Microsoft (MSFT) | The best scenario for climbing📝Hello traders, Microsoft in daily timeframe , this analysis has been prepared in daily timeframe but has been published for a better view in 2 day timeframe.

It is better not to talk about the general nature of this wave and only explain the counted part of the wave.

Based on the counting of the first wave 1 and 2, it has ended in a very normal state and now we are inside the third wave.

From wave 3, waves 1, 2, and 3 are completed, and now wave 4 is formed. We assume that wave 4 is formed in the form of a flat, and two waves are needed from this plate to complete, and the end point of this wave can be rough due to wave 2, which is deep. 0.23 and 0.38, and it is better to start the upward movement for wave 3 by hitting the trend line and breaking the upper side of the channel.

The target for Wave 3 is a multi-fibo collision.

If the warning sign fails, the field analysis will not go down, but will return to normal.

🙏If you have an idea that helps me provide a better analysis, I will be happy to write in the comments🙏

❤️Please, support this idea with a like and comment!❤️

Microsoft

Microsoft | Fundamental Analysis | MUST READ | LONG SETUP ⚡️The market was on the upswing yesterday as receding fears of Omicron strain and renewed expectancy for the "Build Back Better" bill led to significant gains in stocks. Amid all the exciting moves in battered cyclical stocks and small-cap stocks, another important story -- actually, two stories -- surrounding technology star Microsoft may have slipped past your attention. These headlines were not only important in and of themselves, but also in terms of what they connote for Microsoft's growth prospects.

Two days ago, the European Commission approved Microsoft's upcoming deal with Nuance Communications. Microsoft announced a $16 billion deal with Nuance back in April, but its prospects have never been entirely certain. Microsoft is a large and powerful technology company, which means antitrust concerns are always a danger to any deal -- especially a big one. The Nuance deal is the second-largest for Microsoft after its 2016 acquisition of LinkedIn.

But Microsoft seems to know what it's doing when it targets a company. That wasn't evident last year when executives of most FAANG stocks had to testify before Congress about their market power. And Europe has been particularly tough on big tech companies in recent years, even tougher than the U.S.

Nevertheless, the commission concluded that the Nuance acquisition would not significantly reduce competition in artificial intelligence (AI) in health care. Now that the merger is set to take place, Nuance's AI capabilities are expected to strengthen Microsoft's already strong cloud-based healthcare services.

During the merger, CEO Satya Nadella said: "Nuance provides a level of AI at the point of care and is a pioneer in the real-world application of enterprise AI. AI is a critical technology priority, and healthcare is its most relevant application. Together with our partner ecosystem, we will put advanced AI solutions in the hands of professionals everywhere to drive better decisions and create more meaningful connections, accelerating the growth of Microsoft Cloud for Healthcare and Nuance."

Over the past two years, Microsoft has managed to maintain outstanding cloud growth through the introduction of industry clouds. It looks like Nuance will fill some of the gaps in Microsoft's healthcare capabilities.

With the ability to still make large and meaningful acquisitions, MSFT seems to have an advantage over some competitors who seem to be attracting more antitrust attention for some reason. This ability may let it support growth longer than skeptics believe.

Following this good news, Microsoft wasted no time in announcing another acquisition. This time Microsoft will acquire digital advertising technology company Xandr from AT&T. Xandr is the result of a merger of AT&T's own digital advertising capabilities with AppNexus, the programmatic advertising company it acquired for $1.6 billion in 2018.

AT&T had hoped to turn Xandr into a powerful programmatic advertising company, but apparently, the scale wasn't enough to justify keeping it. AT&T has recently sought to sell non-core assets to pay down debt in anticipation of the spin-off and merger of WarnerMedia with Discovery. The terms of the deal have not been disclosed, so we don't know how much Microsoft will pay.

Microsoft will likely try to merge Xandr with Bing, its second-ranked search engine, to create better programmatic and artificial intelligence-driven advertising capabilities. Bing is often something of secondary consideration for Microsoft investors, but it's not worth telling management. Microsoft seems intent on developing its digital advertising capabilities to compete with the dominant "walled gardens" of digital advertising, especially since privacy restrictions could open up competitive opportunities.

While many are willing to settle for Microsoft's enterprise software alone, the tenacity to push into other areas of growth is admirable and is music to the ears of this happy shareholder. If there is any danger of over-diversifying the business away from core capabilities, as AT&T has done, it has not manifested itself in Microsoft's financial performance.

After rising 43% over the past 12 months, marking another successful year for the market, and finding itself just below historic highs at $327 per share, Microsoft may have investors wondering if the company can continue that streak. After all, it's harder to grow fast the bigger you get.

However, people said this a few years ago about Microsoft when the stock price was still in double digits. Earnings in several of the company's core businesses remain strong, and these two new acquisitions demonstrate management's tenacity in pursuing growth across an impressive portfolio.

