The Best Months of The Year to Invest in US Stock to Make Money This video will show you the best months of the year you should be investing in US stock market.

In the video, I showed proof that this method works almost every time.

But if you feel you need me to guide you further on how to manage your investment portfolio, feel free to send me a DM now.

If you find this video helpful, give it a like, drop comments, and share it with your friends.

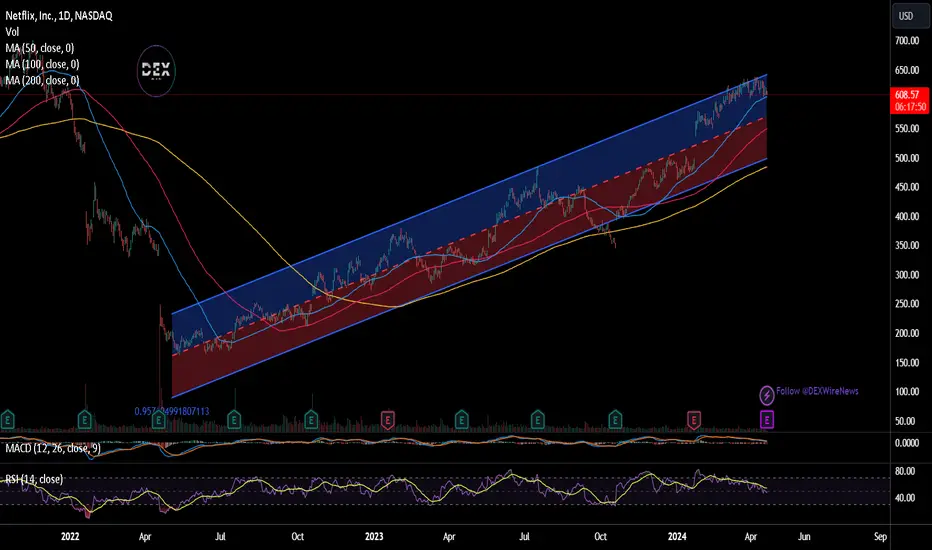

Netflix

NFLX is setting up for another gap down open next weekNFLX is setting up for another gap down open next week

Quite bearish action here, no longs for me until Jan gap close is closed

NFLX: Bullish dip?Friday was nasty for big tech. 10% drops in NFLX and NVDA got some people to fear for the worst. Is the market going to crash 90% now? Maybe not yet. Right now the price only retraced to 0.764 fib. I would expect a little more weakness next week and then a relief rally. Price should come down to about .618 fib retracement area where there is also some market structure support and take off from there. Weekly RSI is showing some bullish divergence, but not confirmed yet. As long as price doesn't fall through market structure supports and below $344, bull case is still on track to 2026 top. Good thing is that NFLX falls fast and recovers fast. Bad news is it is kinds difficult to time the short for this stock because it falls so quickly. So, I am not planning on shorting and also not worried yet on the long bag. Actually planning to add to the bag maybe another $30 below this level. We'll see how things go.

NFLX Netflix Options Ahead of EarningsIf you haven't entered NFLX in the buying zone:

Then analyzing the options chain and the chart patterns of NFLX Netflix prior to the earnings report this week,

I would consider purchasing the 607.50usd strike price at the money Calls with

an expiration date of 2024-4-19,

for a premium of approximately $26.50.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Netflix Faces Subscriber Growth Challenge Netflix has consistently set benchmarks and pushed boundaries. However, as the company gears up to report its earnings, a closer look reveals a nuanced landscape where subscriber growth is no longer a foregone conclusion. The once-lauded crackdown on password sharing, while initially boosting numbers, now presents a plateauing challenge. With the fervor of the pandemic waning, Netflix must navigate through shifting tides to sustain its momentum.

The Password-Sharing Conundrum

Netflix's recent surge in subscriber numbers was partly fueled by its global crackdown on password sharing. Yet, analysts warn that the euphoria from this initiative might be waning, especially in mature markets like the United States. While the crackdown may still yield results in burgeoning markets like India, it's evident that Netflix needs more than a singular strategy to fuel growth.

