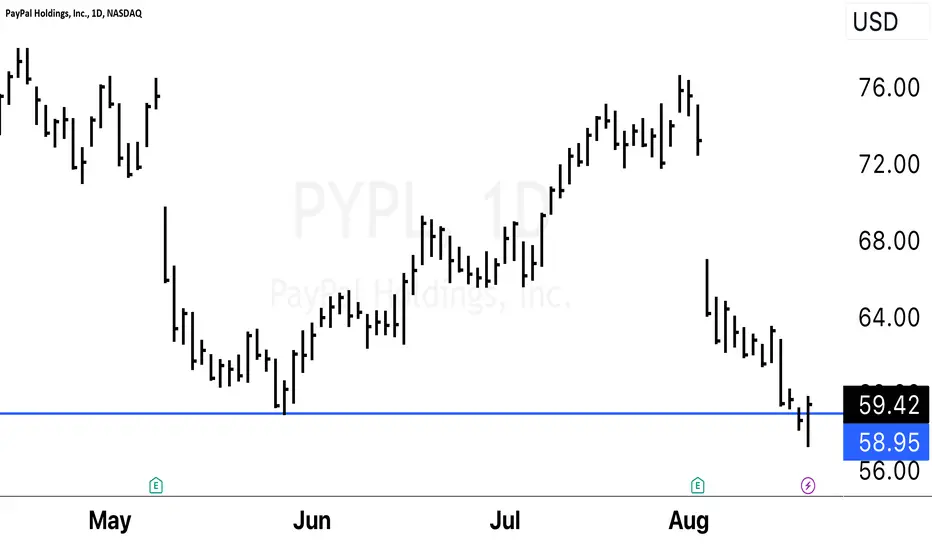

Paypal Close To Dropping Through $50!Apple's foray into the payment industry is impacting PayPal's stock price, causing concern among investors. Analysts are closely monitoring PayPal's third-quarter earnings report to assess the company's current standing and future prospects. Despite projected earnings of $1.16 per share, PayPal's stock has been struggling, experiencing a 32% drop since the beginning of the year, despite positive earnings reports.

So far this year, the stock has declined by 28%, with a 13% drop in October alone. This downward trend raises doubts about PayPal's ability to recover, especially since it lacks strong historical support levels. While the stock may find some support around the $50 mark, a significant rebound is necessary for a complete recovery. In fact, to reach its all-time high, the stock would need to surge by a staggering 505%.

Another significant obstacle is surpassing last year's low of $66. The upcoming third-quarter earnings report, scheduled for release on November 1st, will be crucial in determining PayPal's near-term outlook and its ability to navigate the challenges within the industry.

Paypal

PayPal: Turbulent Journey, Promising FutureI am a big supporter of PayPal but I believe its share value will get worse before it gets better. According to its Q2 2023 results, the online payment company experienced a deterioration in its liquidity with a cash ratio difference (cash/total current liabilities) of -0.04 when compared to its Q2 2022 results. The Q3 2023 Earnings Call taking place on Wednesday (1 November 2023) should set the tone for what to expect in the coming months, a steeper drop in share price or a much desired recovery.

PayPal has had a rocky year with the retirement of its veteran CEO, Dan Schulman, who was officially succeeded by Alex Chriss last month. Because Schulman's departure was planned and not sudden, the change in leadership is not a concern for me. The online payment giant also recently launched its own stablecoin showing its willingness and capability to evolve with the times. All-in-all, I believe PayPal's shares have been mostly rocked by factors outside of its direct control (rising treasury yields, pandemic lockdowns lifting, recession fears, etc) so I am anticipating the Q4 2023 to be a pivotal moment as I believe that's where we will see how Chriss has managed the company.

Despite the expected turbulence I am going to load up on LEAPS calls as I believe this company is extremely undervalued and is due for a strong recovery once the current macroeconomic disturbances subside. If the price continues to slip, I can see us hitting a support around $40 which will be the lowest the stock has been since February 2017. While this would be difficult to stomach, it offers an exceptional purchasing opportunity. A potential near-future recovery to the $58.50 level is also possible; $65 would be the next stop if the $58.50 ceiling is surpassed.

Speculative foresight: noting Elon Musk's prior history with PayPal and his long-term desires for operating an online bank (a desire he has expressed exercising with the newly acquired Twitter, now X, platform), I believe we can expect an attempted merger or acquisition from Musk once he has extinguished the current fires at Tesla and X. In my opinion, an attempt to takeover PayPal would attract high volatility which could launch PayPal's shares to prior highs. This is all speculation of course and probably will not occur for several years, if at all.

