WHO, China and the United States give causes for optimism This week's news background is struggling to get the most out of the sad situation that the world has found itself in (over 850K cases worldwide and the picture is only getting worse). We are talking about the desire of the United States to increase the already unprecedented amount of assistance to the economy. The White House and the Democrats are preparing for a new package of measures if the peak of the epidemic does not pass in the coming weeks. And Trump, in turn, called for another $ 2 trillion for infrastructure projects to support the labor market.

The World Health Organization has done its part to increase optimism, saying the peak of the pandemic in Italy and Spain seems to have passed.

Another reason for moderate optimism gave China. The PMI index in March rose sharply from 29.6 to 52.3 (with a forecast of 37.8). What does this mean especially in light of the information that Wuhan will be unlocked next week? China gives a clear signal that tough measures against the epidemic can minimize the damage to the economy from a pandemic by limiting it to period of 1-2 months.

But the rest of the world is not China. This is evidenced even by the fact that China now occupies only 4th place in the pandemic race.

So it’s too early to relax. Analysts so far only worsen their own forecasts. A week ago, Goldman Sachs expected a decrease in US GDP in the second quarter by 24%, but yesterday the forecast was lowered to 34%. Plus unemployment is expected at around 15%.

So we are still considering the growth in the stock markets at the start of the week as a great opportunity for sales. The only thing to note is that we recommend to protect each sale with relatively small stops - it is better to take a stop, take a break and go again than go against the will of the market (an attack of optimism can be quite sharp).

Amid such news, gold suffered losses. But again, for now, this is just a reason for cheaper purchases — nothing more.

The oil market also experienced some relief. Trump’s call to Putin raised the hopes that the oil price war could end soon. Quotes slightly moved away from the lows. Actually, everything is going according to our medium-term plan, despite all the news that the price of Russian oil has reached its lowest level in the last 20-plus years, Goldman Sachs expects a decrease in global demand by 26 million barrels bpd, while IHS Markit believes that the price oil in April will collapse to $ 10 per barrel, which will provoke a reduction in world production by 10 million bpd.

Newstrading

Oil hits 18-year lows (time to buy), Fitch presses on the poundThe start of the week was surprisingly calm. Honestly, looking at the figures for the number of confirmed coronavirus cases in the United States (exceeded 160K) and Trump's return to reality (he decided to abandon the idea of full economic activity within two weeks), we expected a return to sales on the stock market and increased pressure on the dollar.

But this entire negative was absorbed but the oil. WTI prices reached the minimum values for the last 18 years. The current market sentiment in the complete absence of positive news continues to remain on the side of bears. In general, what is happening is logical: the economic crisis inevitably provokes a fall in commodity markets.

But the case of oil, in our opinion, is quite unique. The fact is that oil collapsed before it became clear that we were dealing with a global economic crisis. This refers to its epic drop of 30% following the OPEC+ gap. That is, oil has exhausted its reasonable potential for reducing in advance. Now oil has to fall below reasonable limits due to general pressure on commodity markets.

Our medium-term trading position for oil yesterday was finally formed. We added to the already opened purchases the last long position opened near $20. Recall that the motivation for this trade is that current prices are already below the average costs in the market, which means that oil is doomed to rise in perspective. It may take months, but ultimately, the price of oil should return to its fair value.

Let’s get back to the other news. Fitch rating agency downgraded the UK sovereign debt rating from AA to AA-, justifying this by a sharp increase in the country's debt, as well as uncertainty with trade negotiations with the EU. Our position on the pound is twofold. In the medium term, in our opinion, his chances of growth are good. But here and now (this week) we are likely to sell the pound against the dollar, at least until the GBPUSD is below 1.25.

Dooms day clock is ticking out. According to most experts, if there will be no turning point for the better in the next few weeks, the world will almost certainly plunge into a deep global recession with all the sad consequences.

In this regard, we recall our recommendation to buy gold. The goal of the current movement has not yet been achieved (we are talking about a re-test of 1700), so this week the growth of asset prices, in our opinion, should continue.

Week in a glance: not a day without records, our positionsEach new week is trying to be even more eventful than the previous one. And so far, in general, it turns out. At least judging by the last week.

The week began with optimism caused by the approval by the Senate of record aid from the US government. Its size exceeds $ 2 trillion, which is unprecedented cases in the history of mankind, and not just the US. In this light, the growth of US stock indices is generally justified and logical, especially if we recall the Fed's zero rates and an essentially unlimited program of quantitative easing. Here, we have another record: the growth of US stock indices on Tuesday became the biggest since 1933. According to experts, the Government and the Central Bank in total are ready to pour in US economy up to $ 6 trillion ($ 2 trillion + $ 4 trillion).

The main problem with the current growth of US stock indices is that it is only temporary. Last week will be remembered by another records, but this time with a “-” sign. For example, the United States has become the world leader in the spread of the epidemic. It takes only 2 weeks. Given the pace of the epidemic in the United States, its economy runs the risk of massive damage. Actually, analysts are already talking about it: at Goldman Sachs expect a drop of 24%, and Morgan Stanley - by 30%. The President of the Federal Reserve Bank of St. Louis, James Bullard, expects a fall in GDP by 50% (!) with unemployment at 30%.

