TRADE IDEA: VRX NOV 18TH 17.5 SHORT PUTOkay, so there's other "big pharma" that I like wayyy better than Valeant (e.g., BMY, GILD). The problem is that BMY and GILD are more expensive and don't have the implied volatility that VRX has (for obvious reasons: they don't have as many "warts" as VRX).

Nevertheless, I'm watching VRX here because its implied volatility is so high (>100%), which makes relatively far out-of-the-money short puts comparatively rich in premium.

Here, I'm eyeing the 17.5 short puts for obvious reasons -- that strike is below historic lows for this poo pile. Moreover, with an implied vol of >100%, I can get .83 ($83) in credit per contract "at the door," which makes it quite attractive for an underlying at this price. The notion here would be to either (a) keep the premium; or (b) get put the shares at 17.5, after which I would sell calls against (covered call).

Optionsstrategy

THE WEEK OF 10/16: WHAT I'M LOOKING ATWhile I grind away on various covered call positions (I only have one covered call with an October short call on; the rest are in November or December), I'm looking ahead to some decent earnings for premium selling.

Generally, I'm looking for underlyings whose implied volatility is above the 70th percentile for the past 52 weeks and that have background implied volatility of greater than 50% to play for a contraction in volatility immediately following the earnings announcement, with the go-to strategies being short strangles or iron condors.

Currently, there are four underlyings with good liquidity options that announce earnings next week and whose volatility is above the 60th percentile for the preceding 52 weeks: IBM, NFLX, UA, and EBAY. I'm screening for >60 implied volatility rank at this point, since volatility in these could still ramp up to my >70%, meaning that they might be worth keeping an eye on.

IBM -- Announces 10/17 after market close. The implied volatility rank is now in the 85th percentile. Unfortunately, the background implied volatility is far from being up to snuff at this point for me (28.3%).

NFLX -- Announces 10/17 after market close. Implied vol rank: 64th percentile; implied volatility 56.6%. It's very nearly "there". Hopefully implied volatility pops a little more right before earnings.

UA -- Announces 10/17 after market close. Rank: 62; implied vol 41.7%. Needs more.

EBAY -- Announces 10/19 after market close. Rank: 93; implied vol 41.6%. Needs more.

After I look at implied volatility percentile and the background implied volatility, I look at what I can get out of a setup. Generally, I'm shooting for a 1.00 credit for either a short strangle or iron condor, since I look to take these off at 50% max profit (i.e., a .50 ($50)/contract profit). Alternatively, I look at whether a short straddle or iron fly would make sense if the underlying is just too cheap to yield a decent enough credit. With short straddles/iron flies, I generally look to get 2.00 in credit at the outset, since I tend to manage those at 25% max.