NASDAQ:PYPL

Can I Venmo You?Long where it began. Profit targets at dark green lines. Be mostly out at orange lines. Let the rest ride. Money sent.

PayPal Becoming Extremely Undervalued & Possible Bitcoin Plan.

I've been watching PYPL for the last year completely free fall out of logic.

1. I don't think PayPal is going bankrupt as they have 435,000,000 Active Accounts

2. They've been hit with the DeFi Fear selling resorting to testing out Ethereum.

3. They're now realizing Ethereum is garbage and makes zero sense meaning PayPal is closer to turning out and adopting a Bitcoin / L2 solution as PYUSD / Stable coins do have a place in this world.

Now its self explanatory I'd like people to remember what happen when Michael Saylor plugged (MicroStrategy) into Bitcoin it sparked a new life into the company.

PayPal? .435,000,000 Accounts? .Extremely undervalued?. Sitting at a 14.11 Ratio?. STDEV basically screaming oversold?.

Either PayPal is secretly bankrupt or the price needs to correct up.

I really do not understand what has happen to PayPal's share price it really reminds me of NASDAQ:META where you get this outflow of investors unable to see the main value here is the USERS they have not the business.

PayPal and META.

Paypal - A Make or Break Moment 1st Nov Paypal - NASDAQ:PYPL

Earnings release on 1st Nov 👀 and two chart patterns are going to hold or break....

Potential Falling Wedge (blue) could be about to hold or break down, along with a potential positive divergence (purple) which needs to hold here also.

I continue my DCA into these lows. Position size is still on the small side and i am DCA'ing with an investment mentality. Setting additional bids at $53.30

PUKA

#paypal #PYPL is looking tastyA long term falling channel and forming wedge , well accumulated. Good.

NOT FINANCIAL ADVICE.

PayPal - Bullish Set Up on the horizon?PayPal faces a long downtrend with a additional big drop down after the last numbers. Again there is a attempt to find a bottom and there cold be a possible rebound with targets at 82 $ and above 100$ due to an cup and handle like figure as well as a not yet active Wolfe Wave. Not a long yet but it could turn into it.

PYPL, Since Massive BEAR-MARKET-Scenarios, What to Expect Now!Hello There!

Welcome to my new analysis about PYPL on several timeframe perspectives. Since PYPL formed the boom highs it showed up with a massive bearish price-action to the downside dumping over 80% and liquidating over 400 Billion long positions. Now, a huge consideration is if this PYPL bear-market dump is going to continue and accelerate further bear market price-action momentum spikes towards the downside. PYPL since August already moved on with the next dump towards the downside on the local term firstly, this can accelerate on the global term also.

PYPL is now forming this ever so crucial bear-flag on the local 4-hour timeframe perspective with the initial wave A that already setup and now PYPL is forming the next ascending-wedge within this local wave-count. This means once the wave B has formed with the completion of the local ascending-wedge it will accelerate bearish dynamics and move forward with the wave C to dump the next 25% firstly on the local term. A continued CBDC implementation acceleration and the potential for a gold-back currency to emerge are likely to increase bearish scenarios for PYPL.

Especially, on the global term PYPL is building a much larger formation here which is actually a head-shoulder-formation. With the right shoulder and head already being completed and now with a likely dump that is going to setup next this will accelerate the bearish price-dynamics and continue with the completion of the right shoulder to complete the whole head-shoulder-formation. If this scenario shows up it will accelerate the massive bearish long liquidations to another 80% bearish price-action and 500 Billion long-liquidations towards the downside.

The next times will be highly crucial for PYPL as they are going to show the importance of the wave-count on the local that is also likely to accelerate the dynamics on the global as well. If a gold-backed currency implementation is going to start within the next times this is also going to increase bearishness for PYPL. Therefore, it will be a highly important dynamic to watch out as the dynamics shifting into a more CBDC and gold-backed currency market condition it can turn out as a huge signal in PYPL to consider.

In this manner, thank you everybody for watching the analysis, support from your side is greatly appreciated.

VP

PYPL | PayPal or MemePal?PayPal Holdings has emerged as a leader in the digital finance landscape, leveraging its consistent growth and strategic initiatives. PYPL has attracted unreasonably high valuation multiples post-pandemic, but the recent crash of around 80% from all-time highs, in combination with its growth outlook, portrays a compelling deep-value play for long-term investors.