Weekly data on initial jobless claims in the United States confirmed the most pessimistic forecasts. The indicator grew by almost 3.3 million (!). This is an absolute record for the entire history of observation, which is also almost 5 times higher than the previous anti-record.

So the worst for the US economy is yet to come. This means that the stock market is doomed to a further fall. That is why current growth is just a great opportunity for sales.

The next candidate for sales is the US dollar. The largest economic loss in history is not a reason for the growth of its national currency. The dynamics of the dollar last week confirmed this. But the most interesting thing is that the dollar has just begun to move away from the maximum levels, so sales from current prices look like a fairly promising deal. Therefore, we sell the dollar. First of all, against the Japanese yen, in order to further participate in the purchase of an asset-refuge (we are talking about the Japanese yen).

Considering that panic in the financial markets, despite all the measures of governments, remains at the highest levels since the global financial crisis, gold purchases remain another promising idea. Actually last week the asset showed what it is capable of. In just a couple of days, gold rose by more than $ 100. Again, this growth is not yet complete. The re-test 1700 seems to be the inevitable and only logical scenario. But even this peak is most likely not limited to. The further goal is 1800, and there already before 2000 it will be at hand. So we buy gold, there have been no more ideal conditions for its growth for many decades (if at all there have been 100 in recent years).

Another interesting result of the week was the formation of the bottom in the oil market. Despite all the negativity that prevails in commodity markets, oil has clearly exhausted its downward potential. This is logical, current prices are already either lower (USA) or at (Russia) cost price. Vivid evidence in favor of this was the maximum decrease in the number of active oil installations in the United States over the past 35 years (hello another record). That is, current oil prices are indeed below cost. The curtailment of production will lead to a drop in supply in the oil market, which in turn will provoke an increase in oil prices in the future. So there’s basically nowhere to drop oil. This means that oil remains a fairly promising medium-term position in itself and will serve as a hedge for sales in the stock market. OPEC+ is going to end this week. But what if: “The king is dead, long live the king”.

Invisible war and the worst forecasts come trueOn the one hand, it’s nice when your forecasts come true (we mean our recommendations to sell the dollar this week), on the other hand, you can’t be happy with the reasons that ensured the implementation of the forecasts. The epidemiological situation in the United States continues to deteriorate rapidly. New York risks becoming a ghost town. In just 7 days, 18,000 cases of coronavirus were diagnosed in the city. On Wednesday, the number of calls to 911 rescue service reached historic highs, which had previously been recorded on September 11.

Data on initial jobless claims justified the forecasts of pessimists: an increase of almost 3.3 million. This is a complete failure even against the background of growth forecasts of 1-1.6 million.

In general, everything is bad. And trillions of dollars can’t change this fact. So today we will continue to sell the dollar. The growth of the pound by 700 points over the current week against this background seems quite logical and we expected it when no one wanted to buy it at 1.16. The decision of the Bank of England to leave the rate unchanged did not surprise anyone or scare anyone. By and large, everything that the Central Bank wanted to do, it did at an extraordinary meeting.

But let’s get back to the problems of the world economy.It not know such a tough and swift landing not during the global financial crisis, not during the oil embargo of 1973, and not during the Great Depression. Even the Second World War did not inflict such a strong and sudden blow on the global supply chain (the largest port in the world - Shanghai - in February reduced the volume of activity by 20%, and the volume of imports to the USA from China in the first two weeks of March decreased by 45% ( !) - this has never been happened before). In fact, the global economy is now in a position as if there is a world war. With one exception, there is no war.

So the growth of US stock indices is an opportunity for sales and nothing more. By the way, a good opportunity, given the scale of growth from local lows.

And finally, recall our recommendation to sell the euro against the Japanese yen. The details of the new program of quantitative easing from the ECB were announced yesterday (we are talking about 750 billion euros) - in fact, the Central Bank can buy any number of bonds from anyone.

2 trillion reasons to calm down and 3 million reasons to worryThe main event of yesterday was the approval by the US Senate of an emergency $ 2 trillion emergency plan. The plan provides $ 1,200 direct payments to low-income Americans, $ 500 billion will be provided in the form of loan guarantees, $ 350 billion will be used to help small businesses.

Against the background of this information, the markets perked up a bit. But for now, we see no reason for global repositioning. The pandemic is in full swing, the damage from it is measured in tens of percent of GDP, so we will use any increase in stock indices for selling shares.

After all, things are bad. New York is becoming the center of an epidemic in the United States and is under siege. California (a quarter of the US economy) may remain in the lockdown for another 8-12 weeks. India is quarantined for three weeks. Great Britain closes Parliament. So repositioning is still very premature.

In addition, today markets will face one more challenge: US jobless claims. A number of experts voice fantastic 3 million initial jobless claims (the average figure recently has been 220K). Recall that the most significant jumps in the indicator were about 8 years ago during the hurricane Sandy. But even then the number was less than 281K (this value was recorded last week). That is, 3 million claims against this background look as terrible and scary as possible.

