has been tapering off. The S&P’s recent leg up occurred on lighter-than-average participation, suggesting institutions may be watching, not chasing. That’s often the case in low-volatility summers, but it also implies that any negative catalyst could cause outsized downside moves.

Macro-Fundamentals May Not Justify Valuation Expansion

Yes, inflation is slowing, and the Fed might cut. But if they do, it’s likely because growth is weakening, not because the economy is roaring. So the very condition that triggers rate cuts could also cap earnings growth!

Projection

Bullish Scenario: A confirmed breakout above 6,280 could carry us toward 6,400–6,500 by mid-Q3, especially if the trade deals progress, July inflation comes in soft, and the Fed signals accommodation.

Bearish Risk: If price fails to hold above 6,120, especially if trade optimism fades, or inflation growth spikes or Fed rhetoric shifts hawkish again, this could then open a quick pullback toward 6,000 or lower, which also aligns with the 50-day SMA.

Key Events to Watch

July 9 Trade Talks Deadline: Any sign of stalling could bring volatility back fast.

June CPI Print (July 10): Crucial for confirming the Fed's next move.

Earnings Season Kickoff (mid-July): Tech-heavy expectations may not be easy to beat after such a strong run.

Conclusion

A record-setting quarter is impressive but not necessarily predictive. This quarter’s rally has been built more on relief and expectations than hard data. When expectations (not earnings) are doing the heavy lifting, any misstep from central banks or geopolitics could unravel gains rapidly.

A rate cut might be delayed, or inflation re-accelerates, or trade talks stall; any of these could leave equities hanging. Remember: the higher the climb without real earnings growth, the harder the fall when sentiment shifts. It's not just about the chart. It is about the narrative behind the price.

What’s your bias for Q3?

Are you buying this breakout or fading the optimism? Drop your thoughts below.

Nightly $SPY / $SPX Scenarios for July 1, 2025 🔮 Nightly AMEX:SPY / SP:SPX Scenarios for July 1, 2025 🔮

🌍 Market-Moving News 🌍

📊 Core Inflation Edges Higher

May’s core inflation rose unexpectedly to 2.7% year-over-year, up from 2.6%, casting uncertainty over the Fed’s timeline for rate cuts. While headline CPI sits at 2.3%, the resilience in underlying prices complicates policymakers’ projections for later this year

💵 Weak Dollar, Rising Rate-Cut Bets

Markets are reacting to “summertime data”—like the core CPI uptick—with renewed optimism. Traders now see up to 75 bps in Fed rate cuts later this year, while the dollar remains near 3½-year lows on concerns about Powell’s independence and trade developments

🇨🇦 U.S.–Canada Trade Talks Resume

Trade talks between the U.S. and Canada restarted today, following Ottawa’s suspension of its digital-services tax. Progress toward a broader agreement could reduce tariff risk and offer further relief to risk assets

📊 Key Data Releases & Events 📊

📅 Tuesday, July 1:

All Day – U.S.–Canada Trade Talks

Markets will watch for updates on tariff resolution and broader trade deals. Any breakthrough could notably boost equities and improve trade sentiment.

10:00 AM ET – ISM Manufacturing PMI (June)

A below-50 reading again would reinforce the narrative of industrial weakness. A rebound could support equities and temper recession concerns

10:00 AM ET – JOLTS Job Openings (May)

Still at elevated levels (~7.39 million in April), this metric assesses labor-market resilience. A decline could shift rate-cut expectations.

⚠️ Disclaimer:

This is for educational and informational purposes only. It does not constitute financial advice. Consult a licensed financial advisor before investing.

📌 #trading #stockmarket #economy #news #trendtao #charting #technicalanalysis

BTC/USD Technical Analysis – Weekly Elliott Wave StructureIn this video, we analyze the weekly chart of Bitcoin ( BYBIT:BTCUSDT ) using Elliott Wave theory.

The current structure suggests the beginning of a new bullish impulse (waves 0, 1, and 2) following a clearly completed and technically correct corrective phase.

We explore potential impulsive scenarios starting from wave 2, using Fibonacci extensions to project possible targets and identifying key support zones and invalidation levels.

This analysis aims to provide a macro perspective based on price action, helpful for traders and investors following BTC from a medium- to long-term technical view.

