THE WEEK AHEAD: KRE, EWZ, GDXJWith the beginning of the next earnings season two weeks out (at least before we see something decent), I'm looking to put on some basic exchange-traded fund premium selling plays to bide my time until then. Even there, however, the premium selling opportunities aren't fantastic:

KRE (Regional Banks): I haven't played this one before, but its background implied volatility is at 25%, putting it slightly above its mid-range over the past six months (it's in the 54% percentile or so). I generally like to see exchange-traded funds at >70% implied volatility percentile over the past six months and implied volatility at 35% or more, but if I abide by those metrics, I'd be totally sidelined here. (The May 19th 49/54/55/60 "nearly an" iron fly pays 2.53 at the mid with a buying power effect of 2.47; preliminary/off hours quotes).

EWZ (Brazil): In spite of the fact that its implied volatility has been a good deal higher over the past six months (background implied is at 32% -- in the 28th percentile over the past six months), it still has some decent premium to be offered if you're willing to short straddle or iron fly. (The May 19th 33/37/38/42 iron fly pays 2.12 at the mid with a buying power effect of 1.88; preliminary/off hours quotes).

GDXJ (Junior Gold Miners): This is one I was actually looking to play directionally off of support, but waited too long to put on the play, so now it's "nondirectional" for me or nothing. (The May 19th 30/33/40/43 iron condor pays 1.21 at the mid with a buying power effect of 1.79; preliminary/off hours quotes).

VIX: With VIX, my eyeballs are always peeled for a "Term Structure" play if there isn't a pop to be had. Unfortunately, neither a pop nor a Term Structure play are to be had currently. VIX spot is at 12.4, and the first /VX futures front month that currently is >16 is September -- way too far out in time for me to put on a play (I currently still have June 17/20, and July 16/19 short call verticals on).

Optionsstrategy

OPENING: VRX MONIED COVERED CALLI'm fading the Ackman dumpage here with a small position bet that price will stay clear of $10 through April 21st expiry ... .

Bought 100 Shares

Sold April 21st 10 Call

Whole Package: 9.38

Max Profit: $62 per 100 shares/contract

Max Loss/BP Effect: $938 per 100 shares/contract

THE WEEK AHEAD: SNAP, FEZ, XLV, AND XRTWith four weeks or so until the next batch of earnings, I'm briefly turning my attention to exchange-traded funds to see if there's anything I can play to bridge the gap between earnings seasons.

As with the previous several weeks, there isn't much; only three are near or above the 70th percentile for implied volatility over the past six months: FEZ, with an implied volatility rank of 86, and a background implied volatility of 20; XLV (68/17) (no surprise there; some friskiness associated with the failed Repeal and Replace measure); and XRT (67/22). I will look to work XLV and XRT with iron flies, possibly, but I may go directional on FEZ, since it's meant to replicate the performance of the Euro Stoxx 50.

The other possibility is SNAP. It hasn't been on the block long enough for it to have a "6 month" metric of anything, but its background implied volatility is at 59%, and that's somewhat high for this market. Because of its potential for rippage, I think the best play in that is directional or where there is no directional risk on one side or the other (put diagonal, Jade Lizard, Big Liz).

I'll putz with possible SNAP setups here and post separately if something looks particularly attractive ... .

TRADE IDEA: A SNAP POOR MAN'SOne thing I'm certain about, and that's that I don't want to buy SNAP stock here with its having whipsawed between 29+ and 19 in the short time since its IPO. But I might want to acquire it later once it settles down -- as with all things, preferably at a lower price than 22.74. A Poor Man's Covered Call gives me the flexibility to play SNAP, give me the option to buy it later by exercising the 15 long call before expiry, as well as to reduce cost basis in that long call while I'm waiting for it to figure out where it's going.

Consequently, here I'm thinking a Poor Man's Covered Call where the long-dated, back month, long option takes the place of long stock and (as with any covered call), the short call looks to reduce cost basis in the long option, while protecting the position from some downside. As with a covered call, you look to roll out the short option for duration, ideally keeping it clear of your cost basis, and you exit the trade for a credit that exceeds what you paid to put it on minus any credits collected due to rolling.

