SPY WEEKLY-MAY 6 2024Welcome to SPY weekly and I have clearly explained which levels to trade & what direction market can take.

If you have any questions feel free to DM

NOTE: AVOID TRADING SPY

Optionsstrategies

BANK NIFTY INTRADAY LEVELS FOR 06/05/2024BUY ABOVE - 48970

SL - 48800

TARGETS - 49130,49300,49480

SELL BELOW - 48800

SL - 48970

TARGETS - 48660,48500,48400

NO TRADE ZONE - 48800 to 48970

Previous Day High - 49610

Previous Day Low - 48660

Based on price action major support & resistance's are here, the red lines acts as resistances, the green lines acts as supports. If the price breaks the support/resistance, it will move to the next support/resistance line. White lines indicates previous day high & low, high acts as a resistance & low acts as a support for next day.

Trendlines are also significant to price action. If the price is above/below the trendlines, can expect an UP/DOWN with aggressive move.

Please NOTE: this levels are for intraday trading only.

Disclaimer - All information on this page is for educational purposes only,

we are not SEBI Registered, Please consult a SEBI registered financial advisor for your financial matters before investing And taking any decision. We are not responsible for any profit/loss you made.

Request your support and engagement by liking and commenting & follow to provide encouragement

HAPPY TRADING 👍

NIFTY INTRADAY LEVELS FOR 06/05/2024BUY ABOVE - 22550

SL - 22510

TARGETS - 22600,22640,22710

SELL BELOW - 22470

SL - 22510

TARGETS - 22430,22360,22320

NO TRADE ZONE - 22470 to 22550

Previous Day High - 22780

Previous Day Low - 22360

Based on price action major support & resistance's are here, the red lines acts as resistances, the green lines acts as supports. If the price breaks the support/resistance, it will move to the next support/resistance line. White lines indicates previous day high & low, high acts as a resistance & low acts as a support for next day.

Trendlines are also significant to price action. If the price is above/below the trendlines, can expect an UP/DOWN with aggressive move.

Please NOTE: this levels are for intraday trading only.

Disclaimer - All information on this page is for educational purposes only,

we are not SEBI Registered, Please consult a SEBI registered financial advisor for your financial matters before investing And taking any decision. We are not responsible for any profit/loss you made.

Request your support and engagement by liking and commenting & follow to provide encouragement

HAPPY TRADING 👍

DDOG Datadog Options Ahead of EarningsIf you haven`t sold DDOG before the previous earnings:

Then analyzing the options chain and the chart patterns of DDOG Datadog prior to the earnings report this week,

I would consider purchasing the 125usd strike price Puts with

an expiration date of 2024-6-21,

for a premium of approximately $9.10.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Mayor resistanceI bought puts there expire a month from now strike 190. That's a mayor resistance zone I think is going to 180 right there 10 dollars drop. My SL 195.

Opening (IRA): IWM Sept/Oct 160/150 Short PutsComments: Going ahead and rounding out Q3 rungs here with IVR at 82.7.

September 20th 160: filled for a 1.99 credit

October 18th 150: filled for a 1.61 credit

Will look to manage shorter duration rungs as I come to them ... .

Opening (IRA): TLT July 19th 86 Short Put... for a .98 credit.

Comments: Adding to my TLT position on weakness here, targeting the strike paying around 1% of the strike price in credit.

I already have rungs on in April/May/June, so am adding a smidge out in July.

With QQQ and SPY knocking on ATH's, holding off on my usual broad market plays to await weakness and/or higher IV.

Opening (IRA): QQQ September 20th 430 Short Put... for a 4.34 credit.

Comments: Adding a rung out in Sept at the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging Into the Q's. I already have rungs on in June, July, and August ... .

Will naturally back-track into shorter duration if I can get in at strikes better than what I currently have on.

Opening (IRA): QQQ August 16th 370 Short Put... for a 4.30 credit.

Comments: Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the Q's.

Adding at a strike better than what I currently have on in August ... .

Opening (IRA): IWM August 16th 170 Short Put... for a 1.78 credit.

Comments: Starting to round out my Q3 rungs here on weakness and higher IV, targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market. Already have June and July rungs on, so going out to August here.

Opened (IRA): IWM June/July 182/180 Short PutsComments: Added at strikes better than what I currently have on in weakness, targeting the <16 delta strikes in the respective expiries paying around 1% of the strike price in credit to emulate dollar cost averaging into the small cap ETF.

June 21st 182: Filled for 1.89

July 19th 180: Filled for 2.22

I also briefly looked at QQQ and SPY, but couldn't get in at strikes better than what I currently have on, so am leaving those positions alone for now.