🛑 Disclaimer: This content is for educational and informational purposes only. It does not constitute investment advice. Each user is responsible for their own trading decisions.

Weekly $SPY / $SPX Scenarios for June 30 – July 3, 2025🔮 Weekly AMEX:SPY / SP:SPX Scenarios for June 30 – July 3, 2025 🔮

🌍 Market-Moving News 🌍

📈 US Stocks Rally to Record Highs

Following a volatile first half, U.S. equities surged into record territory in late June on a combination of easing Middle East tensions, cooling inflation data, and the 90-day tariff pause

💵 Dollar Weakens on Fed and Trade Uncertainty

The U.S. dollar fell to a 3½-year low, pressured by persistent speculations over President Trump replacing Fed Chair Powell and extending rate-cut expectations, as well as progress in U.S.-Canada trade talks

🇨🇦 U.S.–Canada Trade Talks Lift Sentiment

Canada temporarily repealed its digital services tax to facilitate talks seeking a broader trade agreement by July 21, boosting U.S. equity futures

🛢️ Oil Prices Stabilize

After spiking on geopolitical fears, oil traders settled between $65–78/bbl amid supply relief following ceasefire developments and easing Middle East risks

⚠️ July Risks Loom

The coming week will spotlight:

July 4 deadline for Trump’s tax bill

Expiry of the tariff pause on July 9

U.S. Nonfarm Payrolls on July 3

Each poses potential for increased volatility if outcomes disappoint

📊 Key Data Releases & Events 📊

📅 Monday, June 30

9:45 AM ET – Chicago PMI (June): Gauge of Midwestern factory activity

📅 Tuesday, July 1

U.S. markets open, watch trade developments

📅 Wednesday, July 2

Global PMI readings released

📅 Thursday, July 3 (Early close ahead of Independence Day)

8:30 AM ET – Nonfarm Payrolls (June)

8:30 AM ET – Unemployment Rate (June)

8:30 AM ET – Average Hourly Earnings (June)

These labor metrics will be critical for Fed rate outlooking

⚠️ Disclaimer:

This information is for educational and informational purposes only and should not be construed as financial advice. Always consult a licensed financial advisor before making investment decisions.

📌 #trading #stockmarket #economy #jobs #Fed #oil #trade #technicalanalysis

How to Trade When Buy/Sell Alerts Conflict with Market StructureQuestion:

If we have a buy/sell alert and an opposing Market Structure, how can we tell which will prevail or is heavier?

Answer (VX Algo System perspective):

In the VX Algo system, both the alert signals (buy/sell) and the market structure are crucial, but they serve different roles:

Alerts are dynamic triggers based on price action, momentum, or specific algorithmic conditions. They indicate potential entry or exit points.

Market Structure reflects the broader trend and underlying order flow, indicating the prevailing direction of the market (e.g., higher highs and higher lows for bullish structure, or lower highs and lower lows for bearish structure).

When an alert contradicts the prevailing market structure, the heavier factor is usually the Market Structure because it represents the dominant order flow and sentiment. In other words, alerts give you tactical timing, but market structure provides strategic context.

How to tell which prevails:

Confirm with Market Structure: If the market structure is bullish (uptrend), a buy alert aligns with it and is more likely to succeed. A sell alert against that structure is a warning sign that the alert may be weaker or a potential false signal.

Volume and Momentum: Use volume or momentum indicators (built into VX Algo or complementary tools) to see if the alert has strength behind it. A strong sell alert with high volume during an uptrend may indicate an imminent structure shift.

Multiple Timeframe Analysis: Check if the opposing alert is supported or rejected on higher timeframes. A buy alert on a lower timeframe against a bearish higher timeframe structure is less likely to prevail.

Risk Management: If you trade against structure alerts, reduce position size and tighten stops until the structure confirms the shift.

Summary: Market structure is heavier and more reliable for directional bias. Alerts provide tactical entry timing. When they conflict, lean on structure for bias but watch for alert strength as early signals of possible structure changes.

June 27th, 2025 - Morning BriefFriday, June 27, 2025. Markets are on the edge, and if you thought summer would bring calm, think again. Today’s script is pure adrenaline.