This article explores the company's strategic initiatives, development toward market share and competitive edge, the new CEO's impact, the valuation outlook, and a technical assessment, which ultimately supports a strong buy rating for the stock in the next 24 to 36 months.

In today's ever-evolving digital landscape, understanding web traffic dynamics is crucial for any business aiming to stay competitive. PayPal demonstrates a robust trajectory in its web traffic and market presence, positioning itself as a dominant player in the finance sector.

Over the past decade, PayPal's organic traffic has grown steadily, with a Compound Annual Growth Rate (CAGR) of 17.27%, reaching monthly organic traffic of 14.3 million. The sustained growth highlights its strong online visibility and brand recognition.

However, its organic traffic dropped significantly in early 2022 from a level near 18 million per month, a nearly 20% drop from the all-time high due to fierce competition in the industry. Nonetheless, considering recent traffic trends (desktop users) on PayPal.com, the platform's total traffic has surged by 8.05% compared to the previous month, suggesting that PayPal continues to attract and engage a widening user base.

PayPal's web traffic has demonstrated remarkable growth of 9.65% in total visits in the last month, suggesting an expanding user base and heightened online engagement. Correspondingly, unique visitors have risen by 7.91%, reinforcing PayPal's capacity to attract new audiences consistently.

The average user interaction on PayPal's platform is equally remarkable, with users viewing an average of 3.3 pages per visit. This figure, which has increased by 0.78%, suggests that users actively explore the platform's offerings, potentially indicating higher interest and engagement.

Furthermore, the average visit duration is an impressive 5 minutes and 34 seconds, marking a significant 5.03% improvement. This underscores the platform's ability to capture user attention, facilitating extended interactions conducive to achieving business objectives.

Finally, PayPal's diligent efforts are reflected in its bounce rate, which has decreased by 5.38% to 29.47%. A lower bounce rate indicates improved user engagement and content relevance, implying that visitors find the content and offerings on PayPal's platform more aligned with their expectations.

A comparative analysis with a close competitor, Stripe, offers further insights into PayPal's standing. While both platforms have experienced growth in visits (PayPal: 9.65% vs. Stripe: 9.18%) and unique visitors (PayPal: 7.91% vs. Stripe: 5.37%), PayPal maintains a significant lead in both metrics, indicating a stronger market presence. Additionally, PayPal's higher pages per visit (3.3 vs. Stripe's 1.7) further emphasize its ability to capture and retain user attention

Despite a gradual slowdown, the company maintains a substantial user base and has demonstrated a consistent user growth trend in recent quarters. From Q1-22 to Q2-23, active accounts remained relatively stable, ranging from 429 million to 431 million. This includes user and merchant accounts (35 million), contributing to PayPal's versatility as a payment solution for a broad spectrum of users, from individuals to businesses. However, the YoY growth rate has steadily declined, indicating a potential saturation in its market reach. Over this period, YoY growth dropped from 9% to below 1%, signaling the weakness of its strategies to reignite expansion.

Considering the broader industry landscape, PayPal's growth outlook is influenced by the Global Payment Processing Solutions Market's projections. The market is anticipated to experience robust expansion, with an estimated USD 63.48 billion growth between 2022 and 2027. This growth trajectory translates to a CAGR of 12.18%. Despite slowing growth, PayPal's current user base and market share position it favorably to tap into this market growth.

To secure growth, PayPal prioritizes customer retention and engagement within its existing user base to counteract the sluggish YoY growth. This includes enhanced personalized offerings, rewards, and seamless experiences. PayPal also explores untapped markets and demographics geographically and among underserved segments. For instance, if PayPal uses emerging technologies such as blockchain and cryptocurrencies to expand its service portfolio, it may attract tech-savvy users and capitalize on the growing interest in decentralized finance.

PayPal has demonstrated consistent growth in its payment transactions, bolstered by its expanding active account base. Specifically, in Q2-23, PayPal reported processing 6.074 billion payment transactions, representing a 10% YoY increase but with a slower growth rate. A closer look at Transactions per active account (TPA) that reached 54.7 reveals a 12% YoY growth attributable to Braintree's transaction volume, a subsidiary playing a pivotal role in driving the company's transaction growth.

PayPal had nearly 55% market share in 2020, but the fierce competition has taken significant market share away from the fintech conglomerate. However, there are positive signs of stabilization, and PayPal currently holds a market share in the global online payment processing industry, with a commanding position of 40.52% as of July 2023, which stabilized its market share YoY (July 2022: 41%) and indicated PayPal's ability to preserve its market share.

