GRUB - Quick dip to $68, before the jump off to $282 by NYSE:GRUB certainly headed higher, but that C wave has to complete first. my best guess is the golden pocket, the 618. But once past this pothole, ohhhhh boy the fun starts.. I got 161.8% of primary Wave 1, off the “estimated” end of Wave 2... COMING IN HOT $282, The Last Jedi Leap Call Options..

The price awakens December 2019..

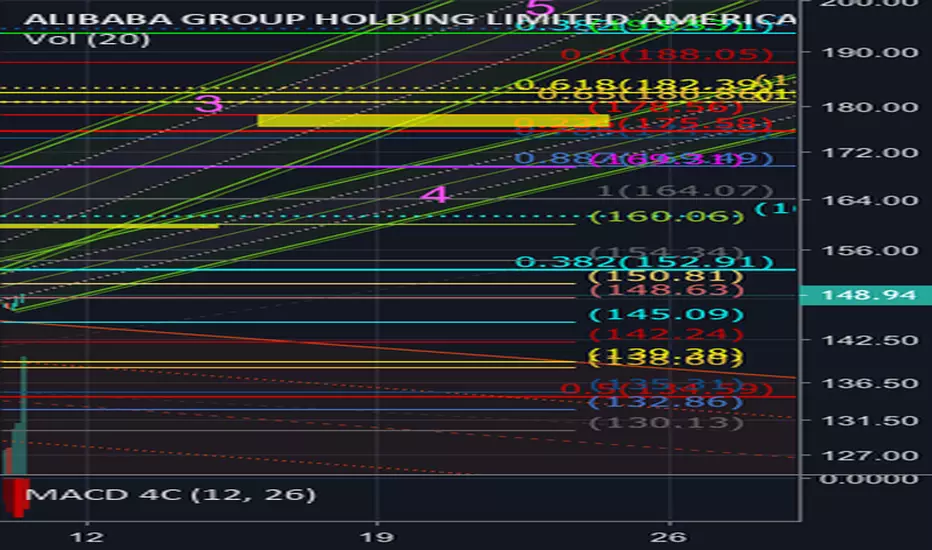

Options-strategy

BABA $160 Options-Light traffic aheadso now there a fall five weave pattern has been completed, technically we have to correct which typically would bring you down to the 50 or to the 618. So by drawing a pitchfork to wear the football is headed I could still estimate that $160 target to be hit prior to the December 14 expiration... I’m on showing a 187% profit if it hits, here’s the link to Options PROFITS calculator, it’s dope. but these deltas ABSOLUTELY change as soon as stock crosses above the 382. Same thing happened w AMZN last week.

opcalc.com

Soon as it crossed above $1696, ZZZOOMM ZZOOM that thing took off.

The Delta went FROM 0.31, to 0.62, to screen shots, couldn’t believe it.

KSS - Neutral Iron CondorThe stock price broke out from a range, made what looks like a head-n-shoulders pattern, and can mirror the channel pattern it made before the head-n-shoulders. Volatility is high and this is a neutral directional bet on the price action.

47.5/50/77.5/80 JAN19 IRON CONDOR @ 0.45 CREDIT

General plan:

Roll if necessary & if possible to reduce risk.

Target maximum profit, unless significant profit appears early.

Comment or direct message for discussion, or on other interesting ideas!

Follow for updates.

BA - Neutral Iron CondorTaking advantage of mixed market feelings toward stock to place wide neutral iron condor to box in price action.

255/265/365/375 JAN19 IRON CONDOR @ 1.67 CREDIT

General plan:

Roll if necessary & if possible to reduce risk.

Target maximum profit, unless significant profit appears early.

Comment or direct message for discussion, or on other interesting ideas!

Follow for updates.

LVS - Bearish-neutral Iron CondorStock has sold off since May/June, with no recovery since last earnings report. Betting on price to stay within this range.

35/40/62.5/67.5 JAN19 IRON CONDOR @ 0.64 CREDIT

General plan:

Roll if necessary & if possible to reduce risk.

Target maximum profit, unless significant profit appears early.

Comment or direct message for discussion, or on other interesting ideas!

Follow for updates.

Fb possible Bounce,strong support $130It is hard to predict o time the market but in this scenario is not much gain for shorting the stock until the stock is at leat near the upper band, max gain for short seller is limited to $4 bucks,also, as a remainder today was a big green candle if you look at 4 Hourly chart and risk takers buy below the lower band, also, the fundamental case for FB trades now at 19x his earnings,industry leader, at the power of reach the world, Never understimate good companys,because of the noise and CNBC propaganda, maybe if you are an option trader Dic 28 Calls ITM $130, If you want to take less risk with 30% Stop Loss or if you want to take more risk, $140.00 Calls OTM There is a good chance that the stock bounce between $147.37-$140.22 and the bearish case is $130.57-126.1533, this is still in down trend and for long term investor is good chance to buy very cheap, for swing trader set a stop loss for a good profit! have a nice day! :'V FB

Netflix Still Has Room To FallDespite a 36% dive, $NFLX can fall another 29% and still post a small gain for the year.

