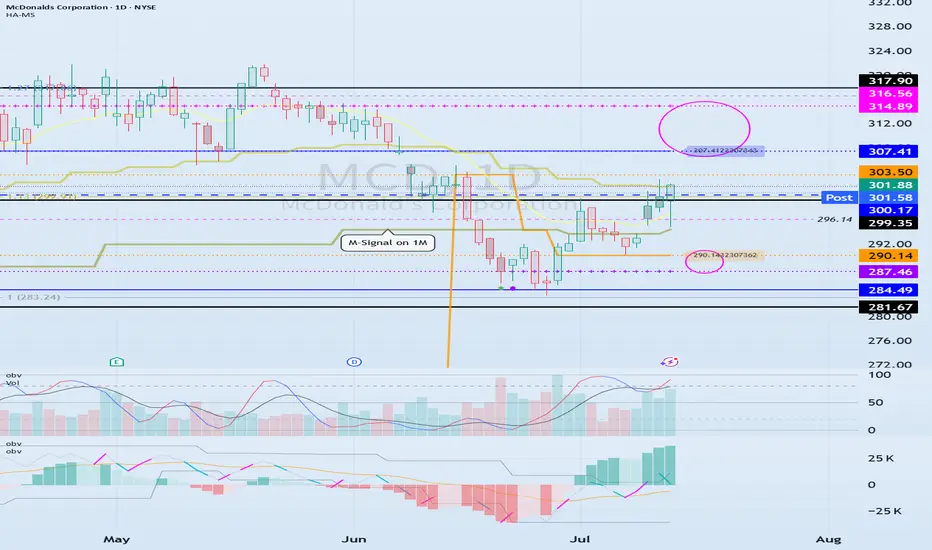

The key is whether it can be supported and rise near 300.17

Hello, traders.

If you "Follow", you can always get new information quickly.

Have a nice day today.

-------------------------------------

(MCD 1D chart)

Before following the basic trading strategy, the first thing to check is whether the current price is above or below the M-Signal indicator on the 1M chart.

If the price is below the M-Signal indicator on the 1M chart, there is a possibility that it will turn into a medium- to long-term downtrend.

Therefore, if possible, it is recommended to trade stocks whose prices are above the M-Signal indicator on the 1M chart.

If the price is below the M-Signal indicator on the 1M chart, you should respond quickly and briefly using the short-term trading (day trading) method.

-

The support and resistance zones can be seen as the 287.46-290.14 zone and the 307.41-314.89 zone.

The 287.46-290.14 zone is the DOM(-60) ~ HA-Low zone, and the 307.41-314.89 zone is the HA-High ~ DOM(60) zone.

These two zones are likely to form a trend depending on how they break through, so they can be seen as support and resistance zones.

-

The 300.17-316.56 zone is the HA-High ~ DOM(60) zone on the 1W chart.

Therefore, we need to check whether it can receive support and rise in the 300.17-316.56 zone.

Therefore, if it falls near the 307.41-314.89 range, you should check for support near 300.17.

-

If it rises above the HA-High ~ DOM(60) range, it is likely to show a step-up trend, and if it falls in the DOM(-60) ~ HA-Low range, it is likely to show a step-down trend.

-

Thank you for reading to the end.

I hope you have a successful transaction.

--------------------------------------------------

Mcdonalds

Is the Golden Arches Losing Its Shine?McDonald's, a global fast-food icon, recently reported its most significant decline in U.S. same-store sales since the peak of the COVID-19 pandemic. The company experienced a 3.6 percent drop in the quarter ending in March, a downturn largely attributed to the economic uncertainty and diminished consumer confidence stemming from President Donald Trump's tariff policies. This performance indicates that the unpredictable nature of the trade war is prompting consumers to curb discretionary spending, directly impacting even seemingly resilient sectors like fast food through reduced customer visits.

The link between sinking consumer sentiment and tangible sales figures is evident, as economic analysts note the conversion of "soft data" (sentiment) into "hard data" (sales). While some commentators suggest that McDonald's price increases have contributed to the sales slump, the timing of the decline aligns closely with a period of heightened tariff-related anxiety and a contraction in the U.S. economy during the first quarter. This suggests that while pricing is a factor, the broader macroeconomic environment shaped by trade tensions plays a critical role.

In response, McDonald's emphasizes value offerings to attract and retain customers navigating a challenging economic landscape. The company's struggles mirror those of other businesses in the hospitality sector, which also report reduced consumer spending on dining out. The situation at McDonald's serves as a clear illustration of how complex trade policies and the resulting economic uncertainty can have far-reaching consequences, affecting diverse industries and altering consumer behavior on a fundamental level.