Diversification Beyond Traditional Models

In a bid to diversify revenue streams and cater to a wider audience, Netflix ( NASDAQ:NFLX ) has ventured into an ad-supported tier. With over 23 million monthly subscribers already onboard, this move marks a significant shift in its business model. Analysts predict that the ad-supported tier could play a pivotal role in mitigating churn and bolstering revenue in the years to come. Moreover, recent price hikes in premium plans could further incentivize users to opt for the ad-supported model, driving up average revenue per user.

Strategic Content Investment

Netflix's commitment to content remains unwavering, with projected investments reaching as high as $17 billion this year. Unlike its competitors, who are trimming content budgets to achieve profitability, Netflix ( NASDAQ:NFLX ) is doubling down on its content strategy. By retaining a flat spending trajectory, Netflix has managed to attract subscribers while securing rights to coveted content. The recent trend of competitors selling exclusive content to Netflix not only reduces churn but also underscores the company's dominance in the streaming arena.

Sports Entertainment: A New Frontier

In a strategic move to diversify its content portfolio, Netflix ( NASDAQ:NFLX ) has entered the realm of sports entertainment. The recent deal with World Wrestling Entertainment (WWE) signals Netflix's intent to tap into the lucrative sports entertainment market without bearing the exorbitant costs associated with traditional sports rights. By acquiring WWE's flagship program, "Raw," Netflix aims to leverage the inherent stickiness of sports content while aligning with its ethos of entertainment-centric programming.

Conclusion:

As Netflix ( NASDAQ:NFLX ) prepares to unveil its earnings report, the spotlight shines on its ability to innovate and adapt in a rapidly evolving landscape. While challenges loom, from plateauing subscriber growth to intensifying competition, Netflix's strategic diversification and unwavering commitment to content position it as a formidable force in the streaming industry. By embracing change, seizing opportunities, and staying true to its vision, Netflix ( NASDAQ:NFLX ) charts a course towards sustained growth and continued relevance in the ever-expanding world of streaming.

Netflix Q124 earnings preview – subscribing to volatility Release time – Thursday on the market close (6 am AEST / 9 pm UK time)

Netflix is one of the preeminent trading stocks - where we often see big movement, a high propensity to trend and sizeable intraday high-low daily ranges that can appeal to the day traders.

With Q124 earnings due on Thursday and the possibility of another sizeable price catalyst, Netflix is a stock that should be on the radar.

Netflix is already something of a market darling, where the share price has significantly outperformed the S&P500 by 19.6 percentage points over the last 3 months and by some 51.7 percentage points over six months.

Going into this earnings release, with price having recently traded to a multi-year high of $639, we now see consolidation with price tracking a range of $639 to $600, and importantly holding above the 50-day MA ($601.12), which has been a solid trend filter since October.

We can see the Bollinger Bands tightening up into Q1 earnings as price moves remain contained to the 20-day MA, and traders refrain from taking risks until the facts are known. A daily close above/below the bands and/or the recent trading range could be meaningful and could suggest a higher probability that we see a trend develop, which could be a compelling hunting ground for more momentum-styled traders.

Earnings pedigree

Netflix does have a strong pedigree at earnings, having beaten consensus expectations in 7 of the past 8 quarterly earnings reports. Many will also recall the Q423 earnings report where NFLX added 13.1m paid streaming subscribers, a number well above expectations and subsequently, the shares rallied strongly.

NFLX has a history of pronounced movement on earnings, with double-digit percentage moves in the prior 2 reporting quarters (on the day of earnings) and taking the period out the absolute move has averaged -/+ 12.8%. Being able to capture that movement in the post-market session is important for traders, and despite a potentially fast-moving market, there should be ample liquidity.

By way of expectations of price movement for this earnings report, we can look at the options market and asses the implied move on the day of earnings, which now currently stands at -/+ 8.1%.

This level of implied volatility speaks to the view that we could easily see movement in the share price once the earnings and guidance are known and could offer opportunity, but it is also a risk that those with existing positions may need to manage.

What to watch this time around?

For CFD traders going through the finer details of cash flow, subscribers’ numbers and sales growth seems a tough proposition. This is why most will let the market tell them how they feel about the shape of the business, and dynamically react to the ensuing price action.