So dollar sales are still relevant today. Recall that the Fed is ready to make an unlimited injection of dollars, which is a threat to the dollar # 1.

In the oil market, meanwhile, there is an active undercover fight. Nothing is known about its actual results. But, in our opinion, a telephone conversation between US Secretary of State Mike Pompeo and Crown Prince of Saudi Arabia Mohammed bin Salman is very revealing. The Trump administration is clearly trying to persuade Saudi Arabia to abandon the plan to dramatically increase oil supply as part of a price war with Russia

Pandemic in progress, Wuhan is waiting, but Trump can't wait The pandemic is in full swing and there are no positive trends around the world. The epicenter remains in Europe. And if yesterday we talked about possible losses of the US economy, today we will give a couple of figures for Europe. According to Goldman Sachs analysts, Italy’s GDP will drop by 11.6% in 2020, Spain - by 9.7%, Germany - by 8.9%, and France - 7.5%. In general, the Eurozone will lose about 9% of GDP. In this light, we recall our recommendation to sell the euro. But not against the dollar, we recommend to sell it against the British pound and the Japanese yen, that is, we sell EURGBP and EURJPY pairs.

This recommendation is confirmed by the March indexes of business activity from the Eurozone, Germany and France. All of them came out significantly worse than already pessimistic forecasts. For example, the composite Eurozone PMI for March was at 31.4 (!) mark with a forecast of 38.8 and a February reading of 51.6 (!).

However, the leadership of the Eurozone in the pandemic race is disputed by the United States. We already wrote that by the end of the week, the States may well catch up with Europe, especially if Trump realizes his promise to open the US as soon as possible.

That is why we do not recommend selling the euro against the dollar, because we consider dollar sales themselves to be a good trading idea in the light of everything that is happening now in the world and the USA in particular. We sell primarily against the Japanese yen. Do not forget to buy gold on the falls.

But there is some optimistic information as well. We mean the news that the capital of the Chinese province of Hubei Wuhan will be open on April 8. That is, China gives us a specific time marks for the duration of the epidemic. Of course 3 Chinese months may well be equal to six months in Italy or the United States, which have not even reached the peak of the epidemic. But you can still begin to prepare for the fact that soon the worst will be behind.

In this light, let us recall our medium-term oil deal (buy oil). Yes, here and now there are no actual reasons for purchases, but if you act in advance, then you can act just right now.

However, at the rumor level, there is information that the United States and Saudi Arabia can create a new alliance in the oil market and agree on coordinated actions. In addition, US oil companies are trying to gain support from the Government to ensure survival in the current environment.

Speaking of support, the amount of assistance to the economy from the US authorities can reach $2 trillion. As a result, yesterday for some time optimism gets back to the US stock market. But it's too early to talk about purchases. On the contrary, we use these growth attempts for sales.

Fed is breaking bad, analysts spread panicThe main news yesterday was the Fed's announcement of a number of programs to support the economy and financial markets. We will not list them all, because the main thing is not even that. The key thing is the fact that for the first time there are no restrictions on the amount. This support is not for $100 billion, or $1 trillion. This is conditionally infinite amount. That is, the printing press is turned on full and whatever happens.

Judging by the reaction of the stock market, investors took this news quite restrained. This means that the market sentiment is still bearish, so we will use any rise in stock prices as a reason for sales.

We believe that the short-term effect of such actions by the Fed will probably be positive for economy, but in the future these are very dangerous steps. The United States in the coronovirus race has already broken into third place and at such a pace country can finish this week if not in first, then in second place.

In addition, analysts compete whose forecast for the US economy in the second quarter will be worse. Goldman Sachs, for example, expects a drop of 24%, and Morgan Stanley - by 30% in US GDP for the 2-nd quarter. But the most scary was the President of the Federal Reserve Bank of St. Louis, James Bullard, who expects a fall in GDP of 50% (!) With a simultaneous increase in unemployment to 30%.

As the result we recommend to sell the dollar (first of all against Japanese yen), as well as to buy gold.

Italy, meanwhile, tightened quarantine measures even more, which led to an almost complete halt of industrial production in the country. In this light, we remind about our recommendation to sell EURGBP. Although it is worth noting that the decision of Germany to provide assistance to the economy in the amount of 750 billion euros may well have a positive effect on the euro. But in this regard, it is better to buy the euro against the dollar.

Of our other positions, we keep on recommend medium-term oil purchases. Motivation: the current force majeure for the oil market, in our opinion, has created a rather unique, but temporary situation. Unique because of the scale of the price drop due to the simultaneous negative impact of a drop in demand (the coronavirus epidemic and the economic consequences of it) and a sharp increase in supply (the actions of Saudi Arabia). But both of these factors are temporary. China has shown that the epidemic (at least its active phase) is rather limited in time and even provided guidance on the duration of the extreme phase - a couple of months. The position of Saudi Arabia is more like an exponential gesture, the purpose of which is obvious - to increase the level of Russia's compliance. With all the bravado, not one of the key oil producers is satisfied with prices near $ 20, which means that there will be an agreement sooner or later. We also note that so far, in fact, production has not been increased significantly. According to Reuters, Saudi Arabian exports totaled 7.3 million barrels per day in March, not 10 million barrels threatened by the Saudis. Thus, it is only a matter of time before the drivers of lower oil prices converge on oil and change their direction of impact from south to north.