Given rising volatility and a broad-market correction, a short position on Netflix could be a good idea.

A bearish strangle with expirations on DEC21 is what I'm currently holding. The possibility for an end of year rally is still there (hence using a strangle for protection if things go awry), but the probability of that rally grows increasingly slim - particularly within the FAANGs as a correction is far past due.

BABA - NO SLEEP TILL BROOKLYN $160Baba did not correct as i thought, it has now passed the $152.90, should be nice ride to $169

Iron Condor for TXN The stock might stay between 102 and 116. Option orders for Iron Condor

-1 TXN $102 Put 10/26 Sell

+1 TXN $100 Put 10/26 Buy

+1 TXN $118 Call 10/26 Buy

-1 TXN $116 Call 10/26 Sell

BABA options Trade.. Hit $160 by Tues, and $175 by ThnxgivingNYSE:BABA

Tech: Has had trouble breaking thru major 382 fib level. Shallow “2 wave” due to market rally and AMZN (same sector) price action..

Trade Rationale: Alibaba’s Singles day (Amazon prime day equivalent) is Monday 11/11/18.. BABA reported highest consumer signups ever and last years 1 day rake was $24B.. I think the if news reports anything remotely good on the numbers, that will give NYSE:BABA enough BUY volume “Boom POW” momentum to get it over the 382 wall it needs to climb... and plus, JD.com ain’t been doin all that well w market share... #JD .com down -49% YTD ~ (-$30.9B mrkt cap)

and BABA down -18% YTD -$82.5B mrkt cap

Option strategy.

1. Long Nov 23 $160 Call Option, Trading at $0.78 currently.. when it hits, 451% return

Stop loss: think, If Baba < $144 = BAD

2. Long Dec 7, $175 Call Option, Currently trading $0.47... If it hits, 1,581% return... Lol

TSLA to $485 by apr?I'm not actually getting in on this trade, there is too much uncertainty around Musk and Tesla for my liking at the moment. I have traded TSLA in the past. This is a stock I would like to see get less unpredictable. That being said, the monthly candle suggests conditions for a bull run.

Bear move coming for NFLX, 26% drop by FebI'm actually long on NFLX stock but I think it'll drop over the next quarter. Overvalued compared to the other streaming services but lots of original content and a huge expected increase in subscriptions to streaming services over the long term.

This chart is based on a monthly consolidation but I am showing the weekly candle to show that my last 5 forecasts with NFLX all hit their targets, although they were shorter term targets.

Expiry Strategy: Sell 290 Nov Put @ CMP 1.7Moving average crossover signals bullishness. Expect this series expiry would above 290.

Expiry Strategy: Sell 1400 Call Oct @ CMP 4Recent fall following bearish engulfing in weekly and close below bollinger lower band would keep the sentiment in negative bias for Oct. Expect the expiry would stay below Rs.1400.

$SLV Bullish Credit Spread (Oct Monthly)Medium term bullish credit spread on SLV ( silver ). As silver attempts to break above 14.35 (spot price) we have a unique opportunity to profit on a 1 month bullish credit spread.

Entry 13.44

Max profit 14.50

Break even 13.70

0.26/1 risk/reward

Expiry Strategy: Sell 680 SEP call @ CMP 2.4Bea rush engulfing in weekly chart would keep the sentiment in bearish bias for this week. Expect Sep contract to expire below 680.

MU - Looking like a $55 stock by Friday. Our extremely thorough analysis indicates that a YOLO trade might be warranted on MU. We are buying $55 calls expiring tomorrow. We expect a large plate of chicken tenders for dinner, should this move occur.

5th wave short - short term bearish - long term bullishI'm soing it with options so my spread is between 35 and 31. Sucking up that premium.

XLE Bullish Credit SpreadNew Bullish Credit Spread on XLE . Expecting to see a push for $75.59 resistance by EoW.

Entry 75.11.

Break Even 74.73.

1:1 r/r

$XLY Bearish Credit SpreadXLY Bearish Credit Spread - Opened. XLY leaning very bearish this morning (Monday) with a possible movement to test the 115 area as expected.

Entry 116.11.

Break Even 116.68.

1.7:1 r/r

Even with the heightened volatility this week, we will let this spread expire as it has a defined risk and reward.

USD/SEK only for option trading ...This is only for option trading ...

from 23.30 to 00.30

1 hour candle will be red....

please wait for active trade below

GBP/CHF only for option trading ...This is only for option trading ...

from 19.30 to 20.30

1 hour candle will be green....

please wait for active trade below