Microsoft Technologies CorporationIt's important to note that Elliott Wave Theory can be subjective, and interpretations can vary among analysts. It's also worth mentioning that Elliott Wave analysis should be used in conjunction with other technical analysis tools and factors such as fundamental analysis and market conditions to make well-informed investment decisions.

Regards

Microsoft

[Microsoft] bearish then bullishBullish divergence in progress, wait for the next golden cross to buy.

Microsoft - Fundamental Analysis: Everything you need to know.Microsoft's Stock Rises on the Back of AI Expansion, Gaming Dominance, and Positive Analyst Outlook

Over the past few months, Microsoft's stock has experienced a remarkable surge of almost 30%, driven by the company's ambitious venture into the field of artificial intelligence (AI). This cutting-edge technology has the potential to revolutionize numerous industries in the years ahead, and Wall Street has taken notice, leading to a bullish outlook on Microsoft's stock. While Microsoft already boasts established brands like Office, Windows, Azure, and Xbox, the growing influence of AI has further enhanced its potential, making it an opportune time to explore the opportunities presented by this tech giant. Here are three crucial factors that knowledgeable investors should consider.

AI Potential:

In 2019, Microsoft made a strategic investment of $1 billion in OpenAI, a move that has proven to be a significant win for the company. OpenAI's advanced chatbot, ChatGPT, has triggered an AI race among tech giants and prompted Microsoft to invest an additional $10 billion in the company. This partnership has positioned Microsoft as a frontrunner in the market, allowing the integration of OpenAI's technology into its own services such as Office, Azure, and Bing. As a result, Microsoft has solidified its position as the leading provider of AI services for both consumers and businesses.

Furthermore, Microsoft's cloud computing platform, Azure, has the potential to become a market leader with the help of AI. Richard Bernstein, an investment manager, predicts that Microsoft's cloud revenue could more than double as the company expands its AI offerings. As of the first quarter of 2023, Azure currently holds the second-largest market share in the cloud industry at 23%, with Amazon Web Services leading at 32%. However, Microsoft's leadership in artificial intelligence gives it the potential to surpass its competitors in the coming years.

Growing Dominance in Gaming:

In addition to making strides in AI and cloud computing, Microsoft has made significant progress in the gaming industry. The Xbox brand has propelled the company to become the fourth-largest games company globally, trailing only Tencent, Sony, and Apple. However, Microsoft is actively taking steps to increase its market share in this sector.

One of Microsoft's notable achievements in gaming is the introduction of the Xbox Game Pass, a game subscription service that has transformed how millions of gamers consume games since its launch in 2017. By offering users access to an extensive collection of games for a low monthly fee, Game Pass eliminates the need to purchase games individually. Moreover, Microsoft adds its own game titles to the platform on their launch day, which is a significant selling point. With the acquisition of more game studios, Game Pass has become increasingly attractive to gamers, offering hit titles and value-added features that make the Xbox console more appealing than competitors like Sony's PlayStation 5.

Despite facing macroeconomic challenges, Microsoft's games business has continued to grow, thanks to the success of Xbox Game Pass. In the third quarter of 2023 (ending March 2023), revenue from the service increased by 3% year-on-year, and the number of Game Pass members grew by an impressive 150% from 2020 to 2022.

Analysts' Optimism:

Investors have been drawn to Microsoft this year due to the company's expansion into AI, resulting in the stock price rising nearly 30% since the beginning of 2023. Microsoft's strong brands, such as Office, Windows, Azure, and Xbox, have already made it an appealing investment. However, the company's foray into AI has further boosted its outlook. Savvy investors recognize that Microsoft possesses significant potential in AI and is leveraging its partnership with OpenAI to integrate the startup's technology across various services, including Office, Azure, and Bing. Additionally, Microsoft has made notable progress in gaming, with the rapid growth of its subscription service, Xbox Game Pass, which adds value to the Xbox console.

Analysts have expressed optimism about Microsoft's prospects, giving the company a buy/strong buy rating. They recognize the significant potential of Microsoft's expanding role in AI, the cloud market, and gaming. The average 12-month price target reflects a projected 7% growth in the stock. With its strong foothold in established industries and its investments in emerging technologies, Microsoft is seen as a long-term buy with substantial growth potential.