Metrics:

Max Loss/Buying Power Effect: $725/contract

Theta: 2.23/contract

Delta: 50.38

As with any diagonal (that's what this is, basically), we don't know much else about the setup in terms of potential profit, but I generally look to exit these north of 10% of what I paid to put them on.

Naturally, this is likely to continue to be somewhat of a roller coaster, so you need to be prepared for somewhat of a bumpy ride, particularly as price moves toward the long call side of the setup (since its delta long).

Notes: There is some piddling that needs to be done with these to ensure that the credit received for the short call exceeds any extrinsic value in the long option. The extrinsic value in the long option can be calculated by subtracting the difference between current price and the long call strike from what you will be paying for the long option 8.20 - (22.74 - 15) = .46. The April 21st 24 short call brings in .95 in credit at the mid, which is greater than the extrinsic value in the long.

Currently, the long option is bid 7.80/ask 8.60, so some further adjustment may be required during regular market hours to recalculate whether the extrinsic value received for the short exceeds that in the long and/or to get a fill.

XLK Synthetic StraddleTrade Setup:

- 1 XLK May 19 45/53/53/57 Synthetic Straddle @ 1.97.

DTE: 57

Max Win: $197

Max Loss: $603 (theoretically), but will manage at 2x credit, so ~$200.

Breakevens: $51.03 & $54.97

Trade Management: 25% profit; WIll risk full loser to upside and only 2x credit received to downside. I often will take off one of the sides when it becomes nearly worthless to reduce risk one of the directions.

Green is profit zone; Vertical black bar is expiration.

OPENING: FDX MARCH 31ST 177.5/182.5/202.5/207.5 IRON CONDOR... for a 1.40 credit. (Earnings; Volatility Contraction Play).

Metrics:

Probability of Profit: 60%

Max Profit: $140/contract

Max Loss/Buying Power Effect: $360/contract

Break Evens: 181.10/203.90

Notes: Will look to manage at 50% of max.

THE WEEK AHEAD: IT'S EYEBALLS ON THE FEDUgh. Doing my weekly market review/screening and there is literally nothing high IVR/high IV to play ... . Nada ... . Zilch ... .

One option is to sell puts in one of these "just high IV" underlyings:

VRX: April 21st 11 goes for .56

AKS: April 21st 7 goes for .31

AMD: April 21st 13 goes for .66

WLL: April 21st 8 goes for .28

CLF April 21st 8 goes for .34

X: April 21st 32 goes for 1.25

These are all at or around the 30 delta ... . Those plays, however, are not my "favorite girls to dance with at the ball."

For earnings, what little "quality" stuff is left to this season is still a few days out:

FDX (IVR 92/IV 30) (3/21 AMC)

GME (IVR 73/IV 46) (3/23 AMC)

MU (IVR 76/IV 47) (3/23)

VIX: For a "Term Structure" play,* the earliest expiry where the 50 delta strike is at 16 or greater and pays ~2.50/contract is June, and that's 101 DTE ... .

Of course, we have that little Fed shindig going on next week. Implied volatility and the VIX can turn on a dime, but I've been waiting for VIX to turn on a dime for weeks ... .

Short term target 46, upsloping trend lineBroke out of uptrend with high volume. CFTC showed specs were long, so there is plenty of room to the downside.

Spreads have been weak and option volatility was low before breakout. As it broke to the downside, longs scrambled to protect with an downside puts and panic left option vol to increase by over 6 points.

On the downside, i am looking into the trendline around 46ish.

I would expect a breather there. if it holds, great, but production in the US is up.

Only an agreement between Russia and the OPEc on production cuts could truly turn this around.

OPENING: ATVI COVERED PUTThis is a continuation of a trade that started as an earnings play iron fly (see post below).

There are a couple of reasons I went this particular way, as opposed to attempting to continue to work the setup "as is."

First, the March 17th 40 short call was deep in the money. Even assuming I could roll to improve that strike a bit, it would still be deep in the money. Deep in the money options are generally made up of a lot of intrinsic value, so you won't get that much time decay out of them.