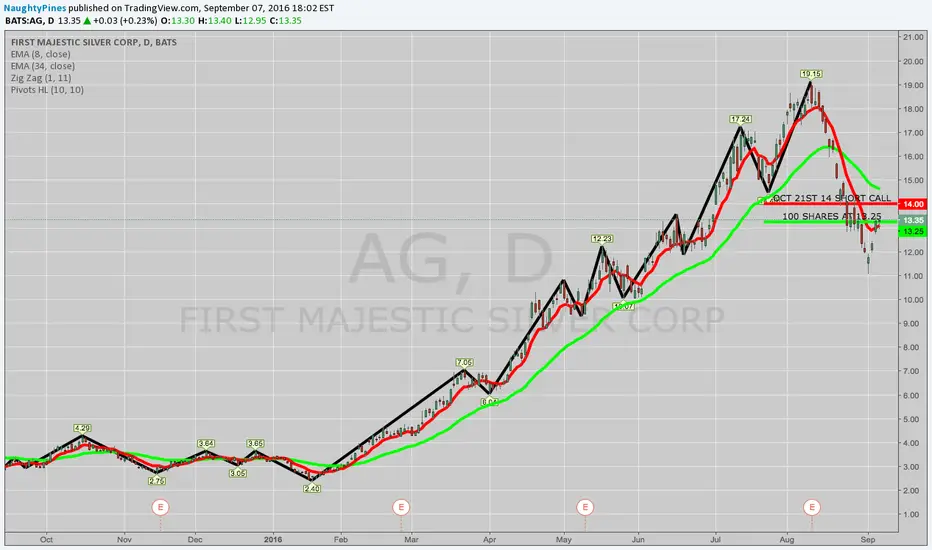

OPENING: AG COVERED CALLMy timing could have been somewhat better on this at the sub-12 dip, but better late than never ... .

Metrics:

Bought 100 Shares at 13.25

Sold Oct 21st 14 call

Whole Enchilada: 12.30 db

Max Profit: $170 (if called away at 14)

ROC: 13.8%

Notes: I promised myself after closing out my XME short put that I wouldn't be dipping into any more miners ... . Just couldn't help myself ... .

TRADE IDEA: XOP OCT 21ST 30/35/35/40 IRON FLYMostly hand-sitting here, but figured I'd take advantage of the increased volatility in the petro sector by selling a bit of premium in XOP, since its IV has popped here.

Metrics:

Probability of Profit: 52%

Max Profit: 2.46 ($256)/contract

Max Loss: 2.54 ($254)/contract

Break Evens: 37.46/32.54

Notes: I'll look to take this off at 25% max profit ... .

OPENING: AKS COVERED CALLIt was either this little fella or X ... .

Bought 100 Shares at 4.60

Sold the Oct 21st 5 call

Filled for a 4.29 debit

Max Profit: $71 (if called away at 5)

ROC: 16.6%

BACK TO WAITING FOR BROAD MARKET VOLATILITY ... BROAD MARKET INSTRUMENT PREMIUM SELLING

Post-Brexit vote in late June, when VIX spiked to >25 (signalling a premium selling opportunity in broad market instruments like SPY/SPX and RUT/IWM in the July expiry), there has been but one >15 spike to >20 in mid-September that allowed for some premium selling in the October monthlies, which have since come off in profit in the ensuing volatility crush.

Consequently, I'm back to sitting on my hands waiting for another >15 VIX spike to sell premium in SPY/SPX or IWM/RUT in a November expiry and/or managing the small number of plays I have on as covered calls or premium selling in sector ETF's like GDX and XOP, where the implied volatility remains high compared to what it is in the broader market (48.4% and 35.5%, respectively).

CAN THIS EARNINGS SEASON NOT SUCK FOR PREMIUM SELLING?

Naturally, I'm also watching potential earnings plays, but I waved off many of those last season because they weren't up to snuff. Generally, I'm looking for those to have implied volatility above the 70% percentile for the past 52 weeks and implied volatility above 50%, and there haven't been many of those around of late due to general market volatility lull. The first earnings play of interest to me right now with a >70% implied volatility rank is EBAY (10 days out), but its implied volatility remains below 50% (35.2%)

TRADE IDEA: XLU NOV 18TH 42/47/47/52 IRON "FLY"I haven't done many of these in the past, but I'm beginning to warm up to them, particular with instruments that wouldn't ordinarily yield jack diddly squat with a traditional iron condor setup.

Here's how this iron fly compares to an iron condor with similar break evens (it would be a Nov 18th 43/46/48/51):*

Probability of Profit: Fly: 52% Condor: 52%

Max Profit: Fly: $220 Condor: $120

Max Loss: Fly: $280 Condor: $180

Break Evens: Same

Theta: Fly: 1.85/day Condor: 1.32/day

Take Profit: Fly: 25% of max ($55 profit) Condor: 50% of max ($60)

Spread "Repair": Same for both setups; roll tested side out for duration and, if feasible, away from current price for strike improvement; sell the oppositional spread against for a credit that exceeds what it cost to roll the tested side. Taking into account all credits received and debits paid, shoot to take off the rolled setup at the original take profit.