In summary, Microsoft's stock has experienced a substantial rise driven by its expanding ventures into AI, its dominance in the gaming industry through Xbox Game Pass, and the positive outlook from analysts. The company's strategic partnership with OpenAI and its integration of AI technology into various services position it as a leading provider in the AI market. Furthermore, Microsoft's cloud computing platform, Azure, has the potential to become a market leader. As Microsoft continues to innovate and expand its offerings, investors recognize the long-term growth opportunities it presents.

Microsoft Stock To Keep In Portfolio!Hello ladies and gentlemen, according to my graphical analysis of Microsoft , I recommend for the moment to keep Microsoft Stock in your portfolio because there is a great probability of reaching 315$ in the next few weeks .

MSFT Swing Short updateWe have hit our entry perfectly and have started to move down. Since we have already moved 2% Its good enough for moving stop loss slightly lower, but I would keep it above the recent high atleast couple of point higher.

Once we breach the while horizontal line and stay under it for a day or two I will move the Stop loss to breakeven after taking small tp and let the rest ride.

If you like my content then please boost and share this post. I have over 6 years of trading and investing experience and have learned a lot in this time. I like to share what I have learned. If you would like to learn from my experience then follow me on trading view to get notified on my trade, market projections and several upcoming technical analysis and in-depth tutorials on technical Indicators. You can also leave a comment and let me know if you want me to look at any specific asset or want to learn about any specific topic in the world of Technical Analysis. I Will do my best to create a post for it.

Keep learning and Happy trading All.

MSFT Swing ShortWe have several bear divs on RSI. The whole move up from 274 to current high will be reversed as it happened on Decelerating volume. We have also tapped the PRZ of butterfly after filling the Gap at 312.

The PRZ of the butterfly has a large zone of reversal, that's why SL is slightly large for this move. Based on your risk appetite, you can either wait for a better entry or size your positions as per the SL , but we are at proper place to look for selling/Shorting opportunities here.

If you like my content then please boost and share this post. I have over 6 years of trading and investing experience and have learned a lot in this time. I like to share what I have learned. If you would like to learn from my experience then follow me on trading view to get notified on my trade, market projections and several upcoming technical analysis and in-depth tutorials on technical Indicators. You can also leave a comment and let me know if you want me to look at any specific asset or want to learn about any specific topic in the world of Technical Analysis. I Will do my best to create a post for it.

Keep learning and Happy trading All.

Apple AAPL - Brace Yourselves for $200. Seriously.Apple is something of a reverse canary in the coalmine when it comes to the Nasdaq, specifically because it's its highest weighted company at almost 14%. All these weeks everyone has been bearish, but yet, Apple is not in anything resembling a bear market.

Instead, everything about Apple from the monthly chart to the daily chart indicates that the January all time high of $182.93 is not very likely at all to be the all time high.

And this is under the circumstance wherein Apple extensively relies on what is effectively slave labor supplied by the notorious Chinese Communist Party, a problem really exacerbated by the regime employing that Zero-COVID stuff.

This is important because the situation with Apple's Foxconn factories and other Chinese factories and the new restrictions on chip makers means there is fundamental problems with this company going forward.

There's fundamental problems and yet it's set up to rally to a new all time high. Apple is more or less in "The Big Short."

Look up "China Quarantine Camps" or "COVID QR Code" on social media. The Chinese are literally being placed by the millions into huge concentration camps and every aspect of their daily life, from their ability to use public transit, their ability to go to work, their ability to purchase goods, their ability to use money, is entirely under the CCP's social credit system, lynch pinned around the colour of their QR code health pass.

And to think this is a system that the Western globalist establishment would like to install for all of us all over the world via central bank digital currencies... all I can say to readers is I hope you are intelligent enough to reject the Communist Party's things and its Marxist-Leninist "Theory of Evolution" and atheism stuff. If you want those things, you'll have to go with those things and experience what those things truly entail.

Personally, I'm calling a bear market rally, with Nasdaq going to 14,000. I suppose it'll be rather humiliating for me if this turns out to be incorrect and we keep dumping. However, fortune favours the bold, and at the same time, this is how bear markets work and there's a logic to the way they operate.