Comprehensive Research - McDonald’s Stock Set to SoarQuick read:

McDonald's stock is poised for a bullish move, with Wave 3 likely starting and strong support near 290.50–295.00. Traders should long on dips within this range, for next resistance levels, 326.00 and 348.00 with a invalidation below 276.00. This setup offers a solid risk-to-reward in a long-term uptrend. Alternative safe entry is possible after the break of corrective channel breakout of wave (2).

Elliott Wave Forecast:

TF - Daily

The chart suggests that McDonald’s stock is in the middle of a larger upward move known as Wave C, which comes after completing a complex correction. Wave C is expected to unfold in five smaller waves, a pattern that usually points to a strong uptrend. It appears the correction is behind us, and a fresh bullish phase is underway.

Starting from the low at 276.53 , marked as Wave B, the price climbed to 326.32 , forming Wave one. After that, the stock pulled back to 290.50 , forming Wave two. This pullback followed a typical ABC pattern within a corrective channel, which often signals the end of a downturn and the beginning of an upward move.

Now, Wave three seems to be starting, and this is usually the strongest part of Wave C. The price is expected to move above 335 , take a small pause for Wave four, and then rise again to complete Wave five somewhere around 345 to 350 dollars. This positive outlook remains intact as long as the price stays above 290.50 . With the breakout from the corrective channel, the setup looks strong and clear for buyers.

Fibonacci levels:

Fibonacci Extension Targets:

1.000 extension: 326

1.618 extension: 348

Correction Retracement Levels:

Wave 2 retracement: 78.6%

A = C in A-B-C correction: 289.21

Price Action & shifting of value:

TF: Weekly

McDonald’s stock has been steadily climbing inside a rising channel since late 2020, showing a clear long term uptrend. The price has respected both the top and bottom edges of this channel very well, and interestingly, the middle line has acted like a pivot, providing support or resistance multiple times over the years.

Recently, the stock made a higher low at 276.53 and bounced back strongly, keeping the bullish structure intact. It then pulled back to 290.50 , right around the middle line of the channel, and held above an upward sloping trendline. This kind of price action shows strength and suggests buyers are stepping in.

The sharp move from 276.53 up to current levels looks like a strong bullish leg, possibly driven by accumulation. If the stock can break above its recent high of 326.32 , it could head toward the upper end of the channel. As long as the price stays above 290.50 and especially above 276.53 dollars, the bulls remain in control. Even if the price dips a bit, the long term trend stays positive unless the lower boundary of the channel breaks down.

I will update more Information here.

Lamb Weston Holdings | LW | Long at $51.32Lamb Weston Holdings NYSE:LW , the potato / French fry king, has gone through a tremendous downturn since 2023. Yet, earnings are forecast to grow 22% per year into 2027. Debt is quite high at 2.5x and this company, like many others, will significantly benefit from lower interest rates in the future. If the US experiences another way of inflation, Lamb Weston Holdings could be on the beneficiary side of things.

From a technical analysis perspective, the price has entered my "crash" simple moving average zone. Typically, this area signals a bottom, but it's not guaranteed. I foresee the daily price gap near $50 being closed in the short-term before a true move up. A dip to $47-$48 is not out of the question. Regardless of trying to predict bottoms, at $51.32, NYSE:LW is in a personal buy zone.

Targets:

$62.00

$68.00

$77.00

The global market is rebootingOn February 18, negotiations between the United States and Russia are scheduled to take place in Saudi Arabia. These talks could pave the way for restoring economic relations and addressing global challenges.

“American companies lost over $300 billion by exiting the Russian market,” said Kirill Dmitriev, head of RFPI, on the eve of talks with the U.S. delegation in Saudi Arabia. He emphasized the importance of economic dialogue, noting that the Russian market remains attractive to investors.

It is now known that several major American companies intend to return to Russia. Amid a potential thaw in U.S.-Russia relations, Visa (#Visa), Mastercard (#MasterCard), Apple (#Apple), PepsiCo (#PepsiCo) and McDonald's (#McDonald) have all announced their intentions in recent days.

The U.S. stock market remains resilient thanks to domestic growth drivers. Additionally, several key factors are expected to drive growth in the near future:

Federal reserve monetary policy: A possible rate cut or maintaining low interest rates is spurring investments. This, in turn, boosts company valuations and pushes up indices such as the Dow Jones (#DJI30) and S&P 500 (#SP500).