The ongoing transition to electronic payments and increased e-commerce, which the coronavirus epidemic further hastened, had boosted PayPal's growth. Although there are niches in the acquiring market, PayPal is the undisputed e-commerce leader, creating a protective moat.

A few new rivals have emerged due to what appears to be a concentration of fintech innovation in the e-commerce sector, even though growth slowed in 2022 as the company overcame some headwinds. The company could face additional headwinds if the economy worsens.

The ongoing global shift towards e-commerce presents a substantial growth avenue for the entire industry, including PayPal. Therefore, given its platform's relative ease and security, PayPal will continue to be a preferred partner in the online world, yet, the company's market position does not allow it to impose terms on other participants or eat up an ever-increasing market.

PayPal's introduction of a fully backed stablecoin, PayPal USD (PYUSD), has the potential to bring about significant long-term benefits to the company from a fundamental perspective.

This move aligns with the ongoing shift towards digital payments, blockchain technology, and the expanding Web3 ecosystem. By launching a stablecoin that's 100% backed by US dollar deposits, short-term US Treasuries, and similar cash equivalents, PayPal aims to bridge the gap between traditional fiat currency and the emerging world of digital assets.

Firstly, PayPal's stablecoin can enhance its role in the evolving digital payments landscape. As the exclusive stablecoin within the PayPal network, PYUSD offers a seamless method for users to transition between fiat and digital currencies. The combination of PayPal's established payments expertise and blockchain's efficiency can facilitate faster transfers, reducing friction for inexperienced payments, remittances, international transactions, and more. As a result, this will likely strengthen PayPal's appeal to consumers, merchants, and developers seeking convenient, low-cost, secure payment solutions.

Furthermore, by leveraging the Ethereum blockchain and adhering to transparency standards, PayPal USD can tap into the growing Web3 community. This opens doors for integration with external developers, wallets, and web3 applications, boosting adoption and usability. The compatibility with Web3 environments positions PayPal as pivotal in expanding digital assets into mainstream use cases.

Interestingly, PayPal's focus on regulatory compliance and its partnership with Paxos Trust Company, a licensed trust company, bolsters confidence in the stability of PayPal USD. Regularly publishing reserve reports and third-party attestations will enhance transparency, reassuring users about the backing of the stablecoin. Finally, this adherence to transparency and regulation will enhance PayPal's credibility and trustworthiness in the digital finance space.

While the loss of the lucrative eBay relationship significantly impacted margins, the company's focus on cost-cutting and long-term strong growth will eventually drive solid margin expansion in the long run.

PayPal is decreasing expenses as its growth slows to maintain its adjusted operating margins. Therefore, PayPal anticipates its adjusted operating margin to improve by "at least" 100 basis points in 2023.

However, PayPal's net margin of 14.27% places it competitively in the industry, and the improvement is due to its strategy to improve transaction margin dollars. As it is management's long-term focus, net margin may improve considerably, providing a solid foundation for its long-term financial outlook.

On a trailing 12-month basis, PayPal has returned $4.9 billion to stockholders via repurchases (buybacks of 63 million shares), highlighting a focus on enhancing shareholder value. This practice continued in Q2-23, as PayPal repurchased approximately 22 million shares at an average price of $68.89 per share, totaling $1.5 billion. The ongoing trend of buybacks signifies the company's confidence in its growth trajectory.

Since becoming an independent company in July 2015, PayPal has generated approximately $29 billion in free cash flow (FCF). This underscores its financial strength and capacity to fund various growth initiatives. The allocation of $19 billion towards share repurchases and $13 billion for acquisitions and strategic investments underscore its focus on rewarding shareholders and driving strategic expansion.

Over five years, PayPal has consistently reduced its Diluted Weighted Average Shares Outstanding to 1.14 billion. This trend indicates potential benefits in earnings per share for existing shareholders, given a constant or growing net income.

PayPal's focused efforts on new product innovations, efficient A/B testing, and enhanced time-to-market capabilities are driving significant improvements in its operational efficiency and customer experience.

By consistently delivering on its roadmap and investing in platform infrastructure, tools, and AI-driven software development processes, PayPal is establishing a competitive edge. The company's commitment to continuous experimentation, with over 300 experiments launched in the year's first half, leads to incremental customer benefits and drives cumulative improvements in key metrics, including branded checkout growth.

PayPal's expansion into the buy now, pay later space and innovations like pre-approved amounts for consumers contribute to accelerated traction in this sector. The company's efforts in onboarding and introducing new experiences are leading to higher engagement and lifetime value among its customer cohorts.