Secondly (and relatedly), you can't get much of a credit to roll a deep in the money short option because you're basically rolling from a mostly intrinsicly valued option to, well, a mostly intrinsically valued option, and so you're not picking up that much premium such that you'll receive a credit for a roll. Just to make sure, I checked to see whether I could get a credit to roll out to the April 21st 40 short call "as is" and receive a credit -- no dice. Alternatively, I looked at how much a strike improvement would cost to roll from the March 17th 40 to the April 21st 41 to see whether I could sell a short put vert against for a credit which would exceed the cost of the roll; I wasn't happy with where I'd have to setup the short put vert to do that (basically, I'd roll into an inverted iron condor setup; far less than ideal).

As compared to a covered call: everything is "upside down" with a covered put: (a) you're looking to increase your cost basis in your short shares by selling puts against them; (b) if price finishes below your short by at expiry, your short shares get called away; and (c) you work to roll the short put out for duration and credit, attempting to keep it clear of current price action until you can exit the whole setup profitably. Here's I'm just looking to mitigate loss from the original broken trade or, ideally, get back to scratch.

OPENING: DKS MARCH 17TH 43/50/50/57.5 IRON FLY... for a 4.35 ($435)/contract credit. I put this on earlier in the week, but neglected to post it here ... . (High implied volatility rank; high implied volatility; it's in the 95th percentile of where implied volatility has been in the past six months; its background implied volatility is at 47%).

Metrics (Currently):

Max Profit: $418/contract

Max Loss/Buying Power Effect: $332/contract

Break Evens: 45.82/54.18

Theta: 5.66/contract

Delta: 1.33/contract

Notes: DKS earnings are currently scheduled for March 14th. The notion here was to play the underlying for sideways chop leading up to earnings, but take it off shortly before. We'll see how that works out .... . If I get an opportunity to close it out in profit before earnings, I may play it again for the earnings announcement ... .

OPENING: BBY MARCH 10TH 38/42/47.5/51.5 IRON CONDORBBY announces earnings tomorrow before market open, so look to put on something today before market close to take advantage of the ensuing volatility contraction. Implied volatility rank is currently at 92 over the preceding six months, with implied volatility just shy of the 50% mark.

I compared and contrasted going with my standard 20-delta iron condor, as well as a full on iron fly. Here, I'm selling the 30-delta shorts as a sort of compromise ... .

Metrics:

Probability of Profit: 57%

Max Profit: $163/contract

Max Loss/Buying Power Effect: $239/contract

Break Evens: 40.39/49.11

Delta: -2.39

Theta: 9.03

TRADE IDEA: GPS 21/25/25/29 IRON FLYHigh implied volatility rank, high implied volatility, earnings/volatility contraction play ... .

Metrics:

Max Profit: $203/contract

Max Loss/Buying Power Effect: $197/contract

Break Evens: 22.97/27.03

Delta: -6.38

Theta: 2.03

Notes: I'll shoot to take this off at 25% max profit ... .

THE WEEK AHEAD: EARNINGS AND A PERSISTENTLY LOW VIXIf you're going to play anything next week premium selling wise, it's going to be in earnings, because that's all that's really out there volatility-wise. The VIX remains persistently low here, and running a screen for exchange-traded funds with >70% implied volatility rank, and >35% implied volatility yields absolutely nothing.

Here's what showed up on my radar -- some sketchy ADR action (WUBA), a little bit of frisky biopharm (BCRX), and some beaten-down brick-and-mortar retail (M, SHLD, JCP):

WUBA (99/56) (Online Retail): It's scheduled to announce earnings on Thursday (2/23) (Short strangle/iron condor).

BCRX (98/287) (Biopharm): Earnings Monday (2/27) Before Market Open. (Short puts, short straddle). This is biopharm, which -- in itself -- should serve as a warning. You may want to do a bit more due diligence on this one than you would ordinarily, since they can explode, but also implode.

DKS (98/48) (Sporting Goods/Retail): Earnings are three weeks out, but I thought I'd put it out there since it's nearly ripe for play implied volatility rank/implied volatility wise. (Short strangle, iron condor).