Technology sector: Ongoing advancements in AI, cloud services, and biotechnology are attracting capital. Moreover, integrating artificial intelligence into large businesses helps reduce costs by automating routine processes, while AI algorithms enhance strategic planning and risk management.

Corporate earnings growth: Increasing corporate profits are one of the key factors supporting the positive momentum in the stock market, including the S&P 500 (#SP500), which reflects the performance of the 500 largest U.S. companies. Strong quarterly reports from these companies play a crucial role in reinforcing investor confidence and ensuring market stability.

Geopolitical expectations: Tensions among major global players like the U.S., EU, and Russia could lead to sanctions, trade wars, and economic restrictions, which negatively impact the global economy and stock markets. A thaw in relations could reduce the likelihood of such conflicts and, consequently, lower the risks associated with sanctions and instability.

FreshForex analysts are confident that as geopolitical tensions ease, companies will start to return, which will undoubtedly drive up their stock prices. Don’t miss this chance – invest in stocks with us!

Our terminal offers 270 trading instruments, including CFDs on corporate stocks and indices. Trade with a favorable leverage of 1:1000 and enjoy attractive bonuses!

McDonald's Stock Crosses $300McDonald's stock has surged over 4.5% , reinforcing its bullish momentum, which had been paused after a prolonged neutral phase. Today’s earnings report has been a key driver, as the company posted earnings per share of $2.83 , in line with forecasts, along with a questionable sales figure of $6.39 billion , slightly below the $6.44 billion expected.

However, what has fueled the temporary bullish momentum is the board of directors’ decision to eliminate certain discounts that had been in place during previous quarters. These promotions are no longer considered essential for boosting sales growth, as they may have negatively impacted the company’s revenue figures. Now, the market sees this shift as a potential catalyst for sustained sales growth, which could in turn support long-term stock price appreciation.

Breaking the Sideways Trend

Until a few sessions ago, McDonald's stock had been trading within a tight range, fluctuating between $300 resistance and $286 support. However, the rising bullish momentum has pushed this sideways phase into the background. Now, analysts are evaluating whether this new upward gap could mark the beginning of a stronger trend movement. This scenario could materialize if the stock manages to reach its previous highs at $317.

Technical Indicators

RSI: The RSI line has spiked rapidly and is now reaching overbought levels, as indicated by the 70-mark threshold. If the stock remains above this level, it could signal a potential downward correction in the coming trading sessions.

MACD: The histogram has started to diverge from the neutral 0 level , indicating that the latest moving average trends continue to support the bullish movement. As long as this bias remains in the MACD, buying pressure could become even more significant.

Key Levels to Watch

$317 – Current key resistance, aligning with the October 2024 high. Consistent movements above this level could signal the beginning of a new and fresh uptrend in the stock.

$300 – New support level, corresponding to the top of the previous lateral channel. If the price dips back below this level, it could increase neutral bias and lead to extended sideways movement. This also serves as a potential retracement area in the short term.

$293 – Support zone, marked by the 50- and 100-period moving averages. If the price falls below this level, it would signal an end to the current bullish momentum, potentially confirming the start of a larger downtrend.

By Julian Pineda, CFA – Market Analyst

MCD_1W_BuyMcDonald's stock analysis McDonald's shares are in an ascending channel and can continue to rise by maintaining the price inside the channel. First support 283 Second support in case of vision 266 We are buying shares for investment towards the target numbers 366 and 383 Share growth percentage 40%

Apple DOWN! Not Fruits or healthy food in MC DONALDS.We can see the selling volume some days ago, that was an important one, ¿WB?

Apple is retesting as the whole S&P seems to chop chop this quarter, remember that was going up when Crypto was Chopping.

Opened the short yesterday, with a tight SL just in case-

Let´s see.

Para pa pa pa Loving IT

McDonald’s (MCD): Crisis Management and Market ReactionWhat a perfect flat this is on McDonald’s. Already back in the range and finished the wave ((ii)) at the 50% Fibonacci retracement level. Far more downside is expected for $MCD. If we are right about this intra wave count, we should see the level of wave ((iii)) to be at a minimum of $258.5.

The outbreak that caused the big drop was linked to slivered onions used in Quarter Pounder burgers, which affected 104 individuals across 14 states and resulted in one death. To address the crisis, McDonald’s will invest $35 million in marketing and advertising campaigns to rebuild customer trust and foot traffic. Additionally, $65 million will be directed toward franchisee support, including deferrals on rent and royalties.

To recover from this significant image damage, it will likely take much time for NYSE:MCD to resolve these challenges. Therefore, it would also be valid if NYSE:MCD sweeps the range low at the level of $245 before coming back to at least the range middle.