As you can see, the probability of profit is the same for setups with the same or substantial similar break evens, and there's little meaningful difference between the profit I would get if I managed the fly like a short straddle (at 25% max) and the condor like a short strangle (at 50% max) ($55 vs. $60).

The research I have looked at for short straddles and short strangles indicates that short straddles reach 25% max in about 30 days on average; short strangles 50% max in about 25 days, www.tastytrade.com (short strangles); tastytradenetwork.squarespace.com (short straddles), which appears to suggest that there is no huge difference in "time to same profit" for the two strategies. (Although those studies involved short straddles and short strangles, you can think of iron flies as "defined risk short straddles" and short strangles as "defined risk short strangles"). Consequently, even though you're receiving greater credit up front for the iron fly, you're probably going to have to wait around for it to reach 25% max profit about the same amount of time as you would an iron fly.

The important takeaway here is that -- but for the iron fly -- I would probably not put on a defined risk trade in XLU. The reward is too small; the risk too great in comparison. So, another tool in the tool box for when you just can't enough credit out of a play in an instrument with your "regular" set of tools ... .

* -- Generally speaking, I would not set up an iron condor this tightly. I'd set up the short option strikes at the edge of the expected move and then the long options out from there 3-5 strikes (e.g., a Nov 18th 42/45/49/52). However, that particular setup would only yield a .72 ($72) credit/contract, and -- were I to manage that trade for 50% of profit -- would only yield .36 ($36) for a setup with a max loss of 2.28/contract ($228). The type of setup for an instrument with these particular metrics (price, implied volatility, etc.) is generally not worth it, in my opinion.

OPENING: GNW COVERED CALLTaking advantage of this "little" dip here to initiate a covered call in this little, high implied volatility bugger (at some point, I'll make the move to "quality" ... ).

Metrics:

Bought Shares at 4.73

Sold Oct 21st 5 call

Whole Package: 4.40

Max Profit: $60

ROC: 13.6%

FOR 45 DTE SETUPS, ROTATING INTO ETF'SSometimes life just plain ass gets in the way of your trading ... . Starting October 1st, my "number's up" for jury duty for the entire month of October. I may be called to serve any time during this period, sit for a lengthy period of time in a room, and then be excused because the parties have reached a last minute agreement or I may have to sit through an actual trial that goes on fairly continuously for a week or two. In sum, there's no way to plan your day, your week, or, really, your month ... .

Since I don't think the environment will be very conducive to trading (even assuming I could do that effectively on my phone or iPad), I'm going to go with trading low key setups that I don't need to keep an eye on, as compared to, for example, short strangle earnings trades with short DTE. As of Friday close, there are several >35% ETF's I have eyeballs on -- GDX (gold miners), XME (miners), EEM (emerging markets), EWZ (Brazil), and XBI (36.1).

Most of these are, in the scheme of things, "fairly cheap," so I may go covered call rather than with an options strategy that has a clock on it (i.e., spreads, strangles with "date certain' expiries).

Naturally, we have the "FOMC dance" coming up, so I may hand sit out this week until the tsunami of media spin, speculative positioning and such, passes ... .

OPENING: EXEL NOV 18TH 11 SHORT PUTHere, I'm looking to sell a touch of premium in an underlying that has both high implied volatility rank (99.6%) and high background implied volatility (99.2%).

Metrics:

Probability of Profit: 70%

Max Profit: $85/contract

Buying Power Effect: Varies by Broker.*

Break Even: 10.15

Notes: I'll shoot to take this off at 50% max profit. However, I could also see working it as a precursor to a covered call. For example, if price breaks 11 by expiry, I would either take assignment of the stock at $11/share (and then proceed to sell calls against) or roll the 11 down and out for additional credit and then look to take assignment at a more favorable price ... .

* -- When I do naked short puts, I operate on the assumption that -- worst case scenario -- I will be assigned stock at the short put strike. Here, for example, I will need $1100 of buying power (100 shares x $11/share) per contract to accommodate the assignment of shares should that occur.