Are we on course for another bitcoin panic?As we all know, investors are panicking, which is driving SPX and OIL to see insanely low prices. Those panics are not exclusive to the main markets, I believe that crypto will follow soon.

Bitcoin remains around 5k, and it might for another couple of days before I believe we will see another major panic sell. We are definitely in a bearish market right now and it would not make much sense for bitcoin to be bullish.

I would advise you to trade with lower amounts of money and use leverage wisely as these times are really uncertain and markets can either dump or rally at any day, we can only try to assume the future but we will not be able to predict, for that reason, I will ask everyone to remain reactive to the markets and if you have a position open please continue monitoring the major indicators and reading the news, as anything can happen now.

ECB promises almost trillion, Trump wants even moreChaos and anarchy are still there in the financial markets. Although even in this chaos, elements of order can be found and money can be made from them. Our yesterday's recommendation to sell EURGBP evidences in this favor. After madness on Wednesday, yesterday everything began to return to their places and more than compensate previous losses.

The reason for the sale of the euro on all fronts was the results of an emergency meeting of the ECB. European Central Bank decided to provide a new program of asset repurchase of € 750 billion.

Trying to keep up with the Europeans Trump offered a $ 1 trillion aid package.

The Bank of England looked good even against this background with its rate cut to 0.1% and the expansion of the quantitative easing program to $ 750 billion. As a result, pound volatility was extremely high on Wednesday.

What else unites Europe and the USA? The simultaneous closure of factories, which has become the largest since World War II. So for those who think that the worst is over, we have bad news.

The Swiss National Bank (SNB), meanwhile, shows what needs to be done in order to prevent an excessive strengthening of the national currency: instead of the usual rate cuts or quantitative easing programs, he resorted to good old currency interventions.

Why SNB experience is interesting here and now? We have already noted that the dollar has strengthened too much. This is bad for the US economy especially right now. The Fed rate cut to 0% did not work. Flooding the repo market with money does not help. Actually, only currency interventions remained as the options to stop the growth of the dollar. Meanwhile, the number of cases in the United States doubled yesterday (!), And this is an excellent reason for panic. We mean that we are preparing for a dollar reversal and are beginning to slowly sell it primarily against the Japanese yen. Sells in the US stock market are still our best trading idea of the year.

Of the other promising positions that we expect to shoot in the foreseeable future, oil purchases continue to be.

Dollar dominates, governments act, RAs downgradeThe dollar continues to dominate in the FOREX. The secret of his success is simple - the increased demand for U.S. Treasury bonds during the crisis, high liquidity of the dollar, as well as the relatively good situation in the U.S. economy, coupled with measures to support it and the current epidemiological situation in the country comparing with the other problem currencies (Euro, pound, commodity currencies).

Anyway, the Dollar Index has reached its highest level since 2017 and, on the whole, looks rather overbought. That is, with his purchases one should be careful and more selective.

The optimal trading tactics for today, in our opinion, is active trading based on the signals from oscillators. Moreover, we recommend using not the classic RSI or Stochastic, but our author's Ranger, since now it is critical to understand where specific pair can go in terms of absolute price values. So today in the FOREX we will both buy and sell.

The pandemic, meanwhile, continues, and problems in the global economy continue to grow like a snowball. And this week the worst is beginning to happen - rating agencies have started to downgrade ratings. This is extremely alarming, because after the blowing up of the stock market bubble (from which greedy investors will mostly suffer. Which will be exclusively their own problems in some way even deserved), the corporate debt market bubble will begin to collapse. This topic is much more serious and potentially more destructive for the global economy. The word default can become very typical in the news.

In general, there is no reason to take a breath. This means that purchases of gold and other safe haven assets continue to be relevant, as well as sales in global stock markets.

It should be noted that in the fight against the crisis the Central Bank, have already largely spoken their words and now it is the turn of governments. That is, we are moving from monetary measures to fiscal stimulus. The White House is preparing to help the US economy for $ 850 billion. France prepared a package of measures for $ 335 billion, Germany for $ 500, etc.

As for our favorite positions for today, this is without a doubt the sell of EURGBP. We will talk about the motivation for this deal in a separate report, which we will publish today later.

Crazy week behind but it's too early to relaxLast week showed as clearly as possible how bad things are now: the crisis is not just a word, but a reflection of sad reality. The Fear Index has reached highs unseen since 2008. Once again: so high it rose only at the peak (!) of the global financial crisis 2007-2009. Is this not the best illustration of how bad everything is?

Italy went into complete lockdown, and other countries followed it, albeit in a milder form. For the Italian economy, this is, if not the end, then a very strong blow. This is the third largest economy in the Eurozone by the way.

Today China has already confirmed alarming fears - the economy suffered a severe blow: industrial production in February fell by 13.5%, and retail sales by 20.5%. As the result everyone suddenly remembered about the safe haven assets again.