However, by way of a kicker, the likely overriding driver will be quarterly subscriber adds and any guidance for Q224 subscribers. The consensus (from investment bank analysts) is for 4.77m net subscriber adds in Q1, with 3.7m pencilled in Q2. The view on the street is this is a low-ball call – which won’t surprise given NFLX have beaten consensus expectations for sub growth for three quarters in a row - and investors are positioned for a number closer to 7m, even 8m.

On headline Q1 earnings estimates, the consensus view is we for:

Earnings per share (EPS) - $4.54 (Q224 estimates $4.55)

Revenue - $9.264b (Q224 estimates $9.50b)

Free cash flow - $1.89b (Q224 estimates $1.50b)

There will be a focus on the crackdown on password sharing and how that is impacting earnings, competition, ad-supported tier, and commentary on unique programming.

The consensus 12-month price target for NFLX is $626, so I question if there is scope for a solid earnings re-rating, which could see these targets revised higher. That said, price targets are largely irrelevant for traders, and price will react far quicker than any analyst can change their models. The market will let us know about the earnings and the operating environment and the price could see some outsized moves – one to put on the radar.

Earnings alert: Companies to watch for potential trades this weeAs we step into the second week of the Q1 earnings season, a roster of major financial players is gearing up to unveil their financial reports.

Expect updates from Goldman Sachs, Bank of America, Morgan Stanley, American Express, Blackstone, and Charles Schwab.

Additionally, non-financial companies like UnitedHealth, Taiwan Semiconductor Manufacturing, Netflix, P&G, J&J, and ASML Holding are also slated to release their earnings.

While bank stocks have been outperforming the broader S&P 500 Index in the past six months, the tide may be turning in the first quarter of this year. Despite JPMorgan's announcement of a modest 6% rise in profits on Friday, shares dropped over 5% following the bank's conservative full-year projections for net interest income. Meanwhile, Wells Fargo and Citigroup saw declines in profits.

On Wednesday, eyes will be on Discover Financial Services as it presents its results following the announcement of its acquisition by Capital One in February. And wrapping up the week is American Express, which is set to report after providing strong full-year guidance and increasing its dividend in the last quarter. Blackstone is expected to reveal a year-over-year increase in earnings driven by higher revenues.

Thursday brings Netflix's report, with the streaming giant aiming to maintain its momentum in subscriber growth. Netflix's management has recently expressed confidence in their growth strategy, emphasizing improvements across all aspects of their platform, the introduction of paid sharing, and the expansion of their advertising offerings.

Consumer product giants Johnson & Johnson and Procter & Gamble will disclose their earnings on Tuesday and Friday respectively, offering insights into whether increased prices are sustaining revenue growth.

Meanwhile, health insurer UnitedHealth Group is set to report on Tuesday amid rumors of an antitrust investigation.

Netflix : Is a Major Market Correction coming? 📉Following our last analysis, Netflix has precisely achieved the forecasted targets, with the wave ((iii)) extending to 227 to 261%. This suggests that a correction towards wave ((iv)) might be imminent, expected to range between 38% and 61.8%, thus laying the groundwork for a wave 5 and the culmination of a significant cycle in the form of a potential wave (2).

A closer examination of the daily chart reinforces our primary scenario: the completion of Wave II at the low of $162.80. We are currently in the process of developing Wave (1), followed by Wave (2), and so forth.

In our alternative scenario, we consider the possibility of a Regular Flat, especially when analyzing the complex correction currently unfolding. This might indicate that rather than concluding Wave (2) at $162.80, it was actually Wave (A), and we are now witnessing Wave (B) achieving exactly 100% of Wave I. Such alignment could signal a 5-wave decline towards a double bottom, marking a significant correction of 70%.

While such a correction would be substantial, it is essential to explore all scenarios to be prepared for any market developments. Despite the potential for a significant pullback, our underlying outlook remains optimistic, expecting a continued upward momentum for Netflix.

Netflix, just another analysis.Have you ever wondered what happens when a growth stock, well, doesn't grow anymore?