MSFT daily chart analysisTrade breakdown:

1. Ideal entry point should be around $331-$330 price range, with stops below $325.

2. 1st PT @ $358, 2nd PT @ $362.

Good luck!

Microsoft Analysis 20.12.2021Hello Traders,

welcome to this free and educational analysis.

I am going to explain where I think this asset is going to go over the next few days and weeks and where I would look for trading opportunities.

If you have any questions or suggestions which asset I should analyse tomorrow, please leave a comment below.

I will personally reply to every single comment!

If you enjoyed this analysis, I would definitely appreciate it, if you smash that like button and maybe consider following my channel.

Thank you for watching and I will see you tomorrow!

Monday Preview. My trading ideas for this weekHi Traders,

These are my ideas for the week for a multiday strategy. Focus on

- EURJPY

- GBPUSD

- AMAZON

- MICROSOFT

- SPX500

This is my view on this pair for the next days on #SPX500 using my 2 intraday strategies.

(I’ve just shared my fully explained 81strategy on Tube)

I remind you that this is only a forecast based on what current data are.

Therefore the following signal will be activated only if specific rules are strictly respected.

If you follow my strategy you will be able to identify the right filters and triggers to enter correctly the market and avoid fake signals.

I really hope you liked this video and I would like to know what do you think about this analysis, so please use the comment section below this video to give me your point of view.

Thank You

MSFT - Softy always leads the Rally into DeclineAhem...

This one is clearly attempting 350 push.

Calls are being bought like no tomorrow

once again.

Gamma Slamma Or oh sh_it.

$MSFT | 12/13-12/17 | Watchlist #3 $MSFT +343

(Over 343 for calls)

Technical Analysis: Bull flag breakout on the hourly chart

News catalyst: Last week, Wedbush Securities named MSFT as one of its top tech picks for 2022.

Microsoft softening up for a fall. MSFTAnyone else notice this triple divergence that already formed? Who knows what will happen with this large cap, as it is constantly propped by bail out coof money, but lets see anyway.

We are not in the business of getting every prediction right, no one ever does and that is not the aim of the game. The Fibonacci targets are highlighted in purple with invalidation in red. Fibonacci goals, it is prudent to suggest, are nothing more than mere fractally evident and therefore statistically likely levels that the market will go to. Having said that, the market will always do what it wants and always has a mind of its own. Therefore, none of this is financial advice, so do your own research and rely only on your own analysis. Trading is a true one man sport. Good luck out there and stay safe!

$MSFT 4hr Fibs and Waves Yawn. let's see.

Rich sold a lot of shares, scary!! Let's be honest, MSFT is a beast and not going anywhere. The weekly shows we owe a larger corrective wave soon though.... so unless there's some PR, etc I expect more chop in the future.

your best bud,

patrick.

Microsoft | Fundamental Analysis | Long Setup | MUST READ ! Microsoft recently became the subject of heated controversy following Satya Nadella selling more than half of his shares for about $285 million at the beginning of last week. As per an F-4 filing, the CEO sold 838,584 shares at prices ranging from $334.37 to $349.22, reducing his total stake to 830,791 shares.

Should investors be worried about such an extensive deal? Let's go back to Nadella's achievements, his salary, and previous stock sales to come to some conclusion.

When Nadella took over as Microsoft's third CEO seven years ago, the tech behemoth was in serious difficulty. New cloud services were undermining its desktop software, Windows users were adamantly sticking with legacy versions of the OS, and the company was losing out to Apple and Alphabet's Google in the mobile market.

But Nadella extremely altered things by actively developing the company's cloud services, redefining Windows as a cloud service, and dropping Windows Phone to launch new mobile apps for iOS and Android.

Microsoft's cloud business has been a major driver of the company's growth, with revenues rising from $86.8 billion in fiscal 2014 to $168.1 billion in fiscal 2021, which ended in June of this year, and EPS more than tripling.

With this growth, Microsoft's market value has risen from $300 billion on Nadella's first day in office to nearly $2.5 trillion today. So Nadella unquestionably earns to sell some of his stock after this historic rally.

In the fiscal year 2021, Satya Nadella's total compensation rose 13% to $49.9 million. This amount includes a base salary of $2.5 million, equity compensation of $33 million, and non-equity incentives of $14.2 million.

Thus, Nadella's latest deal pictures several years of cumulative stock awards. The deals also represent Nadella's only non-equity direct sales in the past two years.

Microsoft CFO Amy Hood also sold 60,000 shares (11% of the stock she owned at the time) at an average price of $303.08 in a direct transaction on Sept. 1. This was Hood's first direct sale since last September.