KO Coca-Cola and the E. coli outbreak linked to McDonald’sIf you haven`t bought the dip on KO:

Now you need to know that Coca-Cola (KO) could see a decline due to the E. coli outbreak linked to McDonald’s, as the two brands have a longstanding partnership, with Coca-Cola products being served widely in McDonald's restaurants.

Negative publicity impacting McDonald's could indirectly affect Coca-Cola by reducing in-store traffic, which may lower beverage sales.

Additionally, Coca-Cola's association with fast food means that consumer sentiment shifting towards healthier options could further impact sales.

If the outbreak spurs changes in public dining behavior, Coca-Cola may face a temporary decline in demand across other food service venues, potentially impacting its stock performance.

Q3 MCD TRADEWaiting for the open, ideally below yesterday's close to allow for a bullish gap fill. With the solid Q3 report, I’ll aim to hold the position throughout the entire day.

Update during the trade. First tp 298

Order Blocks 303Hint: McDonald's earnings report on Tuesday

From a technical perspective, McDonald's has broken the neckline, leading to short-covering and a rebound. It may either shift from an uptrend to a downtrend or enter a consolidation phase. The 303 level presents a good shorting opportunity.

MCD McDonald's Corporation Options Ahead of EarningsIf you haven`t bought MCD before the previous earnings:

Now analyzing the options chain and the chart patterns of MCD McDonald's Corporation prior to the earnings report this week,

I would consider purchasing the 290usd strike price Puts with

an expiration date of 2024-11-15,

for a premium of approximately $5.85.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

QUICK STARBUCKS WATCH THIS ONE REAL ESTATE PROBABLY Why are all the ema's in alignment for a bullish push, when long term rsi suggests down, and how much upside is there really, vs downside.

When it looks like a cookie jar, maybe even with honey.

Sugar?

coffee.

It's always one you forget about, but oh well.

Idk, what I'm saying, but also I'm sure it's because mcdonalds saw a big attack against it, and nobody even talks about starbucks.

McDonald's CorporationHello,

Daily chart.

With a Fibonacci retracement, we arrive at the 0.382 zone.

The price is still above the 200-period simple moving average.

The chart shows the volume accumulation zones with the ranking.

A file to watch for me, but don't panic for now.

Make your opinion, before placing an order.

► Thank you for boosting, commenting, subscribing!

McDonald's (MCD): New setback after quarter pounder incidentOne month ago, we predicted McDonald’s would push into the 127.2%-138% range at max, and now the stock is reacting precisely as we expected. Pre-market trading shows a 6% drop following the news from Tuesday.

The Centers for Disease Control and Prevention (CDC) has reported one fatality and ten hospitalizations linked to McDonald's Quarter Pounder burgers, resulting in the fast-food chain pulling the item from several menus. This incident has brought McDonald's stock back into its previous range, signaling that this wave (B) should mark the local top for now.

If we are correct, we expect to see a 5-wave structure downward from here. While there could be a brief relief pump, we anticipate the stock falling below the wave (A) level of $243. We are patiently monitoring the situation, and if a favorable short setup presents itself, we will share the entry details. For now, we are watching how the news unfolds and waiting on the sidelines.

Can a Single Onion Slice Reshape the Future of Fast Food?In a dramatic turn of events that has sent ripples through the quick-service restaurant industry, McDonald's Corporation faces a watershed moment that transcends mere food safety concerns. The recent E. coli outbreak linked to Quarter Pounder burgers, resulting in 49 reported cases across 10 states, serves as a powerful reminder of how seemingly minor supply chain decisions can cascade into significant corporate challenges. With shares plummeting 7% in after-hours trading, this crisis presents a compelling case study in crisis management, operational resilience, and the delicate balance between efficiency and safety in modern food service operations.

The revelation that slivered onions from a single supplier could potentially trigger such widespread impact challenges conventional wisdom about supply chain diversification in the fast-food industry. McDonald's swift response - removing Quarter Pounders from menus across several Western states and implementing immediate supply chain modifications - demonstrates the complex interplay between brand protection and operational agility. This situation raises profound questions about the industry's approach to supplier relationships and the potential vulnerabilities created by centralized sourcing strategies in pursuit of consistency and cost efficiency.

Beyond the immediate health concerns and financial implications, this crisis illuminates a broader narrative about consumer trust and corporate responsibility in the modern food service landscape. As McDonald's navigates this challenge, their response may well set new standards for crisis management and transparency in the industry. The incident serves as a catalyst for reimagining food safety protocols and supply chain resilience, potentially ushering in a new era where consumer safety and operational efficiency are not just balanced but fundamentally integrated into the fabric of fast-food operations.