So there is nothing surprising in the fact that the ECB has expanded the program of quantitative easing, and the German government promises emergency economic assistance ( more than $500 billion). To understand how much is it lets compare with GDP: this is about 15% of the country's GDP. Measures of this magnitude were not even during the crisis of 2007-09.

The Bank of England at an extraordinary meeting lowered the rate. The Fed expects rate cuts to almost 0% this week.

In general, we are now in the midst of a crisis. And it is not the fact that the worst is over. A pandemic is developing exponentially. Each new day of the epidemic increases the amount of economic impact.

So the upcoming week could be another test. Moreover, on Wednesday the Fed will announce its decision on the parameters of monetary policy. On Thursday, the Bank of Japan will say its word. In addition, there will be quite a lot of macroeconomic statistics.

How to trade in such conditions? For beginners, we would recommend just watching from the side. Otherwise, everything can end extremely sad. For those who are ready to compete with the markets, we recommend expanding the boundaries of the concept of “impossible” as far as possible in terms of the size of daily price fluctuations. Given how dynamic everything is, you can try to trade based on the signals of oscillators - intraday prices constantly rebound by more than serious values.

As for the general directions, given how bad everything is now in Italy and Europe as a whole, we will sell the euro. Moreover, this week we will not do this in pair with the dollar, which itself may be under attack if the Fed takes extraordinary measures, but against the yen and the pound, that is, we will sell EURJPY and EURGBP pairs.

Intraday you can sell oil, but at the same time, we note that in the medium term we have already bought oil (WTI) at $ 30. This is part of a big “buy” plan that involves adding at $ 25 and $ 20 to a super-position.

In addition, this week we will buy gold. It generates great entry points and it’s a sin not to use them. The only thing for positions in gold is the tactics of multiple trades based on small stops. That is, we put small stop-losses on long positions, if they are executed, we wait for a while and restore buy when the movement calms down. Standing against the gold market in the current conditions may be suicidal, but jumps after stops will allow you to control what is happening. And the overall prospects of the position will ultimately allow to beat off all the stops and be in the plus after all.

The crisis as it is: Trump, the Fed and the ECBWhat happened yesterday in the financial markets is on the one hand (from the position of normal price dynamics), was extremely atypical, and on the other (for markets during the crisis) it was quite natural.

On such days, traders either become rich (rarely) or lost their deposits (as a rule). It is better for beginners and even experienced traders on such days to stand aside, because there is very little logic in what is happening, but there are a lot of strong movements.

Of course, one can try to discern order in this chaos. But observation from the outside without involvement in trading allows you to maintain a more objective perception of reality.

Actually, everything is developing according to the scenario that we have voiced since the fall of last year. A critical mass of prerequisites for the crisis was on the table, and it was only a question of a trigger. The coronavirus epidemic has become this cause and now we are dealing with the consequences.

Now everything comes down to answering one question, whether it will be possible to localize the epidemic and when (judging by the data from China, the time frame will more or less clear - it will take about 2-3 months to solve the problem, if real efforts will be provided to solve it), and how long the crisis will last (if the epidemic will be localized within a month or two, then the first half of the year will be a failure, but recovery will begin in the second part of the year).

Central banks, meanwhile, are going to habitually fill the markets with money. In particular, the Federal Reserve Bank of New York announced its intention to conduct repo market transactions totaling more than $ 4 trillion. The US stock market reacted to this with fall. This is a very bad signal for those who still buy there. Recall that since the fall of 2019 we have warned that the bubble will burst.

The ECB did not lower the rate yesterday, but approved new incentive measures. We are talking about expanding the quantitative easing program: the volume of additional net asset purchases will increase by 120 billion euros. That is, the fire of the crisis will be flooded by money. It is very symptomatic that even in conditions when other central banks emergency reduce rates, the ECB cannot do this even in the midst of a panic in the markets. That is, the current rate is the limit.

Trump announced yesterday a ban on travel to the United States from 26 European countries for a month.

The oil market was relatively calm yesterday. Relatively in terms of price, not in terms of news. The oil war is in full swing. And the object of attack of Saudi Arabia is becoming more apparent. This is not the United States and its shale. It's Russia. Riyadh is ready not only to dramatically increase the volume of oil supplies to Europe, but also to offer customers a good discount. European oil refineries, including Royal Dutch Shell, BP, Total, OMV, Repsol and Cepsa have already reserved supplies of Saudi oil, the volume of which exceeds the usual by 25-200%.

Considering how chaotic and dynamic everything is now, today we plan to trade exclusively actively, but with mandatory stops. We will give preference to purchases of the dollar and gold. But this does not mean that in moments of strong overbought, we will not sell it. That is, today we monitor the oscillators and trade according to their signals.

But what if the markets are wrong: lets fish in troubled watersThe start of the week plunged many into a state of deepest stupor. Over the past six months we have already devoted dozens of reviews preparing our readers for the onset of global problems and the collapse of bubbles in risky asset markets.

The most wrong thing a trader can do in such a situation is to lose an adequate perception of reality and rush into the pursuit of the market. We urge our readers to remain calm and analyze the situation as openly as possible.