These insider sales are not certainly an indication that Microsoft is facing difficulties. Executives sell their stock all the time for personal reasons that have nothing to do with the company's immediate and long-term prospects. For example, Microsoft co-founder and first CEO Bill Gates sold most of his stock before leaving the board in early 2020 - but the company's stock has continued to rise.

Over the past three years, Microsoft stock has nearly tripled, and in the past 12 months alone, it has risen more than 50 percent. Analysts expect the company's revenues and profits to grow 17% and 14%, respectively, this year, but the stock certainly isn't cheap -- it's worth 36 times its projected earnings.

This higher ratio -- along with macroeconomic factors such as inflation, supply chain pressures, and the new COVID-19 option -- may have convinced Nadella, Hood, and other Microsoft insiders to sell some of their shares. Nevertheless, Nadella's shareholding will increase again this year as he gets more stock bonuses.

In general, it's more useful for investors to track insider deals at struggling companies -- where insiders can make rosy promises of a turnaround while dumping their own stock -- than at successful companies.

Microsoft is one incredibly successful company, and Nadella's big sale doesn't suggest that its long-term prospects have changed. As an outside investor, you also won't be entitled to more stock like Nadella, who can afford to sell his stock repeatedly because it makes up most of his paycheck.

So it makes no sense to short Microsoft just because the CEO sold half of his current stake. Instead, investors should be looking at Microsoft's cloud growth and expansion of its ecosystem, rather than worrying about Satya Nadella's well-deserved salary.

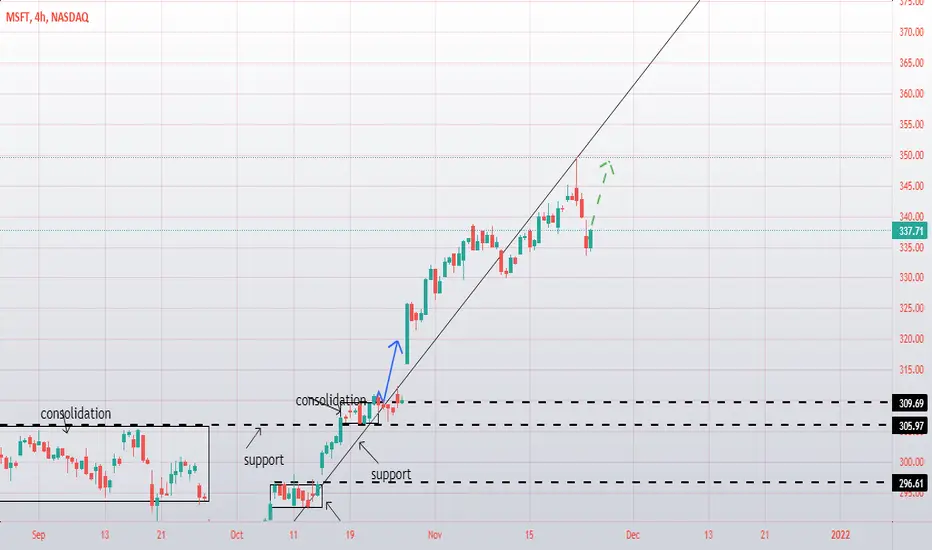

MSFT - STOCKS - 18. OCT. 2021Welcome to our Weekly V2-Trade Setup ( MSFT ) !

-

4 HOUR

Overall bullish market structure..

DAILY

Great fundamentals and technicals.

WEEKLY

Nice long setup!

-

STOCK SETUP

BUY MSFT

ENTRY LEVEL @ 304.18

SL @ 291.89

TP @ Open

Max Risk: 0.5% - 1%!

(Remember to add a few pips to all levels - different Brokers!)

Leave us a comment or like to keep our content for free and alive.

Have a great week everyone!

ALAN

Maybe LONG? or...it looks very strong. the price is going up. do not forget about the stop and possible reversal

Too Many Windows Makes Me Micro Soft this stock has had one too many pies don't mind me it could be the whisky

one too many pies

PIES

NASDAQ:MSFT

CAPITALCOM:MSFT

SWB:MSF

MOEX:MSFT-RM

BCBA:MSFT

BMFBOVESPA:MSFT34

XETR:MSF

BMV:MSFT

NEO:MSFT LSE:MSFT

SIX:MSFT

SIX:MSFT.USD

LSIN:0QYP

MIL:MSFT

BCBA:MSFTD

BCS:MSFT

BCBA:MSFTC

EURONEXT:MSF

EUREX:MSTF1!

HKEX:4338

BVL:MSFT

CHIXAU:TCXMSF

FWB:MSF

TVC:NDX

NASDAQ:NDX

SKILLING:NASDAQ

NASDAQ:NDAQ

NASDAQ:QQQM

NASDAQ:QQQ

MSFT idea #3Consolidating at top of downward channel and looking like an inverse head & shoulders pattern.

Looking to enter long above channel.