Overnight, the U.S. and China finally inked a trade deal that actually matters: tariffs are coming down, and rare earths are flowing again. Tech and manufacturing stocks are already celebrating, with SP:SPX and CME_MINI:NQ1! futures inching toward fresh record highs. NASDAQ:NVDA is still the market’s favorite lottery ticket, hitting another all-time high. Meanwhile, NYSE:NKE just spiked 10% premarket after beating earnings. Never mind the $1 billion tariff punch, they’ll “manage it.” Sure.

But the real show is the May PCE inflation data dropping this morning. The Fed’s favorite gauge is expected to tick up to 2.3% year-over-year, with core PCE at 2.6%. If the numbers surprise, brace for whiplash in rates and risk assets. GDP’s third estimate confirmed a -0.5% contraction in Q1, so the “soft landing” crowd is sweating. Jobless claims and new home sales hit at 10:00 AM ET. Expect every algo on the Street to be watching.

Trump is making noise about firing Powell before 2026, which has traders betting on earlier rate cuts. If you’re looking for stability, you’re in the wrong casino.

Here’s where things stand:

- OANDA:XAUUSD : $3,280–$3,334/oz (slipping as risk appetite returns)

- BLACKBULL:WTI : $65.64–$65.82/barrel (steady, but one headline away from chaos)

- BINANCE:BTCUSDT : $107,215–$107,477 (down, but still a six-figure fever dream)

- CME_MINI:ES1! : Hovering just below the 6,144 record

Today’s takeaway: The market’s running on hope, caffeine, and denial. Stay sharp, one bad print and the rally could turn into a stampede for the exits. Welcome to the volatility vortex.

Been building something for US swing traders — if you’re one, I’d really appreciate your feedback. Free to test, link in Bio

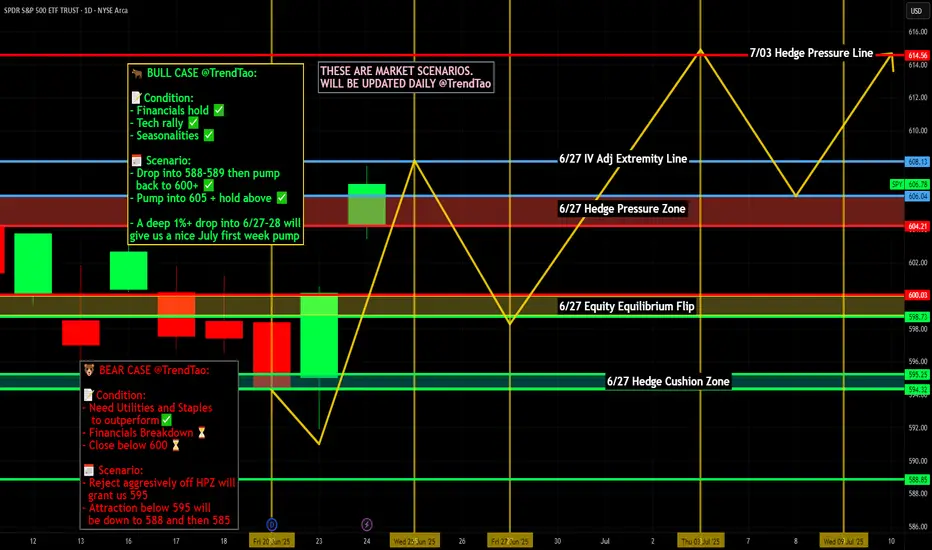

Nightly $SPY / $SPX Scenarios for June 27, 2025🔮 Nightly AMEX:SPY / SP:SPX Scenarios for June 27, 2025 🔮

🌍 Market-Moving News 🌍

📉 Global Markets Bet on Dovish Fed Pivot

Markets are pricing in more aggressive Federal Reserve rate cuts—approximately 125 bps by end-2026—due to speculation that President Trump may replace Chair Powell with a dovish successor. Investors caution excessive political influence could jeopardize Fed independence

🏦 Fed Governor Warns of Tariff Risks

Fed’s Michael Barr emphasized that tariffs could trigger inflation and unemployment, reinforcing the Fed’s wait‑and‑see approach. Expect modest rate cuts later this year, contingent on economic signals

📉 Q1 GDP Revised Sharply Lower

First-quarter U.S. GDP was downgraded to an annualized contraction of 0.5%, a deeper fall than previously reported. The revision underscores drag from weak consumer spending and trade disruptions