Let’s take as example the oil market. Yes, here and now the situation looks completely hopeless. But by and large, all this we already seen in 2014. Situations, of course, are not identical, but in many ways they are similar. So, we can try to draw historical parallels and predict the future development of events and market prices. What happened when the last time oil prices went below $ 30 (WTI)? By the will of the key oil market participants, the current reality at that time was changed (meaning the signing of the first OPEC + agreement).

Actually, here and now everything can be repeated. It is not so difficult to imagine the situation of the OPEC + emergency meeting already at the end of this or next week, at which Russia agrees to cut the production and the situation will turn upside down. Given how dependent the Russian economy is on hydrocarbons, this is the only reasonable option for a country if it does not want to become a second Venezuela.

That is, banal logic suggests that selling oil at current prices is a very risky thing. But purchases, on the contrary, are promising.

Similar thoughts can be presented for the US dollar. Beating of USD in the FOREX, given the current form of the US economy and other countries is undeserved. Yes, the Fed has already lowered the rate, and the ECB has not yet, respectively, the rate differential has narrowed, but it is still in favor of the United States.

At the same time, new historical lows on the yield of US treasury bonds indicate that demand for dollars is not falling, but, on the contrary, is growing. That is another logical contradiction that makes us think that the markets are wrong.

The experience of the year 2008 shows that the insanity into which markets plunge headlong is a relatively short-term phenomenon. And ultimately, common sense returns. We have no particular doubts about this. The only doubt is timing. That is, when everything returns to norm.

Of course, go against the market without stops, trying to impose your will, is potentially a margin call. But at the same time, following your line without fanaticism and with reasonable stops will make it possible in the end not only to catch a local correction, but to be at the origins of a big movement.

That is why today we will continue to follow our basic plan: sell EURUSD, buy USDJPY with simultaneous purchases of gold (all positions with hard and rather short stops), sell in the US stock market, and sell the Russian ruble as well.

Fed`s surprise, coronavirus chronicles, ADP numbersThe main event of yesterday was the Fed’s decision to urgently reduce the rate by 0.5%. The central bank did not wait on March 18 and caught many by surprise. The reaction of the financial markets as a whole seemed logical: the US stock market went up, the dollar was falling, gold was growing. The whole question is whether these trends will continue. We practically do not doubt gold and put on its further growth. The US stock market may well grow by a further wave of optimism by a few percents. But the closer he gets closer to historical highs, the stronger will be our desire to sell. The dollar will be able to take revenge on Friday, but more on that below.

In the meantime, we traditionally continue to review the news from epidemic fronts. The epidemic in China has virtually disappeared (130 new cases), but in the world, everything is in full swing (almost 2000 new cases per day).

G7 countries, meanwhile, held an emergency meeting at which they firmly decided to confront the economic consequences of the epidemic.

Inspired by this news, as well as information about a possible massive easing of monetary policies around the world (the Central Bank of Australia also lowered the rate yesterday and thereby confirmed reasonable expectations), investors again breathed a sigh of relief and rushed to buy cheaper assets. We traditionally do not share this optimism and consider it clearly premature. The consequences are just beginning to manifest. So in the next month, depressing news will be enough.

On the foreign exchange market yesterday there was a certain return of common sense. In terms of the fact that the euro stopped growing at the end of the day (even against the background of information about the Fed’s rate reduction of 0.5%), the pound seemed to have found some ground under its feet. All the attention of traders is focused on the first rand of trade negotiations between the EU and the UK. The results will not be earlier than Thursday. So far, we generally consider all this to be nothing more than noise, which can only give the best entry points. Really, nothing will be solved now, which means you should not worry about anything. Recall that our position on the pound is medium-term purchases. Justification - The EU and the UK will eventually be able to agree again.

As for the euro, it seems that there was a less clear explanation for its growth in recent days. In addition to the classic for almost any strong movement of triggering stop loss and buy-stop, analysts call the curtailment of the trade due to the coronavirus epidemic as the main reason for the sharp strengthening of the euro against the dollar. For those who are not in the know, we explain that the ultra-low rates in the Eurozone made it possible to borrow money there and invest them in markets with higher returns (for example, the USA). Which naturally led to a depreciation of the euro. Curtailment is marked by opposite trends, respectively, the euro strengthened. Rumors that the Fed will sharply reduce the rate in March and may reduce the rate even later in 2020 provoked the start of the process of curtailing the trade, which was especially clearly reflected in the EURUSD pair.

News about the epidemic has recently monopolized the information space so much that it’s easy to miss important news that does not have the word coronavirus or something like that in the headline.

We mean that on Friday statistics on the US labor market will be published. This news is traditionally one of the main ones for financial markets. Considering how sensitive markets are now to any deviations from the norm, these data are of increased importance. But the numbers on the NFP will be published only on Friday, but for now, today we are waiting for data from ADP.

ESPR expect further downsideI just started playing with FDA approvals using my pendulum. I don't see anything good coming out of this news event other than a bounce to sell into.

Symmetry support is $57.15 held once. Will it twice??

If it doesn't hold this 786 fib (53.99), the door is open to $40.

BXRX FDA approval lotto playThis idea comes from recent success in a Sprint trade. It was slow in coming, but it did come through very successfully, which is the impetus for this idea of "reading" tickers with binary events.