Netflix is, at the moment, just a few bucks (I mean billions lol) below the 100 B dollar market cap.

kinda big uh? it's like 100 unicorn start-ups together :D

Anyway, let's get to the point.

In the past, the company now considered OLD for us, the younger, simply exists, and they just work (you know, revenue, FCF etc, all cool stuff)

they're not considered growth, ANYMORE, cuz in the past they must have been considered so right? everyone grows, then you just "keep what you have" or fight for it when you cant grow bigger.

Now, from the internet, it is kinda known (in my studies at least) that a PE of 13-17 makes a company a good buy, but it's not undervalued yet.

Well, it is also true that a PE of 30 for a growth stock is considered a good ratio as well, cuz you know, that's a GROWTH stock.

Ah almost forgot, when there are not a lot of numbers or a lot of past years to analyse, the PE can go well about 30 (remember tesla? XD)

So, the point is: Netflix went from PE>100 in the past years, then it fell to PE = 38 after Q4 2021 and NOW after Q1 2022 has fallen to PE = 19

Does it recall something to you?

My idea? this "thing" just went from "hypergrowth stock" 2 years ago (ofc covid helped, maybe its not a big pharma conspiracy but a Netflix one LOL), to a "simple growth" 1 quarter ago, and now its gone to a "value" stock.

Before I end the analysis, a reminder: at the moment, Netflix has a PE of 19, well above the >13 expected for a value stock to be at a good price, which means the stock should fall another 30% AND, well, what a lucky coincidence another fall of 30% would bring the price to the MA200 of the MONTHLY chart.

Trade safe, and remember that wall street uses Algorithms, faster and better than you for trading purpouses.

Let me know in the comment if you have a DIFFERENT opinion, if you agree with me simply leave a like ;)

NIKE BULL AFTER EARNINGS 120Nike’s stock looks bullish over the longer-term after breaking up from a falling channel pattern on the daily chart1.

If Nike receives a bullish reaction to its earnings print and remains above the 50-day SMA, the eight-day EMA will cross above the 21-day EMA, which would be bullish1.

Wells Fargo analyst Ike Boruchow added Nike to his top picks list, stating, "We simply believe the recovery characteristics and self-help story now beginning at make for a more compelling long idea into 2024

NETFLIX Last pull-back possible before $750Netflix (NFLX) has been trading within a long-term Channel Up on the logarithmic scale for the past 20 months. The trend is very aggressive to the upside and since the first Bullish Leg made a Higher High on February 03 2022 on a +130.30% rise, we do expect a similar % rally that would technically target a little below $800, so aiming at $750 would be a fair price.

Until then however, the Channel Up structure suggests that the stock has entered the Volatility Phase which during the previous Bullish Leg took place right before the Peak. As a result, a last pull-back towards the 1D MA50 (blue trend-line) would also be fair. Technically it could seek the -0.236 Fibonacci extension ($550) from the Take-off Phase's High.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Momentum, Growth & Innovation: Updated WatchlistMomentum, Growth & Innovation: Updated Watchlist

www.tradingview.com

My updated trading watchlist includes a diverse range of companies across various sectors, prominently featuring technology, healthcare, and finance, among others. These companies, currently part of ARK Invest's holdings, are identified as being in a confirmed Stage 2 uptrend, indicating strong bullish trends according to Mark Minervini's methodology. This analysis will highlight key sectors represented, providing a broad understanding of the market dynamics at play.

Technology Sector

Companies like NASDAQ: NASDAQ:AMD (Advanced Micro Devices Inc) NASDAQ: NASDAQ:MSFT (Microsoft) NASDAQ: NASDAQ:NVDA (NVIDIA Corporation) and NASDAQ: NASDAQ:GOOG (Alphabet) underscore the significant emphasis on technology, particularly in semiconductors, cloud computing, and artificial intelligence. These firms are at the forefront of innovation, driving trends in digital transformation, and represent strong growth opportunities as they capitalize on increasing demand for technology solutions.