📃 Trade Deficit Widens in May

U.S. goods trade deficit expanded 11% to $96.6 billion, driven by a $9.7 billion drop in exports. Trade gap dynamics remain a headwind for growth projections

🐘 JPMorgan Sees Stagflation Risks

JPMorgan revised its U.S. GDP growth forecast down to 1.3%, warning that tariff-related “stagflationary impulse” is complicating growth and inflation outlooks—and making recession risks more real

📊 Key Data Releases 📊

📅 Friday, June 27:

8:30 AM ET – U. of Michigan Consumer Sentiment – June (Prelim.)

Expected to reflect growing economic caution. The index fell in May; traders will watch for further weakness.

10:00 AM ET – Fed Stress Test Results

Fed to release annual bank stress-test outcomes. Strong results support financial stability, while weak spots could unsettle markets

⚠️ Disclaimer:

This information is for educational and informational purposes only and should not be construed as financial advice. Always consult a licensed financial advisor before making investment decisions.

📌 #trading #stockmarket #economy #Fed #inflation #macro #charting #technicalanalysis

What Is The Market Waiting For?Good Morning Trading Fam,

Our stock and crypto markets seem to have stalled. You may be wondering what they are waiting for. Quite simply, the S&P 500 has reached a double-top. That's all. There may be some more pause here for the next week or so. Barring any significant bearish geopolitical or other events, I expect us to move higher. Any FUD at all will send the market back down again. So yes, unfortunately, the next move(s) will be mostly predicated on news. Traders are rather fragile rn. Trade accordingly.

Best,

Stew

Nightly $SPY / $SPX Scenarios for June 26, 2025🔮 Nightly AMEX:SPY / SP:SPX Scenarios for June 26, 2025 🔮

🌍 Market-Moving News 🌍

💱 Dollar Mounts Decline on Fed Credibility Concerns

The U.S. dollar dropped to a 3½-year low against the euro after reports that President Trump is considering replacing Fed Chair Powell as early as September or October. The move fueled market concern about the Fed’s independence and prompted traders to raise the likelihood of a July rate cut to 25%, with nearly 64 bps of rate cuts priced in by year-end

📉 Markets Stay Cautious Ahead of Powell’s Testimony

Traders remain on edge as Fed Chair Powell’s Capitol Hill testimony continues. He reiterated caution, noting inflation risks tied to tariffs despite growing calls for easing, keeping interest-rate expectations in limbo .

📈 S&P 500 Nears All-Time Highs in Second-Biggest Bi‑Monthly Rally

The S&P 500 has notched its second-largest May–June rally on record (6.2% in May, further gains in June), bolstered by cooling inflation, easing Middle East tensions, and strong AI earnings momentum led by Nvidia. Bull-case scenarios could push the index to fresh highs

📊 Key Data Releases 📊

📅 Thursday, June 26:

(No major U.S. economic release—markets are focused on Powell’s remaining testimony and global risk dynamics.)

⚠️ Disclaimer:

This information is for educational and informational purposes only and should not be construed as financial advice. Always consult a licensed financial advisor before making investment decisions.

📌 #trading #stockmarket #economy #Fed #inflation #geopolitics #technicalanalysis

Most see rejection. I see a launchpadWhat looks like a failed breakout is actually SOL setting up for a higher timeframe reversal, right at a refined zone of inefficiency and Smart Money interest. The narrative isn’t over — it’s just beginning.

Technical Breakdown:

Current Price: ~$143.30

Context:

Price tagged the Fair Value Gap (FVG) on the daily and showed reaction — a sign of algorithmic awareness

Volume profile suggests thin liquidity above, ripe for expansion if momentum kicks in

Key Levels:

FVG (1D) zone: just under current price (~140.19)

Order Block (OB): ultimate demand zone near 137.23 — strong structural support

Downtrend Line: recently broken, retest in motion

Major Upside Target: 168.36 — a clean liquidity magnet

Strategic Thesis:

Price dipped into FVG but held above the OB — a classic Smart Money accumulation setup

The dashed projection shows potential higher lows forming, giving fuel for a push through prior highs

FVG + OB form the discount zone, where risk/reward is maximized before the next impulse move

Execution Plan:

Entry zone: $140.00–137.50

→ Expect small shakeouts before confirmation

Invalidation: Daily close below $136 kills the bullish case

Target:

Primary: $168.36

Stretch Goal: $172–176 if momentum is sustained into August

Everyone sees consolidation. I see positioningETH is holding just above a key fib cluster, showing signs of controlled distribution, not weakness. Smart Money doesn’t chase — they build positions while the crowd second-guesses.