M (96/49) (Department Store Retail): Earnings Tuesday (2/21) Before Market Open. Because we have a long holiday weekend here, with the markets being closed on Monday, I've probably missed an opp to play this one unless there is high vol afterglow post earnings. (Short strangle, iron condor).

SHLD (93/127) (Department Store Retail): I don't see that this has earnings up, but it's in the process of imploding. (Short puts, short straddle).

BBY (93/47) (Retail): Earnings 3/1 Before Market Open. We're still a ways out from earnings, so like DKS, nearly ripe ... . (Short strangle, iron condor).

HTZ (92/73) (Car Rental): Earnings 2/27 (Monday) After Market Close. Another one that's ripe right now. (Short strangle, iron condor).

JCP (88/65) (Department Store/Retail): Earnings Friday (2/24) Before Market Open. Another beaten down brick and mortar retail issue. (Short puts, short straddle).

OCN (85/70) (Financial): Earnings on 2/22 (Wednesday) After Market Close. (Short puts,short straddle).

TRADE IDEA: SPY MAY 19TH 212/MARCH 17TH 224 SHORT PUT DIAGONALHere, I'm looking to add some long delta to my portfolio, although it's also good as a stand alone trade in this low volatility environment. The short-dated put is being sold at the ~20 delta strike, the long-dated one at the ~15, so I'm picking up about 5.00 positive delta/contract from this setup.

Unfortunately, with diagonals, we're not able to precisely calculate the max profit/loss and break evens for the setup.

However, the net delta for it is 4.83/contract, it's positive theta (1.24/contract), and it will cost a small debit to put on (.60/$60 per contract). Because of the width between the strikes, though, it is a bit pricey to put on -- about $1140/contract of buying power effect (the width between the strikes minus the debit).

How to Work It: The vast majority of traders leave the long option in place and work only the short option, ideally taking the short off at or near max profit as expiry approaches or rolling it down and out for duration and additional credit. If taking the option off at near worthless, the notion is to "re-up" by selling a new short option in the next monthly expiry.

Some also choose to work the long option, rolling it down intraexpiry (within the same expiry) to lock in any increase in value it experiences while the trade is on. Keep in mind that doing this will generally widen the spread between the front month short and the back month and will increase the buying power effect attributable to the setup if you haven't narrowed the spread by rolling the short put down and out at some point.

As far as take profit is concerned, I take a fairly loose approach, since it will depend on what happens during the life of the setup.

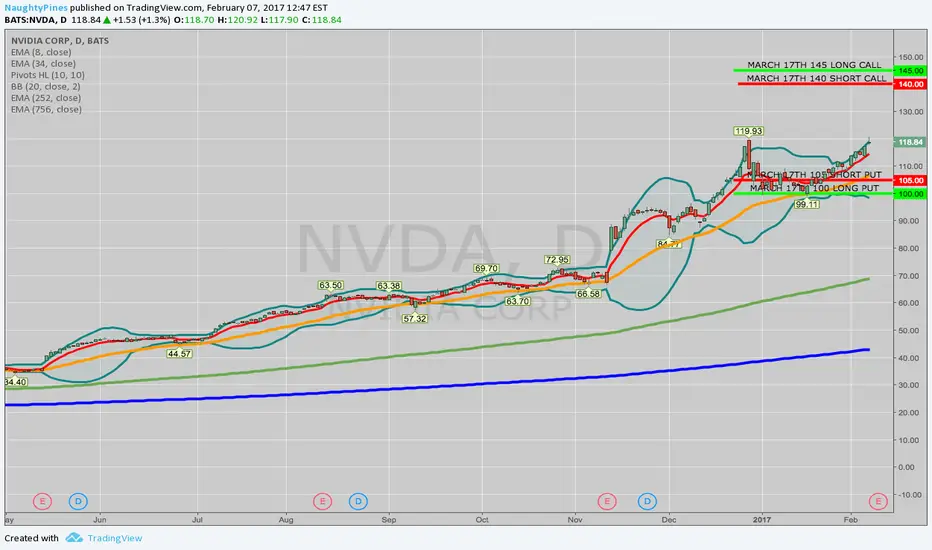

OPENING: NVDA 100/105/140/145 IRON CONDOR... for a 1.57/contract credit. (Earnings; High IVR/High IV).