One of PayPal's strategic initiatives is the rollout of passkeys in the US and Europe, streamlining the checkout log-in experience and enhancing authorization rates. This initiative positions PayPal to maintain and extend its lead over competitors, promoting continued growth.

Moreover, PayPal's focus on differentiated wallet experiences for both PayPal and Venmo users aligns with the company's belief that unique and scaled data sets are essential for leveraging AI's power to drive actionable insights and deliver differentiated value propositions to customers.

Internally, experimenting with an AI-driven PayPal assistant indicates the company's commitment to harnessing AI technology to enhance customer interactions and experiences. By envisioning the integration of this assistant into its consumer app, PayPal is poised to elevate its service offerings further.

In addition, PayPal's growth in the Payment Service Provider (PSP) business (nearly 30% on a currency-neutral basis), strong partnerships with major tech companies, and expansion of value-added services internationally are contributing to the company's robust performance. The rollout of PayPal Complete Payments, a PSP merchant solution, has garnered substantial interest and participation from key channel partners.

PayPal is effectively implementing PayPal Complete payments with various channel partners (Adobe, LightSpeed, Recurly, Shift4, Shopify, Stacks Payments, UltraCare, Wix, and WooCommerce). Notably, over 25 channel partners are slated to go live by 2023. Based on offering a modern and streamlined checkout experience, PayPal enables numerous SMB merchants to access its innovative solutions. Finally, the company's ability to leverage its platform capabilities and AI models is key to its market leadership.

The appointment of Alex Chriss as the new President and CEO of PayPal holds significant support for the company's long-term fundamental growth. Chriss brings extensive experience in technology, product leadership, and a proven track record of driving growth in the small business and self-employed segments. This background aligns well with PayPal's role as a digital payments platform and its focus on serving consumers and merchants.

Under Chriss's leadership, Intuit's (INTU) Small Business and Self-Employed Group experienced substantial growth, with a CAGR of 20% and 23% in customers and revenues, respectively. This success indicates his ability to foster growth engines within business segments and establish market-leading platforms. His leadership overseeing Mailchimp's acquisition demonstrates his ability to expand a company's capacity and customer base.

PayPal's stock is at a pivotal juncture from a technical standpoint. The recent formation of a double bottom around $59.50, marking a six-year low, carries significance. Notably, the pattern was accompanied by a bullish divergence in the Relative Strength Index (RSI), hinting at a possible long-term shift towards a bullish trajectory. In short, the technical setup implies the potential for a vital price reversal.

PYPL, fintech, stablecoin, crypto, stripe, PayPal stock, PYPL stock, PayPal stock price, PayPal stock news, PayPal stock forecast, PayPal stock analysis, PayPal stock performance, PayPal stock market, PayPal stock today, Buy PayPal stock, Sell PayPal stock, PayPal stock quote, PayPal stock symbol, PayPal stock value, PayPal stock chart, PayPal stock trends, PayPal stock investing, PayPal stock outlook, PayPal stock information, PayPal stock predictions.

Looking ahead, a notable resistance level at approximately $76.55 has materialized during the ongoing accumulation phase. A decisive breach above this resistance is pivotal. Once breached, this could trigger a markup phase characterized by robust bullish momentum. The stock may experience rapid appreciation during this phase.

Delving into historical data and projecting forward, there is potential for PayPal's stock price to scale heights and reach an all-time high of over $300 within the next 3-5 years. The bullish momentum highly depends on the company's fundamental progressiveness and the favorable outcomes of its strategic initiatives.

personally I shorting PYPL since it was 255 and here we are at 59$ and despite facing challenges such as shifts in web traffic, competition, and evolving market dynamics, PayPal has showcased resilience and a commitment to growth.

Disney - Is Your Compass Upside Down?On trading social media, Disney has been the target of moonboys for quite a while.

For some reason, whenever a stock is in a landslide and doesn't go up, everyone gets it in their head that they're going to BUY THE CALLS and catch the next MOTHER OF ALL SHORT SQUEEZES.

And this is because you want to gamble on a single day candle, which results in you blowing your account, and then you stop using TradingView and can't have fun anymore.

Disney, fundamentally, is a company that may not have any future whatsoever in a society that returns to mankind's traditions.

For so many years, it has been pushing a warped and depraved culture at both its parks and via its broadcasting networks. It was even an entertainment industry leader in onboarding the Chinese Communist Party's Zero-COVID social credit edicts.