Healthcare and Biotechnology

NASDAQ: NASDAQ:IONS (Ionis Pharmaceuticals) NASDAQ: NASDAQ:RXRX (Recursion Pharmaceuticals Inc) NYSE: NYSE:NET (Cloudflare) and NASDAQ: NASDAQ:VRTX (Vertex Pharmaceuticals Incorporated) highlight the focus on healthcare and biotechnology. This sector benefits from ongoing advancements in medical research, genetic sequencing, and personalized medicine. Companies in this space are pivotal in addressing global health challenges, including new therapies and vaccines, reflecting potential for significant impact and investment returns.

Finance and Cryptocurrency

With holdings like NYSE: NYSE:ICE (Intercontinental Exchange Inc) NASDAQ: NASDAQ:COIN (Coinbase Global Inc) and AMEX: BITO, there's a clear interest in financial services and the burgeoning field of cryptocurrencies. These selections point to the growing influence of digital assets and blockchain technology in reshaping financial transactions, investment strategies, and asset management.

Consumer Discretionary and E-Commerce

Companies such as NASDAQ: NASDAQ:AMZN (Amazon.com Inc) NYSE: NYSE:SHOP (Shopify Inc.) and NASDAQ: NASDAQ:MELI (MercadoLibre) represent the e-commerce and consumer discretionary sectors. Their inclusion underscores the continued growth in online retail and digital consumer behaviors, accelerated by global shifts towards online shopping and digital platforms for goods and services.

Aerospace and Defense

With NYSE: NASDAQ:KTOS (Kratos Defense & Security Solutions Inc) NYSE: NYSE:LHX (L3Harris) and NASDAQ: NASDAQ:AVAV (AeroVironment Inc.) there's an acknowledgment of the importance of aerospace and defense. These companies are involved in cutting-edge technology for national security, space exploration, and unmanned aerial vehicles, sectors expected to see substantial growth due to increased defense spending and interest in space.

Conclusion

My watchlist reflects a strategic focus on high-growth sectors poised for continued expansion and innovation. By targeting companies within technology, healthcare, finance, consumer discretionary, and aerospace & defense, the list aligns with sectors that not only have strong current performance but also hold future growth potential.

Netflix hourly double bottomGreat hourly double bottom shaped yesterday on Netflix chart. The context looks good: we are in the correction wave on daily with retracement ~50%. Broad market also recovered yetserday and looks strong.

I'll be defintely watching reaction near 586 level, where strong sell-off occured on Tuesday, with a goal to enter on the next hourly higher low

Netflix 23 Feb 2024Date : 23 Feb 2024

Main Trend : Up

preferred Transaction : Buy

Reasons : mentioned on chart

Technical Analysis success at level : 684 $

Technical Analysis fail at level : 535 $

NETFLIX Correction starting. How low can it go?Netflix (NFLX) has gone a long way since our November 28 2023 buy signal (see chart below) that reached our $580 Target, giving more than +20% return:

As the price has been consolidating for practically 2 weeks, it is time to update our outlook for medium as well as long-term investors. The long-term Bullish Megaphone pattern that started on the July 13 2022 Low, is intact and the stock continues to respect its Support and Resistance levels.

The current consolidation is coming off an overbought 1D RSI peak at 83.00, which has since corrected, while the price was consolidating, which is a technical Bearish Divergence. We have previously seen the same kind of overbought RSI Bearish Divergence on the July 19 2023 and February 03 2023 peaks, both Higher Highs on the Bullish Megaphone.

As a result, we expect a correction of around 4 weeks and being on a consolidation suggests that it is still early to enter. The 1st Support level is the 1D MA50 (blue trend-line), which has been intact since the October 27 2023 bounce, but we are aiming for the 1D MA100 (green trend-line) as it has been touched during both 2023 correction waves. Our Target is at $485, but we will book the profit earlier if the 1D RSI hits the 30.00 oversold limit first.

The Sine Waves can be used as an extra decision making indicator here. As you can see they fairly match the Peaks and Lows of the stock price, so if the price approaches the Sine Bottom March 20 and hasn't rebounded yet, we will close the shorts and buy long-term regardless.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Netflix is cancelledBack in July 2023 NASDAQ:NFLX on earnings did a weekly price Spike across a major 50% Retracement level. I entered into a short trade on the stock which worked well for a few months until the market turned decidedly bullish in October and then the trade stopped out. The recent earnings pushed the stock price higher as Netflix net income is dramatically higher than it was last year.