I fiddled with various setups long enough ... . Here, I'm going out farther in time than I usually like to go with an earnings play in order to give myself time to be right.

Will look to manage to 50% max profit.

Metrics:

Probability of Profit: 63%

Max Profit: $157/contract

Max Loss: $343/contract

Break Evens: 103.43/141.57

TRADE IDEA: ATVI FEB 17TH 34/38.5/40/44.5 IRON CONDORATVI announces earnings tomorrow after market close, so look to put on a play in the waning hours of the NY sesh ... . Its implied volatility rank is >70%, and its background volatility is on the cusp of 50% ... .

Metrics:

Probability of Profit: 50%*

Max Profit: $231/contract

Max Loss/Buying Power Effect: $219/contract

Theta: 11.33/contract

Delta: -2.47/contract

BE's: 36.19/42.31

Notes: * -- The body of this is so narrow such that it's almost an iron fly; hence, the piss poor POP%. I considered doing the standard 20-delta iron condor here, but just couldn't squeeze out enough credit to satisfy me. I'll basically look to treat it like an iron fly, and look to take it off at 25% max profit.

TRADE IDEA: XOP MARCH 17TH 36/40/40/44 IRON FLYLooking for petro to zombie about in here in the short term ... . Implied volatility rank isn't as high as I'd like it, but background vol is one of the higher ones out there for exchange traded funds.

Metrics:

Max Profit: $242/contract

Max Loss: $158/contract

Break Evens: 37.58/42.42

Notes: Will look to manage at north of 25% max profit.

OPTIONS TIP: "CHEAP CALLS" HERE MAY NOT BE "SMART" ... DEPENDINGBad advice in part; good advice in part; hiding the ball in part. finance.yahoo.com

The good part: cover your stock/equity positions with short calls. This will smooth out your P&L somewhat and protect you -- albeit not completely -- from down side risk while reducing cost basis in your shares. Unfortunately, they don't want to "share their secrets" right up front about "where" to sell those short calls (strike, expiry), so do some research as to where you should sell those (I generally sell the 20 delta short call to cover in the monthlies; others are slightly more aggressive and sell the 30; to a certain extent, it depends on what you're doing with an individual position (i.e., are you looking to reduce cost basis over the long-term or looking to get called away)).

(To be somewhat nit-picky here, though, selling short calls in this environment isn't quite as productive as in a high implied volatility environment. You'll get less than you would were implied volatility were higher. Nevertheless, staying "covered" the vast majority of the time is fairly good advice.)

The bad part, depending on what they're saying: buy calls here because they're "cheap." One of their recommendations is to liquidate a portion of your shares and buy long calls instead. As I've repeatedly said here, buying and holding shares is extremely capital intensive as compared to an options position that "synthetically" represents long stock. When I do a play like this article appears to be recommending (but doesn't come out and say directly), I buy deep in-the-money calls somewhat far out in time (>180 DTE). I buy deep and long-dated because I'm looking for calls with as little extrinsic value/premium in them as possible, because I just don't want to pay for premium in an option that will just decay over time. Even when I do this, I "cover" this "synthetic" long stock position with short calls nearer in time (the options lingo for this setup is a "Poor Man's Covered Call.").

If that's what they're recommending that people do here in this article, then come right out and say it, for goodness sake. Merely saying: "buy calls" is stupid, uninformative, and potentially destructive.

If the article is suggesting that readers buy out-of-the-money calls here just because they're "cheaper" (i.e., made up of less extrinsic value) than usual, well, that's just plain ass stupid advice. The vast majority of OTM calls expire worthless, so you would be throwing your money away on these if you do not get the required movement you need to "make them pay."

Long calls may be comparatively cheap here in this low volatility environment; it doesn't mean they're a "smart" play, depending what you're buying and where ... .

X EARNINGS SHORT STRANGLE/IRON FLYX announces earnings tomorrow (Tuesday) after market close, and with its implied volatility rank and implied volatility metrics, it's ripe for a volatility contraction play. Here are two possible setups, which naturally might need to be tweaked this way or that depending on price movement intraday tomorrow.