And this is a problem if you want to get long.

They always say "zoom out," and so let's look at yearly candles:

8 months of price action for 2023 so far indicates that we've probably just been painting the wick portion of a year that will break the 2020 COVID low.

And the first place you find support below the COVID low is at $40.

"Sure, sure. But it's Disney. It's the stock market. EVERYONE KNOWS it's going up. Bears always get #rekt LOL."

"Bear flags" and "bull flags" are astrology and don't exist. But what does exist is when an equity spends more than a year in an area it should have bounced from and simply doesn't go up, which is what we see on the monthly.

But the contrary, on the Weekly, there is a problem for bears, which is the August of '22 high at $126.

And so there is a potential that tomorrow's earnings call actually results in a raid to $80 that actually produces a bullish buying opportunity with a target of $126.

The problem is, the "JPM Collar" has the world's most significant bank long on SPX 4,200 puts that expire September 29 that have literally been under water every second of every day since they were bought at the end of Q2.

SPX/ES - An Analysis Of The 'JPM Collar'

However, I note in my recent SPX call:

SPX - The Sound of a Shattering Iceberg

And a recent Nasdaq call

Nasdaq NQ - Is It Time To Sell The Rip?

With CPI pending on Thursday morning, what happens tomorrow is really significant.

That although I suspect our index tops to get raided, the problem is, are you going to see $40+ on Disney in a time frame of less than 3 weeks?

September is likely to be something of a "chilly autumn" for equities markets with the way everything is set up, including the SOXS bear semiconductor ETF and the VIX.

If there's to be anymore rally, that rally may only come in Q4.

And thus, that would mean for Disney that a likely scenario would be a raid on the lows from earnings and even more bearish consolidation, with the $126 target being left for the beginning of Q4.

This stock is a lot like Verizon and T-Mobile. It's better left not bothered with until it starts to show you signs that a bank or a fund really wants to rip it bigly in one direction or the other.

There's lower hanging fruit and greener pastures out there to trade.

PayPal added to the watchlistShares of PayPal lost nearly 82% of their value since the top in July 2021, and judging solely by this metric, one could consider the stock cheap. Nonetheless, there is more to it. In 2022, PayPal saw its revenue increase by 8% on a yearly basis and transaction volume grow by 16%. In addition to that, the company processed 22.3 billion payments and $1.36 trillion in total payment volume, with active accounts rising by 2% YoY to 435 million. However, its operating margin dropped by 10% and net income by 42% (using GAAP accounting).

In the first quarter of 2023, the company delivered better results compared to the first quarter of 2022, with net revenue growing 9% YoY, operating income by 41% YoY, earnings per share by 62% YoY, and net income by 56% YoY. As for the second quarter of 2023, the company reported a further increase in net revenues by 7% YoY, operating income by 48% YoY, and earnings per share by 414% YoY. In this quarter, PayPal generated $1.029 billion in net income compared to the loss of $341 million a year earlier.

Based on some of the fundamental improvements and cheap valuation, we think PayPal is growing increasingly attractive and worth watching out for. However, we would like to emphasize that the stock keeps making lower lows and lower highs. Thus, entering the trade is still quite risky. One alternative to approach this situation is to wait for a price to break above the upper bound of the channel and place a long entry there with stop-loss below the bound.

Illustration 1.01

Illustration 1.01 displays the daily chart of PayPal and its losses since the top in July 2021.

Technical analysis gauge

Daily time frame = Bearish

Weekly time frame = Bearish

*The gauge does not necessarily indicate where the market will head. Instead, it reflects the constellation of RSI, MACD, Stochastic, DM+-, ADX, and moving averages.

Please feel free to express your ideas and thoughts in the comment section.

DISCLAIMER: This analysis is not intended to encourage any buying or selling of any particular securities. Furthermore, it should not be a basis for taking any trade action by an individual investor. Therefore, your own due diligence is highly advised before entering a trade.

Target 66Following daily chart and got a long signal for the short term.

TP1 - 66.14

TP2 - EMA100

TP3 - 71.83

SL. - 58.15 , wait for daily candle to close.

PYUSD - The PayPal StablecoinHi Traders, Investors and Speculators of Charts📈📉

PayPal announced yesterday on August 7, 2023 that it has launched a U.S. dollar stablecoin, called PayPal USD (PYUSD) . PYUSD is fully backed by U.S. dollar deposits and short-term U.S. Treasuries, and is issued by Paxos Trust Company. It is available to PayPal customers in the United States with PayPal Balance accounts.