MSFT: Retesting the breakout area or going further down?I will go long with MSFT if it takes support from 330'sh. If it breaks, I will SHORT and buy back at 315'sh.

Slightly Late Bullish Gartley Entry on IntelThis entry is a little late on the daily but on the weekly we do have a bullish engulfing so on that timeframe this entry might not be considered very late. With the release of Windows 11 it seems that intel will be reclaiming some ground against AMD and the Gartley may be giving us a hint that it will.

msft analyse.after the strong up trend in all the time frames biggest then 30min . i think it's gonna be a big correction to 305. . so i expect it will look to go down . that's My Personnal Opinion . Hope You Like it.

Microsoft | Fundamental Analysis | Must Read...Microsoft's stock price reached an all-time high after the tech behemoth published its first-quarter earnings report last Tuesday. The company's revenue increased 22% year-over-year to $45.3 billion, beating analysts' forecasts by $1.3 billion. Adjusted earnings surged 25% to $2.27 per share, $0.19 above expectations.

For the second quarter, Microsoft management expects revenue growth of 16% to 18% year-over-year, which also beat analysts' expectations of 14%.

Microsoft's performance is majestic, but some investors may not crave to buy its stock after its price has already risen almost 50% in 2021. Let's look at a few reasons to buy Microsoft stock, as well as one argument for selling it, to see if it is still an attractive investment at these prices.

First and foremost, of course, is the growth of Microsoft Cloud Computing.

Microsoft's dramatic growth over the past seven years has been booste by the expansion of its cloud services, particularly Azure, Office 365, Dynamics, LinkedIn, and other cloud software. The business records the performance of these businesses together as "Microsoft Cloud."

In the first quarter, Microsoft Cloud's revenue grew 36% year over year to $20.7 billion, matching the 36% growth rate in the fourth quarter.

Revenue from Azure, the most thoroughly supervised segment of Microsoft Cloud, grew 48% on a constant currency basis. That represents an acceleration from Azure's 45% growth on a constant currency basis in the fourth quarter and should allay fears of a possible slowdown.

Azure's share of the global cloud infrastructure market also grew from 19% to 21% between the third quarters of 2020 and 2021, according to Canalys. That puts it in second place behind Amazon Web Services (AWS), whose year-over-year market share was unchanged at 32%.

Microsoft probably could not have achieved this growth without Satya Nadella, who took over as third CEO in 2014 and aggressively expanded these services with his mantra "mobile first, cloud first."

Second, we should not forget the recovery of favorable trends.

Over the past few years, Microsoft has become a fast-growth company again, but it continues to return tens of billions of dollars to its investors.

During the pandemic, several Microsoft enterprise services, including Office 365 Commercial, Dynamics 365, and LinkedIn Marketing Solutions, were disrupted as businesses closed.

However, as businesses resumed operations, those factors eased. In the first quarter, Office 365 and Dynamics 365 provided an acceleration in growth on a constant currency basis, and LinkedIn Marketing continued to grow.

The growth of these "resurgent" segments, along with the continued growth of Azure and other cloud services, is offsetting the slowdown in Microsoft's Surface and Xbox units, which suffered from chip shortages and other supply chains constraints in the first quarter.

Finally, it's returning a lot of cash to shareholders.

In the fiscal year 2021, Microsoft spent more than $39 billion on dividends and stock buybacks, accounting for about 70% of free cash flow (FCF). The company will spend another $10.9 billion, or 58% of FCF, on both activities in the first quarter of 2022.

Microsoft's forward dividend yield of 0.8% won't drag serious investors, but the company has reduced its stock by nearly 10% over the past seven years, offsetting the dilution from stock-based compensation plans.

Still, there is one single reason to sell Microsoft: its valuation.

Today Microsoft is worth $2.4 trillion, about eight times its market value of $300 billion when Satya Nadella became its CEO.

The company's stock currently trades at 13 times this year's sales forecast and 35 times its earnings forecast. Those estimates are slightly overstated compared to analysts' expectations for sales growth of 14% and earnings growth of 9% this year.

Massive market capitalization and high valuations could make it tough for Microsoft to repeat its multiple growth over the past seven years.

Microsoft stock is priced very high, but bears have been sounding the alarm about th is for years while the company's stock has been soaring. Still, most would agree that Microsoft deserves such a high valuation because it is still a perfect long-term investment that will continue to profit from the expanding cloud services market.

MICROSOFT SHARE PRICE ABOUT TO MAKE HUGE DIVEBe careful with Microsoft stock as the monthly RSI is very overbought.

MSFT MICROSOFT WILL GO UP '1 MSFT in trend up

2 MSFT break channel resistance with a high volume

3 MSFT it is time to buy it

4 There's a news support MSFT

connect with me for more stock analysis

good luck

NASDAQ:MSFT