Nasdaq NQ - Unpopular Opinion #2,118: 14,000 is Coming

I also believe that stocks like Amazon and Meta are due for a fat rally

AMZN Amazon - Realistic Expectations In Both Doom and Gloom

Facebook/Meta - Too Much Bear, Not Enough Bull

Before you discount my supposition as hogwash, consider that McDonald's and Lockheed Martin just made all time highs just last month. And this is supposed to be a bear market where everything is going down.

So what's the rationale for saying Apple is going to set a new all time high?

Let's examine the monthly:

1. Apple set the low of the year in June, like everything else, but when it came time for September and October's scary index dumps, Apple remained very strong. October was actually a winning month overall.

2. Although this appears to have sharply reversed in November, it's worth noting we're a total of 4 trading days into the month. The November high as printed is not likely to remain the high.

3. In terms of range equilibrium for this market cycle, which I measure from anything's Coronavirus Disease 2019 pseudo-pandemic hysteria low to its all time high, Apple has not wanted to trade back to equilibrium. This all on its own tells me that the MMs are still heavy on the sell.

Looking at a weekly chart:

Inside the 2022 trading range we can see that Apple is currently trading at a deep discount. The magnification of the fractal shows us that not only is the prior statement true, but that the area below the October of 2021 pivot that led to the ATH has been worked extensively for the last several months.

On the daily, we can see with more clarity that the post-earnings pump was actually a major trade away from this genuine demand zone and back towards range equilibrium. It has since retraced, which is bullish.

If you understand how sell models work, you'll understand why this is "bullish" and not "bearish," and you'll understand why Apple continues to trade like it does and why it doesn't want to make a new low despite how excited everyone always is about the prospect of it crashing so they can buy cheap.

(Hint: When Apple is under $115, don't touch it. It's going to wind up like Facebook.)

But if you understand how sell models work, you'll also know why a new all time high on Apple is bearish, and not bullish.

What I would like to say to everyone is that bear markets rally and rally hard. They do this for a reason and the fundamental reason is that they're not bullish.

It sounds contradictory, right? "Why would something rally so hard if it's not bullish? How can that be?"

You are confused because when you see price go up, you think buying and when you see price go down, you think selling. Yet, if the banks and the funds traded like that, they would blow their account like you do and we would have ourselves a Lehman Brothers moment every 3 to 6 months and society would collapse.

When you see huge rallies like what's ahead you need to govern yourself strictly, and this means:

1. Don't get delusional and think you're in a new paradigm of everything going uppy. No, SPX is not going to 6,000 before Jan. 1 like David J. Hunter has been calling.

2. Check your greed before your greed checks your hide

3. Don't short or buy puts too early. Instead, buy them too late. A bullish Apple is as scary as a bullish Bitcoin.

4. The more complaining you see on social media and your signal groups about the Federal Reserve and "this ponzi," the higher things are going to go. The top is in when the charlatans and grifters start talking about getting long.

5. Buy the dip, but keep your risk low.

6. Make sure you take profits because this is no time to buy and hold.

Because what lies ahead after you see this go on for a bit and VIX hit numbers like 17 and 18, is this, which I called in August,

VIX - 9x8 = 72

The limit down that lies ahead is going to be vicious. Afterwards, North Americans will finally know what a real bear market feels like. It's not fun.

APPL - Daily chartWhen it reaches 166, there will be a

MACD cross over, which can be used for confirmation.

Note: This is for educational purpose.

MSFT - Bearish Harmonics - Short OpportunityMSFT displays multiple bearish harmonics; Some are painted on the Chart.

Downside targets are listed within Chart.

Enjoy!

Microsoft is not ready for more upside Microsoft is not ready for more upside Now , it should be down for make last wave of triangle

Under FWB:250 is buy opportunity for all new high

Amazon - go longSince there is a good closing above the bollinger band in the weekly and daily as well and the above supply area is tested already.

There is a good change for the break out.