TRADE IDEA: VRX "MONIED" COVERED CALLLet's start with the metrics for this setup:

Buy shares at 24.54

Sell Nov 18th 22.5 short call

Whole Package/BE/Cost Basis: 20.40 db per 100 shares/contract (20.40 is also your cost basis and break even)

Max Profit: $210 per 100 shares/contract (if called away at 22.50)

ROC: 10.3%

Now, ordinarily, I like to do "OTM" (i.e., out-of-the money) covered calls where the short call is above the price of the underlying. I feel this gives me a touch more flexibility in working the setup over a substantial period of time should I ultimately decide I want to stay in the play for whatever reason (e.g., continuing high implied volatility, it's ripping to the upside, etc.). Additionally, OTM covered calls offer better ROC %-age metrics, assuming that price continues to move toward your short call.

With a "monied" covered call, you're limiting your upside profit potential from the get-go, although you can naturally attempt to roll the "monied" short call up and out for duration, assuming that you can get a decent credit to do so, which isn't always possible. However, in exchange for "going monied," you're getting a benefit: the stock price can continue to decline somewhat, and you can still make money. For instance, if price is still above the short call strike at expiry, your shares are called away and your profit is the short call strike price (x 100) minus what you paid for the setup -- in this case: $2250 minus $2040. If price is below the short call strike, but still above your cost basis, you still make money; the short call expires worthless (for which you book a profit), but the profit you made from the short call exceeds the price decline of the stock.

As with any covered call, however, you can lose money if price declines below the cost basis of your setup. In that event, I continue to sell calls against my stock, further reducing my cost basis in my shares until I'm able to exit the trade for scratch or a small profit.

OPENING: MIFI COVERED CALLI'm working a lot of these out of a "weenie" account, so a lot of these are going to be "weenie" sub-$10 plays ... .

Metrics:

Bought 100 Shares at 3.30

Sold Oct 21st 4 call

Whole Package: 2.95 db (2.95/share is my cost basis)

Max Profit: $105 (if called away at $4)

ROC: 35.6%

OPENING: SRPT JAN 2017 8 LONG PUTShooting for an .08 ($8) debit fill here. It's a lotto trade (which I hardly ever do), but I think that the drug will ultimately not be approved.

The potential profit is $795/contract, but that's if the stock goes to "0." Additionally, it will only "play out" if there is news prior to expiry. Otherwise, it'll stay way up here.

Things point to 140 for now (2nd month continuation)Looks down to the 140 area for a test. However as long as the orange or blue trends hold, the upwards trend is still intact IMHO.

short call spreads above 165 in Dec or January might be a good idea. I would buy any puts as downside seems limited for the moment and option volatility might decline during a sell off diminishing returns on long option strategies.

1x2 put spreads 10 to 15 cents wide for flat selling the 2 buying one over two month could be good IMHO

BOUGHT NE COVERED CALLBought shares at 6.07; sold the Sept 30th 6.5 call; filled entire package for a 5.78 db; max profit $72 (if called away at 6.5) (12.5% ROC).

NVAX TRADE UPDATEI figured I'd clean up this setup a little bit on the chart to show what's going on with this trade a little more clearly, since we're running into opex, and I'll have to do something with it here shortly. I also for mapping out what I'm going to do if price does certain things relative to my cost basis and original stock purchase price.

The trade originally started out as a "Plain Jane" covered call, where I bought shares at 7.54 and sold the Sept 16th 8 call for something like a 6.39 debit (so my cost basis in the shares at that point was 6.39/share). I proceeded to sell the Sept 16th 5 short put to further reduce cost basis in my shares, as well as to sell some premium in this unusually high implied volatility underlying (I filled the short put for an additional .67 ($67)/contract credit. When, after all, can you get >$50/contract credit for a somewhat far out-of-the-money short put in an <$10 underlying -- rarely. After selling the put, my cost basis in the shares would be 6.39 minus .67 or 5.72/share.