McDonald's (MCD): Time for a Correction!We predicted it back in March, and sometimes you have to give yourself a pat on the shoulder when things play out exactly as expected. A little over six months ago, we said that Wave (A) would likely hit $245.88, and what did we get? $244, which is less than a 1% difference from our target. After that, the stock surged by 24% to what now seems like another high.

Now we find ourselves back at the range high, and we must treat it with caution. Since March, we've been hoping for this exact scenario to unfold, but we're not ready to jump into a short position on NYSE:MCD just yet! The rise has been pretty strong, and we're seeing the RSI hovering around the overbought area. Given this price level, we could either see a smaller pullback before heading higher—possibly up to the 127.2%-138% Fibonacci extension—or NYSE:MCD could fall lower after losing the mid-range level.

In both scenarios, we would like to see lower prices as we still haven't concluded Wave II. We’ve zoomed in on the chart now, but whether we’re right or wrong, we’ll zoom back out to reevaluate when the time is right.

This serves as the perfect reminder that good things take time 🚀.

McDonald's Earnings Miss For the First Time Since 2020McDonald's second-quarter earnings report fell short of analysts' expectations as higher prices contributed to a decline in foot traffic and comparable store sales. Despite efforts to boost sales with promotions like the "$5 Meal Deal," the fast food giant faced challenges in maintaining revenue and profitability.

Key Takeaways:

- Revenue and Profits: McDonald's reported $6.49 billion in total revenue for Q2, nearly identical to the same period in 2023, but fell short of the $6.63 billion projected by analysts. Net income dropped 12% year-over-year to $2.02 billion, missing expectations of $2.24 billion.

- Comparable Sales Decline: Global comparable sales fell 1% from last year, with U.S. locations experiencing a drop in foot traffic due to higher prices. Sales decreases in France and China offset improvements in Japan and Latin America.

- Impact of Promotions: The recent "$5 Meal Deal" promotion provided a late-quarter boost, though its full impact will be more evident in the third quarter.

Detailed Analysis:

Revenue and Profit Performance

In the second quarter of 2024, McDonald's revenue remained flat at $6.49 billion compared to the same period in 2023. Analysts had anticipated a growth in revenue to $6.63 billion, but the reality fell short. This stagnation in revenue was accompanied by a notable decline in net income, which dropped 12% year-over-year to $2.02 billion, compared to analysts' expectations of $2.24 billion.

Comparable Sales and Foot Traffic

The global comparable sales decline of 1% highlighted the challenges McDonald's faced in maintaining customer engagement amid rising prices. In the U.S., higher menu prices led to reduced foot traffic, contributing to a 0.7% decline in same-store sales. Internationally, sales fell by 1.1%, driven by weaknesses in markets like France and China, which overshadowed gains in Japan and Latin America.

Promotional Efforts and Market Response

In response to the declining sales, McDonald's launched the "$5 Meal Deal" promotion in an effort to attract price-sensitive customers. While this promotion only impacted the final days of the second quarter, it is expected to have a more significant effect on third-quarter earnings. Early reports suggest that the promotion has been successful, potentially continuing into August to sustain momentum.

McDonald's CEO Chris Kempczinski emphasized the company's commitment to delivering "reliable, everyday value" and accelerating growth drivers such as chicken and loyalty programs. Despite these efforts, the broader economic environment and consumer price sensitivity have posed substantial challenges.

Market Reaction

Shares of McDonald's have experienced a 15% decline in value so far this year. However, the stock showed a slight recovery, up 3.77% in Monday's trading session following the earnings announcement. This reflects a cautious optimism among investors that the company's strategic initiatives may eventually pay off. The stock has a Relative Strength Index (RSI) of 57.83, indicating potential for further growth. Adding to the potential growth is the bullish flag pattern depicted on the chart.

Conclusion

McDonald's second-quarter performance underscores the difficulties faced by the fast food industry amid rising prices and shifting consumer behaviors. While the "$5 Meal Deal" and other strategic initiatives show promise, the company must navigate a complex landscape to regain growth and profitability.

MCD time for CALLS again we now have a nice daily RSI positive non confirmation I will now buy 260 calls looking for a rally of 11 to 15 $

MCDONALDS WILL GO FURTHER DOWNSIDE WITH THIS PATTERNMCD has formed a bearish flag pattern, suggesting a potential decline towards the daily support level. It's prudent to await confirmation of a bearish breakout from the flag pattern before considering any further action.