Opening (IRA): IWM June 21st 175/July 19th 170 Short PutsComments: Targeting the <16 delta strikes paying around 1% of the strike price in credit to emulate dollar cost averaging into the small caps ETF.

Adding here on weakness, better strikes than what I currently have on in those expires.

Filled the June 21st for a 1.75 credit; the July 21st 170 for 1.76.

Opening (IRA): IWM June 21st 185 Short Put... for a 1.87 credit.

Comments: Targeting the <16 delta strike in the shortest duration that pays around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

The ROC %-age isn't tremendously sexy here, so primarily doing this to keep theta on and burning while I work shorter duration, higher IV underlyings (e.g., SMH, XBI, GDX/GDXJ, etc.).

Opening (IRA): XBI June 21st 82 Short Put... for a 1.90 credit.

Comments: Selling a put here, since the resulting cost basis if assigned shares would be lower than the cost basis of the position I've currently got on now. The full position is now a June 21st 82/88 covered strangle (i.e., short put, stock, short call).

Will look to take profit at 50% max.

Metrics:

Buying Power Effect/Break Even/Cost Basis in Shares if Assigned: 80.10

ROC at Max as a Function of Buying Power Effect: 2.37%

ROC at 50% Max as a Function of Buying Power Effect: 1.19%

Delta/Theta: 23.36/2.42

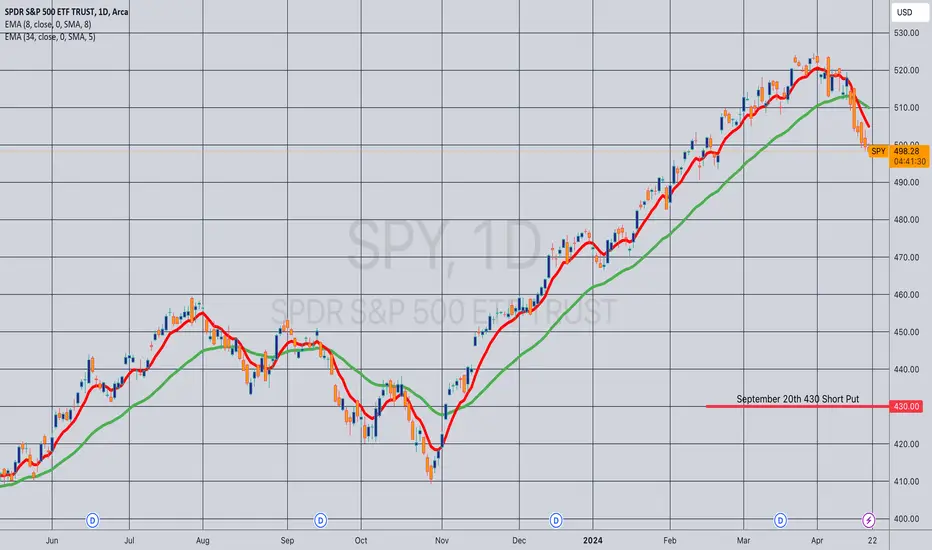

Opening (IRA): SPY September 20th 430 Short Put... for a 4.34 credit.

Comments: Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into S&P 500 ETF, adding at a strike better than what I currently have on.

As with my other broad market, will look to generally take profit at 50% max or -- if assigned -- sell call against at the strike price my short put was at.

Opening (IRA): SPY August 16th 450 Short Put... for a 4.50 credit.

Comments: Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the S&P 500 ETF.

Here, adding a strike better than what I currently have on in the August expiry.

Will generally look to take profit at 50% max.

Opening (IRA): QQQ July 21st 380 Short Put... for a 3.90 credit.

Comments: Starting to tip-toe into Q3 (July/August/September) contracts in broad market (IWM, SPY, QQQ). Targeting the <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging into the broad market.

As usual, will look to sell in shorter duration on weakness, assuming I can get in at strikes better than what I currently have on.

Opening (IRA): QQQ June 21st 395 Short Put... for a 4.09 credit.

Comments: Finally, a bit of weakness ... . Targeting the shortest duration <16 delta strike paying around 1% of the strike price in credit to emulate dollar cost averaging in without actually being in stock.

BANK NIFTY INTRADAY LEVELS FOR 03/05/2024BUY ABOVE - 49480

SL - 49340

TARGETS - 49670,49850,50000

SELL BELOW - 49180

SL - 49340

TARGETS - 49020,48800,48630

NO TRADE ZONE - 49180 to 49480

Previous Day High - 49480

Previous Day Low - 49180

Based on price action major support & resistance's are here, the red lines acts as resistances, the green lines acts as supports. If the price breaks the support/resistance, it will move to the next support/resistance line. White lines indicates previous day high & low, high acts as a resistance & low acts as a support for next day.