Currently, the 8 short call is valued at .72 ($72) (it was originally $115), and the short put is valued at .25 ($25) (originally, $67).

Rolling into expiry, I'm looking to take the short put off at near maximum profit (.05 or less). If price finishes above $8 at expiry, my shares will be called away at $8, and I'll be out of the trade. However, what should I do if price either finishes (a) between my stock purchase price and the short call or (b) price finishes below my stock purchase price, but above my original cost basis for the covered call (6.93/share)?

If price finishes "between", I'm likely to just treat the trade from that point forward as a straight "speculative long" stock play and set a stop loss for my shares at break even and then let the trade ride. The reason why I would probably not continue to sell calls against and set a stop loss on the stock is to avoid the scenario where I would get stopped out on the stock and have a naked speculative short call hanging out there which could get painful if price whips higher on news (which is due out sometime in the 4th quarter and most likely at a presentation NVAX is going to give in mid-October).

If price finishes lower than what I paid for the stock originally, but above my cost basis for the original covered call, I'm likely to just close it entirely out, having made profit on the short put and on the covered call setup ... .

BOUGHT CLF COVERED CALLBought shares at 6.04; sold the Sept 30th 7 call; filled the entire package for a 5.85 db; $115 max profit if called away at 7 (19.7% ROC).

TRADE IDEA: IWM OCT 21ST 112/116/126/130 IRON CONDORWith VIX finally breaking 15 here, I need to strike while the iron is hot ... . The instrument of choice -- IWM, the broad index exchange-traded fund (as compared to SPY, DIA, QQQ) with the highest implied volatility currently ... .

Metrics:

Probability of Profit: 52%

Max Profit: $127/contract

Max Loss/Buying Power Effect: $273/contract

Break Evens: 114.73/127.27

Notes: Naturally, I'm going to watch the markets early next week to see if there's continuation in this dip. If there is, I may hold off slapping something on for even higher volatility. Heck, I waited eight weeks or so for VIX to break 15; I can wait a little longer if it's going to go higher ... . The natural alternative to this setup would be RUT with similar strikes -- i.e., 1120/1160/1260/1300 ... .

OPENING: GPRO OCT 21ST 13 SHORT PUTHere, I'm just trying to suck in a little bit of premium without being all in on the stock ... . (Filled for a .64 ($64)/contract credit).

As usual, I'm selling the strike nearest 30 delta.

I'm fine with getting assigned at 13 (after which I'd proceed to sell calls against), but would naturally prefer cheaper, so will keep an eye out for opportunities to roll down and out for credit and duration if I get a shot at it. Naturally, the Oct 21st expiry is around earnings, so that's something I'll have to keep in mind ... .

BOUGHT WLL COVERED CALLBought shares at 7.50; sold the Sept 30th 8 call; filled for a 6.93 db; max profit $107 (if called away at 8) (15.4% ROC).

Not to jinx it, but it's highly likely that I will be unhappy with one or more of these little fellas that I put on today ... .

TRADE IDEA: AMD COVERED CALL/NAKED SHORT PUTMy "guess" is that AMD will not hold onto this level (I briefly considered going "monied" with the short call with the covered call setup, selling the 7 strike instead of the 8). However. implied volatility is fairly high here (64.6%), and my mechanical approach to most of these setups is basically to "ditch the guessing" and pull the trigger; price will go where it goes ... .

Covered Call Metrics:

Buy 100 Shares at 7.51

Sell Oct 21st 8 Call

Whole Package: 6.93 db (off hours; 6.93 will be my cost basis in the stock)

Max Profit: $107 (if called away at 8)

ROC%: 15.4%

Notes: As an alternative, I looked at selling a put in the Oct 21st expiry below current price. The Oct 21st 7 short put, for example, currently offers up .54 ($54) in premium at the mid. The notion there would either be to (a) keep the premium if AMD finishes above $7 at expiry; (b) look to be put the stock at $7 if it doesn't; or (c) roll the short put down and out for additional credit if price breaks $7. Anything below the $7 strike in the Oct 21st expiry won't offer you much premium at the moment (e.g., the 6 strike offers .25 at the mid, which approaches "not worth it"). At NY open, I'll probably just "flip a coin" as to whether I go with the naked put or the covered call.