This is purely a news driven idea in which there is no technical reading of the chart what-so-ever. I have no idea if this will be correct, and am really using this platform for journaling & finding others who use similar methods. I'm getting the tickers from a freely available online calendar with the PDUFA dates.

I use a pendulum and cards I made up to gain information on the "energy" of the situation. Anyone doing anything similar, please contact me to share information. I'm definitely on the fringes here.

BXRX has a deadline for an FDA approval tomorrow (2/20/20).

My indications are that it is APPROVED. I don't read about the details of the application and I don't care, although reading it may help my insomnia ;)

BXRX is currently trading at the LOD $7.88 - 5.97%

Indications are it could go up to $9.14

The ATH is $9.60

We shall see...

LLY Sell the RallyMy dowsing method suggests LLY gets their FDA approval, and the stock will pop, but that in the longer term, this stock is going to breakdown; probably with the entire market.

I'm getting that the resistance will be around that $145-46 zone, which would also be a test of the uptrend line from below. Good luck!

EURNZD Post news trade set-up + 100 Pip PotentialWe had a good push down on the NZD Interest Rate decision and this pair has now gone into a consolidation between 1.6941 (High) and 1.6857 (Low). Moreover, it is now below the Daily, 60 and 15 min KS, as well as the 15 cloud.

Entry = 1.6920

Stop = 1.6940

Risk = 20 pips

Profit target = 1.6820

Reward = 100 Pips

RRR = 5-1

Once this trade is up + 20 pips, move your stop to breakeven and let it run.

I would appreciate if you leave a comment or like as a thank you.

Allen

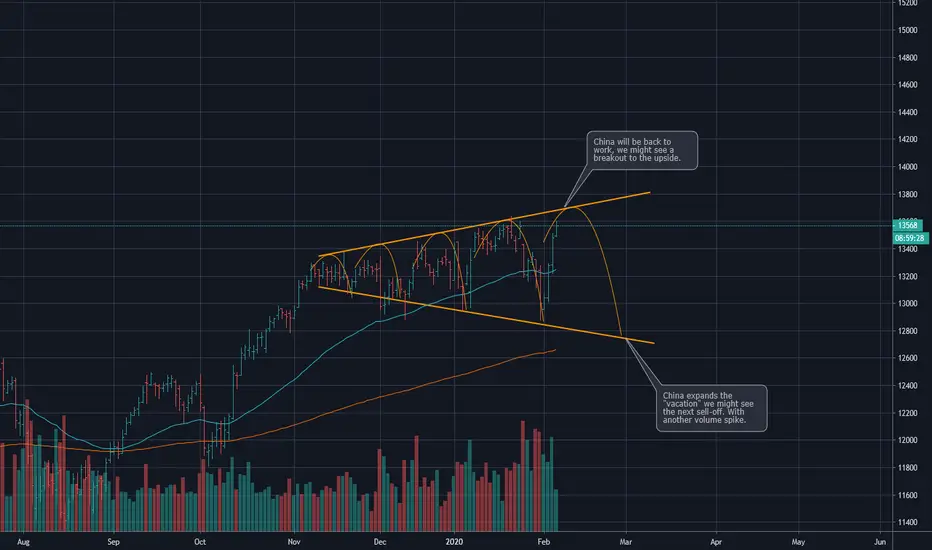

DAX: What if China is not back to work on MondayRight now, we have a broadening formation in the DAX; this usually happens, when the market in disagreement. On the upside this lead us to 13,720, but what would happen if China is going to extend the "vacations" by another two/four weeks. For German manufacturers this would lead to an demand shock, since a lot of German manufacturers are heavily involved in the supply chain of Chinese companies (via JV).

So, what do we see:

Higher volumes: Cash-Market and Future volumes (Source: deutsche-boerse-cash-market)

Trumpet (starting in Nov. 2019 - Feb. 2020); disagreement in the market

Short signal: Hindenburg-Indicator

Short Signal: MACD weekly

Upper end of the trend channel

Event would affect the cashflows of German companies (for at least this year)

My trading plan depends this time on the news which we will get within the next couple of days.

If we see an extend of the "vacation", I expect another sell-off, which could lead us to the EMA 200 daily.

EURAUD Post News Trade Short + 100 Pip PotentialWe had a good push down on the AUD Interest Rate decision and this pair has now gone into a consolidation between 1.64752 (High) and 1.64418 (Low). Moreover, it is now below the 60 and 15 min KS, as well as the 15 cloud.

Entry = 1.6474

Stop = 1.6494

Risk = 20 pips

Profit target = 1.6374

Reward = 100 Pips

RRR = 5-1

Once this trade is up + 20 pips, move your stop to breakeven and let it run.

I would appreciate if you leave a comment or like as a thank you

Have a great week!!

Allen

ECB strategy, record pessimism amid record greedYesterday, the ECB expectedly left the parameters of monetary policy in the Eurozone. This was predictable, so most were interested in the new strategy of the Central Bank. But Lagarde greatly disappointed the markets, saying that before November-December, one could not count on any clarity in this matter.