The Structure:

Current Price: ~2,419

Local High (Premium): 2,482.09

Fib Retracements:

0.236 → 2,394.72 (mild correction)

0.382 → 2,340.68 (initial re-entry zone)

0.5 → 2,296.99 (ideal discount)

0.618 → 2,253.31 (deep entry, high confluence)

0.786 → 2,191.11 (structure last line)

Key Zones:

FVG already filled during the move up — imbalance mitigated

Order block (OB) at 2,191.11: high-probability reaction zone

Strategy Outlook:

Scenario A (Shallow pullback):

ETH tests 2,394 → 2,340, then continues the push to 2,482

→ Aggressive buyers step in early

Scenario B (Deeper sweep):

A drop to 2,296 → 2,253 opens the door for reaccumulation

→ Classic Smart Money trap before the next rally

Invalidation:

A break below 2,191 (and OB failure) kills this bullish narrative

Execution Logic:

Accumulation Zones:

Light: 2,340–2,296

Strong: 2,253–2,191 (discount reload)

Target:

2,482

Extension optional if momentum builds above recent highs

Premium zone tagged — now we watch how the Smart Money reactsBitcoin just tapped into the 108,151 level — the top of a measured premium range and a likely area where profit-taking begins and fresh distribution footprints form.

This run-up wasn’t random. Price surged from inefficiency, cleanly filled the fair value gap (FVG), and is now flirting with a key liquidity pocket.

Here's what the structure says:

Premium reached: 108,151 (0% fib)

If rejection holds, Smart Money looks to discount entries:

0.236: 106,136

0.382: 104,889

0.5: 103,882

Deep retracement zone: 0.618 at 102,874

Final defense for bulls? The unmitigated FVG block between 101,440 → 99,613

Possible Playbook Scenarios:

Quick retrace → higher high:

Bounce off 104,889 or 103,882 before attacking 108,967+

Deeper sweep:

Into 102,874 (0.618) before Smart Money steps in again

Invalidation:

Break below 99,613 closes this bullish narrative and confirms a structural break

TL;DR Execution Logic:

Wait for retracement into 0.5–0.618 fibs

Look for bullish reaction (engulfing or SFP)

Upside targets:

108,151 (retest)

108,967 (liquidity sweep)

Further upside if momentum sustains

UNEXPECTED RISK CRASH FREE FALL AFTER TREND DATA FOR TH NEXT 48HDepending on our study, BTC has a high chance of a new crash below 100K.

The next 48 hours are important for the trend change of BTC, which can allow the trend to free-fall below 100K

BTC is at a top, and it did recovery always recovered on the M volume top., We are now again on the same trend.

BTC can return below 100K as this update shows, with the possibility of targeting the main target 85K - This is the trend zone for new interest.

The reason for this crash is that BTC has not confirmed the cycle, which means the end of the cycle. There is always possibility that the market can act green, but we expect it can show an unexpected breakdown.

Nightly $SPY / $SPX Scenarios for June 25, 2025🔮 Nightly AMEX:SPY / SP:SPX Scenarios for June 25, 2025 🔮

🌍 Market-Moving News 🌍

💱 Dollar Slides on Middle East Ceasefire Optimism

A fragile ceasefire between Israel and Iran lifted risk sentiment across global markets. The U.S. dollar weakened, while the euro and British pound hovered near multi‑year highs

📈 Equities Near Record Highs

The S&P 500 and Nasdaq pushed toward all-time highs on June 25, supported by the Middle East truce and retreating energy prices. The S&P 500 rallied ~1.1%, with tech and discretionary sectors leading the charge

🛢 Oil & Treasuries Dip, Yield Cuts Anticipated

Oil plunged ~6% to ~$65/bbl as conflict fears eased. Softer prices plus weak consumer confidence spurred expectations of up to 60 bps in Fed rate cuts by December; Treasury yields pulled back accordingly

📉 Consumer Confidence Falls Again

The Conference Board’s index dropped to 93—the lowest level since May 2020—as concerns over tariffs and job availability weighed on households

📊 Key Data Releases 📊

📅 Wednesday, June 25:

(No major U.S. economic data scheduled)

Markets remain focused on geopolitical dynamics, Fed commentary, and next week’s PCE inflation release.