Trendlines are also significant to price action. If the price is above/below the trendlines, can expect an UP/DOWN with aggressive move.

Please NOTE: this levels are for intraday trading only.

Disclaimer - All information on this page is for educational purposes only,

we are not SEBI Registered, Please consult a SEBI registered financial advisor for your financial matters before investing And taking any decision. We are not responsible for any profit/loss you made.

Request your support and engagement by liking and commenting & follow to provide encouragement

HAPPY TRADING 👍

NIFTY INTRADAY LEVELS FOR 03/05/2024BUY ABOVE - 22710

SL - 22640

TARGETS - 22780,22830,22880

SELL BELOW - 22640

SL - 22710

TARGETS - 22600,22550,22510

NO TRADE ZONE - 22640 to 22710

Previous Day High - 22710

Previous Day Low - 22550

Based on price action major support & resistance's are here, the red lines acts as resistances, the green lines acts as supports. If the price breaks the support/resistance, it will move to the next support/resistance line. White lines indicates previous day high & low, high acts as a resistance & low acts as a support for next day.

Trendlines are also significant to price action. If the price is above/below the trendlines, can expect an UP/DOWN with aggressive move.

Please NOTE: this levels are for intraday trading only.

Disclaimer - All information on this page is for educational purposes only,

we are not SEBI Registered, Please consult a SEBI registered financial advisor for your financial matters before investing And taking any decision. We are not responsible for any profit/loss you made.

Request your support and engagement by liking and commenting & follow to provide encouragement

HAPPY TRADING 👍

BANK NIFTY INTRADAY LEVELS FOR 02/05/2024BUY ABOVE - 49480

SL - 49250

TARGETS - 49670,49850,50000

SELL BELOW - 49250

SL - 49480

TARGETS - 49020,48800,48630

NO TRADE ZONE - 49250 to 49480

Previous Day High - 50000

Previous Day Low - 49250

Based on price action major support & resistance's are here, the red lines acts as resistances, the green lines acts as supports. If the price breaks the support/resistance, it will move to the next support/resistance line. White lines indicates previous day high & low, high acts as a resistance & low acts as a support for next day.

Trendlines are also significant to price action. If the price is above/below the trendlines, can expect an UP/DOWN with aggressive move.

Please NOTE: this levels are for intraday trading only.

Disclaimer - All information on this page is for educational purposes only,

we are not SEBI Registered, Please consult a SEBI registered financial advisor for your financial matters before investing And taking any decision. We are not responsible for any profit/loss you made.

Request your support and engagement by liking and commenting & follow to provide encouragement

HAPPY TRADING 👍

NIFTY INTRADAY LEVELS FOR 02/05/2024BUY ABOVE - 22600

SL - 22550

TARGETS - 22660,22710,22780

SELL BELOW - 22550

SL - 22600

TARGETS - 22510,22470,22430

NO TRADE ZONE - 22550 to 22600

Previous Day High - 22780

Previous Day Low - 22550

Based on price action major support & resistance's are here, the red lines acts as resistances, the green lines acts as supports. If the price breaks the support/resistance, it will move to the next support/resistance line. White lines indicates previous day high & low, high acts as a resistance & low acts as a support for next day.

Trendlines are also significant to price action. If the price is above/below the trendlines, can expect an UP/DOWN with aggressive move.

Please NOTE: this levels are for intraday trading only.

Disclaimer - All information on this page is for educational purposes only,

we are not SEBI Registered, Please consult a SEBI registered financial advisor for your financial matters before investing And taking any decision. We are not responsible for any profit/loss you made.

Request your support and engagement by liking and commenting & follow to provide encouragement

HAPPY TRADING 👍

BANK NIFTY INTRADAY LEVELS FOR 30/04/2024BUY ABOVE - 49480

SL - 49250

TARGETS - 49670,49850,50000

SELL BELOW - 49250

SL - 49480

TARGETS - 49020,48800,48630

NO TRADE ZONE - 49250 to 49480

Previous Day High - 49480

Previous Day Low - 48310

Based on price action major support & resistance's are here, the red lines acts as resistances, the green lines acts as supports. If the price breaks the support/resistance, it will move to the next support/resistance line. White lines indicates previous day high & low, high acts as a resistance & low acts as a support for next day.

Trendlines are also significant to price action. If the price is above/below the trendlines, can expect an UP/DOWN with aggressive move.

Please NOTE: this levels are for intraday trading only.

Disclaimer - All information on this page is for educational purposes only,

we are not SEBI Registered, Please consult a SEBI registered financial advisor for your financial matters before investing And taking any decision. We are not responsible for any profit/loss you made.

Request your support and engagement by liking and commenting & follow to provide encouragement

HAPPY TRADING 👍