Thus, the euro will not have to rely on support from the ECB in the foreseeable future. So the decline in the single European currency was quite natural yesterday. Not even Lagarde’s remarks on the fact that moderate growth was observed in the European economy did not help.

In general, the euro continues to look attractive enough for sale. Increase pressure on the euro and sales in the EURJPY pair, which we recommended selling the pair when it was quoted above 122.

PricewaterhouseCoopers recently announced the results of a survey of heads of major world companies. We have already analyzed the results of a similar survey from Deloitte and note that PWC confirmed the previous results: the business is experiencing record pessimism since 2009. Only 27% of company heads expect improvement in the economy. Most expect a slowdown in the global economy. Characteristically, the most pessimistic leaders in the United States. Which once again convinces us of the correct course on sales in the US stock market. Meanwhile, the fall of the Chinese Shanghai Composite Index by 2.8% on the last trading day before the lunar New Year, was the largest drop in eight months.

Naturally, with such a level of pessimism, purchases of safe-haven assets look great. So today we will continue to look for points for buying gold and the Japanese yen. Again, the epidemic in China is in the process of development: the second large city, Huanggang (population about 11 million people), has been closed for entry and exit. Railroad interrupted with the city of Ezhou.

Friday promises to be a rather volatile day. Data on business activity indexes for the Eurozone and selected European countries, as well as the UK and the USA, coupled with statistics on retail sales in Canada, practically guarantee that it will not be boring.

UK labor market gives the BoE's room for maneuverThe main event of yesterday in terms of macroeconomic statistics was the publication of statistics on the UK labor market. The data pleasantly surprised. Recall that we expected rather weak statistics - the British economy has been painfully unconvincing in recent times.

Nevertheless, the UK economy for three months until November created 208K new jobs, which is almost 2 times higher than analysts' expectations. The average weekly wage also came out better than expected (+ 3.2%).

Against the background of such data, supporters of the fact that the Bank of England will lower the rate at the next meeting sharply fell silent. Indeed, data on the labor market show that the Central Bank has no reason to rush. This sharply increased the chances that the bet will be left unchanged. The pound, of course, reacted positively to statistics and a shift in market expectations.

Recall in this regard to our recommendation to buy a pound on the slopes.

In general, for Europe yesterday was a good day. Indices from the ZEW Institute came out very good (relative to past data) both in the Eurozone as a whole (the expectations index came out almost 2 times higher than in December) and in Germany (the expectations index was +26.7 with a +15 forecast). So the growth of the euro looked quite natural. But for its continuation, this impulse will be clearly not enough.

In this regard, Thursday looks more promising: on this day, the ECB will announce its decision on the monetary policy parameters in the Eurozone. But we'll talk about this in tomorrow's review.

And today, the main event will be the announcement of the Bank of Canada’s decision on monetary policy parameters. Experts do not expect any changes. We are also inclined to believe that the bid will be left unchanged. But given the general trends in the development of the global economy in general and in Canada, in particular, there are risks of a rate reduction. Moreover, the reduction potential is far from exhausted, unlike the ECB or the Bank of Japan. Considering that the USDCAD pair has been treading water for two weeks now, fluctuating in the range of 50 points, there is a possibility of a strong movement in pairs with the Canadian dollar today. Moreover, the direction of movement is not obvious. Our recommendation in this regard is to work along the way. That is, if the pair goes above 1.3090 - we buy, if below 1.3020 - we sell.

Central Banks week and the IMF head expects a crisisMonday turned out to be a fairly calm day for financial markets. The reason on the surface is a day off in the USA. So today it will almost certainly be more volatile and interesting.

The Bank of Japan set the pace to the news background early in the morning. Monetary policy parameters were left unchanged. The press conference will be somewhat later than the publication of this review, so if any interesting details come up, they will talk about them tomorrow.

Today will be interesting statistics on the UK labor market. Considering how disastrous the data on the British economy last week was, one should not expect any positive. Nevertheless, we continue to believe that Brexit is the main driver of the pound, and statistics in the current reality can lead only to local movements. Accordingly, weak data, of course, will provoke sales but are unlikely to lead to the formation of a trend. This means that purchases in intraday oversold areas remain relevant to us.

Let's get back to the events of yesterday. Perhaps the most significant was the opening of the oil market with a gap up. The reason is concerns about the supply on the market. The fact is that Iraq and Libya drastically reduced oil production. In Iraq, because of protests, in Libya, because of armed groups that blocked the pipeline. And although it is very likely that these force majeure are temporary, we recall our recommendation to buy oil, which continues to be relevant in the current conditions.

We also continue to be supporters of the impending crisis, or at least the strongest correction in the US stock market. So it was nice to note the replenishment in our ranks. The head of the IMF, Kristalina Georgieva, in her last interview, compared the current situation to what was happening in the world on the eve of the Great Depression. A key common feature of the 1920s and the present situation is excessive financial squandering. According to the head of the IMF, depression cannot be avoided. The whole question is only in time.

In this regard, we recall our recommendations on buying safe haven assets (gold in the first place and Japanese yen in the second), as well as the “trading idea of the decade” - in the sale of shares of high-tech companies in the US stock market.