WITH VIX SUB-15, PREEM SELLING OPPS ARE OUSTIDE BROAD INDICESAs I've posted several times before, my preference generally is to (1) sell premium in broad-based index instruments (e.g., SPY, IWM, QQQ, SPX, RUT) if VIX > 15; and (2) if VIX < 15, look for premium selling opportunities in non-index exchange traded funds with implied volatility of >35% and/or individual underlyings with implied volatility of >50% and where the implied volatility percentage is in the 70th or greater percentile for the preceding 52-weeks. Unfortunately, VIX <15 here and underlyings -- whether exchange traded funds or individual underlyings -- with implied volatility both in the 52-week 70th percentile and above 50% implied volatility are absent here.

Consequently, I am "settling" for mere >50% implied volatility plays in exchange traded funds and in individual stocks. This isn't ideal, but I'm playing these small, keeping quite a bit of powder dry in the event that volatility does pick up at some point in the weeks ahead.

There are some opportunities out there, and they're where they've been for the past several weeks: in gold, miners, oil and gas, and biotech. The top IV individual stocks with liquid options are: NVAX (195.0) (biotech); RTRX (132.4) (biotech); GNW (100.3) (financial); WLL (80.5) (O&G); CLF (76.1) (iron ore/mining); AG (75.6) (silver miner); CHF (73.9) (oil and gas); AKS (70.0) (steel); EGO (62.7) (gold miner); VRX (61.9) (biotech); AMD (61.8) (semiconductor); and AUY (61.6) (gold miner). The top IV exchange traded funds are GDX (43.7) (gold miners); and XME (39.2) (mining).

And, because of the "smallness" of many of these underlyings (many are under $10), I'm taking a slightly different strategic tack here, either doing covered calls from the outset or selling puts as a precursor to a covered call, the notion being in the later case to either keep the premium or get put the stock at a lower price, after which I'll sell calls against. Things like short strangles and iron condors simply will not yield enough premium on setup to bother with in most of these smaller stocks.

In the one play that I currently have on in XME (see post below) that I could have strangled, I opted to just naked short put to leave open the option of covered calling it if I get put the stock or rolling the short put down and out for additional duration and credit should the underlying move that way rather than dealing with the hassles of call side risk. Naturally, these options would still be open to me were I to strangle, but doing just the short put relieves me of call side risk (there's always trade-offs).

For me personally, I'm looking to move into plays involving something other than gold, miners, or oil and gas, since I have quite a few of those on already. Unfortunately, this makes for pretty slim pickings in my little list, with the potential focus being on AMD and (ick) VRX. I'm already in NVAX and GNW, and I'm not fond of RTRX (it only offers monthlies and currently the Oct monthly expiry only offers 2 1/2 wide strikes; naturally, that may change ... ).

PREMIUM SELLING: TWLO OCT 21ST 45 SHORT PUTI generally don't like to ride broncos right out of the stall, but I might make an exception here ... .

This is because the Oct 21st 45 short put is currently bid 3.00, ask 3.80 (mid 3.40). That's $340 in premium for a one contract 58 and change underlying ... .

Alternatives:

Sept 16th 45 short put: bid .95, ask 1.11, mid 1.03.

Oct 21st 40 short put: bid 1.65, ask 2.10, mid 1.87.

I wouldn't be looking to acquire here, but rather to just squeeze some premium out and would look to take it off at 50% max profit. Broncos can make for an awfully rough ride ... . Ordinarily, I'd strangle this, but am hesitant to take on potential upside risk if this becomes a rocket sled sorta thang ... .