⚠️ Disclaimer:

This information is for educational and informational purposes only and should not be construed as financial advice. Always consult a licensed financial advisor before making investment decisions.

📌 #trading #stockmarket #economy #geopolitics #Fed #inflation #technicalanalysis

Nightly $SPY / $SPX Scenarios for June 24, 2025🔮 Nightly AMEX:SPY / SP:SPX Scenarios for June 24, 2025 🔮

🌍 Market-Moving News 🌍

🇺🇸 Markets Eye Powell Testimony & Consumer Confidence

Today brings a double dose of market-moving data: the June Consumer Confidence Index and Fed Chair Jerome Powell’s testimony before Congress. These will be key indicators of household sentiment and potential shifts in Fed rate guidance

🛢️ Oil Volatility Persists on Middle East Strain

Oil prices briefly spiked after U.S. strikes on Iran’s nuclear facilities, prompting fears of supply disruptions. However, prices have since dipped as ceasefire hopes emerge. Investors remain cautious on energy headwinds

💱 Dollar Retraces on Safe-Haven Rotation

The dollar softened after peaking as geopolitical tensions eased slightly. Still, it remains sensitive to Powell’s tone and confidence data, which could reintroduce volatility

📊 Key Data Releases & Events 📊

📅 Tuesday, June 24:

10:00 AM ET – Conference Board Consumer Confidence (June)

Monitors household optimism; a rebound could support consumer spending and equities.

10:00 AM ET – Fed Chair Powell Testimony Begins

Powell appears before the House Financial Services Committee. Market focus: inflation outlook, tariffs, and potential timing for rate cuts.

⚠️ Disclaimer:

This information is for educational and informational purposes only and should not be construed as financial advice. Always consult a licensed financial advisor before making investment decisions.

📌 #trading #stockmarket #economy #Fed #trade #energy #technicalanalysis

Weekly $SPY / $SPX Scenarios for June 23–27, 2025🔮 Weekly AMEX:SPY / SP:SPX Scenarios for June 23–27, 2025 🔮

🌍 Market-Moving News 🌍

🌐 Geopolitics Add to Risk Aversion

The S&P 500 is up about 0.9% so far in June, but analysts warn it’s facing a “precarious” phase amid renewed Middle East conflict and looming U.S. tariff deadlines in July–August. Elevated oil prices could fuel inflation, while fiscal and debt ceiling pressures weigh on sentiment

🎙️ Powell Heads to Capitol Hill

Fed Chair Powell will testify before Congress this week. His remarks on inflation and rate outlook—particularly regarding the Fed’s recent dot-plot revisions and monetary policy uncertainty—will be central to market direction

📈 Nike, FedEx & Micron Earnings Under Focus

Key corporate earnings (Nike, FedEx, Micron) could provide fresh insight into how tariffs and supply-chain disruptions are impacting major U.S. businesses

🛢️ Oil Prices Elevated

Oil remains range-bound at multi-week highs near $75–80/bbl following U.S.–Israel military action in Iran, which briefly spiked prices ~7–11%. Continued dependence on Middle Eastern supply may keep energy complex volatile

⚖️ NATO Summit Tightens Security Focus

NATO leaders meet in The Hague, marking an elevated global defense posture amid geopolitical uncertainty. Defense and aerospace stocks may remain pressured or volatile depending on summit outcomes

📊 Key Data Releases & Events 📊

📅 Monday, June 23

9:45 AM ET: S&P Global Flash U.S. Services & Manufacturing PMI (June)

10:00 AM ET: Existing Home Sales (May)

📅 Tuesday, June 24

10:00 AM ET: Consumer Confidence Index (June)

Testimony: Fed Chair Jerome Powell appears before Congress

📅 Wednesday, June 25

10:00 AM ET: New Home Sales (May)

📅 Thursday, June 26

8:30 AM ET: Advance Q1 GDP (Final Estimate)

📅 Friday, June 27

8:30 AM ET: Core PCE Price Index (May) — Fed’s preferred inflation gauge

⚠️ Disclaimer:

This is for educational and informational purposes only. It does not constitute financial advice. Always consult a licensed financial advisor before investing.