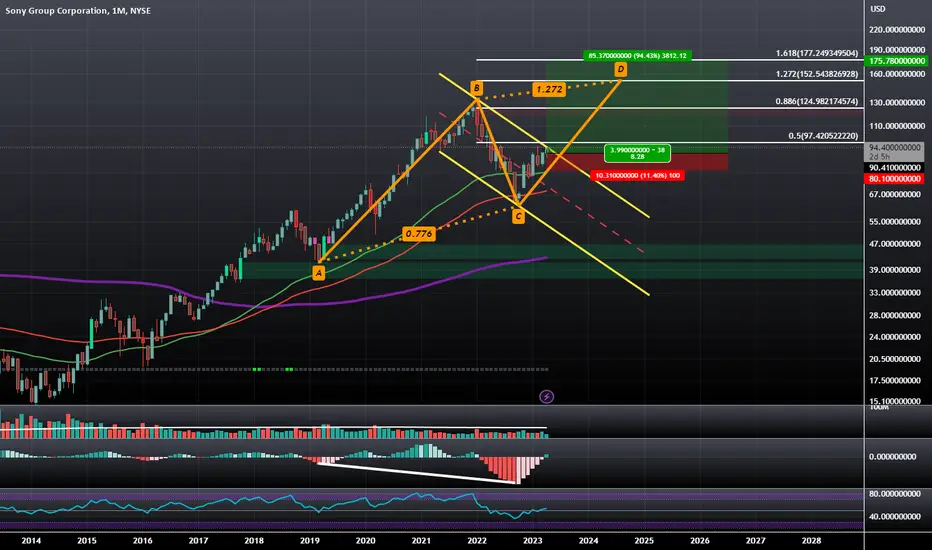

$SONY: Monthly Hidden Bullish Divergence and Channel Breakout NYSE:SONY on the Monthly Timeframe is breaking out of a Descending Channel while confirming Hidden Bullish Divergence and Bullishly Crossing over on the MACD and the RSI enters the Bullish Control Zone; the next obvious target would be between 150 and 177 Dollars as that would be the completion of an AB=CD Harmonic Pattern. One last thing to note on the side is that the NASDAQ:MSFT acquisition of NASDAQ:ATVI has recently hit a brick wall with regulators and this is likely to spur some optimism in the NYSE:SONY camp who has opposed this acquisition in fears that Microsoft would eventually make games like Call of Duty, Xbox Exclusive.

Microsoft H4 As 280 Supports Target 308 NextIn this update we review the recent price action in #Microsoft and identify the next high probability trading opportunity and price objectives to target

MICROSOFT Cup and Handle targeting $320.Microsoft (MSFT) has been trading within a Channel Up pattern since the November 04 Bottom. Supported by an Inner Higher Lows trend-line, we can even see a Rising Wedge forming. Now however, it will face the most important Resistance of this uptrend, the 294.50 of the August 15 High (just below the 0.618 Fibonacci).

If rejected, we may see a Cup and Handle (C&H) pattern materializing, which can pull the price back down to the 1D MA50 (blue trend-line), even the 1D MA200 (orange trend-line). We remain bullish on MSFT but based on our long-term strategy for stocks, we will welcome such pull-back and buy it. Our next target is on the 0.786 Fibonacci at $320.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Is it Worth Buying MSFT Today ?Microsoft Corporation, the American multinational technology company, has been one of the most prominent companies in the tech industry. Founded in 1975, the company’s market capitalization was $2.15 trillion, as of April 18, 2023. The company has had a strong revenue growth, reaching $198.27 billion in 2022, with projections of $262.57 billion in 2025. This growth has been fueled by several products, including Windows, Office Suite, Xbox, and LinkedIn, among others.

The company’s financial statements show strong performance, particularly in revenue, with an impressive compound annual growth rate of 13.3% between 2017 and 2022. The company has also maintained a good profitability level, with an average EBIT margin of 41.4% between 2017 and 2022. However, the company’s net income margin has been fluctuating between 2017 and 2022, reaching its highest at 36.5% in 2021 and its lowest at 31.0% in 2018.