In the meantime I switched my cell phone carrier to T-Mobile and with the unlimited data package (that I need as my backup Internet for trading) it included "free" Netflix. Fine, I'll setup an account, but I will name my profile what I named it...

Neflix content has declined in quality dramatically over recent years as intellectual property owners have rescinded or let expire their content deals to put them on their own platforms. There are also certain... ideological... leanings of Netflix content that I will not expand upon. Either way, my feelings about a company I try to avoid trading upon... because as we can see in this example one's feelings do not translate to good trades alone.

However, in addition to lackluster content a change in their rate plan is underway which may be significant. Netflix is trying to upsell customers on "better video quality" while inserting ads into lower tier content. I for one refuse to watch commercials so I promptly cancelled whatever "free" service that T-Mobile was offering me. Right now I do not think there is a trade to be made either on this change or price but I am watching.

A bit of trading history to share about Netflix... back in 2011 Neflix had a whopping -83% drop when it tried to change its subscription plans to separate the mail order service from the streaming service. Netflix was being forward looking but the market was still living in a world that expected us to be ordering DVDs forever. The market is very often very wrong.

METFLIX LONG TERM TO 1K USD ?!Hi ,

As you can see the channel , we will see netflix to 1K in a few next months

Please trade as your own risk

Netflix Surges 9% In One Day!Disney's recent move to license more TV shows to Netflix marks a significant shift in the streaming industry, bolstering Netflix's extensive content library. Historically, Netflix has heavily invested in content, spending over $17 billion annually at one point, to maintain its industry dominance.

However, Netflix has faced challenges like subscription fatigue and increased competition, leading to reduced profitability and subscriber numbers. In response, the company has implemented cost-cutting measures and introduced strategies like cracking down on password sharing and launching ad-supported tiers to boost revenue.

Despite a heavy debt load exceeding $14 billion, Netflix's operating margin shows signs of improvement, potentially reaching up to 24%. The company's stock has seen a 16% increase in 2024, following a 64% rise in 2023. Notably, the stock surged 9% post-earnings announcement last week, despite Q4 earnings falling short of estimates. This indicates continued investor confidence, as negative earnings didn't dampen stock performance.

Looking ahead, the focus is on whether Netflix can surpass its November 2021 all-time high of $700. Achieving this would underscore the company's resilience and adaptability in the dynamic streaming market.

NFLX Jan 26th Update, Target got hitWe had a great bull flag setup going into the earnings.

Now the target got hit, will be watching for a retracement into early Feb and another push higher into Feb OPEX

Nothing bearish here to even try taking a short trade. There is still one more gap to close above the price, should be hit first before reversal starts.

Also the price might just consolidate/correct in time and push above to a new high. Any shorting should have solid stops

NFLX Short: Gap Fill and High RSIHey All,

I wanted to get your feedback on this analysis.

I am solely basing my opinion based on the RSI indicator, MACD and candlesticks on the daily chart.

Although earnings help NASDAQ:NFLX to go up slightly. It had to restest a strong resistance at 562.46. Once it reached the resistance the bears took control which resulted in a pretty strong bearish pinbar, usually signaling a reverse in trend. Along with the pin bar the RSI is way oversold and the MACD is looking like it is being set up for a bearish divergence, where the price action is trending up, but the MACD is trending down. In addition, there was also a gap up during earnings and that gap will need to be filled.

This signals to me that the there will be a short, even if just to fill the gap up.

What do you guys think?

Netflix's Spectacular Q4 Performance Ignites Investors Spirit Netflix (NASDAQ: NASDAQ:NFLX ) has once again defied expectations with its stellar fourth-quarter performance, surpassing Wall Street estimates and achieving its largest-ever subscriber growth for the final quarter. The streaming giant added a remarkable 13.1 million subscribers, soaring past the projected 8.97 million, and bringing its total subscriber count to a staggering 260 million. As the company's stock experiences an upward surge, it's evident that Netflix ( NASDAQ:NFLX ) is not just riding the wave of its content library but actively reshaping the landscape of streaming services.