PayPal has partnered with Paxos to launch PYUSD. Paxos is a leading blockchain infrastructure company that specializes in stablecoins. Paxos also issues the BUSD stablecoin, which is used by Binance. PYUSD was first announced in January 2022, but its launch was delayed due to regulatory concerns. However, PayPal has since received approval from the New York State Department of Financial Services to issue PYUSD.

PYUSD is currently valued at $1.00 per token. It can be used to buy, sell, hold, and transfer funds on PayPal. It can also be used to make payments to merchants that accept PayPal.

PayPal has been crypto-friendly for some time. In addition to PYUSD, PayPal also offers four other cryptos: Bitcoin, Bitcoin Cash, Ethereum, and Litecoin. PayPal customers can buy, sell, hold, and transfer these cryptocurrencies on the PayPal platform.

PayPal's launch of PYUSD is a significant development in the cryptocurrency space. It is the first major financial technology firm to launch its own stablecoin . PayPal's move is likely to boost the adoption of stablecoins and cryptocurrencies in general.

💭 It's interesting to see how the fundamentals tend to follow the chart or vice versa. When we analyze the PayPal chart, we see a definitive completion of a bearish trend / downward cycle. According to Wyckoff Method and other market phases, the next cycle is the upward cycle / bullish phase. And so, this news comes at just the right time to kickstart a new market cycle!

_______________________

📢Follow us here on TradingView for daily updates and trade ideas on crypto , stocks and commodities 💎Hit like & Follow 👍

We thank you for your support !

CryptoCheck

NASDAQ:PYPL

Symmetrical triangle hereYou know what it means, a good company, good results, waiting for a CEO (Elon Musk maybe) making that part of the 20 years plan for X, but, we have that Symmetrical triangle with a potential 60% in the next months, and two huge falling wedges., Why PYPL have now a crypto?, the answer is X!

$PYPL Double Bottom Bullish closeNASDAQ:PYPL Double Bottom Bullish close

It sounds like you're discussing technical analysis concepts in the context of trading. A "double bottom" is a bullish reversal pattern that occurs after a downtrend and is characterized by two consecutive lows at a similar price level, followed by a breakout above the pattern's neckline. This pattern suggests a potential reversal from the downtrend to an uptrend.

A "false breakdown" occurs when a price breaks below a support level but quickly reverses and closes back above it. This can be interpreted as a bullish sign, indicating that the selling pressure wasn't sustained, and buyers stepped in to push the price back up.

The idea that "the best moves come from failed moves" is a common adage in trading and investing. It suggests that when a market or a security initially breaks out or breaks down and then reverses, it can lead to strong price movements in the opposite direction. This is often attributed to the idea that traders who were positioned on the wrong side of the initial move are forced to close their positions, contributing to the momentum in the opposite direction.

It's important to note that while these concepts are commonly discussed in trading circles, they are not foolproof strategies. Technical analysis is just one approach to understanding price movements in financial markets, and it should be used in conjunction with other forms of analysis and risk management strategies. Markets can be unpredictable, and there is no guarantee that any pattern or signal will always lead to a profitable outcome.

Buy PYPL @ 73-74 Buy PYPL at 73–74. with a stop loss at 56.95. This trade has a positive risk-reward ratio.

PayPal Long?PYPL has been a slow grinder lower. Each time it gains momentum it somehows manages to lose it.

The only positive thing about this chart is the long divergence that is occurring between price & RSI.

When will this divergence bear fruit? Anyone's guess but you do have it on the daily, Weekly & Monthly time frame.

$PYPL PayPal Double BottomThe main reason why I like NASDAQ:PYPL PayPal it has a Double Bottom another one of the reasons why I am starting a small starter position is because Jim Cramer hates the stock.

1. Business Model:

PayPal is a leading digital payment platform that offers a range of online financial services, enabling individuals and businesses to make payments, transfer money, and conduct transactions electronically. It serves as a bridge between buyers and sellers in the digital marketplace.

2. Revenue Streams:

PayPal generates revenue primarily through transaction fees charged to merchants for processing payments, as well as fees for certain value-added services. These services include PayPal Business Solutions, Venmo (a peer-to-peer payment platform), and Xoom (a digital money transfer service).

3. User Base and Market Reach:

PayPal boasts a vast user base, with its services available in more than 200 countries and supporting multiple currencies. The platform is widely used by consumers, businesses, and merchants for various online financial transactions.