The company's valuation ratios have been at reasonable levels over the years. The price-to-earnings (P/E) ratio has ranged from 26.6x in 2022 to 35.3x in 2020. The P/E ratio is expected to reach 23.0x in 2025. The price-to-book (P/B) ratio has ranged from 11.5x in 2022 to 14.3x in 2021, and it is expected to reach 6.54x in 2025.

Microsoft Corporation's enterprise value (EV) to revenue ratio has also remained reasonable, ranging from 9.4x in 2022 to 11.7x in 2021, while its EV to EBITDA ratio ranged from 19.1x in 2022 to 24.1x in 2021. The company's enterprise value over free cash flow (EV/FCF) ratio was at 28.6x in 2022, and it is expected to reach 22.6x in 2025.

The company has a strong balance sheet, with net cash position ranging from $54.98 billion in 2022 to $135.17 billion in 2025. The company's free cash flow (FCF) margin has been reasonable, ranging from 32.9% in 2022 to 34.0% in 2025. Furthermore, Microsoft has maintained high return on equity (ROE) ratios of over 30% since 2018.

In light of the above financial performance, it is not surprising that analysts have a positive outlook for the company's future. They estimate that the company's net income will increase from $92.49 billion in 2025 to around $ billion in 2027, while the earnings per share (EPS) will reach $14.4 in 2027, according to the consensus of Wall Street. Moreover, the company's management has a history of generating high shareholder returns, primarily through share buybacks and dividends. The company’s dividend yield has ranged from 0.83% in 2021 to 1.13% in 2025, and it is expected to remain stable in the future.

Overall, Microsoft is a highly profitable and financially stable company, with strong growth potential in its cloud computing and artificial intelligence segments. While its current P/E ratio of 26.6x may seem relatively high compared to historical averages, it is still within reasonable range for a tech company with its growth prospects. The company's strong net cash position and negative leverage ratio further demonstrate its financial stability.

In conclusion, I believe that Microsoft is a strong investment opportunity for long-term investors. While short-term volatility and market fluctuations are always a possibility, the company's financial strength and growth potential make it an attractive option. With its continued investments in cloud computing and artificial intelligence, Microsoft is well-positioned for success in the rapidly evolving technology landscape.

Microsoft Best Entry for investmentHi every one

You can earn using microsfot stock

Entry 286 USD

SL - 211

Target

424

Microsoft Rounding TOPMSFT looks over bought and time for a correction. The rounding top is quite evident

For Me MSFT Looks Bullish As It is Shown on the chart I think $MSFT is going to go up to reach 262$ in the Mid-term and to 280$ As a next target

Keep in mind that it has an earning forecast today ( and I think it will be positive ) as appears on the price action on the chart.

This is my Humble opinion

Please left a comment about What do you think

AI - Running Away From The NazzyAn AI index, comprised of:

Shown in Blue

Google

Microsoft

NVIDIA

C3.AI

Nasdaq Shown in Orange

We see that they have broken away from the returns offered by the Nazzy Tech Index

Bottom of the Graph:

Spread between the above defined AI index and the Nazzy.

Has reached its All Time High..

Traders would have earned an additional 20+% by investing in the AI index in lieu of the Nazzy

Mind you, these companies have Zero additional profits resulting from AI, at this time.

How to profit from this?

Accepting ideas.

Reversal?Potential reversal identified based on August price action.

We are at a tipping point for tech.

Weekly technicals are oversold.

MACD monthly remains negative.

Jobs report and further Fed hikes may amplify this technical analysis may tip the scales and send tech plummeting.

Good luck,

Opinion - not financial advice

MICROSOFT (MSFT) Still going down?This idea is only for educational purpose, and just from technical perspective. I know nothing about the fundamental analysis.

Harmonics on MicrosoftNASDAQ:MSFT

Harmonics pattern drawn on NASDAQ:MSFT daily timeframe chart suggests that bullish trend may continue till 305, before it starts some correction for next move.

MSFT Microsoft to 290 by JulyPrice action looks like this could be a cup and handle breaking out through the $165 area. Lots of important economic signals coming in the next 2 week which, if good, could be a boon for markets and especially blue chip technology. MSFT is one of the strongest looking stocks of them right now in my opinion. Out on two closes under $140 looking to see this test $290 area when I would set a hard stop order to $280 and let it ride.