Feb 17th 29/38 Short Strangle

Metrics

Probability of Profit: 68%

Max Profit: $130/contract

Buying Power Effect/Max Loss: Broker Dependent/Undefined

Break Evens: 27.70/39.30

Notes: (1) Here, as is my habit, I'm selling the 20 delta call and put. (2) I went out a little bit farther in time to the monthly, since things are generally more liquid there, so I would be more likely to get a fill at the mid without too much diddling around. (3) Look to manage at 50% max profit or about $65/contract.

Feb 17th 25.5/33/33/41 Iron Fly

Metrics:

Probability of Profit: 50%

Max Profit: $392/contract

Max Loss/Buying Power Effect: $408/contract

Break Evens: 29.08/36.92

Notes: (1) The first thing I did was check to see what a three-wide iron condor would pay with the short options at the 20 delta strikes. It was less than 1/3rd the width of the strikes, so I switched to putzing with a fly. (2) Look to manage this setup at 25% max profit (~$98/contract). (3) While the setup looks "sexier" from a max profit standpoint, you'll also notice that the profit zone is narrower than that of the short strangle. Nevertheless, is defined risk going in, so I know what my max loss is if the thing blows up in my face.

TRADE IDEA: VIX MARCH 22ND 11.5/13.5 LONG CALL VERTICALTruth be told, I'm not a "debit spread" guy, namely because I look at them as "one and dones" -- they either work or they don't; rolling these out for duration generally costs more money, and I don't like paying to roll, so I look at them as "one shots."

Here, I looked for a risk one to make one metric for the setup ... .

Metrics:

Max Profit: $105/contract

Max Loss/Buying Power Effect: $95/contract

Break Even: 12.45

Notes: This is a debit spread, which you pay to put on. What you pay to put it on (a debit), is your max loss of the setup, but you certainly don't need to allow it to go to max loss to take it off, especially if it becomes apparent that it's just not going to work by expiry.

As far as take profit is concerned, I would probably shoot for taking it off at 50% max, although the way volatility's been trundling along here (at extremely low levels), I'd also look at taking my money at running at anything north of VIX ~ 15. After all, it hasn't seen fit to break that level since election-time ... .

TRADE IDEA: GDXJ FEB 17TH 30/36/37/45 IRON CONDOR/FLYThere isn't much non-earnings stuff out there that has both high implied volatility rank and high implied volatility. This is one of them.

Here I'm going with an extremely narrow iron condor, such that it's almost an iron fly ... .

Metrics:

Max Profit: $338/contract

Max Loss/Buying Power Effect: $462/contract

Break Evens: 32.62/40.38

Notes: I'm going to treat this as a fly for purposes of take profit and look to get 25% max.

TRADE IDEA: SPY APRIL 21ST 209/212/235/238 IRON CONDORGoing out to April for my core index exchange-traded fund position, since volatility "locally" (<45 DTE) blows here. Very close to getting 1/3rd the width of the wings; it'll have to do ... .

Metrics:

Probability of Profit: 54%

Max Profit: $92/contract

Max Loss/Buying Power Effect: $208/contract

Break Evens: 211.08/235.92

Theta: .67/contract

Delta: -5.34/contract

Notes: Here, I'm setting up my short options at the 20 delta strike, and the long options three strikes out from those. Looking to manage at 50% max profit.

OPENING: SPY MARCH 17TH 205/208/234/237 IRON CONDORI used to do a lot of SPY, IWM, QQQ, and DIA iron condors as a core position, but temporarily wandered away from those given how sporadic the implied volatility has been in these underlyings. Additionally, they have nonexistent "engagement value" (i.e., they're boring), and I haven't been able to get decent premium out of 45 day setups. Because implied volatility is so low right now, I went out to the first expiry in which I could get something approaching a 1.00 credit for a 3-wide, 20-delta setup. Here, though, I actually went a touch wider (the short options are around the 16 delta strikes).

Metrics:

Probability of Profit Percentage: 59%

P50: 75%

Max Profit: $94/contract

Max Loss/Buying Power Effect: $206/contract

Break Evens: 207.06/234.94

As with all of these, I'll look to manage the setup at 50% max profit.