4. Acquisitions and Diversification:

PayPal has strategically acquired several companies to diversify its offerings and expand its market presence. Notable acquisitions include Venmo (a social payments platform), Braintree (a payment gateway), Xoom (a digital money transfer service), and Honey (a browser extension that helps users find discounts and deals).

5. Strong Partnerships:

PayPal has formed strategic partnerships with major e-commerce platforms, payment processors, and financial institutions. These collaborations enhance the reach and convenience of its services, as well as drive transaction volume.

6. Mobile-Centric Approach:

Recognizing the increasing reliance on mobile devices, PayPal has invested in creating user-friendly mobile applications for seamless mobile payments and money transfers. Its subsidiary, Venmo, has become especially popular among younger users for peer-to-peer payments.

7. Financial Performance:

PayPal's financial performance has shown consistent growth over the years. The company's revenue and net income have been steadily increasing, driven by the growing adoption of online and mobile payments, as well as expansion into new markets and services.

8. Innovation and Technology:

PayPal remains at the forefront of financial technology innovation. The company has explored blockchain technology and cryptocurrencies, allowing users to buy, hold, and sell select cryptocurrencies through their PayPal accounts.

9. Regulatory and Compliance Considerations:

Operating in the financial services industry, PayPal is subject to various regulatory and compliance requirements. Adhering to these standards is essential for maintaining trust and securing user data.

10. Competitive Landscape:

The digital payment industry is highly competitive, with players like Square, Stripe, and traditional financial institutions vying for market share. PayPal's ability to innovate, adapt to changing trends, and offer seamless user experiences contributes to its competitive advantage.

In summary, PayPal is a pivotal player in the digital payments landscape, offering a wide range of services that facilitate online transactions and money transfers. Its user base, partnerships, technological innovation, and strategic acquisitions have propelled its growth and solidified its position in the industry. However, like any company, PayPal faces challenges related to competition, regulatory changes, and cybersecurity. Staying ahead of these challenges through continuous innovation and customer-focused services will be crucial to its sustained success.

PYPL | Buy the Fear!!! | LONGPayPal Holdings, Inc. operates a technology platform that enables digital payments on behalf of merchants and consumers worldwide. The company provides payment solutions under the PayPal, PayPal Credit, Braintree, Venmo, Xoom, PayPal Zettle, Hyperwallet, PayPal Honey, and Paidy names. Its payments platform allows consumers to send and receive payments in approximately 200 markets and in approximately 150 currencies, withdraw funds to their bank accounts in 56 currencies, and hold balances in their PayPal accounts in 25 currencies. The company was founded in 1998 and is headquartered in San Jose, California.

Paypal falling wedgeOn the Weekly, I see a falling wedge on PYPL NASDAQ:PYPL #PYPL forming a bullish divergence. marked with a yellow resistance trendline that ones it brakes we will be in an uptrend. till then we have to continue to see how low this falling wedge drops. key levels marked.

What does Paypal USD mean for Eth ? Will we have a McDollar ??Paypal launches PYUSD

This does not mean it will get adoption just because Paypal wants it to. There may be regulatory hurdles incoming just as we saw with Libra and Diem for FB // Meta. This is now a clear trend though where larger traditional companies are seeing the immense upside in their own stablecoin products. I dont think this trend is going to die out.

Where does it go ?

I think this is leading to a McDollar. Just as Big Mac index is a good rule of thumb for judging currencies.. a McDollar is a good option for currency itself. Goods or services in demand can be digitalised into currency on the back of the traditional product. This is great for provider and customer both. Prosperity is about speed. From the wheel to the sail to the car to the internet. Moving things (people//stuff) faster is compounding the human ability to create more together. Prosperity.

Can Eth handle it ?

I believe so. There are many "eth killers" now and there'll likely be more popping up esp by more traditional outfits. At this stage though what Ethereum has done to compete well against crypto competitors is add layers with utility related to their core layer flaws. Rollup technology allows Eth to outsource the heavy lifting of smaller transactions. Rather than individual $3 nfts clogging the network one by one we are likely to see places like Paypal use rollup technology to bundle microtransactions and send them thru the network that way. This will reduce costs involved and increase time to settle for everyone.

PAYPALNASDAQ:PYPL testing its spring before leaving it.

SO this stocks gonna fly up ,

This IDea base on Wyckoff accumulation,

Were on PHASE C that spring must be testing.

Are we gonna see NASDAQ:PYPL FLy upto 178$ per share?

What is your thought?

This is not a financial advice...