Unprecedented Subscriber Growth:

Netflix's robust subscriber growth in Q4 is attributed to strategic content releases, including the much-anticipated final season of "The Crown" and David Fincher's original film, "The Killer." The company's ability to consistently deliver compelling and diverse content has solidified its position as a streaming powerhouse. The 13.1 million new subscribers showcase not only the platform's global appeal but also its adeptness at retaining and attracting viewers.

Financial Triumph:

Netflix's ( NASDAQ:NFLX ) financials also paint a rosy picture, with revenues surging to $8.8 billion, surpassing both forecasts and the company's own guidance of $8.7 billion for the quarter. This represents a remarkable 12.5% year-over-year growth, driven in part by the crackdown on password sharing and the introduction of a subscription plan with advertising. The company's focus on profitability is further emphasized by the increased 2024 full-year operating margin forecast of 24%, up from the previously projected range of 22% to 23%.

Diversification Strategies:

Beyond its core streaming business, Netflix ( NASDAQ:NFLX ) is venturing into new territories, notably advertising and gaming. The streaming giant is keen on making advertising a significant revenue driver, with plans to enhance the attractiveness of its ad-supported tier. Netflix's foray into live entertainment, exemplified by the announcement of streaming WWE Raw starting next year, highlights the company's commitment to diversification and staying ahead of the competition.

Competitive Edge and Future Outlook:

While competitors in the streaming space grapple with profitability concerns and content cutbacks, Netflix ( NASDAQ:NFLX ) remains unwavering in its commitment to investing in a robust content slate. The company's refusal to pursue acquisitions of traditional entertainment companies or linear assets sets it apart in an industry undergoing significant changes. As Netflix ( NASDAQ:NFLX ) anticipates continued competition, its dedication to improving the entertainment offering signals a long-term strategy focused on capturing and retaining subscribers in an evolving market.

Looking Ahead:

Netflix's exceptional performance in Q4 2023 not only cements its status as a leader in the streaming industry but also underscores its resilience in adapting to changing market dynamics. With a record-breaking subscriber base, expanding revenue streams, and a commitment to innovation, Netflix ( NASDAQ:NFLX ) seems poised for continued success in the years to come. As the company navigates the delicate balance between subscriber growth and profitability, its strategic moves in advertising and gaming hint at a future where Netflix ( NASDAQ:NFLX ) goes beyond being a mere streaming service, evolving into a diversified entertainment powerhouse.

TKO Group HoldingsI'm making this just for kicks.

Fundamentals:

Netflix (NFLX) and TKO Group Holding's WWE announced new partnership early Tuesday that will bring WWE's flagship program Raw to the streaming service, beginning January 2025.

TKO's agreement with Netflix has an initial 10-year term for an aggregate rights fee in excess of $5 billion.

Dwayne 'The Rock' Johnson is joining the WWE & UFC parent company's board of directors.

Technicals:

I have a bullish D.B. with this asset. The weekly TF out of the four is bearish, and that can solely be due to price breaking through a key monthly high, which in turn would start the retracement, but not all the time tho!

I would like to see a deeper correction before price actually start to take off, and this current bull movement it's showing looks to be a small pullback before the bears reenter the market in order to push price further down.

We all shall see...

Netflix : Elliott Wave Analysis 🌊 In the aftermath of Netflix's Earnings Call, witness a remarkable 7% surge in after-hours trading!

The intricate chart unfolds the completion of the initial cycle in July 2020, marked by an expanded Flat and Wave II concluding around $165. Embarking on a new Wave (1), the chart showcases an engaging 5-wave structure to the upside.

Upon our analysis, the low of Wave 4 hints at an impulsive rise for Wave ((iii)), targeting a range between 227% and 361%. Anticipating stabilization around $575, the narrative continues with the formation of Wave ((iv)), paving the way for the final ascent of Wave 5. This strategic sequence defines the overarching Wave (1), setting the stage for a robust sell-off in Wave (2) before the next surge of streaming momentum. 🚀🎥