📌 #trading #stockmarket #economy #geopolitics #Fed #oil #charting #technicalanalysis

BTC / USDT - Look Closely!!!Good evening fellas,

Take a very close look and buy bitcoin.

Trade thirsty, my friends.

Nightly $SPY / $SPX Scenarios for June 20, 2025🔮 Nightly AMEX:SPY / SP:SPX Scenarios for June 20, 2025 🔮

🌍 Market-Moving News 🌍

🏦 Fed Holds Rates, Warns on Tariffs

Fed kept interest rates steady on June 19, cautioning that tariffs could stoke inflation and slow growth. Inflation projections were raised from 2.7% to 3.0%, while growth estimates were revised lower to 1.4%

🌍 Middle East Risk Drags Markets

Global stocks fell and safe-haven assets surged after U.S. futures weakened amid heightened tensions in the Israel–Iran conflict. Yields were mixed: gold weakened and bonds gained, while oil held steady near seven-week highs

📈 Treasury Yields Edge Higher

Despite safe-haven demand, U.S. 10‑year yields ticked up as markets absorbed the Fed’s updated rate outlook. The yield curve remains elevated ahead of next week’s $38 bn auction of long-dated notes

📊 Key Data Releases 📊

📅 Friday, June 20:

(No major U.S. economic reports)

Markets will be driven by Fed commentary follow-ups and geopolitical headlines over the weekend.

⚠️ Disclaimer:

This information is for educational and informational purposes only and should not be construed as financial advice. Always consult a licensed financial advisor before making investment decisions.

📌 #trading #stockmarket #economy #geopolitics #fixedincome #inflation #charting #technicalanalysis

Where Most See Resistance, Smart Money Sees OpportunityDOGE is currently hovering around the 0.382–0.5 Fibonacci retracement zone after a reactive bounce from 0.618 (0.16784) — a critical discount level. Most traders panic at these levels, but experienced participants know this is the zone where price builds intention.

Here's the breakdown of the structure:

Price tapped into the 0.618 Fibonacci level (0.16784) and began showing signs of recovery — a typical Smart Money accumulation zone.

The next target is 0.17042, aligning with the 0.236 retracement level, followed by 0.17151, where previous supply might get mitigated.

Potential retracements are possible, but as long as price holds above 0.16670 (0.786), the bullish structure remains intact.

Execution strategy:

Entry (Accumulation Zone): Between 0.16784 and 0.16864

Invalidation: Break below 0.16600 would weaken the bullish case

Upside targets:

• TP1 → 0.17042

• TP2 → 0.17151

• Extension possibility beyond 0.17204

This move appears to be a classic premium-delivery setup — a structural reset, not a collapse. Smart Money steps in quietly when retail panic takes over. If you're trading DOGE like a pro, focus on levels, not emotions.

Let me know if you'd like this converted into a tweet format or turned into a technical newsletter paragraph.

BTC – 15min Reversal Structure & Fibonacci ReclaimWe’re currently witnessing a potential short-term reversal on BTC’s lower timeframe after a volume-supported breakdown and sweep of local lows.

🔍 Key Observations:

Price swept liquidity at local lows (~103,929.27)

Entered into a clear reaccumulation box with responsive buyers

Volume profile shows prior POC just above – room for fill

Fibonacci retracement aligns with key structure:

0.5 = 104,372.94

0.618 = 104,268.23

1.0 = 104,816.60 (final high target for this impulse)

📈 Potential Play:

Entry Zone: Just above the sweep candle (104,100–104,200)

Target 1: 0.382 at 104,477

Target 2: 104,816.60

Invalidation: Close below 103,926

🧠 Mindset:

This is a classic liquidity sweep → reaction → reclaim pattern. If BTC flips the 0.5 level with strong momentum, a short squeeze toward the 104.8K area becomes likely.

Great opportunity for scalpers or day traders.

Let me know if you want this turned into a long-form breakdown or sent in another format.